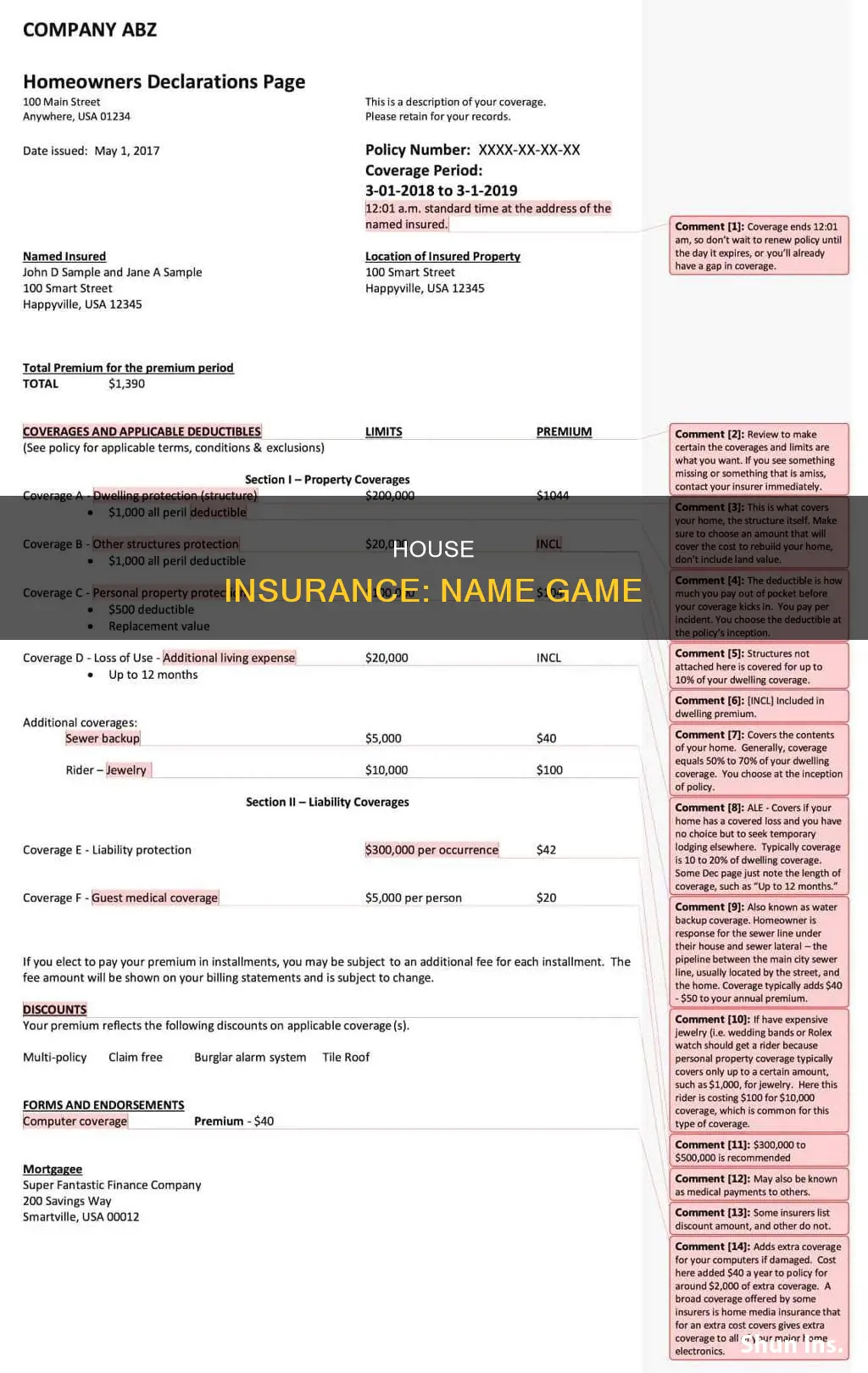

It is important to know whose name should be on house insurance. The rule of thumb is that the person or entity with a financial interest in a business or property should be listed as a named insured. For homeowners insurance, the policy must have the name of the current owner. If the property is jointly owned, both owners should be named insureds on the policy. If one spouse owns the property, the other can be added as a named insured. This is also true for renters insurance, where the primary policyholder and additional named insured are protected under liability coverage.

