Dealing with insurance and towing companies can be a challenging and time-consuming process, and it's natural to wonder who will cover the costs of towing and storage after a car accident. The responsibility for paying these bills can vary depending on several factors, including the circumstances of the accident, your insurance coverage, and state regulations. In this text, we will explore the topic of insurance reimbursement for tow and storage services after a vehicular accident, providing insight into the factors that determine coverage and offering guidance on navigating the complex world of insurance claims and reimbursements.

Explore related products

What You'll Learn

![]()

Collision coverage

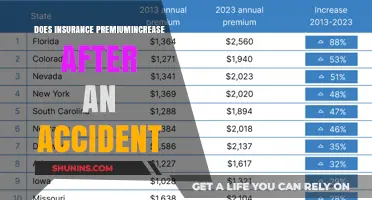

The cost of towing and storing a vehicle after an accident can be significant. Towing costs an average of $109 per trip, with rates ranging from $2.50 to $7 per mile. Storage fees, which are charged daily, can add up to $450 in just a few days. As such, it is important to understand your insurance policy's terms and limits to know whether and to what extent towing and storage costs are covered.

If you have collision coverage, your insurance company may cover the towing and storage expenses for your wrecked car, regardless of who is at fault for the accident. This means that even if you are found to be at fault, your collision coverage may still apply. However, it is important to note that different policies may have varying degrees of coverage for towing and storage costs, so it is essential to review your specific policy and consult your insurance provider to confirm your coverage.

In some cases, you may need to pay for towing and storage costs upfront and then seek reimbursement from your insurance company. Additionally, there may be limits to how much is covered, and you may be responsible for any excess fees. To mitigate costs, it is important to promptly contact the towing company to retrieve your vehicle and avoid additional storage charges.

It is worth noting that state regulations can also play a role in determining who pays for towing and storage fees. Some states have specific laws governing these charges after accidents, dictating whether the at-fault party's insurance, your own insurance, or another source is responsible for covering these expenses. Therefore, it is crucial to familiarize yourself with your state's insurance laws and regulations to understand how these costs are handled in your location.

Best Medical Insurance Options in California

You may want to see also

Explore related products

![]()

At-fault party's liability insurance

The at-fault party's liability insurance may cover towing and storage costs after an accident, but this is not always the case. It depends on the circumstances of the incident, the insurance coverage, and state regulations.

If the at-fault driver has liability insurance, their policy may cover the costs associated with accidents they cause, including towing and storage fees. These costs can be included in the claim filed with their insurance company, and the insurance adjuster will assess and compensate for the total damages, including towing and storage.

However, liability insurance policies often have limits, and there may be fees that are not covered and need to be paid out of pocket. Towing and storage fees can add up quickly, with storage fees charged daily, so it is essential to retrieve your vehicle promptly to avoid additional charges.

In some cases, the at-fault driver may not have insurance (uninsured) or may have insufficient coverage (underinsured). In these situations, you may need to rely on your own insurance policy, such as uninsured or underinsured motorist (UM/UIM) coverage, to cover the towing and storage costs.

It is important to review your insurance policy and understand the terms and limits of your coverage. Additionally, documenting the condition of your car and the fees incurred is crucial for filing claims and ensuring fair compensation.

The Art of Medical Cost Negotiation

You may want to see also

Explore related products

![]()

Uninsured/underinsured motorist coverage

Uninsured motorist coverage comes into effect when you are hit by a driver with no auto insurance, protecting you from the financial burden of damages and injuries. Underinsured motorist coverage, often offered alongside uninsured coverage, provides similar protection when the at-fault driver doesn't have adequate insurance to cover the costs of damages and injuries they caused. These coverages can be crucial in ensuring you are not left with substantial expenses, including towing and storage costs, after an accident involving an uninsured or underinsured driver.

In the unfortunate event of a hit-and-run accident, uninsured motorist coverage can provide valuable support. You can file a claim against your uninsured motorist policy, and it will cover damages to your vehicle and other property, depending on your state's regulations. Additionally, uninsured/underinsured motorist coverage can help cover medical bills for you and your passengers, including long-term care needs, through medical payments and personal injury protection components.

The deductibles for uninsured/underinsured coverage are generally lower than those for collision coverage. When purchasing this coverage, it is advisable to add sufficient property damage protection to replace your vehicle if needed. While insurance companies must offer this coverage when you buy auto insurance, you have the option to decline it in writing if you choose to do so.

