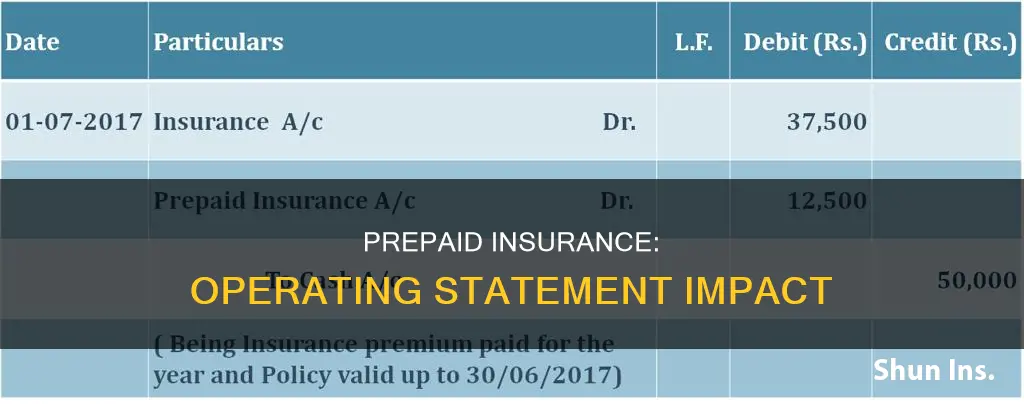

Prepaid insurance is an expense that a company pays in advance for insurance coverage that will take effect in the future. It is considered a prepayment and is recorded as a current asset on the balance sheet. Over the course of the coverage, a portion of the prepaid insurance is expensed on the income statement, reflecting the utilization of insurance coverage in each accounting period. This ensures that expenses match the revenues related to them, following the matching principle in accounting. Prepaid insurance can provide benefits such as financial stability, budgeting precision, and risk mitigation for businesses. However, it is important to note that prepaid expenses are not included in the income statement per generally accepted accounting principles (GAAP) and are only recognized on the income statement when they are incurred.

| Characteristics | Values |

|---|---|

| Definition | Prepaid insurance is a type of prepaid expense, which occurs when a company pays in advance for goods or services it will receive in the future. |

| Examples | Auto insurance, medical insurance, liability insurance |

| Initial recording | Recorded as an asset on the balance sheet. |

| Subsequent recording | Progressively accounted for on the income statement as expenses, reflecting the utilisation of insurance coverage in each accounting period. |

| Benefits | Financial stability, budgeting precision, risk mitigation, reduced administrative burden, protection from premium rises, enhanced creditworthiness |

| Adjustments | At the end of each accounting period, an adjusting entry is made to debit the expired portion of the insurance from the prepaid insurance account to the insurance expense account. |

Explore related products

What You'll Learn

![]()

Prepaid insurance as a current asset

Prepaid insurance is a type of prepaid expense, which occurs when a company pays in advance for goods or services it will receive in the future. Prepaid insurance refers to premiums for insurance that are paid in advance. A premium is a regular, recurring payment made to an insurer for the benefit of having insurance coverage. Insurance companies carry prepaid insurance as current assets on their balance sheets.

When a business pays the premium in advance, the total amount is initially shown as a current asset and is carried as an asset until the coverage is used. As each monthly portion of the prepaid asset is consumed, it is expensed on the income statement, and the balance sheet is adjusted by recording a debit to insurance expense and a credit to prepaid expenses. This ensures that the business is accurately recording the true value of the policy over time and how paying for the policy in advance affects the business's finances from one month to the next.

Prepaid expenses are not included in the income statement per generally accepted accounting principles (GAAP). The GAAP matching principle requires accrual accounting, which stipulates that revenue and expenses must be reported in the period that the spending occurs, not when cash or money exchanges hands. Prepaid expenses are first recorded in the prepaid asset account on the balance sheet. Once expenses are incurred, the prepaid asset account is reduced, and the expense is recorded on the income statement.

