If you have Medicare and another form of health insurance, you may be wondering how the costs will be covered by each provider. In this case, each type of coverage is called a payer, with one deemed the primary payer and the other the secondary payer. The primary payer covers costs up to the limits of its coverage, with the secondary payer then covering the remaining balance. Medicare is usually the secondary payer, though there are exceptions, such as if you are on active duty and have Medicare and TRICARE coverage. In this instance, TRICARE pays first for Medicare-covered services. It is important to notify your doctor or healthcare provider about any changes in your insurance or coverage.

| Characteristics | Values |

|---|---|

| Medicare Part A | Hospital Insurance |

| Medicare Part B | Medical Insurance |

| Medicare Part D | Drug coverage |

| Medicare Supplement Insurance (Medigap) | Extra insurance to help pay your share of costs in Original Medicare |

| Medicare Advantage Plan | Alternative to Original Medicare for health and drug coverage |

| Primary Payer | Pays up to the limits of its coverage |

| Secondary Payer | Pays the remaining balance after the primary payer |

| Conditional Payment | Medicare makes a payment when the primary payer should have but didn't |

Explore related products

What You'll Learn

![]()

Medicare Part A and Part B

Medicare is federal health insurance for anyone aged 65 and older, as well as some people under 65 with certain disabilities or conditions. Original Medicare includes Part A and Part B.

Medicare Part A (Hospital Insurance) covers inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. Most people get Part A for free, but some have to pay a premium for this coverage. To be eligible for premium-free Part A, an individual must be entitled to receive Medicare based on their own earnings or those of a spouse, parent, or child. To receive premium-free Part A, the worker must have a specified number of quarters of coverage (QCs) and file an application for Social Security or Railroad Retirement Board (RRB) benefits. The exact number of QCs required depends on whether the person is filing for Part A based on age, disability, or End Stage Renal Disease (ESRD). QCs are earned through payment of payroll taxes under the Federal Insurance Contributions Act (FICA) during the person's working years.

Medicare Part B is the Medical Insurance component. Once you've signed up for Part A and Part B, you can choose how you get your health coverage. There are two main ways to get your Medicare coverage: Original Medicare and Medicare Advantage. With Original Medicare, you pay for services as you get them. When you get a covered service, Medicare pays part of the cost, and you pay your share. You can see any doctor or hospital that accepts Medicare, anywhere in the US. With Medicare Advantage, you must sign up for Part A or Part B before enrolling. This is an alternative to Parts A and B that bundles several coverage types, including Parts A, B, and usually Part D (which covers prescription drug costs). In many cases, you can only use doctors who are in the plan's network.

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage, then sends the rest of the balance to the "secondary payer". If the secondary payer doesn't cover the remaining balance, you may be responsible for the remaining costs.

Health vs Auto Insurance: What Makes Them Different?

You may want to see also

Explore related products

![]()

Primary and secondary payers

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage and then sends the remaining balance to the "secondary payer".

The primary payer is the insurer that pays a healthcare bill first. The secondary payer covers the remaining costs, such as coinsurances or copayments. When you become eligible for Medicare, you can still use other insurance plans to lower your costs and get access to more services. Medicare will typically act as the primary payer and cover most of your costs once you're enrolled in benefits. Your other health insurance plan will then act as the secondary payer and cover any remaining costs.

For example, if you have an X-ray bill for $100, the bill will first be sent to your primary payer, which would pay the amount agreed upon by your plan. If your primary payer was Medicare, Medicare Part B would pay 80% of the cost and cover $80. Typically, you would be responsible for the remaining $20. If you have a secondary payer, they would pay the remaining $20 instead. In some cases, the secondary payer might not pay all the remaining costs, in which case you will receive a bill for the amount left after the primary and secondary payers have paid their covered parts of the fees.

Medigap policies, or Medicare Supplement Insurance, are extra insurance you can buy from a private company to help pay your share of costs in Original Medicare. Generally, you need Part A and Part B to buy a Medigap policy. Some Medigap policies offer coverage when you travel outside the U.S. Most state Medicaid plans will also cover the majority of your out-of-pocket costs and can act as a secondary payer.

Florida's Cheapest Auto Insurance: How to Find the Best Rates

You may want to see also

Explore related products

![]()

