New York has some of the highest car insurance rates in the country, with the average cost of car insurance being $4,021 per year for full coverage and $1,719 per year for minimum coverage. There are several reasons for this, including the state's no-fault insurance laws, high healthcare costs, and extra coverage requirements. Comprehensive insurance is a type of coverage that pays for repairs or replacements if your car is stolen or damaged in an accident you cause. While it is not mandatory in New York, it can provide valuable protection if you live in an area with a high risk of accidents, thefts, or claims. Factors such as your age, driving record, credit score, and vehicle type will also influence your insurance rates.

| Characteristics | Values |

|---|---|

| Average cost of car insurance in New York | $4,021 per year for full coverage and $1,719 per year for minimum coverage |

| Average cost of car insurance in the US | $1,296 for full coverage and $595 for minimum coverage |

| Factors that influence insurance rates | Age, driving record, credit score, vehicle type, location, and health care costs |

| Impact of accidents on insurance rates | Accidents may increase insurance rates, especially if they result in injuries, fatalities, or significant damage |

| No-fault laws in New York | Insurance companies pay for medical bills and lost wages up to a certain amount, regardless of fault |

| DUI impact | A DUI on your record can significantly increase insurance rates |

Explore related products

![Catalogue of Insurance Publications, American and Foreign: a Comprehensive List of Works Upon All Classes of Insurance, by Well Known Authors of All Countries 1911 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

What You'll Learn

![]()

No-fault insurance laws

In the state of New York, car insurance is generally more expensive than in other states. This is partly due to the state's no-fault insurance laws. No-fault insurance laws are designed to protect the insured. In a no-fault state, your insurance company will pay for your medical bills and lost wages (up to a certain amount), regardless of who caused the accident. This means that even if you are not at fault, your insurance company will still pay for your expenses. This can result in higher premiums for safe drivers who have not caused any accidents.

To receive the benefits of no-fault insurance in New York, the accident must occur within the state, and the driver must have an insurance policy issued by a New York insurance provider. Additionally, no-fault insurance does not cover motorcycles or motorcyclists. It's important to note that New York allows injury victims to pursue a fault-based system if their injuries are deemed "serious" under the law, such as an injury that prevents a person from performing normal daily activities for at least 90/180 days after the accident.

The impact of an accident on insurance rates in New York can vary depending on the insurance company and the specific policy. New York limits insurance companies' ability to impose surcharges on customers following car accidents. Provided that the claim is filed under comprehensive coverage and the damages are less than $2,000 with no physical injuries or fatalities, the insurance company is prohibited from increasing the base premium. However, if a customer is involved in two or more accidents, regardless of the amount of damage, their premiums are likely to increase.

Denied Claims: Insurance Payment Refusals

You may want to see also

Explore related products

![]()

High health care costs

In New York, insurance companies are prohibited from increasing your base premium after a car accident, provided that your claim was filed under your comprehensive coverage, damages were less than $2000, and there were no physical injuries or fatalities. However, if you are involved in two or more accidents, your premiums will likely increase. New York is a no-fault state, meaning that insurance companies must pay for medical bills and lost wages (up to a certain amount) regardless of who caused the accident. This can lead to higher premiums for safe drivers. Additionally, New York requires drivers to have a minimum amount of liability insurance, and rates are typically higher for younger drivers and those with a history of accidents or DUIs.

Now, onto the topic of high healthcare costs. The United States spends twice as much per person on healthcare as similar nations. High healthcare costs are a burden for many American families and are a top financial concern for adults. A significant portion of adults worries about affording unexpected medical bills, the cost of healthcare services, prescription drug costs, and long-term care. These costs can lead individuals to postpone or forgo needed medical care, impacting their health and potentially leading to medical debt. Lowering out-of-pocket healthcare expenses is a priority for many, and healthcare affordability is an important issue in elections.

Several factors contribute to high healthcare costs in the US. Firstly, the US health insurance system is largely voluntary, while other large and wealthy nations have compulsory systems. This results in a smaller risk pool and higher costs for those who choose to participate. Additionally, the US federal and state governments have done relatively less to regulate or negotiate prices for medical services and prescription drugs compared to other countries, leading to higher prices for brand-name drugs, hospital procedures, and physician care. Socioeconomic conditions, income inequality, and lifestyle factors, such as diet and physical activity, also play a role in higher spending and worse health outcomes.

An aging population, labor pressures, and new high-cost prescription drugs are expected to drive further increases in healthcare spending. The pandemic has also had direct and indirect effects on the healthcare system, with COVID-19-related costs and shifts in healthcare utilization. Additionally, healthcare prices increased by 2.9% in 2021, and a rebound in utilization is projected to put upward pressure on prices in the coming years. High healthcare costs disproportionately affect those with lower incomes and those in worse health, but the challenges are pervasive across the US, impacting even those with private health insurance through their employers.

