Medicare is the federal health insurance program for people aged 65 and over. If you have individual health insurance and are wondering if you can enroll in Medicare, there are a few things to consider. Firstly, you need to determine if your current insurance is employer group health plan coverage or individual health coverage. If it is individual health coverage, you may be able to delay signing up for Medicare Part B without a late enrollment penalty. However, if you have individual health insurance and want to switch to Medicare, it is recommended to speak with your benefits administrator or insurance provider to understand how your current coverage will work with Medicare before making any changes. Once you enroll in Medicare, you can choose between Original Medicare and Medicare Advantage, and decide whether to add drug coverage.

| Characteristics | Values |

|---|---|

| Medicare eligibility | Individuals aged 65 and over |

| Medicare Part A | Hospital Insurance |

| Medicare Part B | Medical Insurance |

| Medicare Part C | Medicare Advantage Plans (private insurance option) |

| Medicare Part D | Prescription medications |

| Medicare Supplement Insurance | Medigap (helps pay your share of costs in Original Medicare) |

| Enrollment Period | Begins 3 months before turning 65 and ends 3 months after the month of turning 65 |

| Late Enrollment Penalty | May apply if you miss the Initial Enrollment Period |

| Special Enrollment Period | Available for certain conditions, allowing delayed enrollment without penalty |

| Eligibility for premium-free Part A | Based on earnings, spouse's earnings, or qualifying conditions |

Explore related products

What You'll Learn

![]()

Eligibility for premium-free Medicare Part A

To be eligible for premium-free Medicare Part A, an individual must be entitled to receive Medicare based on their own earnings or those of a spouse, parent, or child. The worker must have a specified number of quarters of coverage (QCs) and file an application for Social Security or Railroad Retirement Board (RRB) benefits.

The exact number of QCs required depends on whether the person is filing for Part A on the basis of age, disability, or End Stage Renal Disease (ESRD). QCs are earned through payment of payroll taxes under the Federal Insurance Contributions Act (FICA) during the person's working years. Most individuals pay the full FICA tax, so the QCs they earn can be used to meet the requirements for both monthly Social Security benefits and premium-free Part A.

Individuals who are eligible for premium-free Part A are also eligible to enroll in Part B once they are entitled to Part A. If you have to pay a premium for Part A, you must meet additional requirements to enroll in Part B, including being a U.S. citizen or lawfully admitted resident.

If you are over 65 and Medicare-eligible, you can sign up for Part A for free if you have at least 40 calendar quarters of work in any job where you paid Social Security taxes in the U.S. Calendar quarters refer to three-month periods ending on March 31, June 30, September 30, or December 31.

You may also be eligible for premium-free Part A if you were a federal employee after December 31, 1982, or a state or local employee after March 31, 1986. If you do not meet these criteria, you will likely pay a monthly premium for Part A, the cost of which depends on your work history.

If you have a low income, you may be eligible for the Qualified Medicare Beneficiary (QMB) program, which pays for your Medicare Part A and B premiums and other costs.

Nxstage and Medical Insurance: What You Need to Know

You may want to see also

Explore related products

$19.95 $9.07

![]()

Medicare Part B enrollment

Leaving individual insurance does allow you to enrol in Medicare. If you have other health insurance or drug coverage, you should talk to your benefits administrator or other insurance provider before making any changes to your current coverage.

Medicare Part B helps pay for your basic healthcare services. If you already have Part A, you can add Part B during specific enrollment periods. If you are enrolling in Part A and Part B, you will need to contact the Social Security Administration (SSA).

If you have to pay a premium for Part A, you can choose to drop it, but you can also choose to drop Part B. However, there are some risks to dropping coverage. If you have retiree coverage from a previous job, it may not pay for your health services if you don't have both Part A and Part B.

If you or your spouse are still working, you may be able to wait to sign up for Medicare without paying a late enrollment penalty. If you have group health insurance available to everyone at your company, you can choose to sign up when you turn 65 or anytime after. You can wait until you or your spouse stop working or lose your health insurance to sign up for Part B, and you won't pay a late enrollment penalty. Once you stop working or lose your insurance, you have an 8-month Special Enrollment Period (SEP) when you can sign up for Medicare or add Part B to existing Part A coverage.

If you've been covered by an active employer group health plan (either yours or your spouse's) since turning 65, and it ended within the last 8 months, you can enroll in Part B without any penalty. This is also considered an SEP, and you can apply any time of the year.

If you don't sign up for Medicare when you turn 65, you may have to pay a monthly Part B late enrollment penalty.

Medical Insurance: Unaffordable and Unavailable for Many

You may want to see also

Explore related products

![]()

Medicare Part A and Part B enrollment options

Initial Enrollment Period (IEP)

The Initial Enrollment Period is the first opportunity for individuals to sign up for Medicare Part A and Part B. This period typically begins three months before an individual turns 65 and ends three months after their birthday month, for a total of seven months. During this time, individuals can enroll in Medicare Parts A and B without incurring late enrollment penalties.

