Homeowners insurance is a type of property insurance that covers the policyholder's property and personal belongings in the event of theft, damage, or destruction. It typically covers the cost of repairing or replacing a home and its contents, as well as providing liability protection for injuries or property damage caused by the policyholder or their family members. Personal belongings covered under homeowners insurance can include furniture, clothing, sports equipment, and other valuable items. It's important to note that the extent of coverage may vary depending on the insurance provider and the specific policy, and additional coverage may be required for certain high-value items.

| Characteristics | Values |

|---|---|

| What does it cover? | Financial protection against loss due to disasters, theft, and accidents. |

| What type of losses are covered? | Replacement cost and actual cash value. Replacement cost covers the item as new at the time of the claim. Actual cash value is the replacement cost minus depreciation. |

| What items are covered? | Furniture, clothes, sports equipment, and other personal items. Expensive items like jewelry, furs, art, collectibles, and silverware are also covered but with dollar limits. |

| Are other people's belongings covered? | Homeowners insurance covers the personal property of you and your family, and this protection often applies to your dependents' belongings when they're in college. |

| What events are covered? | Fire, theft, and other covered perils outlined in the policy. Some policies also cover damages caused by riots and civil commotion and falling objects. |

| Are there any exclusions? | Flood damage and damage caused by earthquakes or routine wear and tear are typically not covered. Damage caused by pets or other animals owned by the policyholder is also usually excluded. |

| How much coverage is needed? | It depends on the value of the personal property. An accurate inventory of items and their replacement costs can help determine the required coverage. |

| Are there any additional coverages? | Yes, homeowners insurance may also include liability protection for injuries or property damage caused by the policyholder or their family. It can also cover additional living expenses if the home becomes uninhabitable due to a covered event. |

| How much does it cost? | The cost of homeowners insurance can vary depending on various factors, including the location of the property and the coverage limits. Installing a home security system or increasing the deductible may help lower the premium. |

Explore related products

$14.99 $14.99

What You'll Learn

![]()

Personal property insurance

The amount of personal property coverage you need depends on the value of the items in your home. To work out how much coverage you need, make an inventory of your personal property, including a description of each item, its make, model, purchase price, serial number, and other relevant details. You should also collect proof of purchase, such as receipts, contracts, and appraisals. Once you know the total replacement cost of your belongings, you'll have a good idea of how much personal property insurance you need.

Insurers typically set limits on certain categories of personal property, known as "sub-limits". For example, you might have a total personal property coverage limit of $100,000 but only be eligible for a smaller set amount for a specific high-value item, such as jewellery or a laptop. If you own high-value items, you may want to increase your coverage limits or purchase scheduled personal property coverage, which allows you to add specific items to your policy. Scheduling items will likely raise your premium, but it helps ensure you're adequately covered.

Term Insurance: Is It a Smart Investment?

You may want to see also

Explore related products

![]()

Additional living expenses

ALE insurance covers temporary accommodation if your home is uninhabitable due to a covered loss. This includes hotel stays, food, transportation, and other living costs above and beyond your normal expenses. It is important to note that ALE does not cover any costs that are part of your regular expenses, such as utility bills, groceries, or mortgage payments. The coverage is meant to maintain your standard of living and typically amounts to about 10% to 20% of the insurance that covers the dwelling.

ALE coverage is triggered when your home becomes uninhabitable due to events like fire, water damage, storm damage, or natural disasters. It is important to check with your policy about what specific events are covered, as some events like floods or earthquakes may be excluded.

In terms of what is covered, ALE can include the cost of doing laundry, furniture rental, and storage costs for the contents of your home under special circumstances. It is designed to cover the out-of-pocket expenses that arise from being temporarily displaced from your home.

It is worth noting that ALE coverage has limits, and there may be a dollar limit and a time limit for how long it will continue to pay your additional costs. Additionally, ALE may not cover certain expenses, such as childcare or insurance payments.

The Roadside Companion: Unraveling Farmers Truck Insurance Exchange

You may want to see also

Explore related products

![]()

