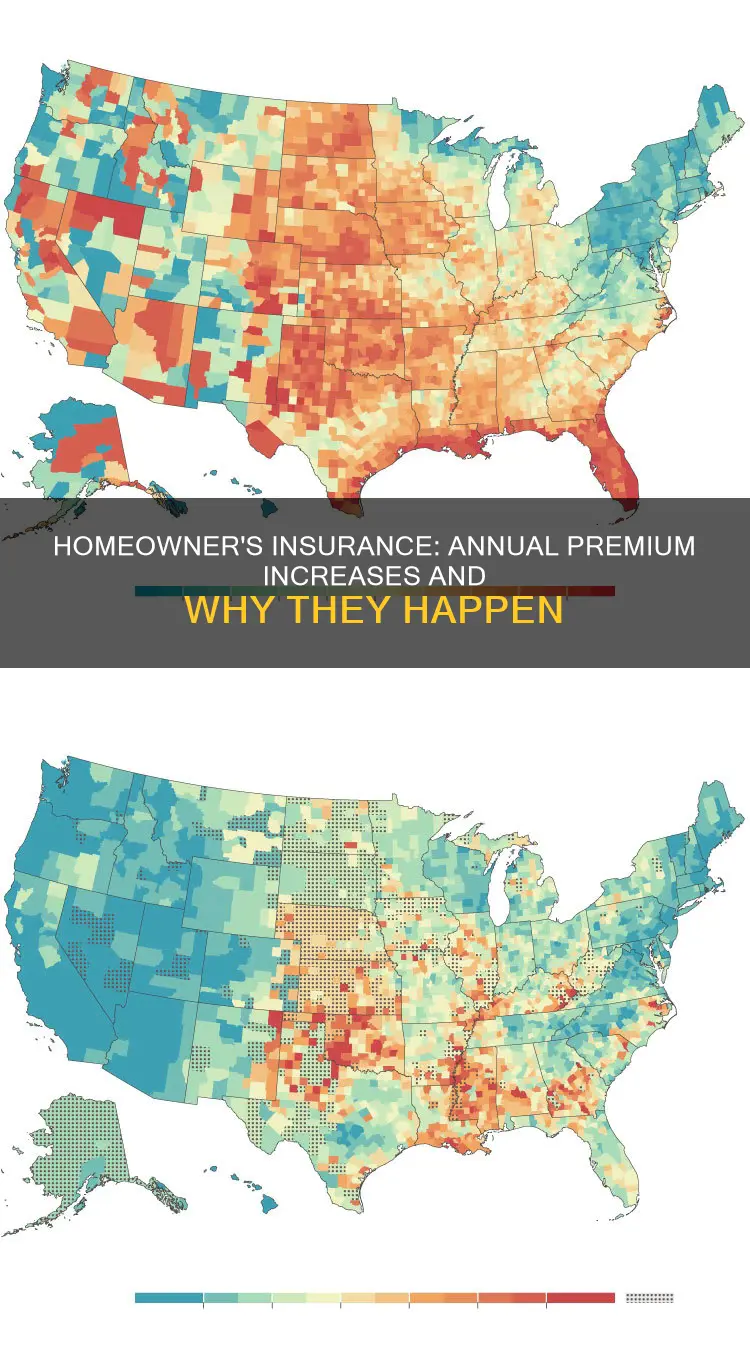

Homeowner's insurance premiums have been rising sharply in recent years, with several factors contributing to this increase. One of the primary reasons is the impact of climate change, leading to more frequent and severe weather events such as hurricanes, floods, droughts, and wildfires. These events have resulted in costly insurance claims and driven up the cost of repairs due to increasing construction and building material costs. Inflation is another significant factor, as insurance companies raise rates to keep up with the rising costs of replacing homes and belongings. Additionally, factors such as individual claims, property value increases, and credit history can also contribute to annual premium adjustments. While some years may see more significant increases than others, it is typical for homeowner's insurance premiums to rise gradually over time.

| Characteristics | Values |

|---|---|

| Does homeowner's insurance typically go up each year? | Yes |

| Reasons for increase | Inflation, increased property value, claims, severe weather events, rising cost of building materials, supply chain issues, unfilled jobs, reinsurance, weak regulatory oversight, natural disasters, location, credit history, bundling policies, safety features |

| Average increase | 0-7% |

| Ways to save | Bundling policies, going paperless, safety features, shopping around |

Explore related products

What You'll Learn

![]()

Inflation and rising costs of materials

Inflation and the rising costs of materials are key factors in the increase in home insurance rates. As inflation increases, insurance companies respond by raising rates. This is because homes and belongings will cost more to replace. The insurance industry references the Consumer Price Index to measure inflation and adjust rates accordingly.

