Insurance itself does not directly give you a credit inquiry. Credit inquiries typically occur when you apply for credit products like loans or credit cards, as lenders check your credit report to assess your creditworthiness. However, certain insurance-related actions, such as applying for insurance financing or allowing an insurer to perform a credit-based insurance score check, may result in a soft inquiry, which does not impact your credit score. Hard inquiries, which can affect your credit, are generally not associated with insurance unless you’re applying for credit through an insurance provider. Understanding the distinction between soft and hard inquiries is key to managing your credit health while navigating insurance options.

Explore related products

$99.46 $119

$35

What You'll Learn

- Impact on Credit Score: Does checking insurance quotes affect my credit score negatively

- Soft vs. Hard Inquiries: How do insurance inquiries differ from credit checks

- Credit Reporting Agencies: Do insurance searches appear on my credit report

- Insurance Score Factors: How does insurance affect my overall creditworthiness

- Minimizing Credit Impact: Tips to avoid credit damage when shopping for insurance

![]()

Impact on Credit Score: Does checking insurance quotes affect my credit score negatively?

When considering the impact of checking insurance quotes on your credit score, it’s essential to understand how credit inquiries work and their potential effects. In most cases, checking insurance quotes does not negatively impact your credit score. This is because insurance companies typically perform a "soft inquiry" or "soft pull" on your credit report when generating a quote. Soft inquiries do not affect your credit score, as they are not visible to lenders or other third parties and are only used for informational purposes. Unlike hard inquiries, which occur when you apply for credit (such as a loan or credit card), soft inquiries are harmless and do not signal financial risk to credit bureaus.

However, there is a nuance to be aware of. While the initial insurance quote itself will not harm your credit score, the process may change if you proceed to purchase a policy. Some insurance companies may perform a hard inquiry when you finalize the policy, especially for certain types of insurance like auto or home insurance. Hard inquiries can temporarily lower your credit score by a few points, though the impact is usually minimal and short-lived. It’s important to ask the insurance provider whether they will perform a hard or soft inquiry before finalizing any policy to avoid surprises.

Another factor to consider is how frequently you check insurance quotes. While multiple soft inquiries from insurance companies will not hurt your credit score, applying for multiple policies that result in hard inquiries within a short period could have a cumulative effect. Credit bureaus often group multiple hard inquiries for the same type of credit (e.g., loans or insurance) within a short timeframe, treating them as a single inquiry to minimize the impact. However, excessive hard inquiries can still raise red flags for lenders, potentially affecting your creditworthiness.

To protect your credit score while shopping for insurance, be strategic. First, confirm whether the insurer uses a soft or hard inquiry for quotes and policy finalization. Second, limit the number of applications that result in hard inquiries. Finally, focus on comparing quotes within a short period, as credit bureaus typically recognize this as rate shopping and minimize the impact on your score. By understanding these distinctions, you can shop for insurance confidently without worrying about unnecessary damage to your credit.

In summary, checking insurance quotes generally does not negatively impact your credit score because most insurers use soft inquiries. However, finalizing a policy may involve a hard inquiry, which could have a minor, temporary effect. By staying informed and planning your insurance shopping, you can maintain a healthy credit score while finding the best coverage for your needs. Always ask questions and clarify the inquiry type with insurers to make informed decisions.

Cancer and Life Insurance: What's the Impact?

You may want to see also

Explore related products

![]()

Soft vs. Hard Inquiries: How do insurance inquiries differ from credit checks?

When it comes to understanding how insurance inquiries impact your credit, it’s essential to distinguish between soft inquiries and hard inquiries. Both types of inquiries are used by insurers and lenders to assess your financial reliability, but they differ significantly in their purpose, impact, and how they appear on your credit report. Insurance inquiries typically fall into the category of soft inquiries, which do not affect your credit score, whereas hard inquiries, often associated with loan or credit applications, can temporarily lower your score.

