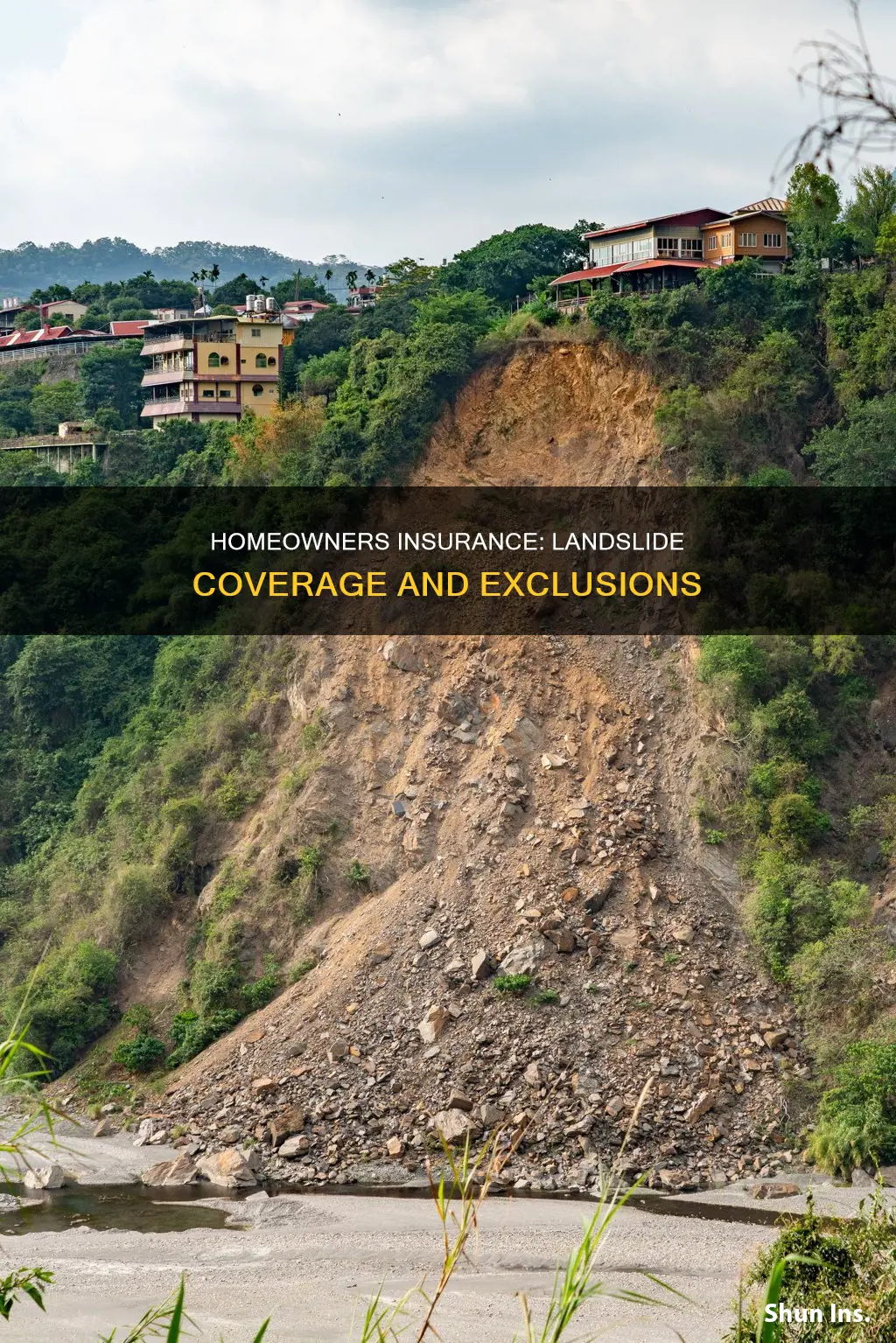

Homeowners insurance is an important investment to protect your home from various risks. However, when it comes to landslides, standard homeowners insurance policies typically do not provide coverage. Landslides are considered earth movement or ground movement, which is explicitly excluded from standard policies. Homeowners in landslide-prone areas may need to consider additional coverage, as standard policies may not offer sufficient protection against landslide damage. The availability and cost of landslide insurance can vary depending on factors such as location, policy type, and level of coverage. To insure against landslides, individuals may need to purchase a separate policy, known as a Difference in Conditions (DIC) policy, which covers landslides, mudflows, earthquakes, and floods.