State Wards: Medical Insurance Coverage Explained in Detail

You may want to see also

![]()

State regulations

Some states have specific laws governing towing and storage charges after accidents. These laws may outline the maximum fees that towing companies can charge for primary towing services and the circumstances under which additional fees may be applied. For example, in some states, towing companies are prohibited from charging excess fees for moving vehicles between their own storage lots.

Additionally, certain states operate under a no-fault insurance system, where each driver's insurance company covers their policyholder's expenses, regardless of who is at fault for the accident. In such cases, your insurance company may cover towing and storage fees, depending on your specific policy.

It is important to familiarize yourself with your state's insurance laws and regulations to understand how towing and storage costs are typically handled in your location. These regulations can impact your insurance coverage, claim processes, and financial responsibilities following an accident.

Furthermore, state regulations may also influence the process of releasing your vehicle from the towing company. In some states, a person or company who fails to release a vehicle upon receipt of the owner's or insurance company's written request and payment of authorized fees may be found guilty of a petty offense or, in the case of repeat offenses, a class 3 misdemeanor.

Health Insurance and Retroactive Coverage: What's the Deal?

You may want to see also

![]()

Mitigating costs

Regardless of who ultimately covers the towing and storage expenses, it is important to take steps to reduce the costs as much as possible. Here are some ways to mitigate the costs:

- Contact your insurance company promptly: It is important to notify your insurance company as soon as possible after the accident. They may have specific requirements or preferences for towing and storage services, and failing to follow their instructions could result in reduced coverage. Additionally, some insurance policies have time limits on coverage for towing and storage fees, so delaying the claim could result in additional expenses.

- Retrieve your vehicle from storage quickly: Towing companies typically charge daily storage fees, which can add up to significant amounts over time. The longer your vehicle remains in storage, the higher the costs will be. In some cases, insurance companies may refuse to pay storage fees beyond what they consider a reasonable amount of time. Therefore, it is in your best interest to retrieve your vehicle from storage as soon as possible to avoid accumulating unnecessary charges.

- Document the condition of your vehicle and fees incurred: Take photographs of the accident scene, including your vehicle, the road, street signs, and any damage to the vehicles involved. This documentation will be crucial when filing insurance claims or pursuing legal action. Additionally, keep a record of all fees and expenses associated with towing and storage to support your claim.

- Understand your insurance coverage and state regulations: Review your insurance policy to clarify the extent of your coverage for towing and storage fees. Different policies have varying degrees of coverage, and some may require you to use specific towing services to qualify for reimbursement. Additionally, state regulations can play a role in determining financial responsibility. Familiarize yourself with the laws in your state regarding towing and storage charges after accidents.

- Choose an affordable towing service: If possible, request to have your vehicle towed to a trusted mechanic or auto repair shop instead of a salvage yard. Towing companies may charge varying rates, so it is worth asking about their fees and comparing prices. Additionally, having your vehicle towed to a location you designate may help expedite the repair process and reduce storage fees.

- Consider membership in an auto club: Joining an auto club, such as AAA, can provide benefits that reduce towing costs. These clubs often offer discounted or included towing services up to a certain distance, which can help mitigate expenses.

Understanding Out-of-Pocket Costs for Medical Insurance Premiums

You may want to see also

Frequently asked questions

Whether or not insurance will reimburse tow and storage costs after an accident depends on the circumstances of the incident, who is at fault, and the type of insurance coverage you have. If you have collision coverage, your insurance company will likely cover towing and storage costs. If you are not at fault, your insurance company may reimburse you for these costs and then seek reimbursement from the at-fault driver or their insurance company.

In addition to the circumstances of the incident and the type of insurance coverage, state regulations can also play a role in determining whether insurance will reimburse tow and storage costs. Some states have specific laws governing these charges, while others operate under a no-fault insurance system, where each driver's insurance company covers their policyholder's expenses, regardless of fault.

To ensure reimbursement for tow and storage costs, it is important to review your insurance policy and consult your insurance provider to confirm the terms and limits of your coverage. Additionally, promptly contacting the towing company to retrieve your vehicle and avoid unnecessary storage charges is essential. Documenting the condition of your car, taking photos of the accident, and collecting the other driver's information and a copy of the police report can also help support your claim.