Liability protection

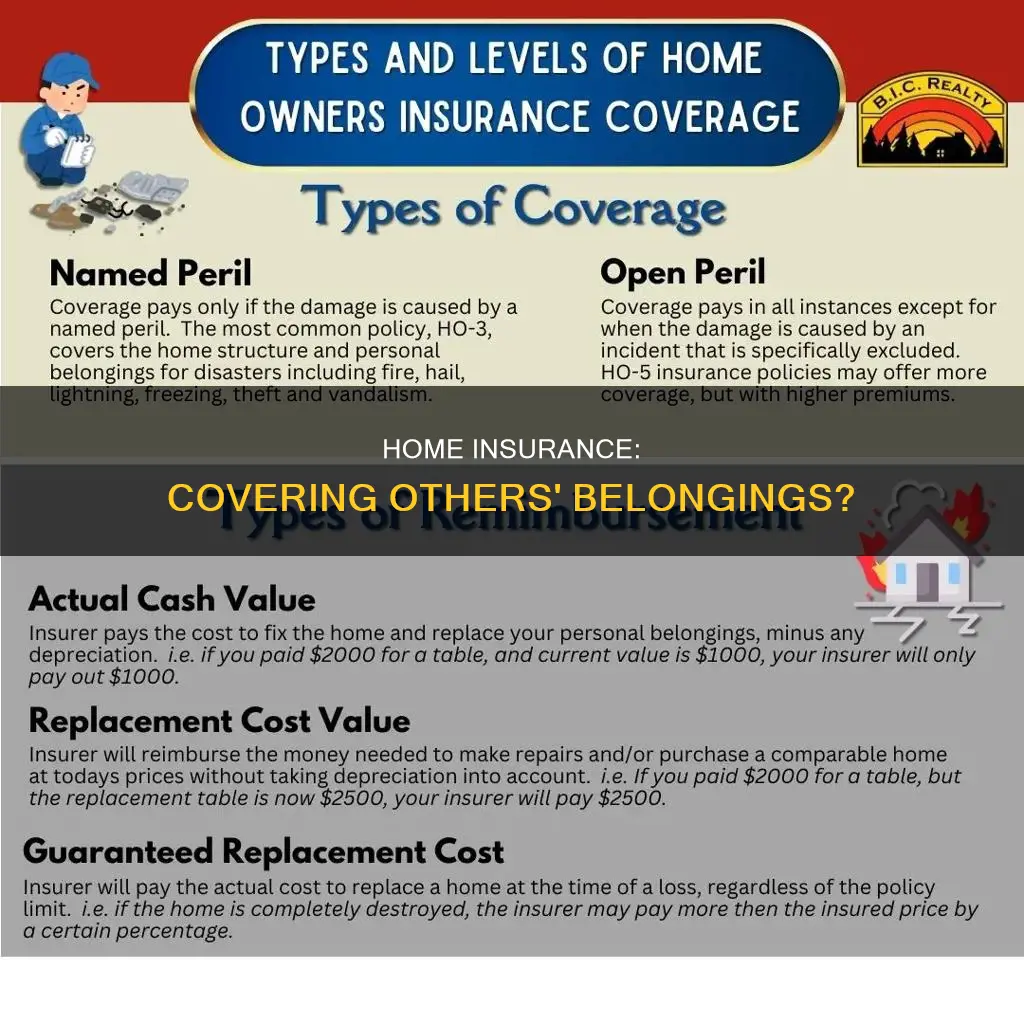

When it comes to liability protection and homeowners insurance, one of the key concerns for many people is whether their policy covers damage to other people's belongings. This is an important aspect of liability protection, and it's reassuring to know that standard homeowners insurance policies typically provide this type of coverage. This coverage extends to situations where you may be legally responsible for damage to another person's property. For example, if you accidentally damage a friend's expensive gadget while visiting their home, your homeowners insurance policy's liability protection could step in to help cover the cost of repairs or replacement. This demonstrates how your policy offers a financial safeguard not only for your own belongings but also for those of others, giving you peace of mind in social situations.

Another scenario where liability protection comes into play is if you accidentally damage someone else's property while renting a home or apartment. For instance, if you accidentally cause water damage that affects your downstairs neighbor's belongings, your liability coverage can help cover the cost of repairs or replacement. This demonstrates how homeowners insurance policies can provide valuable protection even when you don't own the dwelling, offering financial assistance for accidental damage to others' property.

Additionally, liability protection can cover damage caused by your children or minors in your care. If your child accidentally breaks a neighbor's window while playing, your homeowners insurance policy may cover the cost of repairs. This demonstrates how liability protection takes into account various scenarios involving accidental damage caused by your family members or those under your supervision. However, it's important to remember that intentional or malicious acts are typically excluded from coverage.

In conclusion, liability protection is a crucial aspect of homeowners insurance, offering financial protection beyond just your own belongings. By covering damage to other people's property, accidents on your premises, rental situations, pet-related incidents, and accidents caused by minors, liability protection provides comprehensive coverage for a wide range of scenarios. Understanding the extent of your liability protection can give you peace of mind and help you navigate potential challenges with confidence, knowing that you have a financial safeguard in place. Remember to carefully review your policy to fully grasp the scope of your liability coverage and any exclusions that may apply.

Rental Insurance: House Burns Down, Now What?

You may want to see also

Explore related products

![]()

Coverage for belongings outside the home

Homeowners insurance covers the cost of repairing or replacing your home and belongings in the event of damage caused by a covered event, such as a fire, theft, or certain types of bad weather. Personal property coverage is a section of your homeowners insurance policy that covers your personal possessions in the event of a covered loss. This includes your furniture, clothes, sports equipment, and other personal items, which are typically covered if they are stolen or destroyed by fire, hurricane, or other insured disasters.

