The question of whether insurance counts towards credit is a common one, often arising from the desire to understand how financial responsibilities impact credit scores. Generally, insurance payments themselves, such as premiums for auto, health, or life insurance, do not directly contribute to building or improving credit because they are not reported to credit bureaus. However, the relationship between insurance and credit can become relevant in certain scenarios, such as when missed insurance payments lead to collections or when applying for insurance, as insurers may review credit scores to assess risk and determine premiums. Understanding this interplay is crucial for managing both financial health and insurance coverage effectively.

| Characteristics | Values |

|---|---|

| Direct Impact on Credit Score | Insurance payments (e.g., health, auto, life) do not directly impact your credit score, as they are not reported to credit bureaus. |

| Indirect Impact via Debt | Unpaid insurance premiums can lead to debt collection, which, if reported, negatively affects your credit score. |

| Credit-Based Insurance Scores | Insurance companies use credit-based insurance scores to determine premiums, but this does not affect your credit score. |

| Payment History | On-time insurance payments are not reported to credit bureaus, so they do not improve your credit history. |

| Late Payments | Late insurance payments may lead to policy cancellation or debt, but only if the debt is reported to collections will it impact your credit. |

| Credit Checks by Insurers | Insurers may perform soft credit inquiries to assess risk, which do not affect your credit score. |

| Credit Builder Loans | Some insurers offer credit-builder loans, which, if reported, can positively impact your credit score. |

| Bundling Services | Bundling insurance with other financial services (e.g., banking) may offer perks but does not directly improve credit. |

| Credit Monitoring Services | Some insurers provide credit monitoring as a benefit, but this does not count toward your credit score. |

| Policy Cancellations | Cancelled policies due to non-payment may lead to debt, which, if reported, can harm your credit. |

Explore related products

What You'll Learn

![]()

Insurance Payments Impact on Credit Score

Insurance payments generally do not directly impact your credit score, as most insurance companies do not report payment history to the major credit bureaus (Equifax, Experian, and TransUnion). Credit scores are primarily influenced by factors such as credit card usage, loan payments, and public records like bankruptcies or liens. However, there are indirect ways in which insurance payments can affect your credit score, and understanding these nuances is crucial for maintaining a healthy financial profile.

