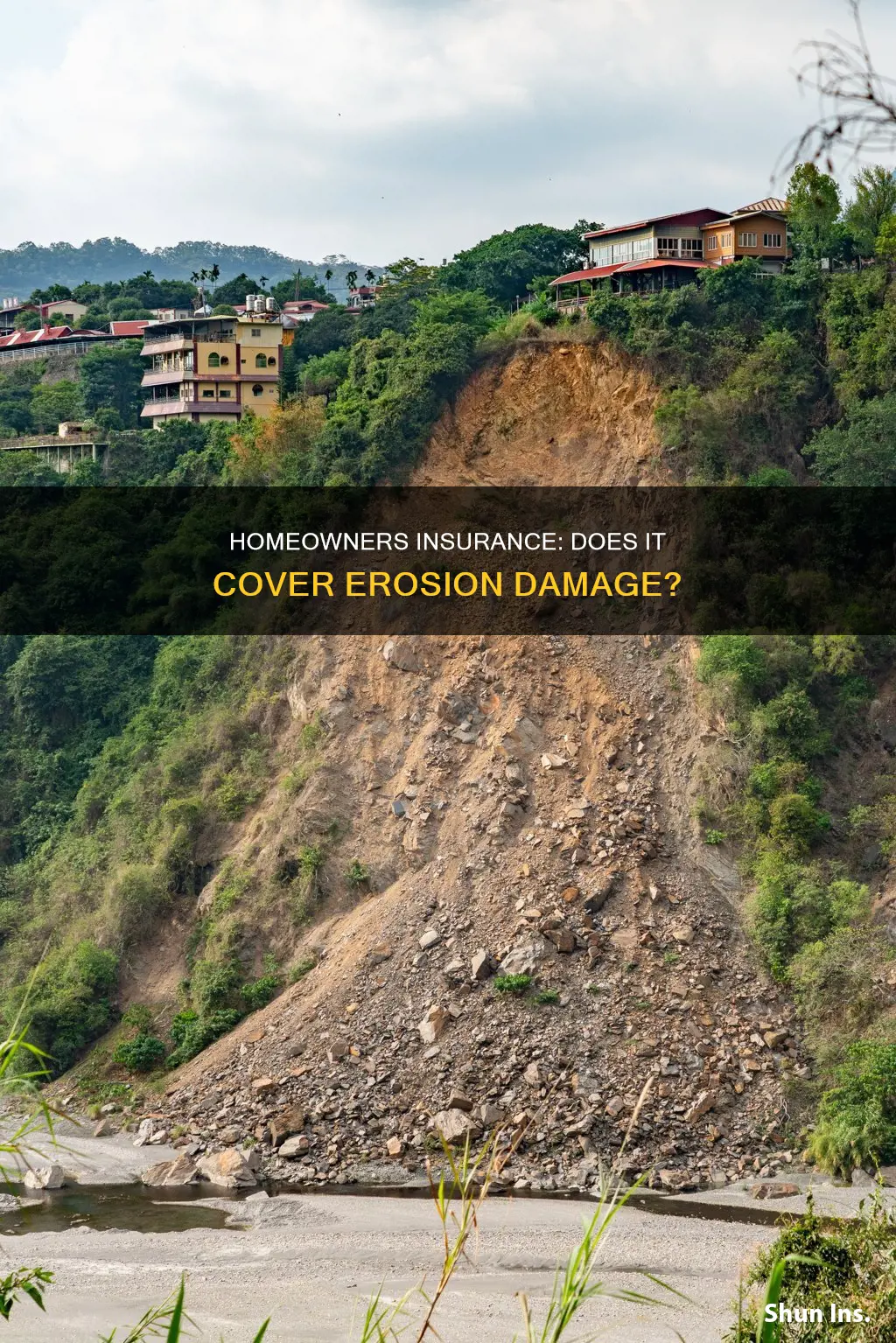

Erosion is not typically covered by homeowners insurance. This is because it is classified as an earth movement, along with earthquakes, sinkholes, landslides, and mudslides, which are not covered due to their infrequency, unexpectedness, and high costs. However, there are some circumstances in which homeowners insurance might cover damage caused by erosion. For example, if a covered event, such as a wildfire, caused erosion, a homeowner could argue that the covered event was the primary cause of the damage. Additionally, some insurance companies offer land stabilization coverage, and retaining walls, which can help prevent erosion, may be covered under certain conditions. Furthermore, policies like Difference in Conditions (DIC) insurance can provide coverage for erosion-related incidents, although they tend to be expensive.