Soft inquiries occur when a company checks your credit report for informational purposes, such as pre-approval offers, background checks, or insurance quotes. Insurance companies often perform soft inquiries to evaluate your credit-based insurance score, which helps them determine your risk level as a policyholder. This score is different from your traditional credit score but is derived from similar credit report data. Importantly, soft inquiries do not harm your credit score because they are not tied to a specific credit application. They are invisible to lenders and only visible to you when you access your credit report. This means you can shop around for insurance quotes without worrying about damaging your credit.

On the other hand, hard inquiries happen when you apply for credit, such as a loan, credit card, or mortgage. These inquiries indicate that you’re seeking to take on new debt, which can be seen as a higher credit risk. Hard inquiries do impact your credit score, typically causing a slight decrease that lasts for about a year. Unlike soft inquiries, hard inquiries are visible to lenders and can influence their decision to extend credit to you. Insurance applications generally do not result in hard inquiries unless you’re applying for a policy that involves borrowing, such as certain life insurance policies with a loan component.

The key difference between insurance inquiries and credit checks lies in their purpose and consequences. Insurance inquiries are primarily soft inquiries used to assess your risk as a policyholder, not to evaluate your creditworthiness for a loan. They provide insurers with insights into your financial behavior, such as payment history and debt management, which can affect your insurance premiums. In contrast, credit checks involving hard inquiries are directly tied to borrowing decisions and have a tangible impact on your credit score. Understanding this distinction helps you navigate financial decisions without unnecessary worry about your credit health.

In summary, insurance inquiries are typically soft inquiries that do not affect your credit score, while hard inquiries, associated with credit applications, can temporarily lower it. Insurance companies use soft inquiries to gauge your risk as a policyholder, whereas hard inquiries are reserved for situations where you’re seeking new credit. By recognizing the difference between these two types of inquiries, you can confidently explore insurance options without fearing negative consequences for your credit. Always review your credit report regularly to ensure accuracy and understand how different financial activities impact your credit profile.

Understanding DIF Insurance: Coverage, Benefits, and How It Protects You

You may want to see also

Explore related products

![]()

Credit Reporting Agencies: Do insurance searches appear on my credit report?

When it comes to understanding whether insurance searches appear on your credit report, it’s essential to know how credit reporting agencies (CRAs) operate. CRAs, such as Equifax, Experian, and TransUnion, collect and maintain financial information about consumers, including credit inquiries, payment history, and account details. Insurance searches, however, typically do not appear on your credit report as a hard inquiry that could impact your credit score. Most insurance companies perform a "soft inquiry" when assessing your risk profile, which does not affect your credit score or appear on your credit report in a way that lenders or other parties can see.

Soft inquiries, or soft pulls, are different from hard inquiries because they are not tied to a credit application. Insurance companies often use these inquiries to evaluate your financial responsibility and predict potential risks. For example, they may review your credit history to determine if you have a pattern of late payments or high debt levels, which could indicate a higher likelihood of filing claims. While this information helps insurers set premiums, it does not leave a visible mark on your credit report that could concern lenders or other creditors.

It’s important to note that not all insurance searches are the same. In some cases, such as when applying for life insurance or certain types of property insurance, insurers may request a more detailed review of your credit history. However, even in these instances, the inquiry is still typically classified as a soft pull. If an insurance company does perform a hard inquiry, it would be rare and usually only occurs with your explicit consent. Hard inquiries from insurance companies are not standard practice and are generally limited to specific high-value policies.

To ensure clarity, consumers can review their credit reports periodically to understand what information is being reported. If you notice an unexpected hard inquiry related to insurance, it’s advisable to contact the insurance company and the credit reporting agency to investigate. While insurance searches generally do not impact your credit report in a negative way, staying informed about your credit profile is always a good practice. Regularly monitoring your credit report can help you identify inaccuracies or unauthorized inquiries promptly.

