When considering whether marketplace insurance counts other income, it’s important to understand how the Affordable Care Act (ACA) determines eligibility for subsidies and coverage. Marketplace insurance, also known as health insurance through Healthcare.gov or state-based exchanges, primarily uses your Modified Adjusted Gross Income (MAGI) to assess your eligibility for premium tax credits or Medicaid. This calculation typically includes wages, salaries, self-employment income, and certain investment earnings. However, other types of income, such as Social Security benefits, unemployment benefits, or child support, may also be factored in, depending on how they are reported on your tax return. Understanding which income sources are counted is crucial, as it directly impacts your eligibility for financial assistance and the affordability of your health insurance plan.

| Characteristics | Values |

|---|---|

| Does Marketplace Insurance Count Other Income? | Yes, but with specific conditions and limitations. |

| Types of Income Considered | Wages, salaries, tips, self-employment income, unemployment benefits, Social Security, alimony, and other taxable income. |

| Excluded Income Types | Child support, gifts, and certain non-taxable income sources. |

| Income Calculation Method | Modified Adjusted Gross Income (MAGI) is used to determine eligibility. |

| Impact on Premium Tax Credits | Higher income may reduce or eliminate eligibility for premium tax credits. |

| Medicaid Eligibility | Medicaid eligibility is also based on MAGI, but rules vary by state. |

| Reporting Requirements | All income must be reported accurately during the application process. |

| Annual Income Updates | Income changes must be reported to the Marketplace to adjust subsidies. |

| Penalty for Underreporting | Underreporting income may result in repayment of excess subsidies. |

| Special Circumstances | Certain deductions and exemptions may apply, such as student loan interest or self-employment expenses. |

| State-Specific Variations | Some states have expanded Medicaid programs with different income thresholds. |

Explore related products

What You'll Learn

![]()

How Marketplace Insurance Calculates Income

When determining eligibility for health insurance through the Marketplace, understanding how income is calculated is crucial. The Marketplace primarily uses Modified Adjusted Gross Income (MAGI) to assess whether an individual or household qualifies for premium tax credits or cost-sharing reductions. MAGI is derived from your Adjusted Gross Income (AGI) as reported on your federal tax return, with certain modifications. This includes adding back certain deductions, such as foreign earned income or student loan interest, to arrive at a more comprehensive income figure. The MAGI calculation ensures that all relevant income sources are considered for insurance purposes.

One common question is whether other types of income are counted in this calculation. The answer is yes—the Marketplace considers a wide range of income sources beyond just wages or salaries. This includes self-employment income, capital gains, unemployment compensation, Social Security benefits, alimony, and rental income. Even non-taxable income, such as tax-exempt interest or certain veterans' benefits, may be included in the MAGI calculation. This comprehensive approach ensures that the Marketplace has a complete picture of your financial situation when determining eligibility for subsidies.

For individuals with fluctuating or irregular income, estimating income accurately can be challenging. The Marketplace advises using your best estimate of the upcoming year's income. If your income changes during the year, you can update your information through the Marketplace to ensure your coverage and subsidies remain accurate. It’s important to report changes promptly, as underestimating or overestimating income can affect your eligibility for financial assistance and may require repayment of excess subsidies at tax time.

Households with multiple income sources must combine all income streams for the MAGI calculation. For example, if a married couple files jointly, both spouses' incomes, including wages, investment income, and other earnings, are added together. Similarly, if a household includes dependents with income, such as a child with a part-time job, that income may also be factored in, depending on how it is reported for tax purposes. This holistic approach ensures fairness in determining eligibility for Marketplace subsidies.

Finally, it’s important to note that certain types of income are not counted in the MAGI calculation. These include gifts, inheritances, child support payments received, and one-time payments like workers' compensation. Additionally, Supplemental Security Income (SSI) and benefits from the Temporary Assistance for Needy Families (TANF) program are typically excluded. Understanding which income sources are included or excluded can help you accurately estimate your eligibility for Marketplace insurance and avoid surprises during the application process.

