The question of whether a health insurance penalty qualifies as a civil penalty is a nuanced legal issue that intersects tax law, healthcare policy, and administrative regulations. Under the Affordable Care Act (ACA), individuals who fail to maintain minimum essential health coverage may face a financial penalty, historically collected through federal tax returns. While this penalty is often referred to as a tax, its classification as a civil penalty has been debated, particularly following the Supreme Court’s ruling in *National Federation of Independent Business v. Sebelius* (2012), which upheld the penalty as a tax under Congress’s taxing authority. However, subsequent legislative changes, such as the Tax Cuts and Jobs Act of 2017, reduced the penalty to $0 at the federal level, shifting the focus to state-level mandates and their enforcement mechanisms. Determining whether such penalties are civil in nature involves examining their purpose—whether they are punitive or remedial—and their enforcement framework, which typically falls under administrative or judicial processes rather than criminal proceedings. This distinction is critical for understanding the legal implications, including potential challenges to enforcement and the rights of individuals subject to these penalties.

Explore related products

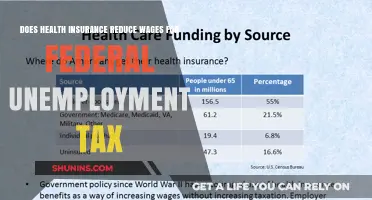

What You'll Learn

![]()

Definition of Civil Penalty

A civil penalty is a monetary fine imposed by a government agency or regulatory body for violations of laws or regulations, distinct from criminal penalties. Unlike criminal penalties, which often involve incarceration and are punitive in nature, civil penalties are primarily remedial and aim to enforce compliance rather than punish wrongdoing. They are typically levied against individuals, businesses, or organizations that fail to adhere to specific legal requirements, such as environmental regulations, financial reporting standards, or healthcare mandates. For instance, the Affordable Care Act (ACA) includes a penalty for individuals who do not maintain health insurance coverage, which is enforced by the Internal Revenue Service (IRS) as a tax assessment. This raises the question: does the health insurance penalty qualify as a civil penalty?

To determine whether the health insurance penalty under the ACA counts as a civil penalty, it’s essential to examine its characteristics. Civil penalties are generally imposed through administrative proceedings rather than criminal courts, and they are often tied to specific statutory violations. The ACA’s penalty, known as the individual shared responsibility payment, was designed to encourage compliance with the mandate to have health insurance. It was collected by the IRS alongside federal tax returns, aligning with the administrative enforcement typical of civil penalties. However, in 2017, the Tax Cuts and Jobs Act reduced the penalty to $0, effectively eliminating it as of 2019, though some states have since reinstated similar penalties at the state level.

One key distinction between civil penalties and other types of fines lies in their purpose. Civil penalties are not intended to be punitive but rather to deter non-compliance and promote adherence to the law. For example, the health insurance penalty was structured to offset the costs of uncompensated care and stabilize insurance markets by ensuring a broad risk pool. This contrasts with criminal penalties, which serve to punish offenders and deter future criminal behavior. Additionally, civil penalties often include mechanisms for appeal or mitigation, allowing individuals or entities to contest the fine or negotiate a reduced amount based on their circumstances.

Practical considerations also play a role in understanding civil penalties. For individuals facing the health insurance penalty, it’s crucial to know that it is assessed based on income and the number of months without coverage. Prior to its elimination, the penalty was calculated as a percentage of household income or a flat fee, whichever was higher, with caps in place to prevent excessive financial burden. For example, in 2018, the penalty was $695 per adult or 2.5% of household income, up to a maximum of the national average bronze-level premium. Understanding these specifics helps individuals assess their potential liability and take steps to avoid penalties, such as enrolling in qualifying health coverage.

In conclusion, the health insurance penalty under the ACA shares key characteristics with civil penalties, including its administrative enforcement, remedial purpose, and focus on compliance. While its elimination at the federal level has shifted the landscape, state-level penalties continue to operate under similar principles. For those navigating these regulations, recognizing the nature of civil penalties—their purpose, structure, and practical implications—is essential for informed decision-making and compliance with healthcare mandates.