In summary, insurance searches typically do not appear on your credit report as hard inquiries that could affect your credit score. Most insurers use soft inquiries to assess risk, which do not impact your credit profile. While exceptions exist, particularly for certain types of insurance policies, these are rare and usually require your consent. Understanding the difference between soft and hard inquiries can help you navigate how insurance companies interact with your credit information and ensure that your credit report remains accurate and reflective of your financial behavior.

Retirement and Life Insurance: Using Cash Value for Your Future

You may want to see also

Explore related products

![]()

Insurance Score Factors: How does insurance affect my overall creditworthiness?

Insurance can indirectly influence your overall creditworthiness, though it does not directly impact your credit score in the same way that payment history or credit utilization does. However, certain insurance-related factors can affect your financial profile and, by extension, your creditworthiness. Understanding these connections is crucial for managing your financial health effectively.

One key factor is payment history on insurance premiums. While insurance payments are not typically reported to credit bureaus, missed or late payments can lead to policy cancellations or collections. If an unpaid insurance bill is sent to collections, it will appear on your credit report and negatively impact your credit score. Collections accounts are considered derogatory marks and can remain on your credit report for up to seven years, significantly lowering your creditworthiness. Therefore, consistently paying your insurance premiums on time is essential to avoid such consequences.

Another factor is insurance claims history. Frequent or high-value insurance claims, particularly in auto or home insurance, can signal higher risk to insurers. While this does not directly affect your credit score, it can lead to higher premiums or difficulty securing coverage. Insurers may share claims data with industry databases, such as the Comprehensive Loss Underwriting Exchange (CLUE), which could indirectly influence your financial profile. Lenders may consider your insurance risk when evaluating your overall reliability, especially if they perceive a pattern of risky behavior.

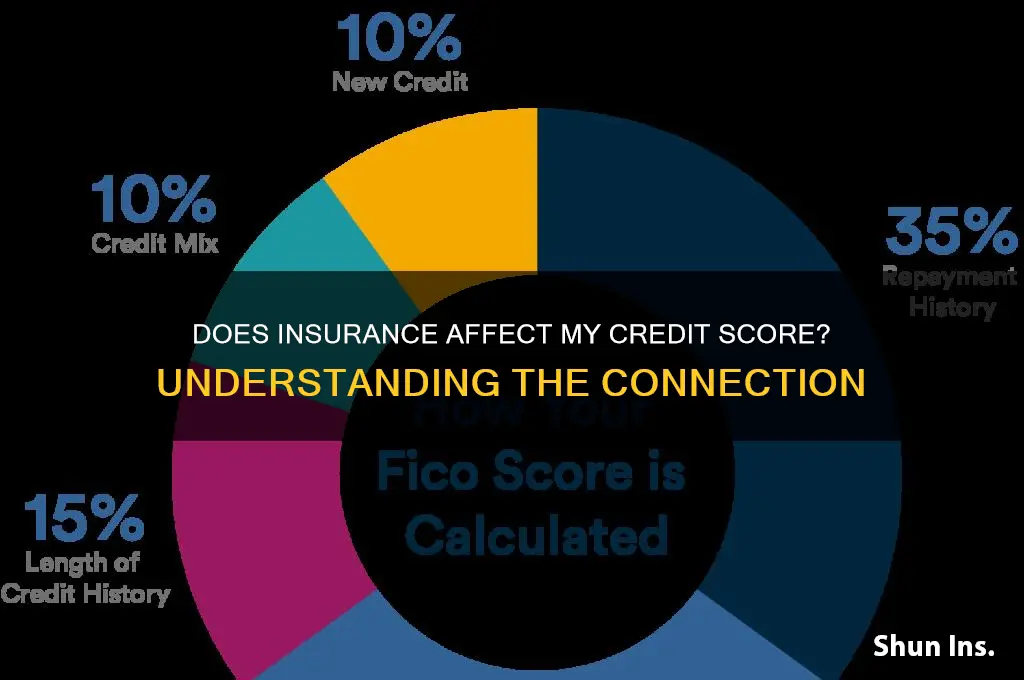

Credit-based insurance scores are also worth noting. Insurers often use these scores, which are similar to credit scores but tailored to predict insurance risk. While they do not directly impact your creditworthiness, they are derived from your credit report data. Factors like payment history, debt levels, and credit age play a role in these scores. Maintaining a strong credit profile can thus improve your insurance score, potentially leading to lower premiums and better coverage terms.

