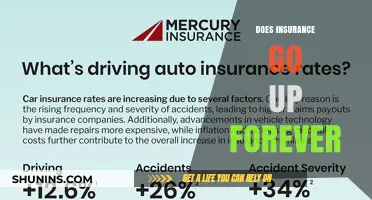

Car insurance rates typically increase after an accident, especially if the policyholder is at fault. The rate increase depends on several factors, including the insurance company, the state, the car, the accident's severity, and whether the policyholder was at fault. Accidents that are not the policyholder's fault may still increase their insurance rate, as they indicate a higher likelihood of future accidents. Some insurance companies offer accident forgiveness programs, which waive rate increases for certain types of accidents, such as the policyholder's first accident or smaller accidents.

| Characteristics | Values |

|---|---|

| Insurance rates after an accident | Tend to go up, especially if the policyholder is at fault |

| Factors affecting insurance rates | The insurance company, the state, the car, the severity of the collision |

| Accident forgiveness programs | Offered by some insurers to waive the first at-fault accident loss |

| Comprehensive claims | May increase insurance rates as they indicate a higher risk of filing more claims |

| Average rate increase after an accident | 10% or less if not at fault, 45% if at fault; rates can go up as much as 60% or as little as 26% |

Explore related products

What You'll Learn

![]()

Accident forgiveness programs

Car insurance rates typically increase after an accident, especially if the accident was your fault. The increase in insurance rates after an accident depends on several factors, including your insurance company, the state you live in, the type of accident, the car you drive, and the severity of the collision. On average, insurance rates increase by 45% if the accident was your fault, and by 10% or less if you were not at fault.

Accident forgiveness is not available in all states, and not all insurance companies offer it. For example, accident forgiveness is not available in California, Connecticut, or Massachusetts. Some insurance companies that offer accident forgiveness include Progressive, Lemonade, Geico, and Erie. Progressive offers accident forgiveness for claims of $500 or less, while Lemonade offers accident forgiveness for drivers with a clean driving history for a surcharge of $100 per year.

It is important to note that accident forgiveness is typically only valid for one collision. If you are in subsequent accidents, your insurance rate will likely increase. Additionally, if you switch insurance companies, your new insurer will factor in any recent accidents when determining your rate.

Switching Insurance Carriers: A Guide

You may want to see also

Explore related products

![]()

At-fault accidents

An accident, especially one where you are at fault, can have a significant impact on your insurance rates. An at-fault accident is viewed by insurance companies as an indicator of a higher risk of future accidents and claims. As a result, insurance companies will often increase rates for at-fault accidents, with the increase depending on various factors.

The severity of the accident is an important factor in determining the impact on insurance rates. An at-fault accident that results in injuries or significant property damage is likely to lead to a larger increase in insurance rates compared to a minor fender bender. The type of insurance policy and the specific insurance company also play a role in the rate increase. Some companies may raise rates by a small amount, while others may increase rates by a significant percentage for at-fault accidents.

The state in which the accident occurs is another crucial factor. Different states have varying thresholds for determining total loss and repair requirements, which can impact insurance rates. For example, in Nevada, the threshold for repairs is 65% of the fair market value of the vehicle. Additionally, each state has different regulations regarding accident forgiveness programs, which can waive rate increases for at-fault accidents. These programs are often offered as endorsements to the insurance policy and may vary in their specific terms and conditions.

The length of time an accident stays on your record also varies by state. On average, an at-fault accident remains on your record for three to five years, but this can range from one year in Pennsylvania to six years in Massachusetts. During this time, insurance companies can review your driving record and take the accident into account when determining your insurance rates.

It is worth noting that not all insurance companies increase rates after an at-fault accident. Some companies, like Travelers, offer lower rates for drivers with an at-fault accident on their record. Additionally, switching to the cheapest insurer in your state after an accident can help mitigate the impact on your insurance rates. Comparing insurance rates from several companies and exploring accident forgiveness programs can help drivers find the most affordable rates after an at-fault accident.

Understanding Insurance: Calendar Year Coverage

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

![]()

Not-at-fault accidents

In most cases, auto insurance rates do not rise after a no-fault accident. However, insurance policies vary, and rates can increase depending on the insurer, the state, and the circumstances of the accident.