The rising costs of building materials, supply chain issues, and labour shortages are also driving up the costs of home repairs. For example, the growth of total costs outstripped the total inflation rate for the year at 4.1%, according to Verisk. Lumber was the only material cost to decrease from October 2022 to October 2023. As a result, insurance companies are paying higher rates for labour and passing these costs on to the consumer.

In addition, severe weather events are becoming more frequent and destructive, causing costly insurance claims. When catastrophic weather hits an area, the cost of construction materials can spike, and labourers are in higher demand, with their rates escalating. Home insurance premiums were up an average of 21% from May 2022 to May 2023, with the average increase being $244 per year.

The combination of inflation and the rising costs of materials is therefore a significant driver of increasing home insurance rates.

Lowering Florida Home Insurance: Tips and Tricks

You may want to see also

Explore related products

![]()

Claims and insurance history

The number and type of claims made on a home insurance policy can influence future premiums. Filing a claim increases your risk in the eyes of your insurance provider, and as your risk profile increases, so do your premiums. The increase in premiums depends on the type of claim, the amount of the settlement, and the number of claims filed in recent years. For instance, liability claims, especially those involving attorney fees, settlements, and medical bills, can be expensive and lead to higher premiums. Similarly, claims related to catastrophic events or natural disasters may result in higher premiums as they often involve substantial payouts.

It is important to note that not all claims are treated equally by insurance companies. Claims from easily preventable perils, such as fire damage or water backup, can cause premiums to jump. In contrast, catastrophes beyond the policyholder's control, like a tree falling on the house during a storm, may not lead to the same increase as they are less likely to recur. Additionally, claims history is typically recorded for up to five to seven years. After this period, the increased premium amount may decrease.

To assess a property's risk, insurance companies use databases like the Comprehensive Loss Underwriting Exchange (CLUE) report, which details previous claims filed for a particular property. This information helps insurance companies set rates, and errors on the CLUE report could result in higher premiums. Moreover, claims filed by previous owners of a home may also impact the rates for new owners.

To mitigate the impact of claims on insurance premiums, policyholders can consider the following strategies:

- Increasing the deductible: A higher deductible can lower the premium. However, it is important to have sufficient savings to cover the deductible in case of a loss.

- Bundling policies: Insurers often offer discounts when purchasing multiple policies, such as home and auto insurance, together.

- Installing protective devices: Some insurance companies provide discounts for smoke detectors, fire alarms, water sensors, interior sprinkler systems, and smart home protection devices.

- Shopping around: Comparing quotes from different insurance providers can help identify lower premiums or companies that reward proactive measures to improve home health.

Accident Forgiveness Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Natural disasters and severe weather

Homeowner's insurance typically increases each year, and natural disasters and severe weather events are significant contributors to this rise in insurance costs.

Natural disasters such as hurricanes, wildfires, tornadoes, flooding, earthquakes, and severe storms can cause extensive damage to homes, leading to costly insurance claims. The increasing frequency and intensity of these weather events have made them more destructive and expensive. As a result, insurers are faced with rising costs of insurance claims, which are then passed on to policyholders in the form of higher premiums.

The impact of natural disasters on insurance rates is influenced by several factors. Firstly, the cost of construction materials tends to spike after a catastrophic event as the demand for rebuilding and repairing homes surges. This was particularly evident during the pandemic, when shortages in building materials and skilled labour drove up the rates of construction. Secondly, labour costs typically increase in the aftermath of a natural disaster due to the heightened demand for workers in affected areas. Thirdly, older homes that require rebuilding to meet modern building codes can incur additional expenses.

