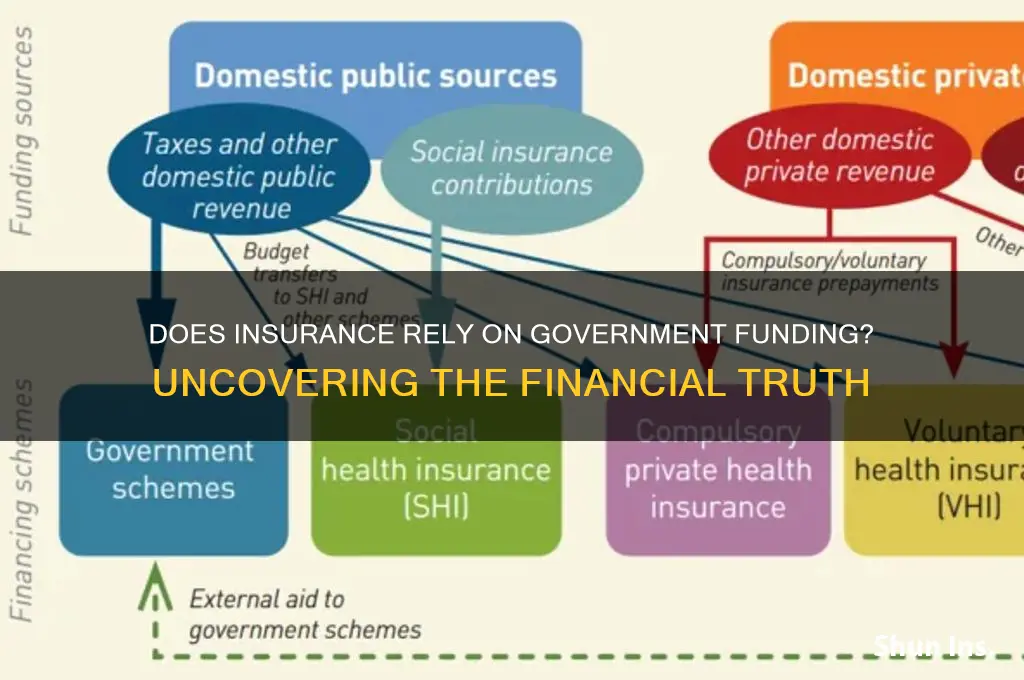

The question of whether insurance companies receive government funds is a complex and multifaceted issue that varies significantly depending on the type of insurance, the country, and the specific policies in place. In many cases, insurance companies operate as private entities, generating revenue through premiums paid by policyholders. However, certain sectors of the insurance industry, such as health insurance or flood insurance, may receive government subsidies, grants, or financial support to ensure coverage for high-risk or underserved populations. Additionally, governments often regulate insurance markets, providing backstops or bailout funds during financial crises to stabilize the industry and protect consumers. Understanding the interplay between insurance and government funding requires examining specific programs, legislative frameworks, and the broader economic context in which these entities operate.

Explore related products

What You'll Learn

![]()

Federal Grants for Insurance Programs

The federal government provides various grants to support insurance programs, ensuring that vulnerable populations have access to essential coverage. These Federal Grants for Insurance Programs are designed to address gaps in private insurance markets, promote affordability, and enhance healthcare accessibility. One prominent example is the Medicaid program, jointly funded by the federal government and states, which offers health insurance to low-income individuals, families, and people with disabilities. The federal government matches state spending on Medicaid, with the matching rate (FMAP) varying based on each state's per capita income, ensuring that states with lower resources receive more federal support.

Another critical federal grant program is the Children's Health Insurance Program (CHIP), which provides low-cost health coverage to children in families who earn too much to qualify for Medicaid but cannot afford private insurance. Like Medicaid, CHIP is funded through a partnership between the federal government and states, with the federal government covering a significant portion of the costs. These programs demonstrate how federal grants directly fund insurance initiatives to protect underserved populations.

In addition to healthcare, the federal government also supports flood insurance through the National Flood Insurance Program (NFIP). Administered by the Federal Emergency Management Agency (FEMA), the NFIP provides grants to help communities reduce flood risks and offers affordable insurance policies to homeowners in flood-prone areas. While policyholders pay premiums, federal grants subsidize the program's operations and ensure its sustainability, particularly in high-risk zones where private insurers are reluctant to provide coverage.