| Characteristics | Values |

|---|---|

| Landslide coverage under standard homeowners insurance | No |

| Landslide considered as | "Earth movement" or "ground movement" |

| Reasons for landslides | Erosion, water accumulation, heavy rainfall, earthquakes, or human activities like construction |

| Additional coverage required | Difference in Conditions (DIC) or "gap coverage" policy |

| DIC policy coverage | Landslides, mudslides, floods, and earthquakes |

| Availability of DIC policies | Not offered by all insurance companies |

| Factors influencing DIC policy cost | Location, policy type, and level of coverage |

| Homeowner's responsibility | Assess the geological characteristics of the property and surrounding areas |

Explore related products

What You'll Learn

- Landslides are considered earth movement events and are excluded from standard homeowners insurance policies

- To protect against landslides, you can purchase a separate Difference in Conditions (DIC) policy

- DIC policies cover landslides, mudflows, earthquakes, and floods

- Homeowners insurance may cover fire, explosion, or theft resulting from landslides

- Location, policy type, and cost influence the availability and affordability of landslide coverage

![]()

Landslides are considered earth movement events and are excluded from standard homeowners insurance policies

Standard homeowners insurance policies do not cover landslides, as they are considered "earth movement" events. This classification includes earthquakes, mudslides, and mudflows, which are also typically excluded from coverage. The separation of these events from standard insurance policies is due to their infrequency and the extensive damage they can cause, making it challenging for insurance companies to provide coverage.

Homeowners seeking protection against landslides have a few options. Firstly, they can purchase a "Difference in Conditions" (DIC) policy, which offers comprehensive coverage for landslides, mudflows, earthquakes, and floods. These policies are sold by surplus lines insurers and can provide the necessary protection for homeowners in high-risk areas. The cost of a DIC policy depends on factors such as location, the level of coverage, and the type of policy chosen.

Another option for homeowners is to add content coverage to their existing homeowner insurance. Content coverage protects the contents of the home from various dangers, including earth movement. However, it is important to note that content coverage does not extend to the building structure itself. The availability of this option may vary depending on the insurer.

The location of the home plays a significant role in determining the availability and cost of landslide insurance coverage. Homes situated in areas prone to landslides, such as mountainous regions or regions with a history of landslides, may find it challenging to obtain coverage from insurance companies due to the higher risk. As a result, homeowners in these high-risk zones should carefully review their policies and consider purchasing additional coverage specifically tailored to landslides.

It is worth noting that while landslides are generally excluded from standard homeowners insurance, some policies may offer landslide coverage as an endorsement or add-on. Therefore, it is crucial for homeowners to carefully review their policies and understand the specific inclusions and exclusions to ensure they have adequate protection against landslides and other natural disasters.

Deactivating Your Farmers Insurance Profile: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

To protect against landslides, you can purchase a separate Difference in Conditions (DIC) policy

Standard homeowners insurance policies typically do not cover landslides, as they are considered "earth movement" events, similar to earthquakes. This means that damage caused by landslides, such as to the structure of your home or its contents, may not be covered by your insurance.

However, if you live in an area prone to landslides, such as a mountainous region, you may want to consider purchasing additional coverage to protect your home and belongings. This is where a separate Difference in Conditions (DIC) policy comes in.

A DIC policy is a type of supplemental insurance that provides expanded coverage for perils that are typically excluded from standard insurance policies. It is designed to fill in gaps in insurance coverage and offer protection from catastrophic events, such as landslides, mudflows, earthquakes, and floods. DIC policies are highly adaptable and can be tailored to meet the specific needs of the policyholder. They are commonly used by businesses with large-scale operations or expensive corporate buildings but can also be beneficial for homeowners in disaster-prone regions.

The cost of a DIC policy can vary depending on factors such as the location of your home, the level of coverage, and the risk of landslides in your area. It is important to note that DIC policies are typically sold by surplus line insurers, and the high-value nature of these policies often results in higher premiums and deductibles.

To determine if a DIC policy is right for you, it is recommended to consult with your insurance agent or broker, who can assess your current policy and advise on whether additional coverage is necessary. They can help you find a surplus line insurer that meets your specific needs and ensure that your home is adequately protected against landslides and other natural disasters.

Vintage Home Insurance: Affordable or Not?

You may want to see also

Explore related products

![]()

DIC policies cover landslides, mudflows, earthquakes, and floods

Standard homeowners insurance policies typically do not cover landslides, mudflows, earthquakes, or floods. These events are generally classified as "earth movement" or "ground movement" and are excluded from coverage. However, homeowners can purchase additional coverage or endorsements to protect their property from these specific perils.

Difference in Conditions (DIC) policies are a type of supplemental insurance designed to fill the gaps in coverage provided by standard insurance policies. DIC insurance is often used by larger organizations or multinational firms to protect against catastrophic perils that are not typically covered by standard insurance.

While DIC insurance is not common for individuals, homeowners concerned about landslides, mudflows, earthquakes, or floods can benefit from purchasing a DIC policy. DIC policies provide expanded coverage for these specific events, offering protection beyond what standard homeowners insurance offers.