In Florida, for example, motorists are required to carry Personal Injury Protection (PIP) insurance. This no-fault insurance system provides immediate benefits to accident victims, covering medical expenses and lost wages, regardless of who is at fault. While fault is irrelevant in terms of PIP coverage, it can impact other aspects of compensation, such as property damage and non-economic damages. Importantly, Florida prohibits insurance companies from raising rates solely based on an accident that was not the policyholder's fault.

In other states, the level of fault assigned in an accident can influence insurance rates. For example, some states operate under comparative negligence laws, where shared liability is considered when determining fault. Even if you are primarily not at fault, your rates could still be affected, especially if the other driver has little or no insurance. In such cases, your insurer may need to dip into your uninsured/underinsured motorist coverage, which could result in higher premiums.

Additionally, factors such as your previous driving record, the severity of the accident, and the number of claims made within a short period can influence insurance rates, even in no-fault situations. Multiple claims within a three-year period are often considered high-frequency and can lead to higher premiums, regardless of fault.

It is worth noting that some insurance companies offer accident forgiveness coverage, which may prevent rate hikes after a no-fault accident. However, obtaining this coverage may come at an additional cost, and the terms can vary among insurers.

Civil Infractions: How They Impact Your Insurance Rates

You may want to see also

Explore related products

![]()

Comprehensive claims

Comprehensive insurance is an optional addition available with most car insurance policies. It covers damage caused by or related to theft, animals, vandalism, weather, car fire, chipped/cracked windshield, and acts of nature. Comprehensive claims tend to cost much less than collision or liability insurance claims.

However, comprehensive claims do not increase insurance rates as much as at-fault accident claims. Comprehensive claims are considered to be outside the driver's control, and so they are not viewed as negatively by insurance companies as at-fault claims.

Insurance companies use your claims history to decide whether to sell you a policy and how much to charge you. They can access your claims history through the Comprehensive Loss Underwriting Exchange (CLUE) to learn about your home or auto claims, even if they were filed with another insurance company.

To avoid rate increases, some people choose not to report accidents and pay for their losses out of pocket. However, this is generally not recommended, as your insurance company will not be able to defend you in the event of a lawsuit.

Aegis Insurance: Surplus Lines Carrier Status

You may want to see also

Explore related products

![]()

High-risk drivers

A total loss accident is a severe crash that results in the total destruction of a vehicle, often caused by another driver's negligence. These accidents can have devastating consequences, including injuries and even fatalities. While insurance is meant to provide financial protection in such situations, it is not uncommon for insurance providers to deny or undervalue claims, impacting policyholders financially.

After a total loss accident, high-risk drivers may experience significant increases in their insurance rates. This is because insurers view these drivers as having a higher probability of being involved in future accidents and filing additional claims. As a result, high-risk drivers are often charged higher premiums to compensate for the perceived increased risk.

However, not all insurance companies take the same approach. Some insurers specialize in providing coverage for high-risk drivers, offering rates that are significantly lower than the national average. These companies recognize that high-risk drivers may have improved their driving habits or taken steps to reduce their risk. Additionally, certain insurers offer accident forgiveness programs, which prevent rates from increasing after minor accidents or a customer's first at-fault accident.

To find affordable insurance, high-risk drivers should compare rates from multiple companies, taking advantage of online tools that provide personalized quotes. They should also consider insurers that offer accident forgiveness and explore options for reduced usage discounts, such as those available to drivers who store their vehicles for extended periods. By being proactive and shopping around, high-risk drivers can find coverage that meets their needs without breaking the bank.

Driving Without Insurance: Jail Time or Not?

You may want to see also

Frequently asked questions

Yes, car insurance rates typically go up after an accident, especially if you were at fault. The increase in insurance rates depends on several factors, including the insurance company, the state you live in, the car you drive, and the severity of the collision.

A total loss occurs when a vehicle is damaged to the extent that the cost of repairing it exceeds its fair market value. The threshold for repairs is typically around 65% of the vehicle's fair market value.

The length of time an accident stays on your record varies by state, typically ranging from one to six years. During this period, your insurance rates may be impacted.

Some insurance companies offer accident forgiveness programs that waive the surcharge for the first at-fault accident or small accidents with claims below a certain amount. Shopping around for insurance providers and comparing rates can also help you find better rates after a total loss.

The increase in insurance rates after a total loss can vary significantly. According to NerdWallet's analysis, rates can go up by as little as 26% or as much as 60% for at-fault accidents. The increase also depends on the specific circumstances of the accident and your insurance provider.