Federal grants also play a role in agricultural insurance through the Federal Crop Insurance Corporation (FCIC), which is part of the U.S. Department of Agriculture (USDA). The FCIC provides grants to private insurance companies to offer crop insurance policies to farmers, protecting them from losses due to natural disasters. The federal government subsidizes premiums, administrative costs, and indemnities, ensuring that farmers can access affordable coverage and maintain financial stability during challenging times.

Lastly, the Affordable Care Act (ACA) introduced federal grants to support insurance programs like Cost-Sharing Reduction (CSR) payments and Advanced Premium Tax Credits (APTCs). These grants help reduce out-of-pocket costs and premiums for eligible individuals purchasing health insurance through ACA marketplaces. While CSR payments are made directly to insurers, APTCs are tax credits that lower monthly premiums for policyholders. These programs illustrate how federal grants directly fund insurance mechanisms to make coverage more affordable for millions of Americans.

In summary, Federal Grants for Insurance Programs are a cornerstone of government efforts to ensure that essential insurance coverage is accessible and affordable. From healthcare initiatives like Medicaid and CHIP to programs supporting flood and agricultural insurance, these grants address critical needs in areas where private markets fall short. By providing direct funding, subsidies, and cost-sharing mechanisms, the federal government plays a vital role in sustaining insurance programs that protect individuals, families, and communities across the nation.

Does Rob Gronkowski Have USAA Insurance? Exploring the Truth

You may want to see also

Explore related products

![]()

State Funding for Health Insurance

The question of whether insurance receives government funds is particularly relevant in the context of health insurance, where state funding plays a crucial role in ensuring access to healthcare services for millions of individuals. State funding for health insurance primarily aims to support low-income families, children, the elderly, and individuals with disabilities who might otherwise be unable to afford coverage. One of the most prominent examples of state-funded health insurance in the United States is Medicaid, a joint federal and state program that provides health coverage to eligible low-income individuals and families. Each state administers its own Medicaid program within broad federal guidelines, and the federal government matches state spending on Medicaid, with the matching rate varying by state based on per capita income.

In addition to Medicaid, the Children’s Health Insurance Program (CHIP) is another key initiative that relies on state funding, often in partnership with federal resources. CHIP provides low-cost health coverage to children in families who earn too much to qualify for Medicaid but cannot afford private insurance. States have flexibility in designing their CHIP programs, and they receive federal matching funds to support these efforts. Both Medicaid and CHIP are essential components of the safety net that ensures vulnerable populations have access to necessary healthcare services, demonstrating the significant role of state funding in health insurance.

Beyond Medicaid and CHIP, some states have implemented their own health insurance programs or subsidies to expand coverage further. For instance, states like California and New York have established state-based marketplaces and offer additional financial assistance to reduce premiums and out-of-pocket costs for residents purchasing private insurance plans. These state-funded initiatives often target individuals who fall into the "coverage gap"—those who earn too much to qualify for Medicaid but still struggle to afford insurance. By providing these subsidies, states aim to increase affordability and reduce the number of uninsured individuals.

While state funding is vital for expanding health insurance coverage, it is not without challenges. Budget constraints, political priorities, and varying levels of federal support can impact the extent to which states can fund these programs. Additionally, the complexity of administering multiple programs and ensuring coordination between state and federal initiatives requires careful planning and resource allocation. Despite these challenges, state funding remains a cornerstone of efforts to make health insurance more accessible and affordable for those who need it most. By leveraging federal partnerships and innovative programs, states continue to play a critical role in shaping the landscape of health insurance in the United States.

Trusts and Life Insurance: Can They Co-exist?

You may want to see also

Explore related products

![]()

Disaster Relief for Insurance Claims

In the context of disaster relief, insurance companies play a critical role in helping policyholders recover from catastrophic events such as hurricanes, floods, wildfires, and earthquakes. While insurance companies primarily operate using premiums paid by policyholders, there are instances where government funds come into play to support disaster relief efforts. This interplay between private insurance and government assistance is essential for ensuring that individuals and communities can rebuild after disasters. Government funds often supplement insurance payouts, especially in cases where the scale of the disaster exceeds the capacity of private insurers.

