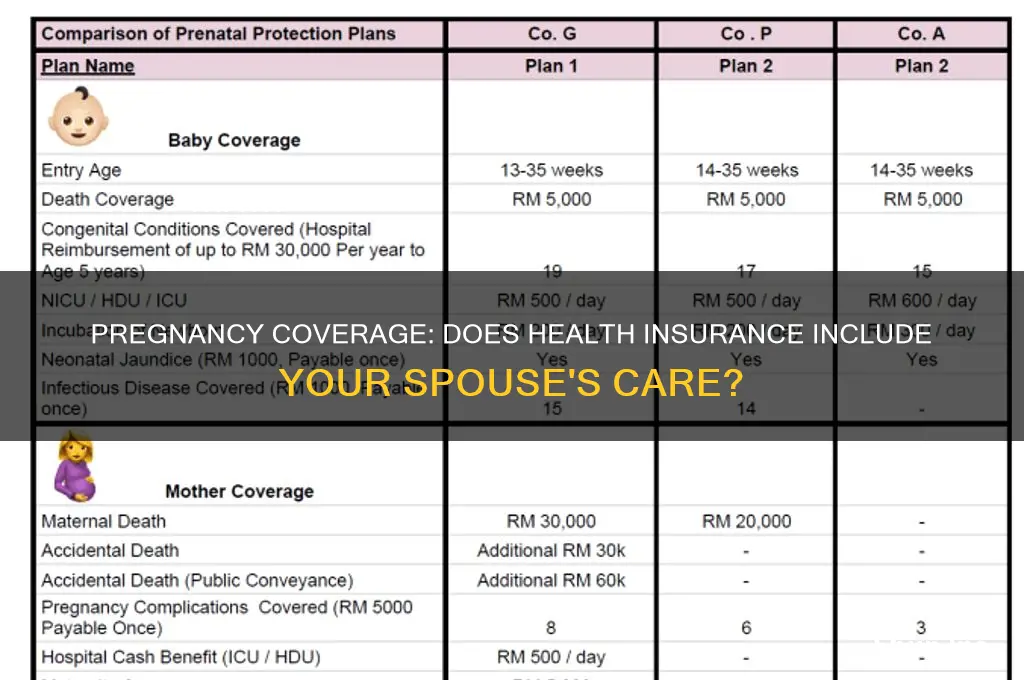

Navigating health insurance coverage for a pregnant spouse can be a critical concern for many families, as the costs associated with prenatal care, delivery, and postpartum care can be substantial. Most health insurance plans in the United States, including employer-sponsored plans and those purchased through the Health Insurance Marketplace, are required by the Affordable Care Act (ACA) to cover pregnancy and maternity care as part of the essential health benefits. This typically includes prenatal visits, ultrasounds, labor and delivery, and postpartum care for both the mother and newborn. However, the extent of coverage, including deductibles, copayments, and out-of-pocket maximums, can vary significantly between plans, so it’s essential to review your specific policy details or consult with your insurance provider to understand what is covered and any potential costs you may incur. Additionally, some plans may offer additional benefits, such as breastfeeding support or childbirth classes, which can further support the health and well-being of both mother and baby.

| Characteristics | Values |

|---|---|

| Coverage for Pregnant Spouse | Most health insurance plans cover pregnancy-related care for the spouse. |

| Prenatal Care | Typically covered, including doctor visits, ultrasounds, and lab tests. |

| Delivery and Hospitalization | Covered, including vaginal delivery, C-section, and postnatal care. |

| Maternity Benefits | Often included, but specifics vary by plan (e.g., breastfeeding support). |

| Pre-existing Pregnancy Coverage | May not be covered if the pregnancy began before the policy effective date. |

| Waiting Period | Some plans have a waiting period (e.g., 9-12 months) for maternity coverage. |

| Out-of-Pocket Costs | Copays, deductibles, and coinsurance may apply depending on the plan. |

| Newborn Coverage | Newborns are typically covered under the mother’s policy for 30 days. |

| Specialized Care | High-risk pregnancy care may be covered but requires prior authorization. |

| Policy Type | Employer-sponsored, individual, or marketplace plans may differ in coverage. |

| State Regulations | Some states mandate maternity coverage in all health insurance plans. |

| International Coverage | Limited; pregnancy care abroad may not be covered unless specified. |

| Exclusions | Fertility treatments and elective procedures may not be covered. |

| Network Restrictions | In-network providers are typically required for full coverage. |

| Policy Renewal | Coverage continues after pregnancy but may change during open enrollment. |

| Tax Benefits | Pregnancy expenses may qualify for tax deductions or HSA/FSA use. |

Explore related products

What You'll Learn

- Coverage for Prenatal Care: Includes regular check-ups, ultrasounds, and lab tests during pregnancy