Understanding the Reasons Behind Your Insurance Premium Rate Hike

You may want to see also

Explore related products

![]()

Health Insurance Mandate Rules

The Affordable Care Act (ACA) introduced a shared responsibility provision, colloquially known as the individual mandate, which required most Americans to maintain minimum essential health coverage or face a financial penalty. This penalty, often referred to as the "individual shared responsibility payment," was a central component of the ACA's strategy to expand healthcare coverage. The question of whether this penalty constitutes a civil penalty is nuanced, hinging on legal interpretations and the mechanism through which it was enforced. Initially, the penalty was collected by the Internal Revenue Service (IRS) as part of federal tax filings, blurring the line between a tax and a civil penalty. However, the Tax Cuts and Jobs Act of 2017 reduced the penalty to $0 starting in 2019, effectively eliminating it at the federal level, though some states have since implemented their own mandates and penalties.

Analyzing the nature of the health insurance penalty reveals its hybrid characteristics. Legally, the Supreme Court upheld the ACA's individual mandate in *National Federation of Independent Business v. Sebelius* (2012) by classifying the penalty as a tax, not a civil penalty. This distinction was pivotal because it allowed the mandate to fall under Congress's taxing authority rather than its power to regulate interstate commerce. However, the penalty's enforcement through the IRS and its purpose—to encourage compliance with the mandate—align more closely with the attributes of a civil penalty, which is typically designed to coerce behavior rather than generate revenue. This duality complicates its categorization, leaving room for debate among legal scholars and policymakers.

For individuals navigating health insurance mandate rules, understanding the implications of non-compliance is crucial. Prior to 2019, those without qualifying coverage faced a penalty calculated as a percentage of household income (2.5% of income or a flat fee, whichever was higher) or a per-person fee ($695 per adult and $347.50 per child, up to a family maximum of $2,085 in 2017). Exemptions existed for financial hardships, religious objections, and certain coverage gaps of less than three months. Today, while the federal penalty has been eliminated, states like California, New Jersey, and Massachusetts have enacted their own mandates with penalties structured similarly to the former federal model. Residents in these states must carefully review their state's rules to avoid fines, which can be substantial.

A comparative analysis of federal and state-level mandates highlights the evolving landscape of health insurance enforcement. Federally, the shift from a penalty-based system to one reliant on incentives and subsidies reflects a policy pivot toward voluntary compliance. In contrast, states with active mandates continue to use penalties as a tool to maintain coverage levels and stabilize insurance markets. For instance, California's penalty for 2023 is modeled after the pre-2019 federal structure, while Massachusetts employs a unique approach by tying penalties to the cost of the state's minimum credible coverage plan. This diversity underscores the importance of locality-specific knowledge when assessing compliance obligations.

Practically, individuals should take proactive steps to ensure adherence to health insurance mandate rules. First, verify whether your state has an active mandate and understand its specific requirements. Second, explore available exemptions, such as those for low income or membership in certain indigenous tribes. Third, consider enrolling in a qualifying health plan during open enrollment periods to avoid penalties. For those in states without mandates, maintaining coverage remains advisable to avoid gaps in care and potential out-of-pocket costs. Finally, stay informed about legislative changes, as healthcare policies can shift rapidly, impacting both federal and state-level requirements. By staying vigilant and informed, individuals can navigate the complexities of health insurance mandates effectively.

Missouri's Health Insurance: Exploring Free Coverage Options and Eligibility

You may want to see also

Explore related products

![]()

Tax vs. Penalty Classification

The distinction between a tax and a penalty is not merely semantic but carries significant legal and financial implications, especially in the context of health insurance mandates. At the heart of this classification lies the purpose and effect of the charge: is it a revenue-raising measure or a punitive action to enforce compliance? The U.S. Supreme Court’s ruling in *National Federation of Independent Business v. Sebelius* (2012) provides a landmark example. The Court upheld the Affordable Care Act’s individual mandate as a constitutional exercise of Congress’s taxing power, reclassifying the "penalty" for lacking health insurance as a tax. This decision hinged on the fact that the charge was collected by the IRS, lacked punitive characteristics such as scienter (intent), and was designed to offset the costs of uncompensated care rather than punish noncompliance.

