Many people wonder whether insurance payments can help them build credit, especially those who want to improve their credit scores to save money on insurance premiums and financing. However, insurance companies do not report to credit bureaus because they do not lend money to people. Therefore, paying insurance premiums on time does not help build credit. That said, there are indirect ways that insurance payments can impact your credit score. For example, if you pay your insurance premiums with a credit card, you can improve your credit score as long as you pay down your credit card balance every month.

| Characteristics | Values |

|---|---|

| Do insurance payments build credit? | No, insurance payments do not build credit. |

| Do insurance companies report to credit bureaus? | No, insurance companies do not report to credit bureaus. |

| Does missing an insurance payment impact credit score? | Missing an insurance payment does not directly impact one's credit score. However, if the debt is sent to a collection agency, it can negatively impact the credit score. |

| Does paying insurance with a credit card impact credit score? | Paying insurance with a credit card can indirectly impact one's credit score. Responsible use of a credit card can positively impact the credit score, while missed or late payments can negatively impact the score. |

| Does buying insurance impact credit score? | No, buying insurance does not impact the credit score. |

| Does cancelling insurance impact credit score? | No, cancelling insurance does not impact the credit score. However, a lapse in coverage can lead to higher insurance premiums in the future. |

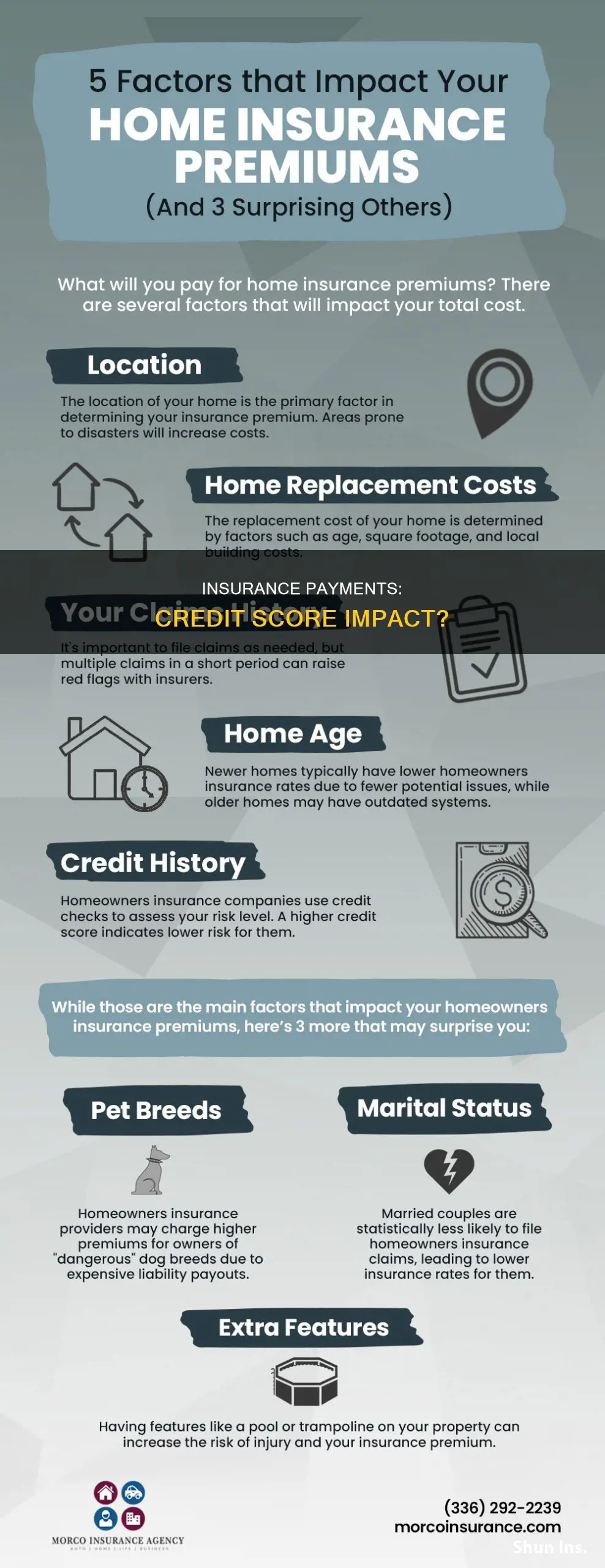

| Does insurance history impact insurance premiums? | Yes, insurance companies consider an individual's credit history and score when determining insurance premiums. |

Explore related products

What You'll Learn

![]()

Paying insurance with a credit card

Now, when it comes to paying insurance with a credit card, there are a few things to keep in mind. Firstly, not all types of insurance can be paid with a credit card. While auto insurance policies often accept credit card payments, life insurance companies usually refuse this payment method. Additionally, if you have a mortgage and an escrow account, you typically cannot use a credit card to pay your insurance premiums because escrow accounts are designed to pay for expenses from a bank account over time, excluding credit cards.

Another important consideration is whether there are any fees imposed by the credit card company or the insurance company for paying with a credit card. These fees could negate any benefits or perks you might gain from using a credit card. On the other hand, some credit cards offer rewards or cash-back incentives, which could make using a credit card advantageous.

If you decide to use a credit card to pay your insurance, it's crucial to ensure that you pay your credit card bill in full and on time to avoid accruing debt and interest charges. Late credit card payments can lead to high-interest rates and negatively impact your credit score. Setting up autopay can help ensure timely payments, but you must have sufficient funds in your bank account to avoid overdraft fees and potential lapses in insurance coverage.

