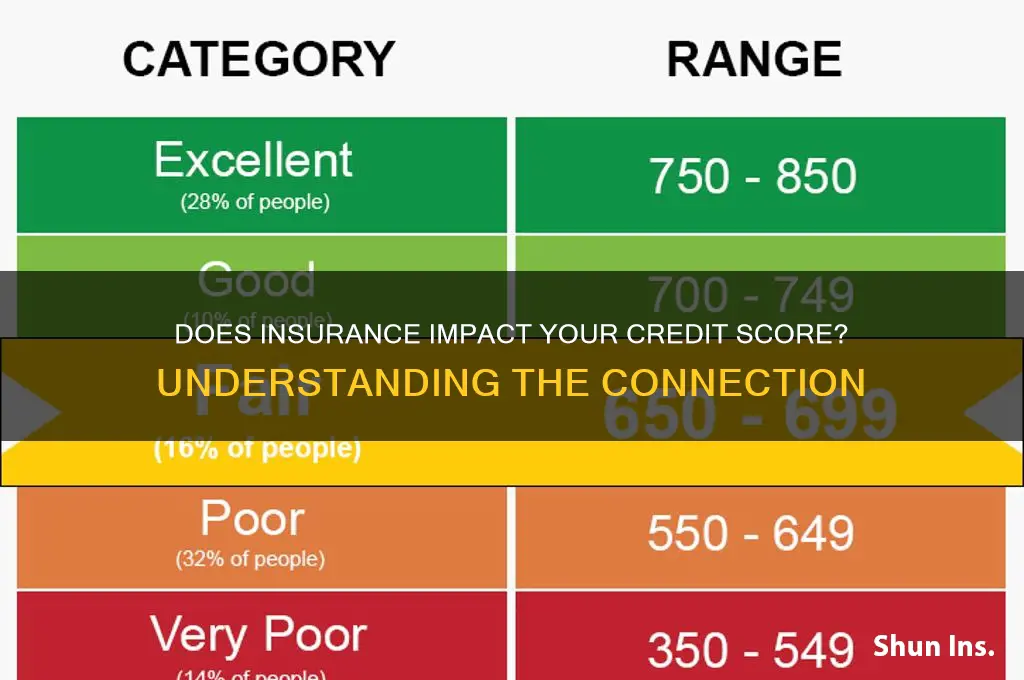

Insurance itself does not directly impact your credit score, as insurance payments are not typically reported to credit bureaus. However, certain aspects of insurance can indirectly influence your credit. For example, missed insurance payments may lead to debt collection or legal judgments, which can negatively affect your credit report. Additionally, some insurers may check your credit score when determining premiums, as individuals with lower credit scores are often considered higher risk. While insurance doesn’t help build credit like loans or credit cards, managing it responsibly can prevent financial setbacks that might harm your credit in the long run.

| Characteristics | Values |

|---|---|

| Direct Impact on Credit Score | No, insurance payments (like auto or health insurance) do not directly impact your credit score as they are not reported to credit bureaus. |

| Indirect Impact via Payment History | Yes, missed insurance payments can lead to debt collection, which, if reported, negatively affects your credit score. |

| Credit-Based Insurance Scores | Insurance companies use credit-based insurance scores to determine premiums, but this does not directly affect your credit score. |

| Late Payments to Insurers | Late payments to insurers may not directly impact credit, but if sent to collections, they can harm your credit score. |

| Insurance Inquiries | Insurance quotes typically result in soft inquiries, which do not affect your credit score. |

| Bundling Insurance Policies | No direct credit impact, but bundling may save money, indirectly helping financial stability. |

| Insurance Claims | Filing claims generally does not affect your credit score, but frequent claims may impact insurance premiums. |

| Credit Monitoring by Insurers | Insurers may monitor credit for policy changes, but this does not affect your credit score. |

| Paying Premiums with Credit Cards | Paying premiums with credit cards can improve credit if managed well (on-time payments, low utilization), but risks debt if mismanaged. |

| Insurance Cancellations | Cancellations due to non-payment may lead to collections, negatively impacting credit if reported. |

| Latest Data (as of 2023) | No new evidence suggests insurance directly improves credit; indirect impacts remain consistent with historical data. |

