Obamacare, officially known as the Affordable Care Act (ACA), has expanded access to health insurance for individuals under 65. Eligibility is based on factors such as income, citizenship, and legal status. Generally, individuals who are not eligible for other public coverage options like Medicaid or Medicare may qualify for Obamacare. While Obamacare has had little direct impact on Medicare Supplement plans, it does require insurers and employers to offer health insurance that provides certain minimum essential coverages. Medicare Supplement Insurance, also known as Medigap, is extra insurance one can buy from a private health insurance company to help pay for out-of-pocket costs in Original Medicare (Part A and Part B).

| Characteristics | Values |

|---|---|

| Official Name | Affordable Care Act (ACA) |

| Common Name | Obamacare |

| Purpose | Provide coverage to the uninsured population |

| Eligibility | Income, citizenship, legal status |

| Age Limit | Under 65 |

| Medicare Beneficiary | May be eligible for Medicare Supplement Insurance (Medigap) |

| Medicare and Obamacare | Individuals may have both |

| Medicare Enrollment | Sign up during the initial enrollment period |

| Medicare Late Enrollment | Penalties may apply |

| Medicare and Marketplace | Marketplace coverage doesn't lower Medicare out-of-pocket costs |

| Medicare Supplement Insurance | Available from private insurance companies |

| Medicare Advantage Plan | May offer extra benefits like vision, hearing, dental |

Explore related products

What You'll Learn

![]()

Obamacare and Medicare eligibility

Obamacare, officially known as the Affordable Care Act (ACA), has expanded access to health insurance for individuals under 65. Eligibility for Obamacare is based on factors such as income, citizenship, and legal status. Generally, individuals who are not eligible for other public coverage options like Medicaid or Medicare may qualify for Obamacare. It also provides subsidies and tax credits to help lower-income individuals and families afford coverage.

Medicare is a federal health insurance program primarily for individuals aged 65 and older, as well as certain individuals with disabilities or end-stage renal disease. Eligibility for Medicare is based on age, disability status, or having end-stage renal disease. Most individuals become eligible for Medicare at age 65, regardless of income or health status.

It is possible to have both Obamacare and Medicare coverage. Individuals who are eligible for both programs are called "dual eligibles". In this case, Medicare is the primary payer for healthcare services, and Obamacare may provide additional coverage and benefits to fill gaps in Medicare coverage, such as prescription drugs or additional preventive services.

If you have Medicare, it is important to know that Marketplace coverage does not end automatically. You must update your Marketplace application to end Marketplace coverage when starting Medicare. If you want coverage that helps pay your out-of-pocket costs in Medicare Part A and Part B, you can buy a Medigap policy. You can also add Medicare drug coverage (Part D) or join a Medicare Advantage Plan to get some extra benefits, like vision, hearing, and dental.

Unusual Career Pairing: Medical Examiner and Insurance Agent

You may want to see also

Explore related products

![]()

Obamacare's impact on Medicare Supplement Insurance

Obamacare, or the Affordable Care Act (ACA), has had a significant impact on the healthcare landscape in the United States. It has expanded access to health insurance for individuals under 65, with eligibility based on factors like income, citizenship, and legal status. While Obamacare primarily focuses on this demographic, it has also brought about changes to Medicare and Medicare Advantage (MA) plans.

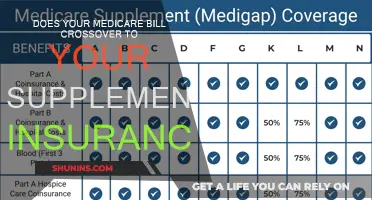

Medicare is a federal health insurance program that primarily covers individuals aged 65 and older, as well as certain younger individuals with disabilities. It offers essential healthcare coverage, ensuring access to necessary medical services as beneficiaries age, and provides financial assistance for those who qualify. However, there are limitations and gaps in Medicare coverage, which is where Medicare Supplement Insurance, or Medigap, comes into play.

Medigap is extra insurance purchased from a private health insurance company to help cover out-of-pocket costs in Original Medicare (Part A and Part B). It fills in the gaps in Medicare coverage, including deductibles, coinsurance, and copayments. Medigap policies are designed to work in conjunction with Original Medicare, and individuals must have Original Medicare to qualify for Medigap.

Obamacare has had little direct impact on Medigap plans. By nature, Medigap plans do not provide minimum essential coverage as defined under Obamacare. However, since Medigap plans are always paired with Original Medicare, which does provide minimum essential coverage, beneficiaries do not have to worry about paying a penalty for insufficient insurance coverage. Additionally, Obamacare's rule prohibiting health insurance companies from denying coverage to individuals with pre-existing conditions does not apply to Medigap plans. Nevertheless, Medicare beneficiaries have some protections related to guaranteed-issue rights when enrolling in Medigap plans.

In summary, while Obamacare has brought about notable changes to healthcare in the United States, its direct impact on Medicare Supplement Insurance (Medigap) is limited. Medigap plans continue to serve as supplemental coverage to Original Medicare, filling in the gaps in Medicare benefits, and beneficiaries of both programs do not face penalties for insufficient coverage.

Pain Medication Refill: No Insurance, Now What?

You may want to see also

Explore related products

![]()

Medicare Supplement Insurance and pre-existing conditions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare (Part A and Part B). Medigap policies can be useful for filling gaps in coverage and reducing out-of-pocket expenses.