One key area where government funds intersect with insurance claims is through the National Flood Insurance Program (NFIP). Administered by the Federal Emergency Management Agency (FEMA), the NFIP provides flood insurance to property owners in participating communities. Since many private insurers do not cover flood damage, the NFIP acts as a government-backed insurance program. Policyholders file claims with the NFIP, which uses a combination of premiums and government funds to pay out claims. In the event of a major flood, Congress may appropriate additional funds to ensure the program can meet its obligations, demonstrating direct government involvement in disaster relief for insurance claims.

Another way government funds support disaster relief for insurance claims is through disaster assistance programs. When a disaster is declared by the President, FEMA may provide financial assistance to individuals and households through programs like the Individuals and Households Program (IHP). This assistance can include grants for temporary housing, home repairs, and other uninsured or underinsured losses. While this aid is not directly funneled through insurance companies, it complements insurance payouts by covering gaps in coverage. For example, if a homeowner’s insurance policy does not fully cover the cost of rebuilding after a wildfire, FEMA grants can provide additional relief.

In some cases, state-based insurance funds also play a role in disaster relief. States like Florida and California have established programs such as the Florida Hurricane Catastrophe Fund and the California Earthquake Authority, which provide reinsurance to private insurers. These funds help insurers manage the financial risk of large-scale disasters by covering a portion of claims that exceed certain thresholds. While these programs are often funded through assessments on insurance policies, they may also receive government support in the form of bonds or direct appropriations during severe events.

Finally, tax incentives and deductions represent an indirect way government funds support disaster relief for insurance claims. Policyholders who suffer uninsured or underinsured losses in federally declared disaster areas may be eligible for tax deductions on their casualties and thefts. This reduces their tax liability, effectively providing financial relief that complements insurance payouts. Additionally, insurers themselves may benefit from tax incentives for participating in government-backed programs like the NFIP, further integrating government funds into the disaster relief ecosystem.

In summary, while insurance companies primarily rely on policyholder premiums, government funds are integral to disaster relief for insurance claims. Through programs like the NFIP, FEMA disaster assistance, state-based funds, and tax incentives, government support ensures that individuals and communities receive adequate financial assistance after catastrophic events. Understanding this interplay is crucial for policyholders navigating the claims process and for policymakers designing effective disaster relief strategies.

Protect Your TV: A Comprehensive Guide to TV Insurance Options

You may want to see also

Explore related products

![]()

Subsidies for Affordable Care Act

The Affordable Care Act (ACA), often referred to as Obamacare, includes a system of government subsidies designed to make health insurance more affordable for individuals and families with moderate to low incomes. These subsidies are a key component of the ACA's strategy to expand healthcare coverage and reduce the financial burden of insurance premiums. The primary subsidies available under the ACA are the Advanced Premium Tax Credits (APTC) and Cost-Sharing Reductions (CSRs), both of which are funded by the federal government.

Advanced Premium Tax Credits (APTC) are the most widely utilized subsidies under the ACA. They are income-based and directly reduce the monthly premiums individuals pay for their health insurance plans purchased through the Health Insurance Marketplace. Eligibility for APTC is determined by household income, which must fall between 100% and 400% of the Federal Poverty Level (FPL). The amount of the subsidy is calculated to ensure that the beneficiary’s premium contribution does not exceed a certain percentage of their income, typically ranging from 2% to 9.83%, depending on their income level. This subsidy is paid directly to the insurance provider, and the beneficiary pays the reduced premium amount.

Cost-Sharing Reductions (CSRs) are another form of subsidy aimed at lowering out-of-pocket costs for eligible individuals and families. CSRs are available to those with incomes between 100% and 250% of the FPL who enroll in a Silver-level health plan through the Marketplace. These subsidies reduce the amount policyholders pay for deductibles, copayments, and coinsurance. Unlike APTC, CSRs are not a separate payment but are integrated into the plan design, providing enhanced benefits at no additional cost to the enrollee.

The funding for these subsidies comes directly from the federal government, making them a clear example of how insurance receives government funds under the ACA. The subsidies are designed to ensure that health insurance remains accessible and affordable for millions of Americans who might otherwise struggle to afford coverage. By reducing premiums and out-of-pocket costs, the ACA subsidies help to mitigate the financial barriers to healthcare access.