- Maternity Hospitalization: Covers delivery costs, including cesarean sections and postnatal care

- Newborn Baby Coverage: Some plans include care for the baby immediately after birth

- Pre-existing Pregnancy: Policies may exclude coverage if pregnancy began before enrollment

- Complications Coverage: Includes treatment for pregnancy-related complications like gestational diabetes or preeclampsia

![]()

Coverage for Prenatal Care: Includes regular check-ups, ultrasounds, and lab tests during pregnancy

Prenatal care is a cornerstone of a healthy pregnancy, encompassing regular check-ups, ultrasounds, and lab tests that monitor both maternal and fetal well-being. Most health insurance plans, including those covering a pregnant spouse, include these essential services as part of their maternity benefits. However, the extent of coverage can vary widely depending on the policy, provider, and geographic location. For instance, while some plans may fully cover routine prenatal visits, others might require co-pays or limit the number of ultrasounds allowed. Understanding these nuances is critical to avoiding unexpected costs and ensuring comprehensive care throughout pregnancy.

Regular check-ups, typically scheduled monthly during the first and second trimesters and biweekly or weekly in the third trimester, are vital for tracking the mother’s health and the baby’s development. These visits often include blood pressure checks, weight monitoring, and discussions about nutrition and lifestyle adjustments. Lab tests, such as blood work to screen for anemia, gestational diabetes, and infectious diseases, are also standard components of prenatal care. For example, the glucose tolerance test, usually performed between 24 and 28 weeks, helps identify gestational diabetes, a condition affecting up to 10% of pregnancies. Insurance plans generally cover these tests, but it’s essential to verify if any specific procedures require pre-authorization.

Ultrasounds, another critical aspect of prenatal care, provide visual insights into fetal growth, position, and potential abnormalities. Most pregnancies involve at least two ultrasounds: one in the first trimester to confirm viability and due date, and another around 18–22 weeks for anatomical evaluation. Additional ultrasounds may be recommended for high-risk pregnancies or complications. While most insurance plans cover these scans, some may impose restrictions, such as limiting 3D or 4D ultrasounds to medical necessity. Pregnant individuals should review their policy details or consult their insurer to clarify coverage limits and potential out-of-pocket expenses.

A practical tip for maximizing prenatal care coverage is to choose healthcare providers within your insurance network. Out-of-network services, including specialist consultations or diagnostic tests, can significantly increase costs even if the procedure itself is covered. Additionally, consider enrolling in supplemental insurance or health savings accounts (HSAs) to offset potential expenses not fully covered by your primary plan. Finally, keep detailed records of all prenatal appointments, tests, and communications with your insurer—this documentation can be invaluable if disputes arise regarding coverage or billing.

In summary, prenatal care coverage for a pregnant spouse typically includes regular check-ups, ultrasounds, and lab tests, but the specifics depend on the insurance plan. By understanding policy details, staying within network providers, and proactively managing potential costs, couples can ensure comprehensive care without financial strain. Prenatal care is not just a medical necessity—it’s an investment in the health and future of both parent and child.

Amethyst Birth Control Coverage: What Your Health Insurance May Offer

You may want to see also

Explore related products

![]()

Maternity Hospitalization: Covers delivery costs, including cesarean sections and postnatal care

Maternity hospitalization coverage is a critical component of health insurance plans, particularly for expectant parents. This coverage typically includes delivery costs, whether it’s a vaginal birth or a cesarean section, as well as postnatal care for both the mother and the newborn. Understanding the specifics of this coverage can alleviate financial stress during a time that should be focused on health and family. For instance, cesarean sections, which account for approximately 32% of deliveries in the U.S., can cost upwards of $20,000 without insurance, making comprehensive coverage essential.

When evaluating a health insurance plan, scrutinize the details of maternity hospitalization benefits. Most plans cover prenatal visits, labor and delivery, and postnatal care, but the extent of coverage varies. For example, some policies may limit the number of postnatal days covered in the hospital, typically ranging from 48 hours for vaginal deliveries to 96 hours for cesarean sections. Additionally, check if the plan includes neonatal intensive care unit (NICU) expenses, which can arise unexpectedly and are often excluded in basic policies. Practical tip: Review the Summary of Benefits and Coverage (SBC) document provided by your insurer to identify any gaps in maternity care.

A comparative analysis reveals that employer-sponsored plans often offer more robust maternity hospitalization coverage than individual market plans. For instance, under the Affordable Care Act (ACA), all marketplace plans must include maternity care as an essential health benefit, but employer plans may provide additional perks like private rooms or extended postnatal stays. However, ACA-compliant plans still vary in their cost-sharing structures, with some requiring higher deductibles or copays for maternity services. Caution: Be wary of short-term health plans, which often exclude maternity care altogether, leaving families vulnerable to high out-of-pocket costs.