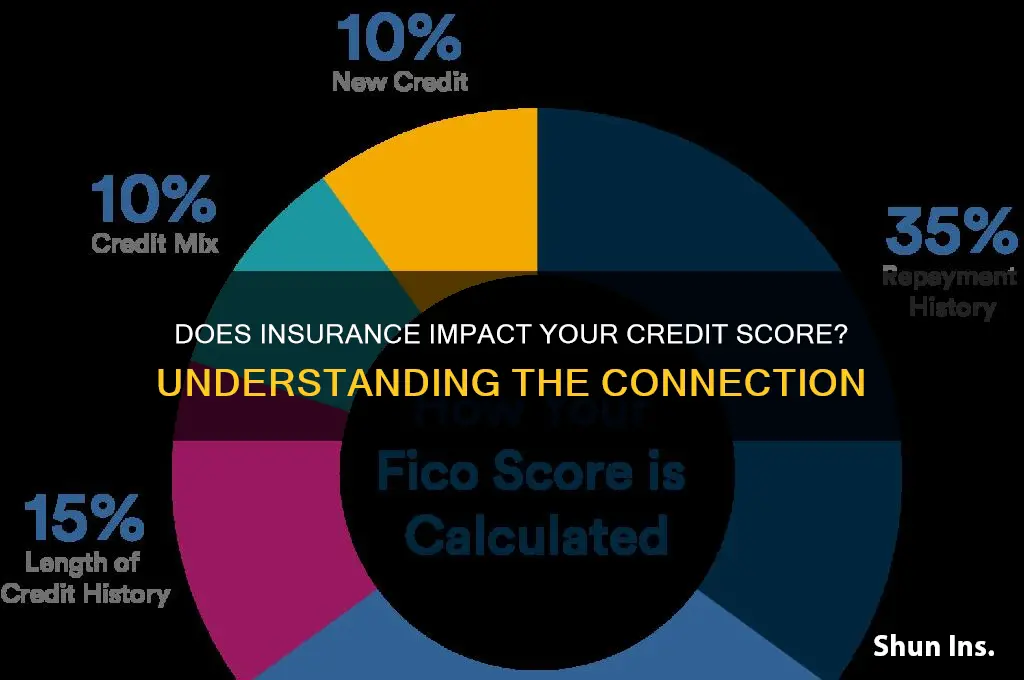

One indirect way insurance payments can impact your credit score is through missed payments or defaults. If you fail to pay your insurance premiums and the account is sent to collections, the collection agency may report the delinquency to the credit bureaus. This negative mark can significantly lower your credit score, as payment history typically accounts for 35% of your FICO score. To avoid this, ensure timely payments or set up automatic payments if your insurer offers this option. Additionally, some insurers may require a deposit or prepayment if your credit score is low, which could indirectly tie your creditworthiness to your insurance obligations.

Another indirect connection arises when you finance insurance premiums. Some insurance companies or third-party lenders allow policyholders to pay premiums in installments, often with interest. If you opt for this financing, the lender may report the account to the credit bureaus. In this case, on-time payments can positively impact your credit score by demonstrating responsible financial behavior. Conversely, late or missed payments on a financed insurance policy can harm your credit. Always check if the financing arrangement is reported to credit bureaus before committing.

It’s also important to note that certain types of insurance, such as credit life or credit disability insurance, are tied to loans or credit accounts. While these policies themselves do not affect your credit score, the loans they are associated with do. For example, if you have a loan with credit life insurance and the insurer pays off the loan upon your death, your credit report will reflect the loan’s closure, not the insurance payment. However, if you default on the loan and the insurance fails to cover it, the delinquency will negatively impact your credit score.

Lastly, insurance inquiries, such as those conducted when you apply for a new policy, do not affect your credit score. These are considered "soft inquiries" and are not reported to credit bureaus. However, if an insurer uses a third-party financing option that requires a "hard inquiry," it could temporarily lower your credit score by a few points. Hard inquiries remain on your credit report for two years but only impact your score for the first year. To minimize this, limit applications for financed insurance policies unless necessary.

In summary, while insurance payments typically do not directly impact your credit score, indirect factors like missed payments, financed premiums, and associated loan obligations can play a role. Staying vigilant about timely payments and understanding the terms of your insurance and financing agreements are key to protecting your credit score. Always review your credit report regularly to ensure accuracy and address any discrepancies promptly.

Bestow Life Insurance: An Easy, Affordable Option

You may want to see also

Explore related products

![]()

Types of Insurance Affecting Credit Reports

Insurance itself typically does not directly impact your credit score, as insurance payments are not reported to the major credit bureaus (Equifax, Experian, and TransUnion). However, certain types of insurance and related financial behaviors can indirectly affect your credit report and score. Understanding these nuances is crucial for maintaining a healthy credit profile.

Health Insurance and Credit Reports

Health insurance premiums are generally not reported to credit bureaus, so paying or missing these payments does not directly influence your credit score. However, unpaid medical bills resulting from insufficient insurance coverage can be sent to collections if left unresolved. Collection accounts are reported to credit bureaus and can significantly damage your credit score. To avoid this, ensure timely payment of medical bills and address any discrepancies with your insurance provider promptly.

Auto Insurance and Credit Reports

Auto insurance payments are not reported to credit bureaus, but missed payments or canceled policies due to non-payment can lead to financial consequences. If an unpaid auto insurance bill is sold to a collection agency, it will appear on your credit report and negatively impact your score. Additionally, some insurers use credit-based insurance scores to determine premiums, which are derived from your credit report. While this doesn’t directly affect your credit score, maintaining good credit can lead to lower insurance rates.

Life Insurance and Credit Reports

Life insurance premiums do not directly affect your credit report or score. However, if you have a life insurance policy with a cash value component (e.g., whole life insurance) and take out a loan against it, the loan itself may not be reported. If you fail to repay the loan, the insurer may cancel the policy, and the outstanding balance could be sent to collections, indirectly harming your credit.