| Characteristics | Values |

|---|---|

| Does homeowners insurance cover erosion? | No, homeowners insurance does not typically cover damages caused by erosion. |

| What is covered by homeowners insurance? | Homeowners insurance covers damage caused by fire, lightning, theft, and vehicles (not owned or operated by a resident of the house). |

| What is not covered by homeowners insurance? | "Earth movements", including earthquakes, sinkholes, landslides, and mudslides, are not covered by homeowners insurance. |

| Are there any exceptions to the erosion coverage? | In rare cases, homeowners may be able to claim erosion coverage if it is caused by a covered event, such as a wildfire, or if they have a separate flood insurance policy that covers erosion. |

| Are there any additional policies that cover erosion? | Difference in Conditions (DIC) policies specifically cover perils that are excluded from standard homeowners insurance, including erosion. |

| How can one prevent erosion? | Planting trees and shrubs on slopes can help reduce soil erosion. Retaining walls can also stabilize soil and prevent erosion. |

Explore related products

What You'll Learn

![]()

Homeowners insurance rarely covers erosion

Erosion is rarely covered by homeowners insurance. Standard policies typically exclude "earth movements", which include earthquakes, sinkholes, landslides, and mudslides. While retaining walls are often considered detached structures and may be covered under certain conditions, most homeowners insurance does not cover damage to garden retaining walls and yard erosion.

However, there are some rare situations where homeowners can fight for erosion coverage. For example, if a covered event, such as a wildfire, caused the erosion, a homeowner could cite "efficient proximate cause". Additionally, some insurance companies offer land stabilization coverage, which can help prevent erosion.

If you are looking for protection against erosion, there are a few options available. You can purchase a Difference in Conditions (DIC) policy, which covers perils not named in homeowners insurance, including landslides, earthquakes, and flooding, all of which can cause erosion. However, these policies tend to be expensive and are usually used by businesses rather than homeowners. Another option is to purchase flood insurance, which can cover damage caused by erosion if it is the result of flooding.

It is important to note that coverage may vary depending on your state and insurance provider. It is always a good idea to carefully review your policy and contact your insurance agent to understand what is and is not covered.

Mortgage Insurance: Is It Necessary for Rental Properties?

You may want to see also

Explore related products

![]()

Flood insurance may cover erosion

Standard homeowners insurance does not typically cover damage caused by erosion. This is because erosion is classified as "earth movement", which is usually listed as an exclusion in insurance policies. However, if you live in an area prone to flooding, you may want to consider purchasing flood insurance, which may offer some protection against erosion.

Flood insurance is available to homeowners, renters, and business owners through the National Flood Insurance Program (NFIP). This type of insurance is designed to protect against damage caused by floods, which can include erosion. While NFIP policies have limits on building coverage and contents, they can provide valuable protection if you live in an area at risk of flooding or erosion.

It is important to note that not all flood insurance policies are the same, and coverage may vary. For example, the Standard Flood Insurance Policy (SFIP) provided by FEMA does not cover loss to property caused by earth movement, even if it is a result of a flood. However, there are exceptions to this exclusion. The SFIP does cover losses from mudflow and land subsidence resulting from erosion that falls under the definition of a flood. This includes the collapse or subsidence of land along a body of water caused by waves or currents exceeding anticipated levels, resulting in a flood.

In addition to NFIP policies, you may also want to consider a Difference in Conditions (DIC) policy. This type of policy covers perils not named in homeowners insurance, including erosion. While DIC policies are typically used by businesses, they can also be beneficial for homeowners in high-risk areas as they are customizable to the specific risks faced by the insured property. However, these policies tend to be more expensive due to the comprehensive coverage they provide.

While flood insurance may provide some protection against erosion, it is not a guarantee. It is always important to carefully review the terms and conditions of any insurance policy before purchasing it to understand what is and isn't covered. Additionally, it is worth noting that preventative measures, such as planting trees and shrubs or installing retaining walls, can help stop erosion or minimize its effects on your property.

The Hunt for the Farmers Insurance Open: A Golfing Odyssey

You may want to see also

Explore related products

![]()

Difference in Conditions (DIC) insurance covers erosion

Standard homeowners insurance policies do not typically cover damages caused by erosion. Erosion is often classified as an "earth movement" event, along with earthquakes, sinkholes, and landslides, and is excluded from coverage. However, there are some alternative options available for those seeking protection against erosion.

Difference in Conditions (DIC) insurance is a type of policy that fills the gaps in coverage left by standard insurance policies. It provides protection against significant natural disasters and other perils that are usually excluded from standard policies. DIC insurance is highly customizable and can be tailored to meet specific needs. While it is more commonly purchased by businesses, it can also be beneficial for homeowners in high-risk areas.

DIC policies often cover a range of events, including landslides, earthquakes, flooding, and mudslides, which can all contribute to erosion. By purchasing a DIC policy, homeowners can gain peace of mind, knowing that they are protected against the devastating effects of erosion. This type of insurance can be particularly useful for those in areas prone to natural disasters or with a high risk of erosion.

It is important to note that DIC insurance is not a replacement for standard property insurance but rather a supplement. It is designed to provide additional coverage for perils that are beyond the scope of normal insurance policies. The deductibles for DIC policies may also be higher, as they are typically based on a percentage of the insured value.