Insurance Requirements for Plow Carriers

You may want to see also

Explore related products

![]()

Driving violations

New York operates on a points-based system, where different traffic offenses carry different point values. For instance, a minor speeding violation might add three points to your record, while more severe offenses, such as reckless driving, can add five points or more. Accumulating points on your driving record can lead to increased insurance premiums as insurance companies closely monitor drivers' records, and the accumulation of points signals that you are a higher risk. Consequently, your insurance premiums can increase significantly. It is not uncommon for insurance rates to spike after just one or two traffic violations, depending on the severity of the offenses and your overall driving history.

The impact of traffic violations on car insurance rates is not limited to the immediate aftermath of the violation. Points typically stay on your driving record for a certain period, usually 18 months to 3 years, depending on the violation. During this time, insurance companies will take them into account when calculating your rates. However, as the points age and eventually expire, their impact on your rates will diminish.

The New York Department of Motor Vehicles (DMV) operates the points system to track and penalize drivers who commit traffic violations. The more serious the offense, the higher the number of points assigned. Points are assigned for a wide range of violations, including speeding, running red lights, reckless driving, and driving under the influence (DUI). The number of points assigned for each violation varies depending on its severity. For example, speeding in a school zone may result in higher points than regular speeding.

There are a few strategies to mitigate the impact of traffic violations on your insurance rates in New York. One effective strategy is to take a defensive driving course. New York offers a Point and Insurance Reduction Program (PIRP), which allows drivers to complete an approved defensive driving course to reduce the points on their driving record. By successfully completing the course, you can remove up to four points from your record, which can lead to a reduction in your insurance premiums. Defensive driving courses demonstrate to insurance companies that you are taking proactive steps to improve your driving skills and reduce risk, and many insurers offer discounts to drivers who complete such courses.

Another approach to consider when dealing with traffic violations is contesting the violation. In New York, you have the right to challenge a traffic ticket in court. While this process can be time-consuming and may require legal assistance, successfully contesting a ticket can prevent points from being added to your driving record, thereby avoiding potential increases in your insurance rates. An attorney who understands the intricacies of traffic law in New York can be invaluable in presenting your case effectively, potentially leading to a dismissal or reduction of charges.

Insurance Rates and SR22: What's the Connection?

You may want to see also

Explore related products

![]()

Vehicle type

In the state of New York, vehicle insurance is mandatory and the type of insurance depends on the vehicle. For instance, motorcycles are registered for one year and all motorcycle registrations expire on April 30. Unlike other vehicles, you are not required to surrender your plate if you terminate your motorcycle liability insurance.

