The number of miles driven annually impacts car insurance rates. The more you drive, the higher your insurance rate is likely to be. This is because the more miles you drive, the higher your risk of an accident and the more likely you are to file a claim. Insurance companies typically ask for an estimate of your annual mileage when you apply for insurance, and some offer discounts for low-mileage drivers.

| Characteristics | Values |

|---|---|

| Mileage impact on insurance rates | Yes, higher mileage raises accident risks and car insurance rates, while lower mileage reduces costs. |

| Average annual mileage | 13,476 miles per year, according to the Federal Highway Administration (FHA) |

| High mileage threshold | Driving 15,000 miles or more every year is generally considered high mileage. Most companies use 15,000 to 20,000 miles per year as a benchmark for high mileage. |

| Low mileage discounts | Insurers may offer lower rates for low-mileage drivers, especially those driving under 7,000 miles annually. |

| Mileage tracking methods | Insurance companies may use onboard devices, odometer readings, smartphone apps, or third-party estimates to track mileage. |

| Mileage-based insurance plans | Pay-per-mile, usage-based, or telematics insurance plans offer lower rates for low-mileage drivers by adjusting premiums based on miles driven. |

| Risk profile | Lower mileage may result in a lower risk profile, reducing the likelihood of accidents and mechanical failures. |

| State and insurer variation | Mileage impact on rates varies by state and insurer; in California, mileage is a top factor, while in other states, it may be less significant. |

| Other factors | Age, gender, driving record, vehicle type, coverage amount, deductible, and location also affect insurance rates. |

| Mileage estimation methods | Annual mileage can be estimated by tracking mileage during an average month and multiplying by 12, or by dividing total miles by car ownership months and multiplying by 12. |

| Overestimating mileage | Exceeding annual mileage estimates may affect rates and lead to higher premiums at renewal, depending on the insurer and extent of overage. |

| Underestimating mileage | Consistently underreporting mileage may result in higher premiums at renewal. |

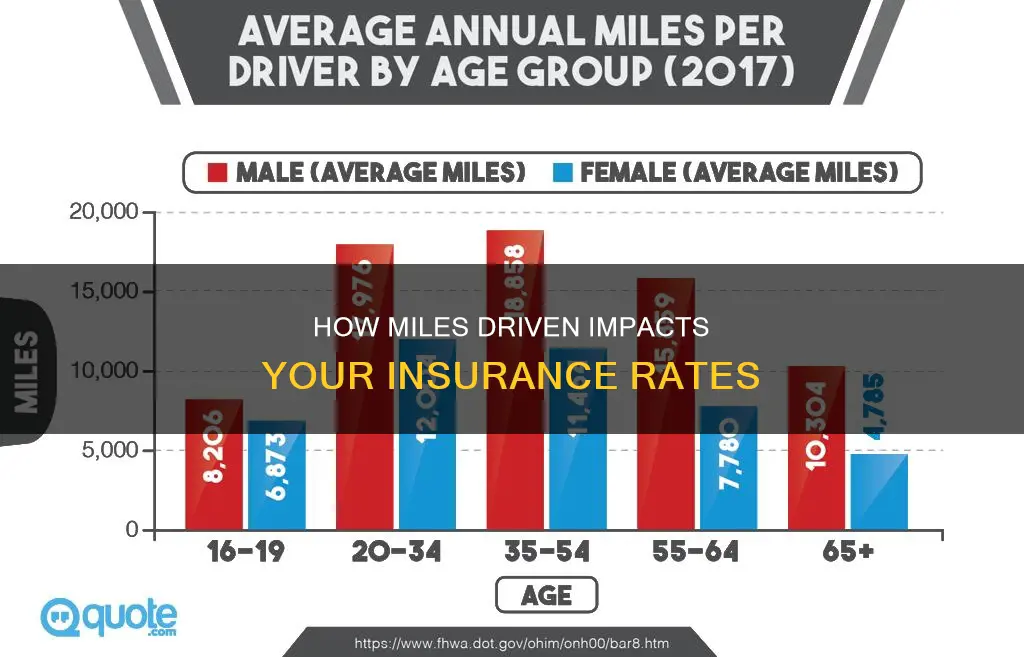

| Average miles by age | Data from DOT shows that Americans between 35 and 54 years old drive the highest average miles per year. |

| Average miles by gender | On average, men drive 6,408 more miles per year than women, according to data. |