Homeowners or Renters Insurance and Credit Reports

Like other insurance types, homeowners or renters insurance payments are not reported to credit bureaus. However, missed payments leading to policy cancellation can result in unpaid claims being sent to collections, which will negatively impact your credit. Additionally, insurers may use your credit report to assess risk and determine premiums, though this does not directly affect your credit score.

Lapsed Policies and Credit Impact

While insurance payments themselves do not build credit, lapsed policies due to non-payment can lead to financial issues that indirectly harm your credit. For example, a lapsed auto insurance policy might result in legal penalties or accidents without coverage, leading to unpaid debts that could be reported to collections. Always maintain active insurance policies and address payment issues promptly to avoid such scenarios.

In summary, insurance payments do not directly contribute to your credit score, but certain insurance-related financial behaviors, such as unpaid bills or canceled policies, can lead to negative entries on your credit report. Staying proactive in managing insurance obligations is key to protecting your credit health.

Understanding SR22 Insurance Requirements in Colorado: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Late Insurance Payments and Credit Damage

Late insurance payments can have a significant impact on your credit score, though the relationship between insurance and credit is not always direct. Typically, insurance payments themselves do not directly contribute to building your credit history, as insurance companies generally do not report on-time payments to the credit bureaus. However, late or missed insurance payments can indirectly damage your credit in several ways. When you fail to pay your insurance premiums on time, the insurance company may cancel your policy, leading to potential financial instability. This instability can affect your ability to manage other credit obligations, which are reported to the credit bureaus.

One of the most direct ways late insurance payments can harm your credit is if the unpaid debt is sent to collections. Insurance companies often work with collection agencies to recover unpaid premiums. Once a debt is in collections, it can appear on your credit report and significantly lower your credit score. Collection accounts remain on your credit report for up to seven years, making it harder to secure loans, credit cards, or even rent an apartment. This negative mark is a clear example of how late insurance payments can indirectly but severely damage your credit.

Another indirect consequence of late insurance payments is the potential for policy cancellation or non-renewal. Without active insurance coverage, you may face legal penalties or financial risks, such as being personally liable for damages in an accident. These financial setbacks can lead to missed payments on other credit accounts, such as loans or credit cards, which are directly reported to the credit bureaus. For instance, if you’re involved in an uninsured accident and face a lawsuit, the resulting financial strain could cause you to fall behind on credit card payments, directly damaging your credit score.

It’s also important to note that some insurance companies may check your credit score when determining your premiums or eligibility for coverage. A damaged credit score resulting from late payments or collections can lead to higher insurance rates or difficulty obtaining coverage. This creates a cycle where late insurance payments contribute to credit damage, which in turn makes insurance more expensive, increasing the likelihood of future financial strain. Therefore, maintaining timely insurance payments is crucial not only for avoiding direct credit damage but also for preserving your overall financial health.

To mitigate the risk of credit damage from late insurance payments, consider setting up automatic payments or reminders to ensure premiums are paid on time. If you’re facing financial difficulties, communicate with your insurance provider to explore payment plans or temporary adjustments to your policy. Addressing the issue proactively can prevent the debt from going to collections and protect your credit score. Additionally, regularly monitoring your credit report can help you identify and address any negative impacts early, ensuring that late insurance payments do not cause long-term harm to your financial standing.

Life Insurance and SSI Disability: How Does OPM Affect You?

You may want to see also

Explore related products

![]()

Insurance Claims and Credit Influence

Insurance claims generally do not directly impact your credit score, as insurance activity is not reported to the major credit bureaus (Equifax, Experian, and TransUnion). Credit scores are primarily influenced by factors such as payment history, credit utilization, length of credit history, types of credit, and new credit inquiries. However, there are indirect ways in which insurance claims can influence your financial situation and, by extension, your creditworthiness. Understanding these connections is crucial for managing your financial health effectively.

One indirect way insurance claims can affect your credit is through unpaid medical bills. If you file a health insurance claim and there are discrepancies or denials, the unpaid medical bills may be sent to collections. Once in collections, these debts are reported to the credit bureaus and can significantly lower your credit score. To avoid this, it’s essential to verify that your insurance provider processes claims correctly and to address any billing issues promptly. Regularly reviewing your Explanation of Benefits (EOB) and communicating with healthcare providers can help prevent unpaid bills from escalating.