The coverage for personal belongings under homeowners insurance typically extends beyond the home, providing worldwide coverage for your belongings even when they are stored off-premises or taken with you on a trip. This means that your belongings are protected anywhere in the world, and you can have peace of mind knowing that your insurance policy has you covered in the event of a loss or damage.

It is important to note that while homeowners insurance provides comprehensive coverage for your belongings, there may be certain limitations or exclusions. For example, there might be sub-limits or dollar limits on expensive items like jewelry, furs, art, collectibles, and silverware in the event of theft. To ensure adequate coverage for these valuable items, you may need to schedule them individually or purchase additional coverage, such as a special personal property endorsement or floater, to insure them for their full appraised value.

Additionally, it is worth mentioning that homeowners insurance typically does not cover personal items that you have misplaced. It primarily covers damaged or stolen property, and the coverage may vary depending on the specific terms of your policy and your location. Therefore, it is always advisable to carefully review your policy, understand the coverage limits, and discuss any concerns with your insurance provider to ensure that your belongings, both inside and outside the home, are adequately protected.

By understanding the extent of coverage for belongings outside the home, you can make informed decisions about your homeowners insurance and take the necessary steps to protect your valuable possessions, no matter where they are.

Flood Insurance: What Mortgage Holders Need to Know

You may want to see also

Explore related products

![]()

Identity theft protection

Identity theft is a serious issue that can have severe consequences for your financial future. While no option is foolproof, there are several ways to protect yourself from identity theft. Here are some measures you can take to safeguard your personal information and mitigate the financial impact in the event of identity theft:

Vigilance and Self-Protection:

- Regularly check your financial statements and credit reports for any unauthorized transactions or signs of foul play.

- Set up randomized and strong passwords for your online accounts.

- Enable two-factor authentication for an extra layer of security.

- Avoid sharing personal information with suspicious parties, such as scam emails or phone calls.

- Take advantage of the free protections offered by your credit card company or bank.

Identity Theft Insurance:

Identity theft insurance can provide financial relief and assistance in restoring your identity and credit. It is typically offered as an add-on to homeowners insurance policies or can be purchased separately. Here are some key points about identity theft insurance:

- Reimbursement of Expenses: Identity theft insurance can reimburse you for expenses incurred in restoring your identity, such as legal fees, notary fees, postage fees, and lost wages. Some policies may also cover child care costs during the restoration process.

- Fraud Alerts and Monitoring: Insurance providers actively monitor your credit reports and watch for signs of fraud. They can set up fraud alerts and notify you of any suspicious activity.

- Access to Specialists: Many companies offer access to fraud specialists who can advise and assist you in repairing the damage caused by identity theft. They may even communicate with creditors, government agencies, and financial institutions on your behalf.

- Cost of Coverage: The cost of identity theft insurance varies depending on the insurer and the level of coverage. It typically ranges from $20 to $60 per year for basic coverage, but more comprehensive policies can cost over $500 per year.

- Limitations: It's important to note that identity theft insurance does not prevent identity theft or reimburse direct monetary losses. It assists in mitigating the financial impact and helping you restore your identity and credit.

Standalone Identity Theft Protection Services:

In addition to insurance, there are dedicated identity theft protection services offered by companies like CyberScout, Generali Global Assistance, LifeLock, and IDShield. These services actively monitor your personal information, send alerts for suspicious activity, and provide restoration services if your identity is compromised. Some companies, like Experian, offer dark web surveillance and credit monitoring as part of their protection plans.

In conclusion, while there is no guaranteed way to prevent identity theft, a combination of vigilance, insurance coverage, and dedicated protection services can significantly reduce the risk and financial burden associated with this crime. It is important to carefully review the terms and conditions of any insurance policy or protection service before purchasing to ensure it meets your specific needs and provides adequate coverage.

Lightning Strikes: Are You Insured?

You may want to see also

Frequently asked questions

Homeowners insurance covers the cost of repairing or replacing your home when it gets damaged by a covered event, such as a fire, theft, or certain types of bad weather. It also covers your personal belongings, other structures on your property, and provides liability protection for injuries or property damage caused by you or your family.

Homeowners insurance covers the personal property of you and your family, and this protection often extends to your dependents' belongings when they are in college. However, the coverage limit for personal items taken outside of your property may be lower than if something is stolen from your home.

To determine how much homeowners insurance you need for your belongings, start by making an inventory of the items in your home, including furniture, electronics, appliances, and personal items. Then, calculate the replacement cost for each item, and add up the total to get an idea of how much personal property insurance you require.

Yes, it's important to note that homeowners insurance typically does not cover personal items that have been misplaced. Additionally, standard policies usually exclude coverage for damage caused by floods, earthquakes, or routine wear and tear. There may also be sub-limits on certain categories of personal property, such as jewellery, art, or collectibles.