It’s important to note that the ACA subsidies are subject to annual adjustments based on changes in income, family size, and the cost of living. Enrollees are required to reconcile their subsidies when filing their federal taxes to ensure they received the correct amount. If an individual’s income increases during the year, they may need to repay a portion of the subsidy, while those with lower-than-expected income may receive a refund. This reconciliation process ensures the integrity of the subsidy program and aligns it with the ACA’s goal of providing targeted financial assistance.

In summary, the subsidies for the Affordable Care Act—Advanced Premium Tax Credits and Cost-Sharing Reductions—are direct examples of government funding for insurance. These programs play a critical role in making health insurance affordable for millions of Americans, demonstrating the significant interplay between government funds and the insurance industry under the ACA. Understanding these subsidies is essential for individuals seeking to maximize their healthcare coverage while minimizing costs.

Becoming a Life Insurance Agent: Getting Accredited

You may want to see also

Explore related products

![]()

Government Bailouts for Insurers in Crisis

The question of whether insurance companies receive government funds is a complex one, and the answer varies depending on the context and the specific situation. In times of financial crisis, insurers, like other large financial institutions, may find themselves in need of government support to prevent systemic collapse. This is where the concept of government bailouts for insurers in crisis comes into play. Government bailouts are essentially financial assistance packages provided by the government to struggling companies, including insurers, to help them avoid bankruptcy and maintain stability in the financial system.

In the United States, for example, the Troubled Asset Relief Program (TARP) was established in 2008 to provide financial assistance to banks and other financial institutions, including insurers, during the global financial crisis. The program authorized the US government to spend up to $700 billion to purchase troubled assets and equity from financial institutions, with the aim of stabilizing the financial system and preventing a deeper economic downturn. While the majority of TARP funds went to banks, several insurance companies, including American International Group (AIG), also received significant bailouts. AIG, which was on the brink of collapse due to its exposure to toxic mortgage-backed securities, received a total of $182 billion in government funds, making it one of the largest bailouts in history.

The rationale behind government bailouts for insurers in crisis is to prevent systemic risk and maintain financial stability. Insurers play a critical role in the economy by providing risk management services and financial protection to individuals and businesses. If a large insurer were to fail, it could have far-reaching consequences, including the loss of policyholder protection, reduced credit availability, and a decline in economic activity. By providing financial support to struggling insurers, governments aim to prevent these negative outcomes and maintain confidence in the financial system. However, government bailouts are not without controversy, as they can be seen as a form of corporate welfare and may create moral hazard by encouraging insurers to take excessive risks.

Despite these concerns, government bailouts for insurers in crisis remain an important tool for maintaining financial stability. To minimize the need for bailouts, regulators have implemented various measures, such as increased capital requirements, stress testing, and improved risk management practices. Additionally, some countries have established resolution frameworks that provide a structured process for dealing with failing insurers, which can help reduce the need for government intervention. Nevertheless, in situations where an insurer's failure poses a significant threat to financial stability, government bailouts may still be necessary. In such cases, it is essential that the bailout is designed to minimize taxpayer exposure, ensure accountability, and promote long-term sustainability in the insurance sector.

In conclusion, government bailouts for insurers in crisis are a complex and controversial issue, but one that is necessary to maintain financial stability and prevent systemic risk. While bailouts can be effective in preventing the collapse of struggling insurers, they should be used judiciously and designed to minimize taxpayer exposure and promote long-term sustainability. As the insurance sector continues to evolve and face new challenges, it is likely that government bailouts will remain an important tool for managing financial crises and maintaining stability in the financial system. By understanding the dynamics of government bailouts for insurers in crisis, policymakers, regulators, and industry participants can work together to create a more resilient and stable insurance sector.

Transferring Life and Health Insurance Licenses: Is It Possible?

You may want to see also

Frequently asked questions

In most cases, private insurance companies do not receive direct government funds for their operations. However, certain government programs, like Medicare and Medicaid in the U.S., pay insurance companies to manage healthcare plans for eligible individuals.

Some insurance companies receive indirect government support through subsidies, tax breaks, or payments for administering government-funded programs. For example, insurers participating in the Affordable Care Act (ACA) marketplaces may receive subsidies to reduce costs for low-income individuals.

Yes, the government funds insurance programs for specific populations, such as Medicare for seniors, Medicaid for low-income individuals, and veterans' health insurance through the VA. These programs are fully or partially funded by taxpayer dollars.