The death of a homeowner can be a challenging time for their loved ones, who may be left wondering what will happen to their mortgage. Mortgage protection insurance (MPI) is a type of insurance policy designed to cover outstanding mortgage payments in the event of the borrower's death. MPI policies are typically offered by lenders or their partner companies during the mortgage application process and are not required when buying a home. While MPI can provide peace of mind and financial security for loved ones, it is important to understand its differences from traditional life insurance policies and the specific regulations and laws that come into play when dealing with mortgages after the death of a homeowner.

| Characteristics | Values |

|---|---|

| Who is it for? | Homeowners with limited savings or who may not qualify for traditional life insurance due to health issues |

| What does it cover? | Pays off the mortgage balance directly to the lender if the policyholder dies or becomes unable to work |

| Who does it protect? | The policyholder's family, by ensuring they can continue living in their home |

| What are the different types of mortgage insurance? | Mortgage protection insurance (MPI), private mortgage insurance (PMI), mortgage disability insurance, level term insurance, decreasing term insurance |

| How does it differ from life insurance? | Life insurance pays out to the policyholder's family, whereas mortgage protection insurance pays out to the lender |

| What are the pros? | Easy approval with minimal or no medical exams, accessible for a wider range of people, provides financial stability for loved ones |

| What are the cons? | More expensive for healthy homeowners, less valuable over time, limited flexibility |

Explore related products

What You'll Learn

![]()

Mortgage protection insurance (MPI) vs. private mortgage insurance (PMI)

When taking out a mortgage, you may come across several acronyms: PMI, MPI, and MIP. While these acronyms sound similar, they have distinct meanings and purposes. Here is a detailed comparison of Mortgage Protection Insurance (MPI) and Private Mortgage Insurance (PMI):

Mortgage Protection Insurance (MPI)

MPI is a type of insurance that protects the borrower. It typically covers mortgage payments for a specified period if the borrower loses their job, becomes disabled, or faces other circumstances that make it challenging to keep up with payments. MPI can also pay off the remaining mortgage balance when the borrower dies, ensuring that the family retains ownership of the home. MPI is generally voluntary and is suitable for borrowers who may have higher risk factors, such as health issues or an unstable job situation. The cost of MPI can vary depending on factors like age, health, occupation, and lifestyle.

Private Mortgage Insurance (PMI)

PMI, on the other hand, protects the lender in case of the borrower's default or failure to make loan payments. It is typically required by lenders when the borrower's down payment is less than 20%. In such cases, the borrower has to pay an additional amount each month to cover the PMI premium on top of the regular mortgage payments. PMI is generally associated with conventional loans that are not backed by a government program. It is important to note that PMI does not cover the borrower's payments in case of job loss, disability, or death; instead, it safeguards the lender's interests.

In summary, the key difference between MPI and PMI is who they protect. MPI is designed to protect the borrower by ensuring mortgage payments are covered in case of financial hardship or paying off the mortgage upon the borrower's death. On the other hand, PMI protects the lender by reducing their risk of loss if the borrower defaults on the loan. While PMI is typically required for loans with a low down payment, MPI is voluntary and depends on the borrower's risk factors and financial situation.