The rising cost of materials and labour contributes to the overall increase in the cost of insurance. Insurers adjust their rates based on anticipated and actual weather-related losses, which further drives up insurance premiums.

It is important for homeowners to understand how their insurance policies cover natural disasters and to take proactive steps to ensure adequate coverage. Standard home insurance typically covers disasters unless specifically excluded, but additional coverage may be necessary for events like earthquakes and floods, which are often excluded from basic policies.

Mortgage Protection Insurance: Benefits and Advantages

You may want to see also

Explore related products

![]()

Home improvements and property value

Home improvements can have a significant impact on the cost of homeowner's insurance. While some improvements may lead to higher premiums, there are also renovations that can result in lower insurance costs.

Firstly, it is important to understand that the cost of rebuilding your home is a key factor in determining insurance premiums. If you add a room, increase square footage, or install higher-end materials, your rebuilding costs will increase, leading to higher premiums. On the other hand, renovations that make your home more resistant to damage, such as installing a sturdier roof or impact-rated windows, can lower your premiums.

Additionally, market conditions, such as the rising cost of building materials and labour shortages, can also impact your insurance rates. Severe weather events and natural disasters, such as hurricanes, wildfires, and floods, have become more frequent and destructive. As a result, insurance companies may adjust rates based on anticipated weather-related losses in specific regions, leading to potential premium hikes for homeowners in these areas.

To manage costs, it is advisable to review your insurance policy regularly and work closely with your insurance agent or company. They can guide you in evaluating your coverage needs and ensuring you have adequate protection. Installing protective devices, such as smoke detectors, fire alarms, and smart home security systems, may also help you qualify for premium discounts.

Furthermore, bundling your insurance policies, enrolling in paperless billing, and taking advantage of customer retention programs can provide additional cost savings. By being proactive and informed, you can better manage the impact of home improvements and market conditions on your homeowner's insurance premiums.

Homeowner's Insurance: Heating System Replacement Covered?

You may want to see also

Explore related products

![]()

Credit history and personal performance

Homeowner's insurance premiums may increase annually, and while this is not always the case, it is a common occurrence. Several factors influence these rising rates, including inflation, severe weather events, and an increase in the cost of building materials.

The impact of credit history on insurance rates varies depending on the insurer and the state of residence. In some states, such as California, Maryland, and Massachusetts, the use of credit history as a rating factor is prohibited. However, in most states, credit history and CBI scores influence the insurance rates offered to homeowners. A poor credit history may result in higher insurance rates, as insurers consider individuals with poor credit to have higher loss ratios. Conversely, individuals with excellent credit scores may enjoy reduced insurance premiums, sometimes by 20% or more.

It is important to note that while credit history is a significant factor, it is not the sole determinant of homeowner's insurance rates. Other factors, such as home characteristics, claims history, marital status, and the amount of coverage, also play a role in calculating insurance premiums. Additionally, shopping for insurance and comparing quotes can help individuals find the most cost-effective options, even with poor credit histories.

To summarise, credit history and personal performance are crucial factors in determining homeowner's insurance rates. Insurers use credit-based evaluations to assess an individual's risk and set insurance premiums. While a poor credit history may lead to higher rates, other factors also come into play, and shopping around can help individuals find the most suitable and affordable insurance options.

Combining Home Insurance: Live-In Partners and Policies

You may want to see also

Frequently asked questions

Homeowner's insurance rates have been increasing every year, with the Consumer Federation of America reporting an average increase of 24% over three years. Several factors contribute to the rising cost of homeowner's insurance, including inflation, labour shortages, and severe weather events.

As inflation increases, insurance companies raise rates because your home and belongings will cost more to replace. The insurance industry references the Consumer Price Index to measure inflation and adjust rates accordingly.

As climate change continues to alter weather patterns, certain areas that were once considered low risk are now more vulnerable to extreme weather events such as hurricanes, wildfires, floods, and tornadoes. Homeowners in these areas may experience steep premium hikes as insurers account for the increased likelihood of weather-related damage and claims.

In addition to inflation and severe weather, labour shortages and the rising cost of construction materials can drive up insurance rates. Other factors include filing claims, increasing the square footage or value of your home, and having a poor credit score.