When it comes to pre-existing conditions, there are a few things to keep in mind. Firstly, according to the Centers for Medicare and Medicaid Services, a pre-existing condition is an illness or injury that you had before joining the health plan. Examples include cancer, heart disease, diabetes, and asthma. Insurers typically use medical underwriting to consider an individual's health history, including pre-existing conditions, when determining acceptance into a plan and premiums.

During the Medicare Supplement Open Enrollment Period, which lasts for six months for individuals aged 65 or older and enrolled in Medicare Part B, insurance companies cannot refuse to sell a policy or charge higher premiums based on pre-existing conditions. This is because, during this period, medical underwriting cannot be used when considering applications. However, after the Open Enrollment Period ends, medical underwriting may come into play, and individuals may be subject to a "pre-existing condition waiting period."

This waiting period means that individuals may have to pay out-of-pocket costs for their pre-existing condition for up to six months before the Medicare Supplement insurance plan covers those costs. It is important to note that this waiting period can be avoided or shortened if the individual had at least six months of creditable coverage before applying for the Medicare Supplement insurance plan. Creditable coverage could include individual health insurance, group health insurance, or military retiree benefits.

While Medigap can provide added financial protection, it may be challenging for Medicare beneficiaries with pre-existing conditions to obtain. Outside of specific circumstances, Medicare Advantage enrollees who switch to traditional Medicare may be denied a Medigap policy due to pre-existing conditions. Additionally, federal law allows Medigap insurers to use medical underwriting to deny policies or charge higher premiums outside of guaranteed issue periods.

Insurance Coverage for Passengers in Car Accidents

You may want to see also

Explore related products

![]()

Obamacare and Medicare Advantage Plans

Obamacare, or the Affordable Care Act (ACA), expanded access to health insurance for individuals under 65. Eligibility for Obamacare is based on factors such as income, citizenship, and legal status. Generally, individuals who are not eligible for other public coverage options like Medicaid or Medicare may qualify for Obamacare. It also provides subsidies and tax credits to help lower-income individuals and families afford coverage.

Medicare is a federal health insurance program in the United States that primarily provides coverage for individuals aged 65 and older, as well as certain younger individuals with disabilities. It offers different options to suit individuals' needs and provides financial assistance for those who qualify. While Medicare covers a wide range of services, there are certain limitations and gaps in coverage that may require individuals to consider additional private insurance options, such as Medicare Advantage Plans.

Medicare Advantage Plans, also known as private Medicare plans, are offered by private insurance companies and must provide the same coverage as Medicare Part A and Part B but have different deductibles and copayments. These "bundled" plans often include additional benefits such as vision, hearing, and dental coverage.

Obamacare has had little direct impact on Medicare Advantage Plans. However, it has brought about significant changes to the healthcare landscape, including expanding access to coverage, protecting individuals with pre-existing conditions, and providing essential health benefits.

It is possible to have both Obamacare and Medicare Advantage Plan coverage. Individuals who are eligible for both programs are called "dual eligibles." In this case, Medicare is the primary payer for healthcare services, and the Obamacare plan may help cover any out-of-pocket expenses not covered by Medicare.

Understanding Tax Deductions for Medical Payments and Insurance

You may want to see also

Explore related products

![]()

Obamacare and Medicare costs

The Affordable Care Act (ACA), also known as Obamacare, has had a significant impact on the healthcare landscape in the United States. It has expanded access to health insurance for individuals under 65, lowered costs, and provided financial assistance to those who need it.

ACA has reduced the number of uninsured people in the country. As of 2024, 21.4 million people have selected an ACA marketplace plan, and 40 states and the District of Columbia have expanded Medicaid. The number of uninsured people dropped from 45.2 million in 2013 to 26.4 million in 2022.

ACA marketplace plans and Medicaid provide lower-cost coverage to millions. Temporary enhancements to premium tax credits (PTCs) have reduced ACA marketplace enrollee premiums by an average of $800 per year. For 2024, 4 out of 5 enrollees were able to find a plan for $10 or less per month. People with incomes up to 150% of the poverty level ($21,870 for an individual) are eligible to pay $0 in premiums for the “benchmark” silver-level plan.

However, the enhanced PTCs are set to expire at the end of 2025, which will cause premium costs to increase for marketplace enrollees of all ages and income levels. The average person who buys ACA insurance will be paying 75% more for their premium.

Medicare is a federal health insurance program that primarily provides coverage for individuals aged 65 and older, as well as certain younger individuals with disabilities or end-stage renal disease. It offers different options to suit individuals' needs and provides financial assistance for those who qualify.

Individuals who are eligible for both ACA and Medicare coverage are called "dual eligibles," with Medicare being the primary payer for healthcare services. It's important to note that marketplace coverage doesn't lower Medicare out-of-pocket costs and isn't used in place of Medicare Part B.

To fill the gaps in Medicare coverage and reduce out-of-pocket expenses, individuals can purchase Medicare Supplement Insurance (Medigap) from a private health insurance company. Medigap helps pay the individual's share of out-of-pocket costs in Original Medicare (Part A and Part B).

Boeing Retiree Medical Insurance: What's the Current Status?

You may want to see also

Frequently asked questions

Obamacare, or the Affordable Care Act (ACA), expanded access to health insurance for individuals under 65. Eligibility for Obamacare is based on factors such as income, citizenship, and legal status.

Medicare is a federal health insurance program in the United States that primarily provides coverage for individuals aged 65 and older, as well as certain younger individuals with disabilities.

Obamacare has little, if any, direct impact on Medicare Supplement plans. Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare (Part A and Part B).