Finding Mortgage Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

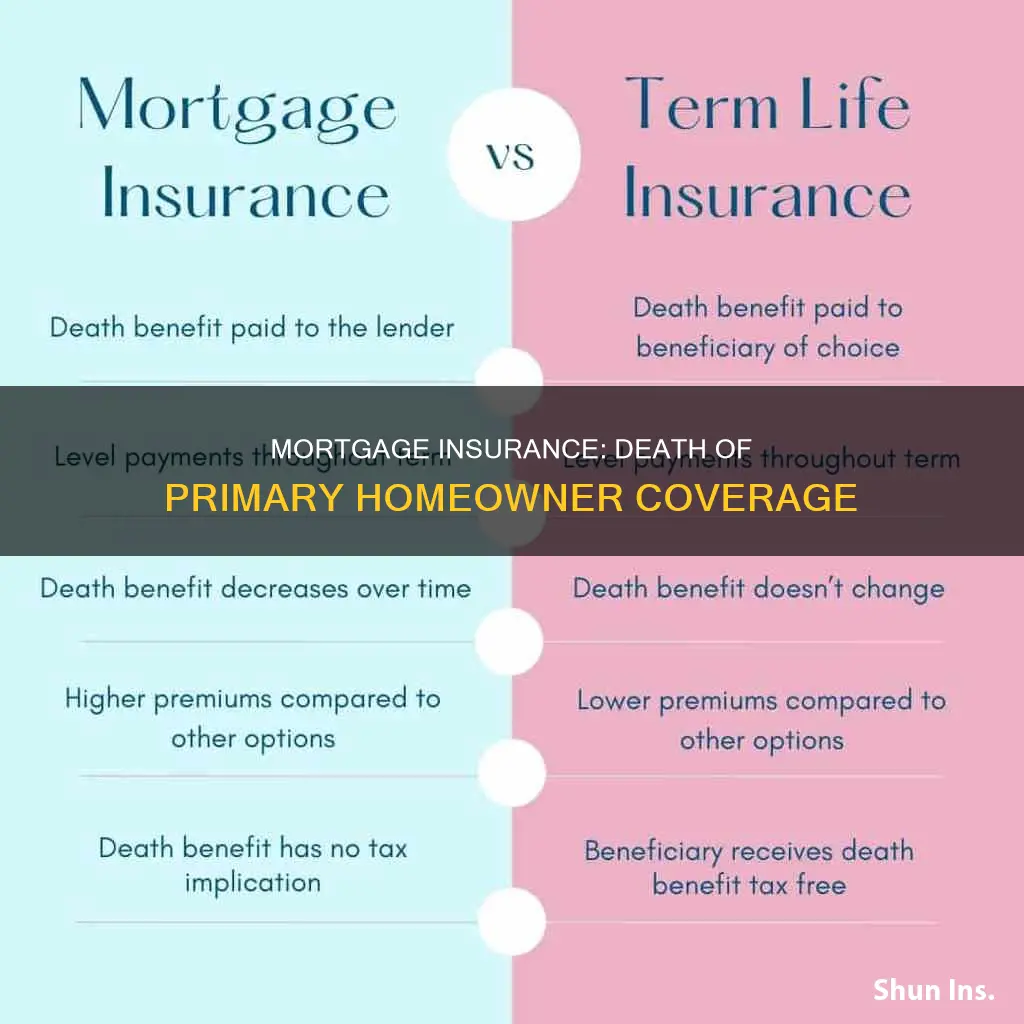

Mortgage life insurance: death benefit paid to lender

Mortgage life insurance is a type of insurance policy that pays off your mortgage debt if you die or, in some cases, become gravely ill or disabled. It is typically offered by the mortgage lender or one of their partner companies during the mortgage application process. Unlike traditional life insurance, the beneficiary of mortgage life insurance is the mortgage lender, not the policyholder's spouse or family.

Mortgage life insurance policies have a specified coverage period, usually matching the term of the mortgage, which can be 10 to 30 years. The death benefit is structured to correspond with the outstanding mortgage balance, and it is paid directly to the lender. This means that the payout decreases over time as the mortgage is paid off. The premium, however, remains the same, resulting in shrinking coverage. If the coverage amount exceeds the outstanding mortgage balance at the time of death, the policyholder's family will not receive any additional funds.

Mortgage life insurance is often chosen by individuals with pre-existing medical conditions who may be unable to obtain traditional term life insurance. Since mortgage life insurance typically does not require a medical examination, it is a more accessible option for those with health issues. However, it may be more expensive for healthy homeowners as the policies assume a higher risk.

It is important to note that mortgage life insurance solely covers mortgage debt and does not provide flexibility in how the death benefit is spent. Therefore, if the policyholder's beneficiaries need to cover other expenses, this type of insurance may not be suitable. Additionally, some mortgage life insurance policies only pay out if the policyholder dies from an accident, excluding natural causes. Thus, it is recommended to carefully consider the terms and limitations of the policy before purchasing mortgage life insurance.

Income Limit for Mortgage Insurance: Who Qualifies?

You may want to see also

Explore related products

![]()

Life insurance: death benefit paid to beneficiaries

Mortgage life insurance is designed to repay mortgage debts and associated costs in the event of the borrower's death. The beneficiary of the policy is the mortgage lender, not the family of the deceased. This type of insurance is ideal for those with pre-existing medical conditions that would otherwise prevent them from obtaining traditional life insurance.

Life insurance, on the other hand, pays out a death benefit to the policyholder's designated beneficiaries. This money can be used to pay off the mortgage, but it is not limited to this purpose. The beneficiary of a life insurance policy can be a family member, a charity, or another organisation chosen by the policyholder.

There are several types of life insurance policies, including whole life and universal life insurance, which may build cash value over time. This means that the beneficiary may receive more than the face value of the death benefit. Some policies also offer an accelerated death benefit, allowing policyholders with a terminal illness to access part of the death benefit while they are still alive to help pay for their care.