Supplemental Life Insurance: Enhancing Your Coverage and Peace of Mind

You may want to see also

Explore related products

$49.56 $99.99

![]()

Types of Income Counted in Subsidy Eligibility

When determining eligibility for health insurance subsidies through the Marketplace, understanding which types of income are counted is crucial. The Affordable Care Act (ACA) uses Modified Adjusted Gross Income (MAGI) as the primary measure to assess subsidy eligibility. MAGI includes most, but not all, sources of income reported on your federal tax return. This ensures a comprehensive evaluation of your financial situation to determine if you qualify for premium tax credits or cost-sharing reductions.

Earned Income is one of the primary types of income counted in subsidy eligibility. This includes wages, salaries, tips, and any other compensation received from employment. Self-employment income, such as profits from a business or freelance work, is also included. These forms of earned income are reported on your tax return and directly impact your MAGI, which in turn affects your subsidy eligibility. It’s important to accurately report all earned income to ensure proper calculation of your subsidy.

Unearned Income is another category that factors into subsidy eligibility. This includes investment income, such as dividends, capital gains, and interest earned from savings accounts or other investments. Rental income, royalties, and pension or retirement benefits are also considered unearned income. Even taxable Social Security benefits and unemployment compensation are counted. While these sources may not be as straightforward as earned income, they are still included in your MAGI and can influence your eligibility for subsidies.

Taxable Non-Cash Benefits and certain tax-exempt income are also counted in subsidy eligibility calculations. For example, tax-exempt interest (like from municipal bonds) and employer-provided adoption benefits are included in MAGI. Additionally, foreign earned income and housing allowances for military personnel or civilians working abroad are factored in. These less common forms of income can sometimes be overlooked but are important to report accurately to avoid discrepancies in subsidy calculations.

Lastly, income from dependents may be considered if they are required to file taxes. For instance, if a dependent has significant investment income, it could be included in the household’s MAGI. However, income from child support or other non-taxable benefits, such as Supplemental Security Income (SSI), is generally not counted. Understanding which types of income are included—and which are excluded—is essential for accurately estimating your subsidy eligibility and ensuring compliance with Marketplace rules. Always consult the latest guidelines or a tax professional for specific advice tailored to your situation.

Does Insurance Cover Windshield Replacement in Florida? What You Need to Know

You may want to see also

Explore related products

![]()