Auto insurance claims can also have indirect implications for your credit, particularly if the claim leads to increased premiums. Higher insurance costs may strain your budget, making it harder to manage other financial obligations, such as credit card payments or loans. Missed or late payments on these accounts will negatively impact your credit score. Additionally, if an auto insurance claim results in a totaled vehicle and you need a new car loan, a higher debt-to-income ratio or a poor credit score could affect your ability to secure favorable loan terms.

Another consideration is the relationship between insurance and credit when it comes to credit-based insurance scores. While not the same as credit scores, insurance companies often use credit-based insurance scores to assess risk and determine premiums. Filing frequent insurance claims, especially for incidents that could be perceived as indicative of risky behavior (e.g., multiple auto accidents), may lead to higher premiums. Although this does not directly affect your credit score, it can increase your overall financial burden, potentially making it harder to manage credit obligations.

Lastly, certain types of insurance, such as credit life or credit disability insurance, are tied directly to loans or credit accounts. These policies pay off or cover payments on a loan if the insured dies or becomes disabled. While these policies do not directly improve your credit score, they can protect your credit by ensuring that your loan obligations are met in the event of unforeseen circumstances. However, it’s important to note that purchasing such insurance does not count as a positive factor in your credit history.

In summary, insurance claims do not directly count toward your credit score, but they can indirectly influence your creditworthiness through unpaid bills, increased financial strain, and higher insurance premiums. Proactive management of insurance claims, timely resolution of billing issues, and maintaining a balanced budget are key strategies to protect your credit health while navigating insurance-related financial challenges.

Does Dr. El Khatib Accept Mercy Insurance? Find Out Here

You may want to see also

Explore related products

![]()

Credit-Building Through Insurance Premiums

While traditionally associated with financial protection, insurance can indirectly play a role in building your credit. Here's how:

Timely Premium Payments: The most direct way insurance can impact your credit is through consistent, on-time premium payments. While insurance payments themselves aren't typically reported to credit bureaus, missed payments can lead to debt collection, which will negatively affect your credit score. Conversely, a history of timely payments demonstrates financial responsibility, a key factor considered by lenders.

Bundling and Credit Checks: Some insurance companies may perform a soft credit inquiry when you apply for a policy. This type of inquiry doesn't impact your credit score. However, bundling multiple insurance policies (e.g., auto and home) with the same provider can sometimes lead to discounts and potentially a more favorable view from lenders, as it indicates stability and loyalty.

Credit-Builder Insurance Products: Certain specialized insurance products are designed specifically to help build credit. These policies often involve paying a premium in exchange for a small loan, which is then reported to credit bureaus as you make timely repayments. This can be a viable option for individuals with limited credit history.

Indirect Benefits: Insurance can indirectly contribute to creditworthiness by providing financial security. Having adequate insurance coverage can prevent unexpected expenses from derailing your budget and leading to missed payments on other credit obligations. Additionally, insurance can protect your assets, which can be valuable collateral for loans, potentially improving your borrowing power.

Important Considerations: It's crucial to remember that insurance premiums themselves are not directly reported to credit bureaus. The primary focus should be on maintaining a positive payment history across all your financial obligations. While insurance can indirectly support credit-building efforts, it's not a substitute for responsible credit management practices like keeping credit card balances low and avoiding excessive debt.

By understanding these nuances, you can leverage your insurance choices to contribute to a healthier overall financial profile, which in turn can positively impact your creditworthiness. Remember, building good credit takes time and consistent effort, and insurance can be one piece of the puzzle.

Does Insurance Cover Birth Control? Understanding Your Policy and Benefits

You may want to see also

Frequently asked questions

No, insurance itself does not directly impact your credit score. Credit scores are primarily influenced by factors like payment history, credit utilization, and length of credit history, not insurance coverage.

Generally, paying insurance premiums on time does not directly affect your credit score, as insurance companies typically do not report payments to credit bureaus.

Missed insurance payments can indirectly harm your credit if the insurer sends the debt to collections. Collection accounts are reported to credit bureaus and can negatively impact your score.

Insurance accounts do not typically appear on your credit report unless there is a delinquency or debt sent to collections. Regular insurance payments are not reported to credit bureaus.