Explore related products

What You'll Learn

- Insurance Payments Impact: Timely premium payments may indirectly improve credit by avoiding debt or collections

- Claims and Credit: Filing claims doesn’t directly affect credit, but unpaid debts from claims can

- Insurance Credit Checks: Insurers may check credit, but it’s a soft inquiry, not harming your score

- Lapsed Policies: Cancelled policies for non-payment can lead to debt, negatively impacting credit

- Insurance and Loans: Better credit may lower insurance premiums, creating a positive financial cycle

![]()

Insurance Payments Impact: Timely premium payments may indirectly improve credit by avoiding debt or collections

Insurance payments, particularly timely premium payments, can have an indirect yet significant impact on your credit health. While insurance payments themselves are not typically reported to the major credit bureaus (Equifax, Experian, and TransUnion), the consequences of missing these payments can directly affect your credit score. Paying your insurance premiums on time ensures that you avoid late fees, policy cancellations, and potential debt accumulation. This proactive approach helps maintain financial stability, which is crucial for overall credit management.

One of the primary ways timely insurance payments indirectly improve your credit is by preventing debt or collections. When you fail to pay your insurance premiums, the insurer may cancel your policy, and the unpaid amount could be sent to a collections agency. Collections accounts are highly detrimental to your credit score and can remain on your credit report for up to seven years. By consistently paying your premiums on time, you eliminate the risk of such negative entries on your credit report, thereby protecting your credit score.

Additionally, avoiding debt from missed insurance payments helps maintain a healthy debt-to-income ratio, which is an important factor in your overall financial profile. While this ratio is not directly included in your credit score, lenders often review it when assessing your creditworthiness. Consistently paying your insurance premiums ensures that you are not accumulating unnecessary debt, which can improve your chances of securing loans or credit in the future. This financial discipline reflects positively on your ability to manage obligations responsibly.

Another indirect benefit of timely insurance payments is the avoidance of policy lapses, which can lead to gaps in coverage. Gaps in insurance coverage may force you to pay higher premiums when you reinstate or purchase a new policy, increasing your financial burden. Higher premiums can strain your budget, potentially leading to missed payments on other credit obligations, such as credit cards or loans. By maintaining continuous insurance coverage through timely payments, you reduce the risk of financial stress that could negatively impact your credit.

Lastly, paying your insurance premiums on time contributes to a broader pattern of financial responsibility. Lenders and creditors value consistency in meeting financial obligations, even if insurance payments are not directly reported to credit bureaus. Demonstrating reliability in paying premiums can create a positive impression of your financial habits, which may indirectly influence your creditworthiness. While insurance payments do not directly boost your credit score, their role in preventing debt and collections is a critical aspect of maintaining and improving your credit health.

Who Can Sell Their Life Insurance?

You may want to see also

Explore related products

![]()

Claims and Credit: Filing claims doesn’t directly affect credit, but unpaid debts from claims can

When considering the relationship between insurance and credit, it’s important to understand that filing an insurance claim itself does not directly impact your credit score. Credit bureaus like Equifax, Experian, and TransUnion do not track insurance claims as part of your credit history. Whether you file a claim for a car accident, home damage, or medical expenses, the act of filing alone will not appear on your credit report. This means you can file a claim without worrying about immediate negative consequences to your credit score. However, this is only part of the story, as indirect factors related to claims can still influence your credit.

While filing a claim is neutral for your credit, unpaid debts resulting from insurance claims can have a significant impact. For example, if you file a medical claim and your insurance doesn’t cover the entire cost, the remaining balance becomes your responsibility. If you fail to pay this debt, it may be sent to collections, and collections accounts are reported to credit bureaus. Once reported, these unpaid debts can lower your credit score and remain on your credit report for up to seven years. Similarly, if you dispute an insurance claim and the provider denies coverage, leaving you with unpaid bills, these debts can also harm your credit if not addressed promptly.

Another scenario to consider is when an insurance claim leads to a gap in coverage or an increase in premiums. If unpaid premiums cause your policy to lapse, the insurer may report the debt to collections, which can then affect your credit. Additionally, if you finance insurance premiums (e.g., paying in installments) and miss payments, those delinquencies can be reported to credit bureaus. It’s crucial to manage insurance-related debts proactively to avoid these negative outcomes. Regularly reviewing your insurance policies and ensuring timely payments can help prevent credit damage.