Impact of Spousal Income on Premiums

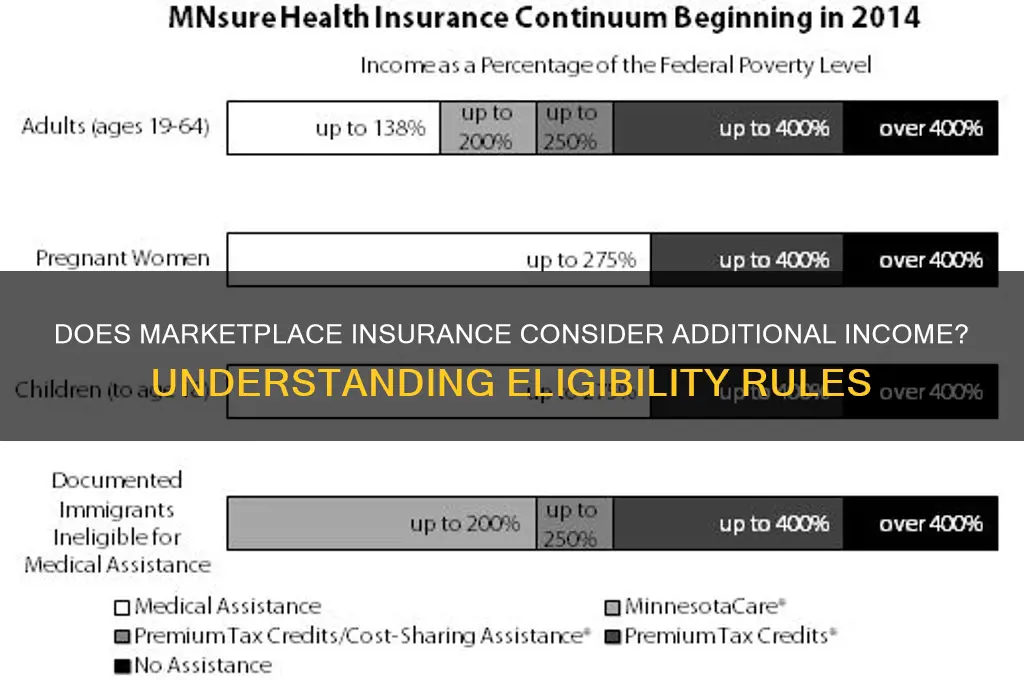

When applying for health insurance through the Marketplace, understanding how spousal income impacts premiums is crucial. The Marketplace, also known as the Health Insurance Marketplace, considers the total household income, including spousal income, to determine eligibility for premium tax credits and cost-sharing reductions. This means that if you’re married and filing taxes jointly, your spouse’s income will directly affect the premiums you pay for health insurance. The combined income is used to calculate the Modified Adjusted Gross Income (MAGI), which is a key factor in assessing your financial eligibility for subsidies.

The impact of spousal income on premiums becomes significant when it pushes your household income above certain thresholds. For instance, if your combined income exceeds 400% of the Federal Poverty Level (FPL), you may no longer qualify for premium tax credits. This can result in higher out-of-pocket costs for health insurance. Conversely, if your spousal income is low or moderate, it may help you qualify for subsidies, reducing your overall premium costs. It’s essential to accurately report both your and your spouse’s income to ensure you receive the correct amount of financial assistance.

Another important consideration is how spousal income affects the benchmark plan and your premium tax credit. The benchmark plan is the second-lowest-cost silver plan available in your area, and the premium tax credit is designed to cover the difference between the benchmark plan’s premium and a percentage of your income. If your spousal income increases, the percentage of income you’re expected to pay for the benchmark plan also increases, potentially reducing the amount of your tax credit. This can lead to higher premiums if your income rises significantly.

For couples with uneven incomes, where one spouse earns significantly more than the other, the higher-earning spouse’s income will have a more substantial impact on premiums. However, even if one spouse has no income, the other’s income will still determine eligibility for subsidies. It’s also worth noting that certain types of income, such as Social Security benefits or unemployment compensation, may be counted differently, so it’s important to understand how all sources of income are treated in the calculation.

Lastly, changes in spousal income during the year can affect your premiums and subsidies. If your spouse’s income increases or decreases significantly, you may need to update your information on the Marketplace to avoid repaying excess subsidies at tax time or missing out on additional assistance. Regularly reviewing and updating your income information ensures that your premiums remain accurate and that you’re receiving the appropriate level of financial support. Understanding these dynamics is key to managing your health insurance costs effectively.

Haven Life vs AAA: Which Insurance is the Best?

You may want to see also

Explore related products

![Magi Adventure of Sinbad COMPLETE BOX (Limited Edition) [Blu-ray] JAPANESE EDITION](https://m.media-amazon.com/images/I/71oJ3zSScuL._AC_UY218_.jpg)

![]()

Self-Employment Income and Marketplace Subsidies

When applying for health insurance through the Marketplace, self-employment income plays a significant role in determining eligibility for premium tax credits and other subsidies. The Marketplace considers all sources of income, including self-employment earnings, to calculate your Modified Adjusted Gross Income (MAGI). This figure is crucial because it helps assess whether you qualify for financial assistance to reduce your monthly premiums or out-of-pocket costs. Self-employed individuals must accurately report their net profit from self-employment, which is calculated by subtracting business expenses from total revenue. Failing to account for all income sources, including self-employment, can lead to incorrect subsidy amounts and potential repayment of excess credits during tax season.

For self-employed individuals, estimating income for the upcoming year can be challenging due to fluctuating earnings. The Marketplace allows you to project your annual self-employment income based on past earnings, current trends, and expected changes in your business. It’s essential to be as accurate as possible when estimating, as underestimating income may result in receiving more subsidies than you qualify for, while overestimating could mean missing out on financial assistance. If your actual income differs significantly from your estimate during the year, you should update your Marketplace application to avoid surprises when filing taxes.