Explore related products

What You'll Learn

![]()

Low-mileage drivers may be eligible for discounts

While mileage is one of the factors that affect car insurance rates, low-mileage drivers may be eligible for discounted rates. This is because the fewer miles you drive, the less likely you are to be involved in an accident, and the lower your risk profile.

Insurance companies typically request your odometer reading or an estimate of your annual mileage when you apply for insurance. To see if you qualify for low-mileage discounts, they'll track your mileage either via an onboard device or by getting an odometer reading from you or a third party.

There are several ways to calculate your annual mileage. You can track your mileage during an average month and multiply that by 12. You can also divide the number of miles you've put on your car since you bought it by the number of months you've owned your car to get an average monthly mileage, which you can then multiply by 12. You can also set your car's odometer to zero and take note of the number of miles your car travels over the next week. To get the current annual average mileage, multiply the obtained odometer value by 52.

If you drive less than 26 miles per week, you may be eligible for "pay per mile" insurance, where you pay for each mile you drive. Low-mileage discounts vary, with some auto insurance providers offering as much as 20% for a low-mileage discount. However, on average, drivers get 5% or less.

Some companies that offer low-mileage discounts include USAA (for military members and their families), State Farm, and Progressive.

Launching a Commercial Auto Insurance Brokerage: Steps to Success

You may want to see also

Explore related products

![]()

Mileage is one of many factors that affect insurance rates

Insurance companies typically request your odometer reading or an estimate of your annual mileage when you apply for insurance. They use this information to calculate your premium and determine your risk profile. The average American drives 13,476 miles per year, according to the Federal Highway Administration (FHA). However, each insurance company has its own criteria for how many miles are considered low mileage and how mileage affects insurance rates.

If you drive infrequently, you may be eligible for low-mileage car insurance, which can be offered as a standalone policy or a program through standard auto insurance providers. Low-mileage insurance typically tracks your miles driven using a telematics device installed in your vehicle or through a smartphone app, and your premium is based on the number of miles you drive each month. Some companies offer discounts for low-mileage drivers, especially those who drive under 7,000 or 5,000 miles annually.

In addition to mileage, other factors that affect insurance rates include your age, gender, driving record, the type and model of your vehicle, your coverage amount, deductible, and where you live. It's important to note that annual mileage is not always a major consideration in setting insurance rates, and other factors may have a more significant impact on your premium.

Auto Owners Commercial Auto Policy: Understanding Trailer Coverage and ACV

You may want to see also

Explore related products

![]()

Mileage-based insurance policies are available

With pay-per-mile insurance, you usually pay a flat monthly rate and a small per-mile fee. This type of insurance is often less expensive than traditional insurance. Major companies offering pay-per-mile insurance include:

- Progressive

- State Farm

- Allstate

- MetroMile

- Esurance

- Root Insurance

- Nationwide

In addition to these companies, many other standard insurance providers offer mileage-based savings programs. For example, Progressive offers the Snapshot program, which tracks your driving via a mobile app or a plug-in device and monitors how, when, and how much you drive. State Farm offers the Drive Safe and Save with OnStar program, which tracks your mileage and provides discounts based on annual mileage.

When applying for insurance, insurance companies will typically request your odometer reading or an estimate of your annual mileage. They may offer lower rates for low-mileage drivers, especially those who drive under 7,000 or 5,000 miles annually. Driving fewer miles can reduce your risk profile, making you less likely to be involved in an accident and reducing wear and tear on your vehicle. However, it's important to note that annual mileage is just one of many factors that affect insurance rates, including driving behaviour, the type and model of vehicle, coverage, deductible, age, gender, driving record, and location.