DIC policies are sold by surplus lines insurers, and interested homeowners can work with their insurance agents or brokers to find a suitable policy. These policies are flexible and can be tailored to the specific needs of the homeowner, including coverage for their property and any unattached buildings on their land.

It is important for homeowners to carefully review their existing policies and understand the risks associated with their property's location. By assessing their coverage needs and the geological characteristics of their area, homeowners can make informed decisions about purchasing additional coverage, such as a DIC policy, to ensure adequate protection against landslides, mudflows, earthquakes, and floods.

Mortgage Insurance: Missing 1098 Details Explained

You may want to see also

Explore related products

![]()

Homeowners insurance may cover fire, explosion, or theft resulting from landslides

Homeowners insurance does not typically cover landslides, as they are considered "earth movement" events, which are excluded from standard policies. However, it's important to note that homeowners insurance may provide coverage for specific scenarios resulting from landslides. For instance, fire, explosion, or theft ensuing from a landslide may be covered by your homeowners insurance policy.

While landslides themselves are generally not covered, some insurance companies offer comprehensive protection against such events through "Difference in Conditions" (DIC) policies. These policies are specifically designed to fill the gaps left by standard homeowners insurance and provide coverage for landslides, mudflows, earthquakes, and floods. The cost of a DIC policy can range from several hundred to a few thousand dollars annually, depending on the insured items and the level of coverage.

It is worth noting that the availability and cost of landslide coverage are influenced by several factors, including the location of your home, the policy type, and the risk level. If you reside in an area prone to landslides, such as mountainous regions or steep slopes, obtaining landslide insurance coverage may be more challenging and expensive due to the higher risk associated with these zones.

Before purchasing homeowners insurance, it is crucial to carefully review the policy to understand its inclusions and exclusions. If you live in a landslide-prone area, consider acquiring a DIC policy or opting for a homeowners insurance plan that includes landslide coverage as an add-on. This proactive approach ensures that your home is adequately protected in the event of a landslide or related incidents.

Additionally, it is important to be aware of other factors that may contribute to landslides, such as construction activities. In some cases, if the landslide was caused by human activities rather than natural slope erosion, you may have legal recourse against the responsible party. Consulting with a specialized lawyer can help determine your options in such situations.

Phone Insurance Claims: A Step-by-Step Guide

You may want to see also

![]()

Location, policy type, and cost influence the availability and affordability of landslide coverage

Landslides are generally excluded from standard homeowners insurance policies because they are considered "earth movement" events, similar to earthquakes. To obtain landslide coverage, you typically need to purchase additional coverage or a separate policy, and the availability and cost of this coverage can vary depending on various factors.

Location plays a significant role in the availability and affordability of landslide coverage. If you live in an area prone to landslides, such as regions with hilly terrain or areas susceptible to heavy rainfall or erosion, obtaining affordable landslide coverage may be more challenging. Insurance providers may charge higher premiums or have more limited coverage options in these high-risk areas. Conversely, in regions where landslides are less frequent or unlikely, landslide coverage may be more readily available and affordable.

The type of policy you choose also influences the availability and cost of landslide coverage. Standard homeowners insurance policies typically exclude landslide coverage, so you may need to purchase a separate "Difference in Conditions" (DIC) policy or a similar endorsement. These policies usually provide comprehensive coverage for landslides, mudflows, earthquakes, and floods, but they may be more expensive or have higher deductibles due to the increased coverage they offer.

Additionally, the cost of landslide coverage can vary depending on the value and location of your home, as well as the level of coverage you require. If you live in an area with a higher risk of landslides, the cost of coverage may be higher to reflect the increased likelihood of a claim. Similarly, if you have a higher-value home or require coverage for both the structure and contents of your home, the premium for landslide coverage will likely be higher to account for the potential cost of repairs or replacement.

It's important to note that insurance regulations and offerings can vary by state and insurance provider. Therefore, it's advisable to consult with a local insurance professional or agent to understand the specific options available in your area. They can guide you through the process of obtaining appropriate coverage for your needs and help you navigate the complexities of landslide insurance.

Overall, by considering factors such as location, policy type, and cost, you can make informed decisions regarding landslide coverage and ensure that you have adequate protection for your home and belongings.

T-Mobile Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

No, landslides are considered "earth movement" events and are excluded from standard homeowners insurance policies.

You can purchase a separate policy known as a "'Difference in Conditions' (DIC) policy", which covers landslides, mudflows, earthquakes, and floods. Not all insurance companies offer DIC policies, so you may need to purchase it from a different company.

The location of your home, the type of policy, and the level of coverage will all impact the availability and cost of landslide insurance. If you live in an area prone to landslides, such as a mountainous region, insurance companies may not offer coverage or may charge higher premiums due to the increased risk.