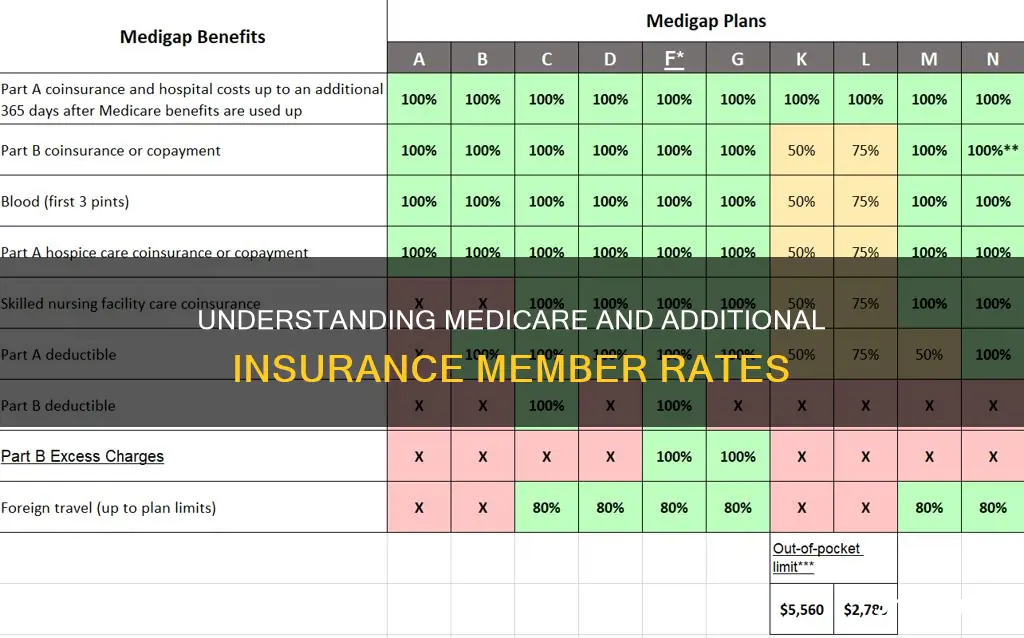

Medicare Supplement Insurance (Medigap)

Medicare Supplement Insurance, also known as Medigap, is additional insurance that can be purchased from a private health insurance company to help cover out-of-pocket costs in Original Medicare (Parts A and B). Medigap policies are designed to assist with costs such as deductibles, copays, and coinsurance, which are not covered by Parts A and B. These plans are available across the United States and Washington, D.C., with some variation in premiums and enrolment eligibility. Medigap policies are standardized, and in most states, they are named by letters indicating the level of coverage, such as Plan G or Plan K. The benefits within each lettered plan are consistent, regardless of the insurance company providing it. The primary difference between policies with identical letters offered by various companies is the price.

To be eligible for Medigap, you typically must already have Original Medicare, including Part A (Hospital Insurance) and Part B (Medical Insurance). Most individuals are eligible for Part A without a premium, but some may need to pay for this coverage depending on their specific circumstances. To qualify for premium-free Part A, an individual must meet certain requirements based on their earnings or those of their spouse, parent, or child. Enrolment in Part B, on the other hand, may depend on factors such as prior volunteer service outside the United States or eligibility for TRICARE.

Medigap coverage generally has no network limitations and can be used anywhere that accepts Medicare. Some Medigap plans also offer coverage for foreign travel emergency services. It is important to note that Medigap policies typically do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Additionally, if you are under 65, there may be restrictions or higher costs associated with purchasing a Medigap policy.

When considering Medigap insurance, it is essential to understand how Medicare coordinates with other insurance providers. If you have Medicare and another form of health insurance, each type of coverage is designated as a "payer." The "primary payer" pays up to its coverage limit and then forwards the remaining balance to the "secondary payer." If the secondary payer does not cover the remaining balance, you may be responsible for the outstanding costs. This coordination of benefits ensures that your healthcare expenses are appropriately covered by the respective insurance providers.

Virginia Auto Insurance Limits Explained

You may want to see also

Explore related products

![]()

Medicare Advantage Plans

When considering Medicare Advantage Plans, individuals should talk to their employer, union, or benefits administrator about any applicable rules. They can also contact their local State Health Insurance Assistance Program (SHIP) for free personalized health insurance counselling.

To learn more about the specific costs associated with a Medicare Advantage Plan, individuals can refer to the official Medicare website for detailed information on plan costs.

Predicting Auto Insurance Loss Ratios: Why It Matters

You may want to see also

Explore related products

$9.97 $19.99

![]()

Medicare with other insurance

Medicare is a public health insurance programme provided by the government. It is available to individuals aged 65 or older, and to younger people with disabilities, end-stage renal disease, or amyotrophic lateral sclerosis (ALS). Medicare is divided into Part A (Hospital Insurance) and Part B (Medical Insurance). Most people get Part A for free, but some have to pay a premium for this coverage. Medicare Part B usually requires a premium to be paid.

Medicare can be combined with other insurance plans, such as private insurance, employer-provided plans, COBRA, or TRICARE. When an individual has both Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage and then sends the remaining balance to the "secondary payer". If the secondary payer does not cover the remaining balance, the individual may be responsible for the remaining costs.

The primary payer is determined by the type of private insurance and the individual's situation. In some cases, Medicare may be the primary payer, while in other cases, it may be the secondary payer. For example, if an individual has comprehensive health coverage through an employer or union when they become eligible for Medicare, their existing plan may be the primary payer, or it may be secondary to Medicare.

It is important to inform Medicare of any other coverage to avoid owing a Part B late-enrollment penalty. Additionally, individuals should inform their doctor or healthcare provider if they have multiple insurers to ensure proper coordination of benefits.

Auto Insurance in Oregon: Understanding the Risks and Penalties

You may want to see also

Frequently asked questions

Medicare Part A is Hospital Insurance. Most people get Part A for free, but some have to pay a premium for this coverage.

Medicare Part B is Medical Insurance. You must keep paying your Part B premium to keep your supplement insurance.

Medicare Supplement Insurance (Medigap) is extra insurance you can buy from a private company that helps pay your share of costs in Original Medicare.

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage, then sends the rest of the balance to the "secondary payer".