Self-employment income is not just limited to freelance or contract work; it also includes income from gig economy jobs, small business ownership, and other entrepreneurial activities. The Marketplace counts all taxable income from these sources, so it’s important to keep detailed records of your earnings and expenses. Using tools like profit-and-loss statements or consulting a tax professional can help ensure accurate reporting. Additionally, if you have both self-employment income and other sources of income (e.g., investments or rental properties), all of these will be factored into your MAGI for subsidy calculations.

One common misconception is that self-employment income might disqualify individuals from receiving Marketplace subsidies. In reality, self-employed individuals often qualify for premium tax credits, especially if their income falls within the eligibility range (100% to 400% of the federal poverty level, depending on household size). However, those with income above 400% of the poverty level are not eligible for premium tax credits but may still purchase plans through the Marketplace without subsidies. Understanding how self-employment income affects your MAGI is key to maximizing your eligibility for financial assistance.

Finally, self-employed individuals should be aware of how changes in income throughout the year can impact their Marketplace subsidies. If your income increases or decreases significantly, you must report these changes to the Marketplace promptly. Failure to do so could result in incorrect subsidy payments and potential repayment obligations. Regularly updating your income information ensures that your subsidies remain aligned with your financial situation, providing the appropriate level of assistance for your health insurance coverage. By staying proactive and informed, self-employed individuals can navigate the complexities of Marketplace subsidies effectively.

Understanding Liberalization in Insurance: Benefits, Challenges, and Impact

You may want to see also

Explore related products

![]()

Reporting Additional Income to Healthcare.gov

When applying for health insurance through Healthcare.gov, it’s crucial to accurately report all sources of income to ensure you receive the correct premium tax credits or subsidies. The Marketplace considers not just your primary income but also additional income sources to determine your eligibility and financial assistance. This includes income from self-employment, investments, rental properties, alimony, and other taxable sources. Failing to report additional income can lead to incorrect subsidy calculations, potentially resulting in higher premiums or repayment of excess credits when you file taxes.

To report additional income on Healthcare.gov, start by gathering all relevant income documentation, such as tax returns, pay stubs, and records of other earnings. During the application process, you’ll be prompted to provide details about your household income. Be sure to include all sources, even if they are irregular or sporadic. For example, if you receive income from freelance work or a side business, estimate your annual earnings and report them accurately. The Marketplace uses your modified adjusted gross income (MAGI) to assess eligibility, so transparency is key.

If your income changes during the year, it’s essential to update your information on Healthcare.gov promptly. Life events such as starting a new job, receiving an inheritance, or earning capital gains can impact your eligibility for subsidies. Log into your Marketplace account and report the changes to avoid discrepancies. Failure to update your income could result in overpayment of subsidies, which would need to be repaid at tax time, or underpayment, leading to higher premiums than necessary.

For those with complex income situations, such as self-employment or multiple income streams, it may be helpful to consult a tax professional or use the tools provided on Healthcare.gov to estimate your income accurately. The Marketplace offers resources to help you understand how different types of income are counted. Remember, the goal is to provide a complete and accurate picture of your financial situation to ensure you receive the appropriate level of assistance.

Finally, keep in mind that the Affordable Care Act (ACA) requires verification of income, and the Marketplace may cross-reference your reported income with data from the IRS. Providing truthful and comprehensive information not only ensures compliance with the law but also helps you secure the most affordable health insurance plan available. Reporting additional income correctly is a critical step in navigating the Healthcare.gov application process and maximizing your benefits.

Life vs Health Insurance: Which Policy Sells Better?

You may want to see also

Frequently asked questions

Yes, Marketplace insurance counts your spouse's income as part of your household income when determining eligibility for subsidies or Medicaid.

Yes, income from investments, rental properties, and other sources is typically included in the calculation of your household income for Marketplace insurance purposes.

Yes, Social Security benefits, including retirement, disability, and Supplemental Security Income (SSI), are generally counted as income for Marketplace insurance eligibility.

Yes, child support and alimony payments received are typically included as part of your household income when applying for Marketplace insurance.