Persuasively, investing in a plan with comprehensive maternity hospitalization coverage is not just a financial decision but a health one. Adequate coverage ensures access to necessary medical interventions, such as emergency cesarean sections, which can be lifesaving for both mother and child. Postnatal care is equally vital, as it addresses complications like postpartum hemorrhage or infection, which affect 1 in 10 women globally. For expectant fathers or partners, understanding this coverage also means being prepared to support their spouse through the financial and emotional aspects of childbirth.

Finally, a descriptive approach highlights the peace of mind that comes with knowing delivery costs are covered. Imagine a scenario where a couple welcomes their first child via an unplanned cesarean section. Without insurance, they could face bills exceeding $50,000. With comprehensive maternity hospitalization coverage, their focus remains on bonding with their newborn rather than navigating medical debt. This underscores the importance of proactively selecting a plan that prioritizes maternity care, ensuring a smoother transition into parenthood.

Gender Disparity in Health Insurance: Who's More Covered, Men or Women?

You may want to see also

Explore related products

$27.89 $30.99

$12.81 $14.99

![]()

Newborn Baby Coverage: Some plans include care for the baby immediately after birth

Newborn baby coverage is a critical yet often overlooked aspect of health insurance plans, especially when considering coverage for a pregnant spouse. Many plans automatically extend coverage to the newborn for the first 30 days of life, but the specifics can vary widely. For instance, some policies may require you to add the baby to the plan within 30 days to avoid gaps in coverage, while others might offer seamless integration from birth. Understanding these nuances is essential to ensure your newborn receives immediate medical care without unexpected out-of-pocket costs.

From an analytical perspective, the inclusion of newborn coverage in health insurance plans reflects a broader recognition of the immediate healthcare needs of infants. Newborns often require routine check-ups, vaccinations, and sometimes specialized care within the first few weeks of life. Plans that cover these services immediately after birth can significantly reduce financial stress for new parents. However, it’s crucial to review the plan’s details, as some may limit coverage to specific providers or exclude certain procedures, such as neonatal intensive care, unless explicitly added.

For parents navigating this process, here’s a practical step-by-step guide: First, contact your insurance provider as soon as possible after the birth to notify them and initiate the enrollment process for your baby. Second, verify what services are covered under the newborn clause, including well-baby visits, immunizations, and emergency care. Third, if your plan requires formal enrollment within 30 days, set a reminder to complete the necessary paperwork to avoid coverage lapses. Finally, keep detailed records of all communications and submissions to resolve any potential disputes later.

Comparatively, plans without automatic newborn coverage often require parents to purchase additional policies or extensions, which can be costly and time-consuming. In contrast, comprehensive plans that include immediate newborn care tend to offer better value, particularly for families anticipating multiple births or potential complications. For example, a plan with a $500 deductible and 80% coverage for neonatal care could save thousands of dollars compared to paying out-of-pocket for unexpected hospital stays.

Persuasively, opting for a plan with robust newborn coverage is not just a financial decision but a proactive step toward ensuring your child’s health from day one. The first few weeks of life are crucial for developmental assessments and early interventions, which can have long-term benefits. By choosing a plan that prioritizes newborn care, you’re investing in your child’s future while safeguarding your family’s financial stability during an already expensive life event. Always compare plans carefully, considering both immediate and long-term needs, to make an informed choice.

Indiana Insurance for Kids: Application Process Simplified

You may want to see also

Explore related products

$38.99 $41.99

![]()

Pre-existing Pregnancy: Policies may exclude coverage if pregnancy began before enrollment

Pregnancy is a life-changing event, but for many, the joy can be tempered by the complexities of health insurance coverage. A critical yet often overlooked detail is the concept of pre-existing pregnancy—a term that can significantly impact your spouse’s coverage if the pregnancy began before enrolling in a new health insurance plan. This exclusion is rooted in the insurance industry’s classification of pregnancy as a pre-existing condition when it predates policy enrollment, potentially leaving families with unexpected out-of-pocket expenses. Understanding this nuance is essential for anyone navigating health insurance during pregnancy.

Consider this scenario: Your spouse discovers she’s pregnant, and shortly after, you switch jobs, requiring a change in health insurance. If the pregnancy began before the new policy’s effective date, the insurer may exclude maternity care, prenatal visits, and even childbirth-related expenses from coverage. This exclusion isn’t universal—some states and plans offer protections—but it’s a common enough practice to warrant careful scrutiny. For instance, under the Affordable Care Act (ACA), pregnancy is no longer considered a pre-existing condition for denying coverage, but the timing of enrollment can still affect what’s covered.