To determine if DIC insurance is necessary, homeowners should review their current policy levels with an agent or broker. They can assess whether the current coverage is sufficient and advise on the potential benefits of adding a DIC policy. While it may not be needed by everyone, DIC insurance can provide valuable protection against erosion and other excluded perils.

Home Insurance: Contractor Errors and Damages Covered?

You may want to see also

Explore related products

![]()

Preventing erosion with retaining walls

Standard homeowners insurance plans typically do not cover damages caused by erosion. This is because erosion is classified as "earth movement", which is excluded from policies along with other events like earthquakes, sinkholes, and landslides.

Retaining walls are an effective solution for preventing soil erosion and stabilizing slopes in a landscape. They act as a barrier, intercepting the flow of water and redirecting it, allowing more water to be absorbed into the ground. This prevents the water from carrying soil with it, which would result in soil erosion.

To effectively prevent soil erosion behind a retaining wall, careful planning, proper design, and the implementation of erosion control measures are necessary. Here are some measures to prevent erosion with retaining walls:

- Drainage System: Construct a well-designed drainage system to direct water away from the wall. Install drainage pipes at the base of the wall and create weep holes at regular intervals to allow water to escape. This prevents water accumulation, reducing the risk of hydrostatic pressure and subsequent soil destabilization.

- Backfill Material: Choose granular, well-draining materials such as crushed stone or gravel for backfill. These materials facilitate drainage by allowing water to flow through them easily. Ensure the backfill material is compatible with the native soil to prevent differential settling and maintain wall stability.

- Vegetation: Incorporate vegetation and planting, such as grass, shrubs, or ground cover, behind the retaining wall. Plant roots anchor the soil in place, reducing the impact of rainfall on the soil surface and preventing erosion.

- Terracing and Staircases: Implement terracing or staircases in steep slope areas. Terracing involves creating multiple levels or steps in the slope and constructing retaining walls at each level. This reduces the slope's steepness, minimizing the risk of erosion. Staircases help divide the slope into smaller sections, preventing water accumulation and reducing erosion potential.

- Regular Inspection and Maintenance: Regularly inspect the retaining wall and the area behind it for signs of erosion, such as exposed roots, bare patches, or sediment accumulation. Promptly address and repair any areas showing signs of erosion to maintain the wall's integrity and prevent further damage.

By implementing these measures, you can effectively prevent soil erosion behind retaining walls, ensuring the long-term stability of your landscape.

Launching a Farmers Insurance Branch: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Homeowners insurance covers landscaping damage

Standard homeowners insurance does not typically cover damage caused by erosion. Erosion is classified as "earth movement" and is considered alongside earthquakes, sinkholes, and landslides, which are also not usually covered. However, there are some circumstances in which homeowners insurance may cover landscaping damage.

Homeowners insurance generally covers landscaping damage resulting from specific perils, such as fire, lightning, theft, and vandalism. Some policies also include coverage for damage caused by vehicles not owned or operated by a resident of the house. In the case of fallen trees, if the tree fell due to a covered peril, such as a storm or strong winds, and damaged an insured structure, the removal costs would likely be covered. However, if the tree fell due to the homeowner's negligence or a maintenance issue, the removal costs would typically not be covered.

While erosion itself is generally not covered, there are measures you can take to prevent or mitigate its effects. For example, planting trees and shrubs on slopes can help reduce soil erosion by absorbing water and stabilizing the soil with their roots. Retaining walls can also break up land into terraces, stabilizing the soil and leveling the ground. Temporary fixtures like plastic sheets or mesh coverings can also be placed over at-risk areas before a storm to mitigate erosion.

In rare cases, homeowners may be able to claim erosion coverage if a covered event, such as a wildfire, indirectly caused the erosion. For example, the water used to put out the flames and the resulting loss of vegetation could lead to erosion, and a homeowner could argue that the covered event was the primary cause.

Additionally, while not typically needed by the average person, a Difference in Conditions (DIC) policy can provide coverage for perils not named in standard homeowners insurance, including erosion. This type of policy is often used by large commercial businesses but may be beneficial for homeowners in high-risk areas. The National Flood Insurance Program (NFIP) is another option for those in areas prone to flooding or rising water, as it can provide protection if a flood causes erosion that puts your home at risk.

Homeowners Insurance: Rental Expense or Not?

You may want to see also

Frequently asked questions

Unfortunately, your homeowners insurance will likely not cover damages caused by erosion. Most insurance policies exclude coverage for "earth movements", which includes erosion, earthquakes, sinkholes, landslides, and mudslides.

If your property is on a hill or incline, consider planting trees and shrubs on the slope. Plants can reduce soil erosion on the surface by halting and absorbing moving water, and their roots hold the soil in place. Retaining walls can also help stabilise the soil and level the ground.

While standard homeowners insurance policies do not cover erosion, there are some policies that can provide coverage. Difference in Conditions (DIC) policies are a specific type of coverage for perils not named in homeowners insurance, including erosion. Flood insurance may also cover erosion if it is caused by flooding.