Special Enrollment Period (SEP)

The Special Enrollment Period allows individuals who missed their Initial Enrollment Period to sign up for Medicare Parts A and B at a later date without penalties. This period is available to those who have maintained an active employer group health plan, either their own or their spouse's, after turning 65. The SEP typically lasts for eight months, starting from the month after the group health plan coverage ends.

Exceptional Conditions SEP

Individuals who missed their Initial Enrollment Period due to exceptional circumstances, such as volunteering outside the US for at least 12 months or being incarcerated, may qualify for the Exceptional Conditions SEP. They can enroll in Medicare Parts A and B without penalties during the specified time frame.

General Enrollment Period (GEP)

The General Enrollment Period is for individuals who did not sign up during their Initial Enrollment Period or a Special Enrollment Period. The GEP takes place annually, from January 1 to March 31, and allows individuals to enroll in Medicare Parts A and B. However, those enrolling during this period may have to pay a late enrollment penalty.

Medicare Advantage Open Enrollment Period

The Medicare Advantage Open Enrollment Period occurs annually, from January 1 to March 31. During this time, individuals who are already enrolled in Medicare Parts A and B can make changes to their coverage, such as switching to a different Medicare Advantage Plan or returning to Original Medicare.

It is important to note that Medicare Part A provides hospital insurance, while Part B offers medical insurance. Individuals can choose to enroll in these parts of Medicare based on their eligibility, personal circumstances, and health needs.

Bupa Medical Insurance: Understanding the Cost and Coverage

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare enrollment periods

Medicare is a federal health insurance program for people aged 65 and over, and younger people with disabilities. There are different ways to get Medicare coverage, including Original Medicare (Parts A and B) and Medicare Advantage Plans (Part C).

If you are leaving your individual insurance plan, you may be able to enroll in Medicare during a Special Enrollment Period (SEP). A Special Enrollment Period is a specific time outside of the standard Initial Enrollment Period when you can sign up for Medicare without paying a late enrollment penalty.

- Initial Enrollment Period: This is the first chance for individuals to sign up for Medicare when they turn 65. It lasts for 7 months, starting 3 months before your 65th birthday and ending 3 months after the month you turn 65. If you miss this period, you may have to pay a late enrollment penalty for Part B coverage and premium Part A coverage.

- Special Enrollment Period (SEP): A Special Enrollment Period is a specific time when you can enroll in Medicare outside of the standard Initial Enrollment Period without paying a late enrollment penalty. You may qualify for a Special Enrollment Period if you have certain life changes, such as losing your current health coverage or ending volunteer service outside the US. The length of the SEP varies depending on the situation, but it typically lasts for 6 to 8 months.

- General Enrollment Period: If you missed your Initial Enrollment Period and do not qualify for a Special Enrollment Period, you can enroll in Medicare during the General Enrollment Period. This period runs from January 1st to March 31st each year. Your coverage will start the month after you sign up, and you may have to pay a monthly late enrollment penalty.

- Medicare Advantage Plan Enrollment Periods: If you are enrolled in a Medicare Advantage Plan (Part C), you can make changes to your plan or switch back to Original Medicare during certain times of the year. These enrollment periods are specific to Medicare Advantage Plans and may vary depending on the plan.

It is important to note that the rules and requirements for Medicare enrollment can be complex, and they may change over time. Therefore, it is always a good idea to review the official Medicare website or consult with a benefits administrator to ensure you have the most up-to-date and accurate information.

Understanding Family Medical Leave Insurance

You may want to see also

Explore related products

![]()

Cancelling Medicare coverage

If you have individual insurance, you can choose to sign up for Medicare when you turn 65. You can also wait until you stop working or lose your health insurance to sign up for Medicare without paying a late enrollment penalty.

If you cancel your Original Medicare (Parts A and B) or Medicare Advantage (Part C) plan without a replacement, you may be fully responsible for all healthcare costs moving forward. You can sign up for new Medicare coverage during the next open enrollment period or the next special enrollment period, but you may be subject to late enrollment penalties.

