Whether or not a citation with no points will increase your insurance rate depends on several factors, including the type of violation, your driving record, location, and insurance company. While insurers do not directly factor points into your car insurance rate, accumulating a significant number of points due to multiple violations may result in an increase. Certain states, such as Arizona, California, and Oregon, issue demerit points for traffic tickets, which can directly impact your insurance rates. Minor violations, such as speeding less than 10 miles per hour over the limit, may not affect your insurance rates, especially if you have a clean driving record. However, more serious violations, such as DUIs or reckless driving, are likely to result in higher insurance premiums as they indicate a higher risk. Ultimately, the impact of a citation on your insurance depends on the specific circumstances and the policies of your insurance provider and state regulations.

| Characteristics | Values |

|---|---|

| Does a citation without points impact insurance rates? | It depends on the state and insurer, but generally, insurers will surcharge a driver with a single moving violation in the past 3-5 years. |

| How much do insurance rates increase? | Insurance rates could increase by 30-95% depending on the type of violation and location. |

| How long do tickets stay on your record? | This depends on the state and the nature of the violation. Insurers typically consider violations on a driver's record for 3 years, but some violations may impact rates for up to 10 years. |

| How to avoid insurance rate increases? | Some states allow drivers with their first violation to keep minor infractions off their record by completing traffic school or a driver safety class. |

Explore related products

What You'll Learn

![]()

The impact of a single citation

The impact of receiving a citation or ticket depends on several factors, including the type of violation, the state in which it occurred, and the driver's insurance company, driving record, and insurance history.

In some states, insurers are forbidden from considering texting or red-light camera tickets when determining rates. However, in states where this is not banned, insurers may treat these as minor moving violations, which can lead to an increase in insurance rates. Similarly, while parking tickets typically do not affect insurance rates as they are not moving violations, failure to pay them can result in consequences beyond a rate increase, such as the state refusing to renew your vehicle registration.

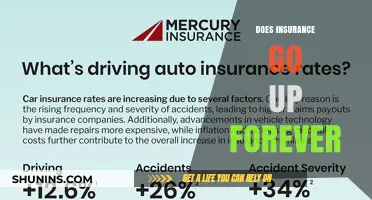

Speeding tickets, one of the most common traffic violations, can have varying impacts on insurance rates. Some states add points to a driver's license for speeding, with the number of points depending on the severity of the infraction. These points can remain on a driver's record for a year or even permanently. While insurance companies do not directly factor points into insurance rates, accumulating a significant number of points can lead to an increase in rates due to the number of violations. Additionally, insurers may consider drivers with higher points as high-risk and set their rates accordingly.

The impact of a single speeding ticket on insurance rates can vary. Some insurers do not raise rates after a single speeding violation, especially if it is the driver's first offense and their driving record is otherwise clean. In such cases, the ticket may not have any impact on insurance costs. However, other insurers may surcharge a driver with a single moving violation within the past three to five years, resulting in a loss of a good driver discount and potentially higher rates. The increase in insurance costs due to a single citation can be significant, ranging from 30% to 95% or even doubling in some cases.

It is important to note that the impact of a citation on insurance rates can vary by state and insurer, and it is always advisable to consult with a legal professional to determine the best course of action after receiving a citation.

Georgia's Penalties for Driving Without Insurance

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide - Property and Casualty Exam Secrets, Practice Test Questions, Detailed Answer Explanations [2nd Edition]](https://m.media-amazon.com/images/I/71fBYXIP4iL._AC_UY218_.jpg)

![]()

State-based variations

State laws vary, and this impacts how insurers treat violations. For example, some states forbid insurance companies from considering texting tickets when setting rates, while others treat them as minor moving violations, which may result in a rate increase. Similarly, some states ban insurance companies from using red-light camera tickets when determining rates, while others treat them as minor moving violations, which may lead to higher insurance rates.

The number of points added to a license for a speeding violation differs by state. For instance, Arizona assigns three points for speeding, while Nevada's point system is more nuanced, ranging from one to five points based on speed. Most states add points to a driver's record for each violation, and insurers consider drivers with higher points as high-risk, potentially setting higher rates. However, insurance companies do not directly factor points into car insurance rates. Instead, rates may increase due to the number of violations on a driver's record.

The length of time a ticket stays on a driving record varies by state and the severity of the violation. For example, in Nevada, demerit points remain on a driver's record for one year, while the speeding ticket itself remains on the permanent record. Insurers typically consider violations on a driver's record for three years, though certain violations, like a DUI in California, can impact rates for up to ten years.

The impact of a speeding ticket on insurance rates also depends on state laws and the insurer. Some states do not increase rates for a first-time speeding violation, while others may offer a "good driver" discount that can be lost due to a violation. The increase in insurance rates also varies by state; for example, a Pennsylvania driver may pay 15% more after a speeding ticket, while a North Carolina driver could pay 50% more.

UPC Insurance: Admitted or Not?

You may want to see also

Explore related products

![]()

Driving record implications

The impact of a citation on your insurance depends on a variety of factors, including the type of violation, the state in which it occurred, and your driving record. While a single citation may not always result in an insurance increase, multiple violations or more serious infractions can have significant implications for your insurance rates and driving record.