The death benefit of a life insurance policy is typically paid out as a lump sum, but it can also be structured as a series of payments. The amount of the benefit is determined by the size of the policy, which is chosen by the policyholder based on how much they want to leave to their loved ones and how much they can afford to spend on premiums.

It is important to note that the beneficiary of a life insurance policy can be designated as either revocable or irrevocable. A revocable beneficiary can be easily changed, but an irrevocable beneficiary must consent to any changes to their designation or their share of the benefit.

Homeowner's Insurance: Easement Disputes and Your Coverage

You may want to see also

Explore related products

![]()

Level term insurance: fixed death benefit

Mortgage life insurance is designed to repay mortgage debts and associated costs in the event of the borrower's death. The beneficiary of the policy is typically the mortgage lender. While it is not required when buying a home, mortgage life insurance helps ensure there will be enough coverage to pay off your mortgage, so your family will not have to move if you pass away.

Level term insurance is a type of life insurance policy where the premium and death benefit remain the same for the duration of the coverage. The death benefit payout remains the same regardless of when the insured dies. Level term insurance is suitable for borrowers with interest-only mortgages who want to ensure the full mortgage amount is covered in the event of their death. The length of coverage may depend on your age, career stage, and dependents.

Level term insurance offers fixed rates and protection for a set period. The premium never changes, and beneficiaries receive a death benefit payout if the insured dies during the coverage period. Level term policies do not build cash value over time, making them a more affordable option. They are straightforward and simple to understand.

Level death benefits are available with both term life insurance and permanent life insurance policies. They offer predictable payouts and premiums but are subject to inflation, reducing their real value over time. Level death benefits allow insurers to forecast their future financial liability accurately.

In summary, level term insurance with a fixed death benefit provides financial protection for beneficiaries by offering a guaranteed payout if the insured dies during the coverage period. It is suitable for borrowers with interest-only mortgages who want to ensure their mortgage debt is covered. Level term insurance offers fixed rates and protection for a specified duration, making it a straightforward and affordable option for individuals seeking life insurance.

Home Insurance: Rain Flood Coverage Explained

You may want to see also

Explore related products

![]()

Estate planning: last will and testament

Estate planning is a crucial aspect of financial management, and creating a Last Will and Testament is an essential step in this process. A Last Will and Testament, commonly known as a Will, is a legal document that outlines your wishes for your property and affairs after your death. It allows you to explicitly state how you want your assets to be distributed and helps protect your family's financial well-being.

A Will gives you control over how your assets are distributed after your death. Without a Will, your assets will be distributed according to state laws, and your loved ones may not receive what you intended. A Will also allows you to appoint an executor, who is responsible for ensuring your wishes are carried out and your estate is settled. Additionally, if you have minor children or dependents, a Will enables you to name legal guardians and set up financial support for them.

Types of Wills

There are several types of Wills to consider, depending on your specific needs and the complexity of your estate:

- Simple Will: Allows you to state your basic wishes and appoint an executor.

- Testamentary Trust: Distributes assets after your death and is often used when beneficiaries require extended care, such as minors or dependents with special needs.

- Joint Will: Useful when you want your spouse to be the initial beneficiary, with the final beneficiaries being your children after both you and your spouse pass away.

Creating Your Will

When creating your Will, start by making a comprehensive list of your assets, including real estate, cash, vehicles, jewellery, and other valuables. Identify any assets that have a co-owner, beneficiary, or trust, as these will be treated differently. Also, make a list of your debts and liabilities, such as mortgages and loans, which will need to be paid off from your estate. Finally, consider your personal and family circumstances and decide who you want to inherit your assets, including your spouse, children, relatives, or charities.

In conclusion, a Last Will and Testament is a vital tool for estate planning. It ensures that your wishes are carried out, provides peace of mind, and helps protect your loved ones' financial future. By understanding the importance of creating a Will and the various options available, you can take control of your legacy and make informed decisions about your estate.

Roof Repairs: What Home Insurance Covers

You may want to see also

Frequently asked questions

Mortgage protection insurance (MPI) is a type of insurance policy that helps your family make your monthly mortgage payments if you – the policyholder and mortgage borrower – die before your mortgage is fully paid off.

Most MPI policies work the same way as traditional life insurance policies. Every month, you pay the insurer a monthly premium. This premium keeps your coverage current and ensures your protection. If you die during the term of the policy, your policy provider pays out a death benefit that covers a set number of mortgage payments.

Private mortgage insurance (PMI) is a type of protection that safeguards the owners of your home loan if you stop paying your mortgage. If you can’t pay your mortgage and you have PMI, your home will likely go into foreclosure. You’re typically required to pay for PMI if you take out a conventional loan with a down payment of less than 20%.