To protect your credit while navigating insurance claims, it’s essential to stay informed and take preventive measures. First, communicate with your insurance provider to understand what is and isn’t covered under your policy. If you receive a bill after a claim, address it immediately to avoid it becoming a delinquent debt. If you’re unable to pay the full amount, consider negotiating a payment plan with the healthcare provider or creditor. Monitoring your credit report regularly can also help you catch any errors or unexpected collections accounts early. By staying proactive, you can minimize the risk of insurance-related debts harming your credit.

In summary, filing insurance claims does not directly affect your credit score, but unpaid debts arising from claims can have serious consequences. Whether it’s medical bills, property damage expenses, or lapsed insurance premiums, unpaid obligations may be reported to collections and damage your credit. Understanding your insurance coverage, managing debts responsibly, and monitoring your credit report are key steps to ensuring that insurance claims do not indirectly harm your financial health. By taking these precautions, you can maintain a strong credit profile while utilizing insurance as intended—to protect against unforeseen events.

Life Insurance: Building Generational Wealth Protection

You may want to see also

Explore related products

$18.89 $24.95

![]()

Insurance Credit Checks: Insurers may check credit, but it’s a soft inquiry, not harming your score

When considering the relationship between insurance and credit, it’s important to understand how insurers use credit information. Insurance credit checks are a common practice in the industry, but they differ significantly from the hard inquiries that occur when applying for loans or credit cards. Insurers often review your credit history to assess risk and determine premiums, but this is done through a soft inquiry. Unlike hard inquiries, soft inquiries do not impact your credit score. This means you can shop for insurance without worrying about damaging your credit. The purpose of these checks is to evaluate financial responsibility, as studies show a correlation between credit behavior and insurance claims.

The reason insurers perform credit checks is rooted in their risk assessment models. A soft credit inquiry allows them to access a modified version of your credit report, which provides insights into your financial habits. Factors like payment history, debt levels, and credit utilization are considered to predict how likely you are to file a claim. For example, individuals with higher credit scores may be seen as less risky and could qualify for lower premiums. However, it’s crucial to note that this process does not harm your credit score, as soft inquiries are not recorded in the same way as hard inquiries. This ensures that exploring insurance options remains a risk-free activity for your credit health.

It’s a common misconception that insurance applications negatively affect your credit. In reality, insurance credit checks are designed to be non-intrusive. While insurers use credit information to tailor policies, they do not report these inquiries to credit bureaus in a way that impacts your score. This distinction is vital for consumers who may hesitate to seek insurance due to credit concerns. Understanding that these checks are soft inquiries can empower individuals to compare policies and find the best coverage without fear of financial repercussions. It’s also worth noting that not all insurers use credit-based scoring, but when they do, it’s always a soft inquiry.

If you’re worried about how insurance might influence your credit, remember that soft inquiries are a standard part of the process and pose no threat to your score. Instead, focus on maintaining good financial habits, such as paying bills on time and managing debt responsibly, as these factors can indirectly benefit your insurance premiums. While insurance itself does not directly improve your credit, the soft inquiries associated with it are harmless. By demystifying insurance credit checks, consumers can approach the insurance market with confidence, knowing their credit score remains unaffected.

In summary, insurance credit checks involve soft inquiries that do not harm your credit score. Insurers use these checks to assess risk and set premiums, but the process is designed to be consumer-friendly. Understanding this distinction can alleviate concerns and encourage individuals to explore insurance options freely. While insurance doesn’t directly help your credit, the soft inquiry system ensures that seeking coverage won’t hinder your financial standing. This knowledge allows you to make informed decisions about insurance without worrying about unintended credit consequences.

Gerber Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Lapsed Policies: Cancelled policies for non-payment can lead to debt, negatively impacting credit

Insurance policies are designed to provide financial protection, but when they lapse due to non-payment, the consequences can extend beyond the loss of coverage. A lapsed policy occurs when premiums are not paid, and the insurer cancels the policy. This situation can lead to debt and have a detrimental effect on your credit score, which is a critical aspect of your financial health. Understanding this relationship is essential for anyone looking to maintain a positive credit profile.