In summary, paying insurance with a credit card can offer benefits, such as rewards and flexibility, but it also carries the risk of debt and interest charges if not managed properly. It's important to consider your financial situation and spending habits before deciding to use a credit card for insurance payments.

Check Peachstate Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Insurance companies don't report to credit bureaus

Insurance companies do not report to credit bureaus. Credit agencies are therefore unaware of whether you make your insurance payments on time or not, and your credit score will not be affected either way.

Insurance companies do not lend you money, and the contractual obligations to pay insurance premiums are not considered debts. As such, insurance companies do not report payments or any other information about your coverage or claims to the credit bureaus.

However, while insurance payments do not directly impact your credit score, unpaid insurance bills can harm your credit report if the insurer turns them over to collection agencies. If your account goes into collections, this will show up as a negative entry on your credit report and lower your credit score.

Additionally, while insurance payments themselves do not affect your credit score, insurance companies do consider your credit score when determining your premiums. Insurers in many states, particularly auto insurers, use a credit-based insurance score to help determine your premiums. This is because an insured person's credit health can help predict how likely they are to file a claim.

Federal Insurance Funding: Is It Better?

You may want to see also

Explore related products

![]()

Missed payments and cancellations

Missing an insurance payment can have several consequences, including policy cancellation, coverage lapse, higher premiums, fines, and difficulty obtaining future coverage. Most insurance companies offer grace periods, typically ranging from 7 to 30 days, during which you can pay your bill without penalties. However, if you don't make the payment within the grace period, your policy may be cancelled.

Before cancelling your policy, your insurer will usually send you a missed payment notice, either by registered letter or email, informing you of their intended action. It is advisable to proactively contact your broker or insurer if you anticipate financial difficulties making payments. Once your policy is cancelled, you may still need to pay any outstanding amounts to your previous insurance company, and this debt can be sent to collections, negatively impacting your credit score.

If you miss a payment but are generally a timely payer, your insurance company might be lenient, especially if you're only a few days overdue. Contacting your insurance provider as soon as possible and explaining the situation can help prevent further issues. Setting up autopay can also help avoid future missed payments. If you're struggling to afford the premiums, it's worth checking with your current carrier about any additional discounts you may qualify for or shopping around for more affordable coverage.

While missing a payment or having your policy cancelled due to non-payment won't directly affect your credit score, it can still have financial implications. If your debt is sent to collections, your credit score will be negatively impacted. Additionally, insurers may charge higher premiums for future coverage, as they assess rates based on your credit history.

Insurers Check Convictions: How to Get Covered?

You may want to see also

Explore related products

![]()

Credit-based insurance scores

FICO considers five key areas to determine an individual's ability to manage risk, each with a different weight in the overall score:

- Payment history (40%): How well an individual has made payments on their outstanding debt.

- Outstanding debt (30%): The amount of debt an individual currently holds.

- Credit history length (15%): How long an individual has had access to credit.

- Pursuit of new credit (10%): Whether an individual has applied for new lines of credit.

- Credit mix (5%): The types of credit an individual has, such as credit cards, mortgages, or auto loans.

It is important to note that credit-based insurance scores are not the same as traditional credit scores. While insurance companies may consider credit scores when determining premiums, they do not report on-time payments to credit bureaus. Additionally, while missing insurance payments can result in higher premiums or policy cancellation, it will not directly impact an individual's credit score unless the account is sent to collections.

Robinhood Checking: Are Your Funds Insured?

You may want to see also

Explore related products

![]()

Improving credit score through other payments

Car insurance payments do not directly impact your credit score. This is because insurance is not a line of credit; it is a service that you pay for. Insurance companies do not report to credit bureaus, so your credit score will not be affected by on-time payments or late payments. However, if you miss multiple payments, your account may be sent to collections, which will negatively affect your credit score.

To improve your credit score through other payments, you can focus on the following:

- Credit card payments: Make timely credit card payments to improve your credit score. Credit card payments offer flexibility in terms of when and how much you pay. However, if you use a credit card to pay your insurance premiums, ensure that you pay your credit card bill on time, as late payments can incur interest of up to 20%.

- Credit utilization: Keep your credit utilization low to improve your credit score. Credit utilization refers to the percentage of available credit that you are using. Aim to keep your credit utilization below 30%, although there is no strict rule. Pay down credit card balances before your billing cycle ends to keep your credit utilization low.

- On-time payments: Make on-time payments to improve your credit score. Payment history makes up a significant portion of your credit score, so it is important to pay your bills on time. A late or missed payment can remain on your credit report for up to seven years.

- Length of credit history: Maintaining older credit accounts can positively impact your credit score. Older accounts demonstrate a longer history of handling credit, which lenders view favourably.

- Authorized user: Become an authorized user on a friend or family member's account to improve your credit score. This is especially useful if you have a short credit history, but remember that you will be jointly responsible for paying off the card.

- Dispute inaccuracies: Inaccurate information on your credit report can negatively impact your credit score. Review your credit reports for any discrepancies and dispute them with the credit reporting agencies. This can help remove fraudulent accounts or incorrect information that may be lowering your score.

Elephant Insurance Payment Plans: What You Need to Know

You may want to see also

Frequently asked questions

No, paying insurance does not build your credit score. Insurance companies don't report to credit bureaus because they don't lend money to people. However, if you pay your insurance with a credit card, your credit score could be indirectly affected.

If you pay your insurance with a credit card, your credit score could be indirectly affected. The responsible use of your credit card could have a positive effect on your credit score. Conversely, if you miss a payment, your credit score could be negatively affected.

You can build your credit score by paying off your credit card and making on-time payments to your student loan lender, mortgage lender, and other lenders.