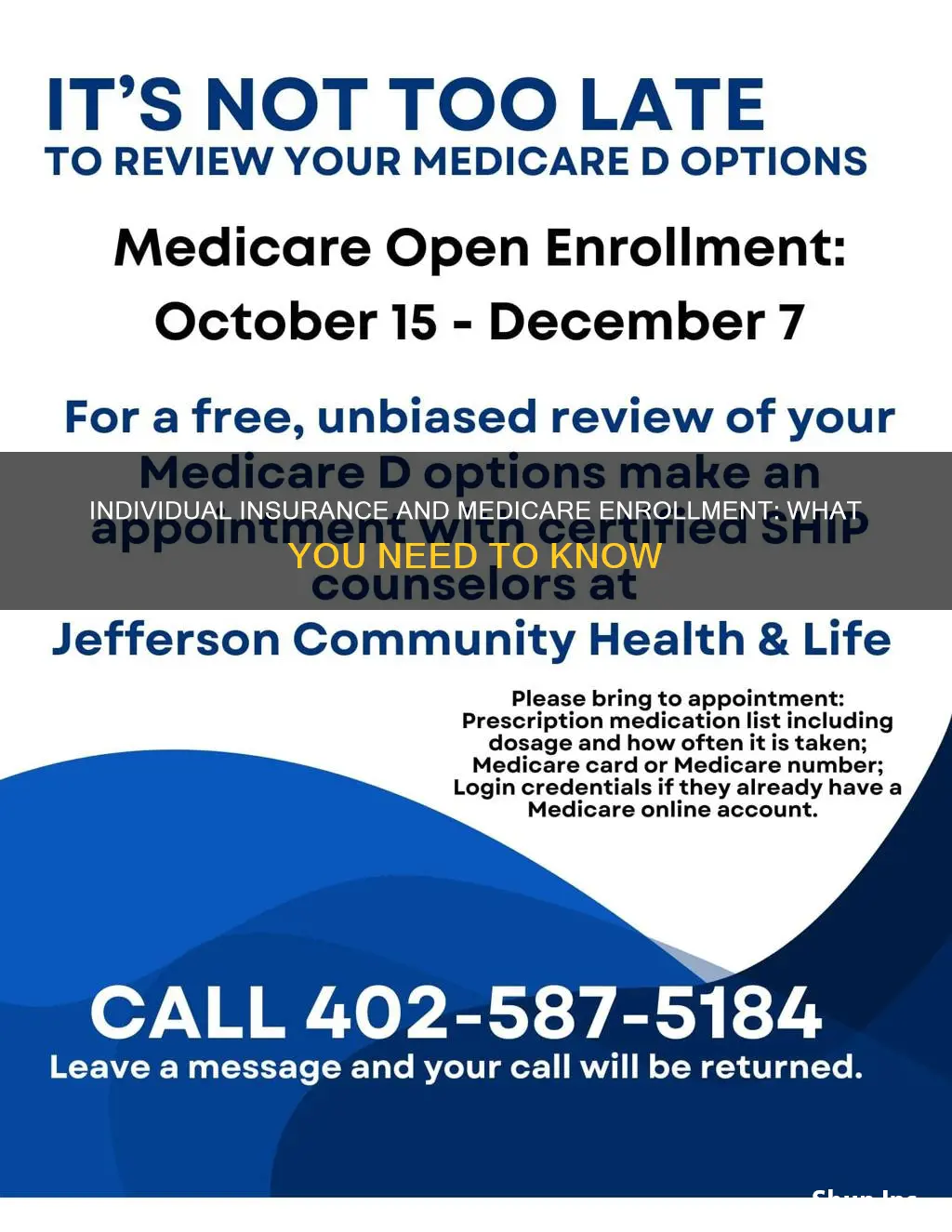

You can only cancel Part C during an open enrollment period or special enrollment period. The annual open enrollment period for all Medicare plans lasts from October 15 to December 7. To cancel, you must contact your Part C provider directly. It usually involves submitting a written request or completing a disenrollment form.

You can cancel premium Part A at any time. You can only cancel Part A if you pay a monthly premium. To cancel, download Form CMS-1763 from the Medicare website or visit your local Social Security office to receive a paper copy. Make sure you fill it out completely.

You can cancel Part B at any time. If you recently received a welcome packet notifying you of your automatic enrollment, you must follow the instructions included in your packet to opt out of coverage. This usually involves mailing your Medicare card back. If you don’t return the card, you will be responsible for paying the monthly premium for Part B.

You can only cancel Part D during an open enrollment period or special enrollment period. The annual open enrollment period for all Medicare plans lasts from October 15 to December 7. It usually involves submitting a written request or completing a disenrollment form.

Job Insurance Terminated? Apply for Coverage Now!

You may want to see also

Frequently asked questions

Medicare Part A is insurance for hospitalization, home or skilled nursing, and hospice.

If you have individual insurance, you may not need to apply for Medicare Part B at age 65. You may qualify for a Special Enrollment Period and can delay signing up for Medicare without a late enrollment penalty.

The Initial Enrollment Period for Medicare begins 3 months before you turn 65 and ends 3 months after the month you turn 65—a total of 7 months. You may have to pay a penalty if you miss this period.

If you have other health insurance or drug coverage, talk to your benefits administrator or insurance provider before making any changes to your current coverage.