In terms of driving record implications, it's important to understand that insurance companies typically consider your driving record for three years after an infraction. During this period, you may not be eligible for "good driver" discounts, which can result in higher rates. Additionally, certain violations, such as a DUI, can impact your insurance rates for even longer periods, such as 10 years in California.

The number of points on your license is a significant factor in determining the impact on your insurance. While insurance companies do not directly factor points into your rate, a higher number of points indicates a higher number of violations. As a result, insurers may consider you a higher-risk driver and increase your insurance rates accordingly.

The type of violation also plays a crucial role in determining the impact on your insurance. Minor offenses, such as speeding less than 10 miles per hour over the limit, may not affect your insurance rates if your driving record is clean. On the other hand, more serious violations, such as DUI or reckless driving, can result in substantial insurance increases and may even lead to difficulty finding insurance coverage.

The state in which the citation occurs also influences the impact on your insurance. Some states, like Arizona, California, and Oregon, issue demerit points for certain violations, which can directly affect your insurance rates. Other states may have different thresholds for when a speeding ticket impacts your insurance, with some states considering infractions of less than 15 miles per hour over the limit as non-rate-affecting.

In summary, while a single citation may not always result in an insurance increase, it can have significant driving record implications. Multiple violations or more serious infractions will likely result in higher insurance rates and may impact your insurance for several years. The number of points on your license, the type of violation, and the state in which it occurred all play a role in determining the ultimate impact on your insurance.

Workers' Comp: Self-Insured or Carrier-Insured?

You may want to see also

Explore related products

![]()

Insurer's policies

While insurers do not directly factor points into car insurance rates, accumulating a significant number of points due to violations can lead to an increase in insurance rates. This is because insurers consider drivers with higher points as high-risk and may set higher premiums accordingly. The impact of points on insurance rates also depends on the specific policies and practices of the insurer and the state in which the driver resides.

Some states add points to a driver's license for each traffic violation, with the number of points varying based on the severity of the violation. For example, minor violations like speeding by a small margin may result in 1-3 points, while major violations such as DUI or reckless driving can lead to 4 or more points. These points remain on a driver's record for a certain period, typically one year, and can affect insurance rates during that time.

Insurers typically consider violations on a driver's record for three years after the infraction, and in some cases, the impact on insurance rates can last even longer. For instance, a DUI violation in California will impact a driver's insurance rate for ten years. While violations may no longer count after three years, drivers usually have to wait for five years after their last violation to be eligible for "good driver" discounts.

The presence of points on a driver's license can make finding cheap insurance more challenging. However, some insurance providers may offer specialized rates for drivers with points or those who have completed speed awareness courses. Comparing different insurers and their policies regarding points and violations is essential for managing insurance costs.

Additionally, it is worth noting that not all violations result in points, and some states may not consider points when determining insurance rates. For example, parking tickets are typically not considered moving violations and do not affect insurance rates unless they remain unpaid, leading to issues with vehicle registration.

Insurance: When Trailers Need Coverage

You may want to see also

Explore related products

![]()

Discounts and surcharges

While insurers don't directly factor points into your car insurance rate, your rate is likely to increase if you've accumulated a lot of points due to the number of violations on your record. Insurers consider drivers with more points on their license as high-risk and may set their rates accordingly.

Insurers offer discounts to customers who they deem to be low-risk. For example, if you work from home and drive very little, your insurer may consider you to be less likely to have accidents and file claims, and will therefore charge you less for coverage. Similarly, if you have a child with impressive grades, you may be eligible for a "good student" discount. Other common discounts include those for customer loyalty, bundling multiple policies, early renewal, insuring multiple cars, low mileage, anti-lock brakes, anti-theft devices, and more.

It's worth noting that insurance companies are not always transparent about the exact amount that these discounts will save you. Some companies provide a list of discounts but do not specify the monetary value of each. However, you can still benefit from significant savings by strategically applying multiple discounts.

On the other hand, surcharges are fees added to your insurance premium, usually as a result of a ticket or at-fault accident. Surcharges are meant to cover the additional cost or risk of insuring a driver with a poor driving record. For example, if you receive a speeding ticket, you may lose any "safe driver" discounts you previously had, and your insurance rates may increase. The amount of the increase depends on various factors, including the insurer, the state, the number of tickets, and the severity of the violation.

While a single traffic ticket can lead to a surcharge, multiple violations on your record can significantly impact your insurance rates. For instance, a speeding ticket can result in a fine of about $150, but it can also increase your insurance costs by $540+ per year for three years, amounting to over $1,600 in insurance penalties alone. Therefore, it is essential to be aware of the potential financial implications of traffic violations and to proactively seek out applicable discounts to mitigate these costs.

Insuring Fleet Trucks: Which Carrier?

You may want to see also

Frequently asked questions

It depends on the state and insurer, but generally, yes, a citation will increase your insurance costs. Even a simple ticket that only adds one insurance point to your record can result in a 30% increase in your insurance costs.

Speeding 10 mph or less over the speed limit under 55 mph.

Illegal passing, following too closely, accidents resulting in property damage between $2,300 and $3,850, and speeding 10 mph or less over a speed limit of 55 mph or higher.

Yes, a DUI conviction will likely increase your insurance premium as it makes you a riskier customer to insure. Some insurers won't even sell a policy to someone with a DUI.

Speeding tickets may drop off your driving record within 3-5 years, depending on how long your state keeps violations on its records.