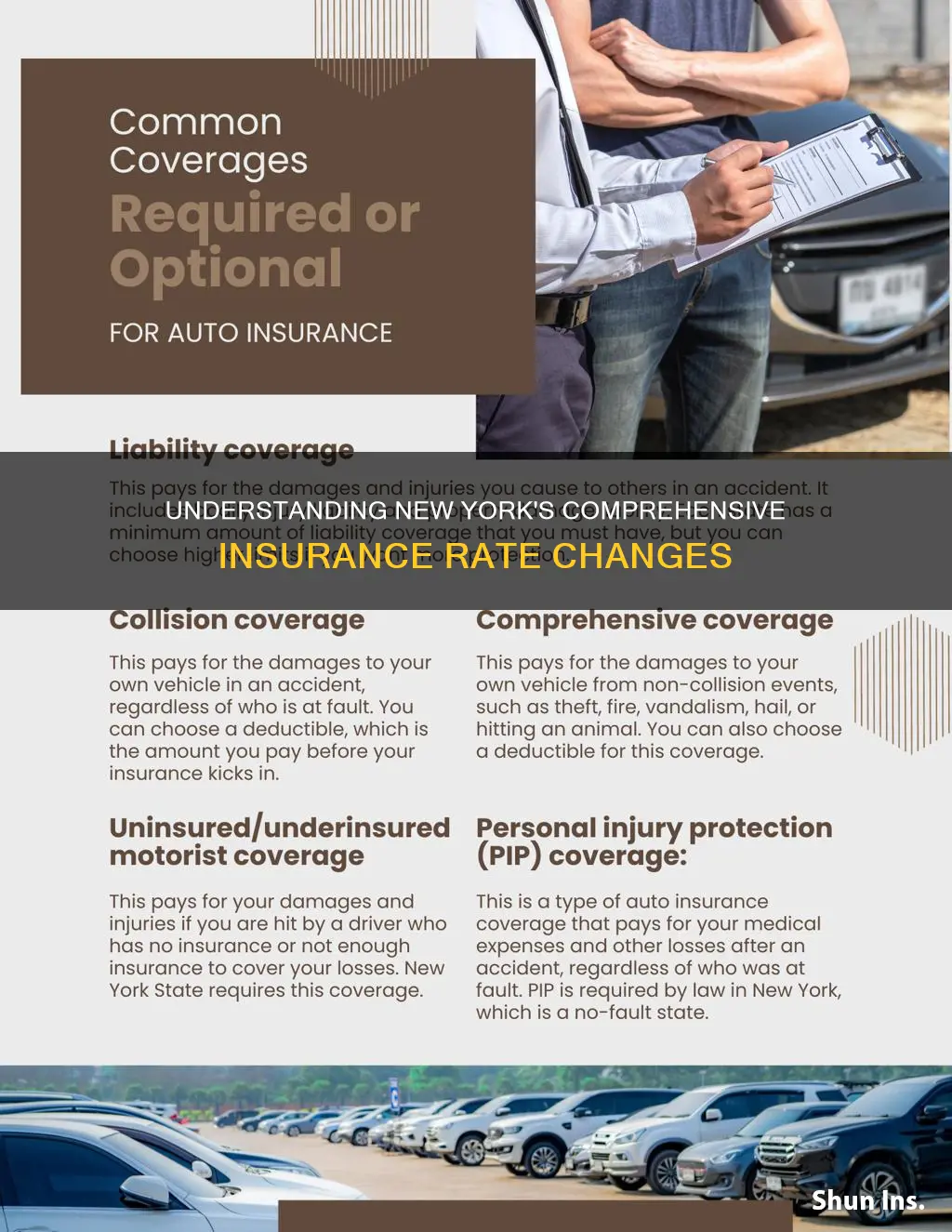

For other vehicles, the minimum amount of liability coverage is $25,000 per person, $50,000 per accident in bodily injury coverage, and $10,000 in property damage. This basic liability insurance is mandatory for all vehicles. Additionally, New York requires uninsured motorist coverage and personal injury protection.

Comprehensive insurance is not mandatory in New York. It covers damage to your own vehicle, including property damage from things like extreme weather conditions or vandalism. Comprehensive insurance will also pay out if your car is stolen.

If you have a car loan or lease, your lender will likely require you to carry full coverage, which includes comprehensive and collision insurance.

Concealed Carry Insurance: Protection for Gun Owners

You may want to see also

Explore related products

![]()

Location

New York State has some of the highest car insurance rates in the country. The average cost of car insurance in the state is $4,021 per year for full coverage and $1,719 per year for minimum coverage. This is significantly higher than the national average of $1,296 for full coverage and $595 for minimum coverage.

There are several reasons why car insurance is so expensive in New York. One factor is the state's no-fault insurance laws, which require drivers to have personal injury protection (PIP) coverage. This type of coverage pays for medical bills for anyone injured in an accident, regardless of who caused it. Only 12 states have this type of insurance, and it can drive up the cost of premiums for everyone, even safe drivers.

Another reason for high insurance rates in New York is the state's high healthcare costs. As healthcare costs increase, insurance companies have to pay more in claims for injury treatments, which leads to higher premiums. New York also has a high number of traffic fatalities and severe weather risks, which can also contribute to higher insurance rates.

The cost of car insurance in New York can also vary depending on where you live in the state. Drivers in high-density urban areas, such as New York City, may pay more for coverage than those in more rural areas due to the increased risk of accidents and vehicle theft. In fact, insurance companies treat the entire state as one group when it comes to accident risks, so drivers who live far from New York City may end up paying more due to the accidents that happen in the city.

Finally, individual factors such as age, credit score, driving record, and vehicle type can also affect the cost of car insurance in New York. Older drivers with good credit and a clean driving history tend to enjoy cheaper rates, while teens and drivers with DUIs or at-fault accidents on their records will pay more.

Conceal Carry: School Insurance Surge

You may want to see also

Frequently asked questions

Yes, insurance companies review your record going back three to five years to determine your rates. If you have a history of accidents, your insurance premiums will likely increase.

Yes, multiple accidents within a short period will elevate your insurance rates. New York is a no-fault state, so your insurance company will pay for your medical bills and lost wages, regardless of who caused the accident.

Insurance companies do not differentiate between city and country drivers. New York insurance companies treat the whole state as one group, so drivers outside of New York City may pay more due to the increased risks in urban areas.

Insurance rates in NY are influenced by age, credit score, vehicle type, driving violations, healthcare costs, and weather risks.

Yes, comprehensive insurance covers car theft. However, insurance rates are influenced by theft rates, so areas with higher theft or vandalism rates will have higher premiums.