When an insurance policy lapses, the insurance company may initially attempt to contact the policyholder to rectify the payment issue. If the payment remains outstanding, the policy is typically canceled, and the insurer might then send the unpaid balance to a collection agency. This is where the impact on your credit begins. Collection accounts are considered negative marks on a credit report and can significantly lower your credit score. The presence of such accounts indicates financial mismanagement and can remain on your credit report for several years, affecting your ability to secure loans, credit cards, or even favorable interest rates.

The debt from a lapsed policy doesn't just disappear. It becomes a financial obligation that must be addressed. If the debt is sold to a collection agency, you may start receiving calls and letters demanding payment. Ignoring these notices will only worsen the situation, as the debt may continue to grow with added fees and interest. It's crucial to take proactive steps to resolve the issue, such as negotiating a payment plan with the collection agency or, if possible, paying off the debt in full.

Furthermore, the impact of a lapsed policy on your credit can have long-lasting effects. Credit scores are used by lenders, landlords, and even potential employers to assess your financial responsibility. A low credit score resulting from unpaid insurance debts may lead to higher interest rates on loans, difficulty in renting an apartment, or even missed job opportunities. It's a ripple effect that highlights the importance of maintaining active insurance policies and managing payments effectively.

To avoid these negative consequences, policyholders should prioritize timely premium payments. Setting up automatic payments or reminders can be an effective way to ensure payments are not missed. If financial difficulties arise, it's advisable to contact the insurance company promptly to discuss potential options, such as adjusting coverage or arranging a payment plan, rather than letting the policy lapse. Being proactive in managing insurance payments is a key aspect of protecting your credit and overall financial well-being.

Insurance Simplified: A-Win Insurance Spruce Grove

You may want to see also

Explore related products

![]()

Insurance and Loans: Better credit may lower insurance premiums, creating a positive financial cycle

While insurance itself doesn't directly impact your credit score, there's a fascinating connection between your creditworthiness and insurance premiums. This relationship can create a positive financial cycle, benefiting those with good credit.

Here's how it works: many insurance companies, particularly auto and home insurers, use credit-based insurance scores to assess risk. These scores, derived from your credit history, predict the likelihood of you filing a claim. Statistically, individuals with higher credit scores tend to file fewer claims. As a result, insurers often offer lower premiums to those with good credit, viewing them as less risky customers.

This means that maintaining a healthy credit score can directly translate to savings on your insurance costs. For example, a driver with excellent credit might pay significantly less for car insurance compared to someone with a poor credit history, even if their driving records are identical. This premium reduction essentially rewards responsible financial behavior, encouraging individuals to prioritize creditworthiness.

Lower insurance premiums free up more money in your budget. This extra cash can be strategically allocated to further improve your financial health. You could use it to pay down existing debt faster, reducing your credit utilization ratio, a key factor in your credit score.

Alternatively, you could invest the savings, potentially growing your wealth over time. This positive cycle continues as a higher credit score leads to lower insurance costs, which in turn allows for more financial flexibility and opportunities to strengthen your credit profile.

It's important to note that not all states allow insurance companies to use credit-based scoring, and the weight given to credit varies by insurer and policy type. However, understanding this connection highlights the importance of good credit management. By prioritizing timely payments, keeping credit card balances low, and regularly reviewing your credit report for inaccuracies, you can not only improve your chances of loan approval but also potentially enjoy lower insurance premiums, creating a virtuous cycle of financial well-being.

Whole Life Insurance: Who Is a Good Candidate?

You may want to see also

Frequently asked questions

No, having insurance does not directly improve your credit score. Credit scores are primarily based on credit history, payment history, credit utilization, and other financial factors, not insurance coverage.

Generally, paying insurance premiums on time does not directly impact your credit score, as insurance payments are not typically reported to credit bureaus. However, missed payments that lead to debt collection may negatively affect your credit.

Insurance accounts (like auto or health insurance) do not typically appear on your credit report unless there are unpaid debts or claims that go to collections. Only then might it negatively impact your credit.