To classify a charge as a tax, it must meet specific criteria. First, it should be tied to a legitimate government interest, such as funding public programs or offsetting societal costs. For instance, the health insurance "tax" under the ACA was structured to generate revenue to support the expansion of healthcare coverage. Second, the amount assessed should be proportional to the activity being taxed, rather than escalating based on repeated violations. In contrast, penalties are typically punitive, aiming to deter behavior through financial consequences that increase with repeated offenses. For example, a civil penalty for environmental violations might double or triple for each subsequent infraction, whereas a tax remains consistent regardless of compliance history.

When evaluating whether a health insurance penalty qualifies as a civil penalty, consider its enforcement mechanism and intent. Civil penalties are often enforced through administrative or judicial proceedings and may include additional remedies like injunctions or license revocations. Taxes, however, are generally collected through routine processes, such as payroll deductions or annual filings. For individuals under 30, the ACA allowed for a "young invincibles" exemption, permitting the purchase of a lower-cost catastrophic plan instead of paying the tax. This exception underscores the revenue-focused nature of the charge, as it provided an alternative means of compliance rather than imposing a punitive fine.

Practically, understanding this classification matters for financial planning and legal strategy. If a charge is deemed a tax, it may be deductible under certain circumstances, such as when itemizing deductions on federal tax returns. Conversely, penalties are rarely tax-deductible and may trigger additional legal consequences. For employers, misclassifying a penalty as a tax could result in underpayment of obligations, leading to audits or fines. To navigate this complexity, consult IRS Publication 518 or seek guidance from a tax professional, especially if you operate in industries with overlapping tax and penalty structures, such as healthcare or environmental compliance.

In conclusion, the tax vs. penalty classification is a nuanced issue with far-reaching implications. By examining purpose, structure, and enforcement, individuals and businesses can better understand their obligations and rights. Whether you’re a 25-year-old considering catastrophic coverage or a small business owner navigating ACA requirements, clarity on this distinction ensures compliance and minimizes financial risk. As legislative landscapes evolve, staying informed remains the best defense against unintended consequences.

Affordable Health Insurance in Kansas: Tips to Find the Best Deals

You may want to see also

Explore related products

![]()

ACA Penalty Enforcement

The Affordable Care Act (ACA) introduced a shared responsibility provision, often referred to as the individual mandate, which required most Americans to have health insurance or pay a penalty. This penalty, formally known as the "individual shared responsibility payment," was a key enforcement mechanism to encourage compliance. The question of whether this penalty qualifies as a civil penalty is nuanced, as it straddles the line between a tax and a punitive measure. The Supreme Court’s ruling in *National Federation of Independent Business v. Sebelius* (2012) upheld the mandate by classifying the payment as a tax, not a penalty, for constitutional purposes. However, for enforcement and collection, the IRS treated it as a tax liability, which complicates its categorization under civil penalty frameworks.

Enforcement of the ACA penalty involved a structured process. Individuals who lacked qualifying health coverage for more than a short gap (typically three months) were required to make the payment when filing their federal income taxes. The penalty amount was calculated as the greater of a flat dollar amount per adult and child or a percentage of household income above the filing threshold. For example, in 2018, the last year the penalty was in effect, the flat rate was $695 per adult and $347.50 per child, up to a maximum of $2,085 per family, or 2.5% of household income over the tax return filing threshold. This dual calculation ensured the penalty was proportional to both income and family size, balancing fairness and deterrence.

Despite its design, the ACA penalty faced challenges in enforcement. The IRS lacked the authority to use traditional collection methods, such as liens or levies, for nonpayment. Instead, it relied on offsetting refunds to recover unpaid penalties. This limitation reduced the penalty’s effectiveness as a deterrent, particularly for individuals who did not expect tax refunds. Additionally, the Tax Cuts and Jobs Act of 2017 reduced the penalty to $0 starting in 2019, effectively eliminating it as an enforcement tool. However, some states, like California and New Jersey, reintroduced their own mandates and penalties to maintain coverage requirements, highlighting the ongoing debate over the role of penalties in healthcare policy.