To avoid this pitfall, take proactive steps. First, review your current and prospective insurance policies for clauses related to pre-existing conditions and pregnancy coverage. If you’re switching plans, coordinate the transition to ensure there’s no gap in coverage. For example, if your spouse is already pregnant, consider maintaining the current plan until the pregnancy concludes, even if it means paying COBRA premiums temporarily. Alternatively, if you must switch, look for plans with explicit maternity coverage or those compliant with ACA standards, which prohibit denying coverage for pre-existing conditions but may still have waiting periods.

A comparative analysis reveals that employer-sponsored plans often provide more comprehensive maternity coverage than individual plans, especially for pre-existing pregnancies. However, individual plans purchased through state or federal marketplaces may offer subsidies that offset higher premiums. For instance, a family earning up to 400% of the federal poverty level ($111,000 for a family of four in 2023) may qualify for premium tax credits, making ACA-compliant plans more affordable. Additionally, some states, like California and New York, have stricter regulations requiring all plans to cover maternity care regardless of when the pregnancy began.

In conclusion, while the exclusion of pre-existing pregnancy from coverage is a potential hurdle, it’s not insurmountable. By understanding the specifics of your policy, planning transitions carefully, and leveraging available resources, you can ensure your spouse and unborn child receive the care they need. Always consult with an insurance broker or healthcare navigator to explore all options and avoid costly surprises. Pregnancy should be a time of anticipation, not anxiety over insurance gaps.

Understanding Insurance Premium Costs Within Medical Expenses

You may want to see also

Explore related products

![]()

Complications Coverage: Includes treatment for pregnancy-related complications like gestational diabetes or preeclampsia

Pregnancy-related complications can arise unexpectedly, even in healthy individuals, making complications coverage a critical component of health insurance for expectant spouses. Conditions like gestational diabetes and preeclampsia require prompt medical intervention to safeguard both maternal and fetal health. For instance, gestational diabetes, which affects approximately 6-9% of pregnancies in the U.S., necessitates regular glucose monitoring, dietary adjustments, and sometimes insulin therapy. Without insurance coverage, these treatments can impose significant financial strain, potentially delaying care and worsening outcomes.

When evaluating health insurance plans, scrutinize the specifics of complications coverage. Some policies may cover diagnostic tests, such as glucose tolerance tests for gestational diabetes, but exclude specialized care like endocrinologist consultations or continuous glucose monitoring devices. Preeclampsia, a severe condition marked by high blood pressure and organ damage, often requires hospitalization and medications like magnesium sulfate to prevent seizures. Ensure the plan covers inpatient care, emergency services, and prescription drugs, as these are essential for managing acute complications.

A comparative analysis of plans reveals that while most comprehensive health insurance policies include complications coverage, the extent varies. HMOs may require referrals for specialist care, while PPOs offer more flexibility but at a higher cost. For example, a PPO plan might cover 80% of out-of-network specialist visits for preeclampsia management, whereas an HMO may limit coverage to in-network providers. Additionally, some plans cap coverage for high-risk pregnancies, leaving families vulnerable to out-of-pocket expenses. Always review the policy’s exclusions and limitations to avoid surprises.

To maximize complications coverage, take proactive steps during enrollment. Verify that prenatal care, including screenings for complications, is fully covered under preventive services. Keep detailed records of all medical visits and prescriptions, as these may be required for claims processing. If complications arise, consult with your insurer immediately to confirm coverage for recommended treatments. For instance, if gestational diabetes requires insulin, confirm the specific brands covered and any prior authorization requirements. Finally, consider supplemental insurance or health savings accounts (HSAs) to offset potential gaps in coverage.

In conclusion, complications coverage is not just a benefit—it’s a necessity for pregnant spouses. By understanding the nuances of what’s covered, from diagnostic tests to specialized treatments, families can navigate pregnancy with financial security and peace of mind. Always prioritize plans that offer comprehensive, transparent coverage for pregnancy-related complications, ensuring timely access to the care needed for a healthy outcome.

Kaiser Health Insurance Birth Control Coverage: What You Need to Know

You may want to see also

Frequently asked questions

Yes, most health insurance plans cover pregnancy and maternity care for a spouse if they are added to the policy. However, coverage details may vary, so it’s important to review your plan’s benefits, including prenatal care, delivery, and postpartum care.

While many health insurance plans cover essential pregnancy-related services, some expenses like specialized treatments or elective procedures may not be fully covered. Check your policy for exclusions, copays, deductibles, and out-of-pocket maximums.

Adding a pregnant spouse to your health insurance plan after pregnancy may be subject to open enrollment or qualifying life event rules. Some plans may consider pregnancy a pre-existing condition if added outside these periods, so it’s best to enroll during open enrollment or within the allowed timeframe after marriage.