Lastly, bundling insurance policies can indirectly benefit your creditworthiness. By consolidating policies (e.g., auto and home insurance) with one provider, you may save money, reducing your overall financial burden. Lower expenses can improve your ability to manage debt and make timely payments, positively influencing your credit score. Additionally, some insurers offer discounts for bundling, freeing up funds that can be allocated to debt repayment or savings, further enhancing your financial stability.

In summary, while insurance does not directly contribute to your credit score, factors like premium payment history, claims activity, credit-based insurance scores, and policy bundling can indirectly affect your creditworthiness. Proactively managing these aspects ensures that your insurance decisions support, rather than hinder, your overall financial health.

Employer Life Insurance: A False Sense of Security?

You may want to see also

Explore related products

![]()

Minimizing Credit Impact: Tips to avoid credit damage when shopping for insurance

When shopping for insurance, it’s essential to understand how the process can impact your credit score. Insurance companies often perform a "soft inquiry" or "soft pull" on your credit report to assess your financial reliability. Unlike a "hard inquiry," which can lower your credit score, a soft inquiry does not affect your credit. However, not all insurers handle credit checks the same way, and some actions you take during the shopping process could inadvertently lead to credit damage. To minimize credit impact, start by confirming with insurers whether they use a soft or hard inquiry. Many insurance companies explicitly state that their initial quotes involve only soft pulls, which is a safer option for your credit. Always ask before proceeding to ensure you’re not risking unnecessary harm.

Another effective strategy is to limit the number of insurance applications you submit within a short period. While comparing quotes is smart, each formal application could trigger a credit check. Instead of applying with multiple insurers, narrow down your options to two or three providers after researching their offerings. Use online comparison tools or speak with agents to gather preliminary information without initiating a credit check. This way, you can make informed decisions without exposing your credit score to multiple inquiries. Additionally, time your applications strategically—if you know you’ll be applying for a loan or mortgage soon, avoid insurance shopping simultaneously, as multiple hard inquiries in a short timeframe can compound credit damage.

If you’re working with an insurance agent or broker, communicate your concerns about credit impact upfront. A knowledgeable professional can guide you through the process, ensuring that only soft inquiries are performed during the initial stages. They can also help you understand which insurers are more credit-friendly and how to structure your applications to minimize risk. Transparency with your agent can save you from unintended credit consequences and streamline the shopping experience. Don’t hesitate to ask questions and advocate for your financial well-being throughout the process.

Finally, monitor your credit report regularly to catch any unexpected hard inquiries or discrepancies. Free credit monitoring services or annual credit reports from major bureaus can help you stay informed. If you notice a hard inquiry from an insurer that wasn’t disclosed, contact the company immediately to clarify and, if necessary, dispute the inquiry. Being proactive about monitoring your credit ensures that you can address issues promptly and maintain a healthy credit profile while shopping for insurance. By combining these strategies, you can navigate the insurance market confidently while safeguarding your credit score.

Life Insurance for Military Service Members: What You Need to Know

You may want to see also

Frequently asked questions

Yes, applying for certain types of insurance, such as auto or home insurance, may result in a soft credit inquiry. This type of inquiry does not affect your credit score.

No, insurance-related credit inquiries are typically soft inquiries, which do not impact your credit score. Hard inquiries, which can lower your score, are usually associated with loans or credit cards.

Soft credit inquiries from insurance applications do not appear on your credit report and are not visible to lenders or other third parties.

It depends on the insurer and the type of insurance. Some insurers may not check your credit at all, while others may require a soft inquiry. You can ask the insurer about their policy before applying.