| Characteristics | Values |

|---|---|

| Who should be named on house insurance? | The person who owns the home that is being insured. |

| Who can be added as an "additional insured"? | Spouses, blood relatives, other people with the owner's permission to live in the house, and even an organization operating from within the home. |

| What happens when the insured person dies? | The estate becomes temporarily insured, with coverage expiring at the end of the policy period. |

| What happens when the property is inherited? | The new owner will need to negotiate with the insurance company regarding coverage and work to secure their own homeowner's insurance policy. |

| Do both spouses need to be on homeowners insurance? | Technically, no. But if both spouses own the property jointly, they should both be named insureds. |

| What happens if one spouse isn't on the policy? | They won't be able to make claims or changes to the policy, even if they live in the house. |

| Can unmarried couples have a joint policy? | Yes, but it is a rarer circumstance. |

| What about non-married partners? | The insurer may not agree to add them as a named insured. |

| What should the non-married partner do in this case? | They will need to get renters insurance to protect their belongings and limit their liability exposure. |

Explore related products

What You'll Learn

![]()

The primary policyholder

If the primary policyholder is the sole owner of the property, they can add their spouse as a named insured on the policy. This will provide coverage for their spouse and allow them to make claims or changes to the policy. It is important to note that adding a spouse as a named insured may increase the rate of the policy, depending on their claims history.

If both spouses own the property jointly, they should both be named insureds on the policy. In this case, the homeowners' insurance policy will be issued to both spouses, and they will have equal rights and responsibilities regarding the policy. This can prevent disputes and misunderstandings in the event of a claim or policy change.

Farmers Insurance ISP Outsourcing: The CSC Takeover

You may want to see also

Explore related products

![]()

Additional insured

An additional insured is a person or entity that is added to an insurance policy on top of the main policyholder (the named insured). The named insured is the person who took out the policy, and their name is on it.

The rule of thumb is that any person or entity with a financial interest in a business or property should be listed as an insured. In the case of home insurance, the main reason to add additional insureds is when multiple people who are not directly related share ownership of a home. For example, if you buy a house on your own and your significant other moves in with you, you could add them as an additional insured.

An additional insured must have an insurable interest in the property being insured; they must have some financial stake in the property. Usually, this involves some degree of ownership of the property. For instance, if you and a friend decide to purchase an investment property together, and you take out a home insurance policy, you would be the named insured, and your friend would be an additional insured.

The cost to add an additional insured to a policy varies by provider, but it is generally not expensive. It can be anywhere between $25 to $250 per person. Adding an additional insured to a policy does not change the amount of coverage the policy offers.

A.J.'s Insurance Insights: Navigating the World of Farmers Insurance

You may want to see also

Explore related products

![]()

Transferring deeds

A deed is a legal document representing property ownership. While it is possible to transfer a deed without a lawyer, it is important to ensure that the deed complies with your state's legal regulations to prevent any future legal challenges. The process of transferring deeds can be complex and may vary depending on the type of deed and the relationship between the parties involved. Here are the steps to transfer a deed:

- Retrieve your original deed: If you cannot find your original deed, obtain a certified copy from the recorder of deeds in the county where the property is located. Information such as the name on the deed, the year of purchase, and the property address will be required. There may be a fee for obtaining a copy of the deed.

- Obtain the appropriate deed form: Ensure you select the correct form for the specific county and state where the property is located.

- Draft the deed: The deed must clearly identify the property and include a legal description of the property, setting forth its boundaries. Include your name as the grantor (the party transferring the property) and the full legal name of the grantee (the new owner). The grantor's name on the new deed should match the name on the current deed. Also, provide the address, county, appraiser's property folio number or parcel ID, and the transfer date. The deed should contain a statement conveying the interest from the grantor to the grantee and specify the amount of consideration (the value exchanged for the deed). If there is no monetary exchange, it is common to state the consideration as $1.

- Sign the deed before a notary: As the grantor, you will need to sign the deed in the presence of a notary public, who will charge a small fee. In some states, the grantee may not need to sign, but the deed must be delivered and accepted by the grantee to be valid.

- Record the deed with the county recorder: The grantee should record the deed in the county where the property is located. This typically involves obtaining a Preliminary Change of Ownership Report to note the transaction details.