Waivable Tickets: Insurance Impact and What You Need to Know

You may want to see also

Explore related products

![]()

Higher mileage increases accident risk and insurance rates

Driving more increases the likelihood of accidents, raising car insurance rates. This is because the number of miles you drive predicts the risk of you filing a claim. For example, a Verisk analysis found that vehicles driven less than 3,000 miles annually are involved in 40% fewer claims. On the other hand, cars driven 20,000 miles or more annually record 31% more claims.

Insurers often ask how many miles you drive. The more miles you drive, the higher your rate could be. Driving fewer miles also reduces wear and tear on your vehicle, which can lead to fewer mechanical failure-related claims.

Most auto insurers consider your annual mileage when calculating your premium. However, annual mileage isn't necessarily a major consideration in setting insurance rates. In fact, policyholders driving 30,000 miles per year paid just 1% to 3% more on average than those driving 10,000 miles per year, according to insurance industry site The Zebra.

Some insurers offer pay-per-mile policies, which are ideal for drivers with low annual mileage. Providing accurate mileage helps avoid denied claims or overpaying for coverage. Exceeding the annual mileage listed on your car insurance policy can affect your rates, depending on your insurer and how much you exceed the estimate.

If you drive infrequently, you may be a good candidate for low-mileage car insurance. This type of insurance tracks miles driven using a telematics device installed in your vehicle or through a smartphone app. Also known as pay-per-mile insurance, these insurance policies are available as either a standalone policy or a program you can enroll in through many standard auto insurance providers. With pay-per-mileage car insurance, your premium is based on the number of miles you drive each month. Usually, you pay a flat monthly rate and a small per-mile fee.

Insurance Without Car Registration?

You may want to see also

Explore related products

![]()

Mileage affects insurance rates differently in different states

In California, for example, insurers can weigh mileage as one of the top three factors determining insurance premiums, along with driving record and the number of years behind the wheel. California law also requires carriers to collect annual mileage readings from drivers every three years. Drivers must submit a mileage estimation form for the upcoming year and may be asked for supporting documentation if the estimate is unusually low. If the form is not returned before the policy is renewed, insurance companies may update the annual mileage to the state average, resulting in a policy increase.

The definition of "low mileage" also varies by state laws and insurance company guidelines. While most insurance companies consider under 12,000 miles per year to be lower than average, some insurers require less than 10,000 miles to qualify for low-mileage discounts. These discounts can be significant, with some companies offering larger discounts for those who drive fewer than 7,000 or even 5,000 miles per year.

The impact of mileage on insurance rates also depends on the type of insurance plan. Traditional insurance plans typically have a flat monthly rate and a small per-mile fee. In contrast, usage-based insurance (UBI) programs focus on driving habits rather than mileage alone, tracking factors such as speeding or hard braking, which can affect your score and rates. Pay-per-mile insurance is another option, where your premium is based on the number of miles driven each month. This type of insurance is not available in every state, but it is often less expensive than traditional insurance for low-mileage drivers.

Overall, while mileage does impact insurance rates, the extent of its influence varies across different states in the US due to varying state laws, regulations, and insurance company guidelines.

Auto Insurance: Non-Collision Repairs Covered?

You may want to see also

Frequently asked questions

Yes, higher mileage raises accident risks and car insurance rates. Driving more increases the likelihood of accidents, which raises car insurance rates.

Insurance companies typically request your odometer reading or an estimate of your annual mileage when you apply for insurance. They may track your mileage via an onboard device or by getting an odometer reading from you or a third party.

Driving fewer miles may qualify you for discounts or pay-per-mile policies. You can also consider telematics or usage-based insurance, where premiums are based on miles driven.

![Dome Auto Mileage Log, Undated, 32 Forms [Set of 3]](https://m.media-amazon.com/images/I/91tXadNGiVL._AC_UL320_.jpg)