From a legal standpoint, the ACA penalty’s classification as a civil penalty remains ambiguous. While it shared characteristics with civil penalties—such as being imposed for noncompliance with a legal requirement—its treatment as a tax for constitutional and administrative purposes distinguishes it. Civil penalties typically involve explicit punitive intent, administrative adjudication, and potential appeals processes, which were not fully applicable to the ACA penalty. This ambiguity underscores the complexity of blending tax policy with regulatory enforcement in healthcare, leaving room for interpretation in future legislative and judicial contexts.

For individuals and policymakers, understanding the ACA penalty’s enforcement mechanisms provides valuable insights into the challenges of incentivizing compliance. While the federal penalty is no longer in effect, its legacy informs ongoing discussions about the role of financial penalties in healthcare policy. States with their own mandates offer a testing ground for alternative enforcement strategies, such as higher penalties or stricter collection methods. Practical tips for compliance include verifying coverage eligibility, exploring exemptions (e.g., for low income or religious objections), and staying informed about state-specific requirements. As the healthcare landscape evolves, the lessons from ACA penalty enforcement remain relevant for designing effective and equitable policies.

Understanding the Cost of Forgoing Medical Insurance

You may want to see also

Explore related products

![]()

Legal Precedents and Cases

The question of whether health insurance penalties qualify as civil penalties has been a subject of legal scrutiny, with several cases shaping the interpretation of such penalties under U.S. law. One pivotal case is *National Federation of Independent Business v. Sebelius* (2012), where the Supreme Court examined the Affordable Care Act’s individual mandate. The Court characterized the penalty for not purchasing health insurance as a tax rather than a civil penalty, reasoning that it was collected by the IRS and lacked traditional punitive characteristics. This decision hinged on the penalty’s structure, which was designed to encourage compliance through financial incentives rather than punishment.

In contrast, *California v. Texas* (2021) revisited the ACA’s penalty structure after Congress reduced the individual mandate penalty to $0 in 2017. The Supreme Court dismissed the case on standing grounds, avoiding a direct ruling on whether the penalty remained a tax or transformed into a civil penalty. However, the Court’s earlier reasoning in *NFIB v. Sebelius* suggests that the absence of a financial penalty weakens the argument for classifying it as a civil penalty, as there is no longer a coercive mechanism in place.

Another relevant case is *United States v. Sotirios (2016)*, where a federal court addressed whether penalties under the ACA could be discharged in bankruptcy as civil penalties. The court ruled that they could not, emphasizing that the ACA penalties were not punitive in nature but rather served as a means to offset the cost of uncompensated care. This decision underscores the importance of legislative intent in distinguishing between civil penalties and other financial obligations.

From these cases, a key takeaway emerges: the classification of health insurance penalties as civil penalties depends on their purpose, enforcement mechanism, and legislative intent. Penalties designed to raise revenue or offset costs are less likely to be considered civil penalties, while those with punitive or coercive elements may meet the criteria. For individuals and businesses navigating this issue, understanding these legal precedents is crucial for compliance and strategic planning.

Practically, when assessing whether a health insurance penalty applies to your situation, consider the following steps: 1) Review the specific language of the penalty in the relevant statute or regulation. 2) Examine how the penalty is enforced—is it collected by a tax agency or a regulatory body? 3) Evaluate the penalty’s purpose—is it to punish non-compliance or to offset costs? By applying these criteria, you can better determine whether the penalty aligns with the legal definition of a civil penalty and take appropriate action.

State Farm Life Insurance: Medical Exam Needed?

You may want to see also

Frequently asked questions

Yes, the health insurance penalty under the ACA, also known as the individual shared responsibility payment, is considered a civil penalty rather than a tax.

The health insurance penalty is enforced through the IRS, which can withhold the amount owed from tax refunds but cannot use more aggressive collection methods like liens or levies, as it is a civil penalty.

Generally, civil penalties are not dischargeable in bankruptcy. However, since the ACA penalty is no longer assessed as of 2019 (due to the Tax Cuts and Jobs Act reducing it to $0), this question is largely moot for current cases.

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UY218_.jpg)

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UY218_.jpg)

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UY218_.jpg)

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UY218_.jpg)

![TurboTax Business Desktop Edition 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UY218_.jpg)