- Obtain the new original deed: The grantor should keep a certified copy of the newly recorded deed, while the grantee (new owner) should keep the original in a safe place.

Types of Deeds

There are several types of deeds, each with its own requirements and implications:

- Quitclaim deed: This type of deed is commonly used for transfers between family members or when no money is exchanged. With a quitclaim deed, you transfer whatever interest you have in the property without guaranteeing clear title or protecting the recipient from future defects in the title.

- Warranty deed: Also known as a general warranty deed, this type of deed is typically used when selling residential properties on the real estate market. It promises that there are no unmentioned lienholders, and the seller will defend the buyer's title against any claims. It also assures that the seller has resolved all mortgages, tax liens, and other relevant debts.

- Transfer-on-death (TOD) deed: This type of deed allows you to maintain full control of your property while you are alive, and it transfers to your chosen relative upon your death, avoiding probate.

- Joint tenancy: This involves creating a new deed listing both you and your relative as joint tenants with rights of survivorship. In this case, you are effectively selling your property to yourself and your relative, and both of you must acquire equal shares at the same time.

Important Considerations

When transferring a deed, there are several important considerations to keep in mind:

- Tax implications: Understand the potential tax consequences before transferring real estate, including any taxes on the deed transfer itself.

- Medicaid: Federal law and state provisions impose a waiting period after transferring an interest in a house before you can qualify for Medicaid benefits.

- Divorce: If you use a quitclaim deed to transfer your interest in a jointly owned property, remember that you may still be responsible for any mortgages or community property connected to the loan.

- Insurance: Ensure that your home insurance policy is updated to match the name on the deed. Contact your insurance company to make any necessary changes and discuss the specific requirements.

- Mortgage: If there is a mortgage on the property, it will need to be paid off or assumed by the recipient. Adding someone to the deed instead of conveying it outright may be a workaround, but there can be drawbacks to sharing the title.

Farmers Insurance and Erie Insurance: Partners or Competitors?

You may want to see also

Explore related products

![]()

Joint tenancy

To establish a joint tenancy, four conditions, often referred to as "unities", must be met:

- Unity of title: Each joint tenant owns the same property at the same time.

- Unity of interest: Each joint tenant has an identical percentage of interest in the property.

- Unity of possession: Each joint tenant has the right to possess the entire property.

- Unity of time: Each joint tenant receives their interest in the property at the same time.

In the context of home insurance, it is generally preferable to have a single policy for all joint tenants. This ensures that each joint tenant has the same level of protection against potential liability, damage, or loss due to a covered claim. Therefore, when taking out home insurance, it is important to include all the names of the joint tenants on the policy.

One key feature of joint tenancy is the right of survivorship. This means that if one joint tenant dies, their share of the property automatically passes to the surviving tenant(s) without the need for probate or court involvement. This seamless transfer of ownership can save costs associated with creating wills and probate proceedings.

However, joint tenancy also has some potential disadvantages. For example, joint tenants must make decisions together, which can lead to disagreements, especially during a divorce. Additionally, if one joint tenant incurs debts, creditors could place a lien on the property, impacting the investments of the other joint tenants.

Dashcam Discounts: Do They Impact Farmers' Insurance Policies?

You may want to see also

Explore related products

![]()

Marital status

In addition, marriage often results in more items and vehicles that need to be insured. Combining home and auto insurance policies can lead to significant discounts for married couples. It is important to update your policy to reflect your change in marital status and ensure your partner is covered.

Furthermore, living with a partner means that belongings are combined, requiring additional personal property coverage. Any new gifts received as newlyweds, such as fine china, appliances, or jewellery, should be added to the coverage.

While marriage can result in lower insurance premiums, it is important to note that other factors, such as driving records and claims history, also play a role in determining insurance costs.

Florida Home Insurance: A Must-Have?

You may want to see also

Frequently asked questions

While adding a joint policyholder is not compulsory, without it, the other person would not be able to make a claim or cancel the policy.

A named insured is entitled to 100% of the benefits and coverage provided by the policy. An additional insured is someone who is not the owner of the policy but, under certain circumstances, may be entitled to some of the benefits and a certain amount of coverage under the policy.

The property owner, meaning the person whose name is on the title of the house, typically goes on the homeowners insurance policy.