Prepaid insurance is usually considered a current asset, as it becomes converted to cash or used within a year. However, if a prepaid expense is not consumed within the year after payment, it becomes a long-term asset, which is not a very common occurrence.

Amica: ATV Insurance Options

You may want to see also

Explore related products

![Careers for Teens Surgeon (Medical) [Special Edition]](https://m.media-amazon.com/images/I/71C5FTcgxAL._AC_UY218_.jpg)

![]()

How prepaid insurance impacts financial statements

Prepaid insurance is a type of prepaid expense, which occurs when a company pays in advance for goods or services it will receive in the future. Prepaid insurance refers to premiums for insurance that are paid in advance. Insurance providers may allow a business to pay multiple monthly premiums in advance, in the form of one lump sum. The payment may represent six or twelve months of premiums.

Prepaid expenses are first recorded on the balance sheet as an asset. They are not included in the income statement per generally accepted accounting principles (GAAP). Instead, as the products and services are received, prepaid expenses are recognised on the income statement for each period when the money is spent. Prepaid expenses are considered assets because they provide future economic benefits to the company.

In the case of prepaid insurance, the full value of the prepaid insurance is recorded as a debit to the asset account and as a credit to the cash account. Each month, as a portion of the prepaid premiums are applied, an adjusting journal entry is made as a credit to the asset account and as a debit to the insurance expense account. In this way, the asset value of the prepaid insurance will be reduced to zero at the end of the prepaid period.

The regular adjustments made to the prepaid insurance account ensure financial statements accurately reflect how much of the prepaid expense remains as an asset and how much has been consumed. Getting these records right is important for investors and auditors, who use them to gauge a company's financial health and compliance with accounting standards.

Churches: Workers Comp Insurance — Mandatory?

You may want to see also

Explore related products

![]()

Prepaid insurance and the matching principle

Prepaid insurance is a common expense that companies incur, where they pay for an insurance policy upfront for a future period. For example, a company might pay $60,000 for a year of liability insurance in advance. This initial payment is recorded as an asset called "prepaid insurance" on the balance sheet.

However, as per the GAAP matching principle, this prepaid expense is not immediately recognised as an expense on the income statement. Instead, each month, a portion of the prepaid insurance is moved from the prepaid account to the expense column, reflecting that month's insurance coverage. These monthly moves are called "adjusting entries", and they ensure that expenses are matched with the revenues they help to generate. In the case of prepaid insurance, the expense is allocated monthly over the course of the year to match the period of benefit.

The matching principle is a cornerstone of accrual accounting, which stipulates that expenses should be reported in the same period as the revenues they are related to. This principle is crucial for creating reliable financial statements and providing a more accurate reflection of a company's financial performance. By aligning expenses with revenues, stakeholders can make better-informed decisions, and business owners can gauge true profitability.

For example, if a company incurs costs for producing goods in December but sells those goods in January, the expenses related to production should be recorded in January's financial statements to match the revenue generated in that month. This ensures that the financial statements accurately reflect the financial results of that period.

In summary, prepaid insurance is initially recorded as an asset on the balance sheet, and then, through adjusting entries, it is gradually recognised as an expense on the income statement to match the period of benefit. This process is in accordance with the GAAP matching principle, which is essential for accurate financial reporting and understanding a company's financial position.

Horsepower and Insurance: A Costly Relationship

You may want to see also

Explore related products

![]()

Adjusting entries for prepaid insurance

Prepaid expenses are payments made for goods and services that a company intends to pay for in advance but will receive in the future. Prepaid insurance is one of the most common types of prepaid expenses, along with prepaid rent. Prepaid expenses are considered assets because they provide future economic benefits to the company. They are recorded on the balance sheet as assets but are not included in the income statement per generally accepted accounting principles (GAAP).

Adjusting entries for prepaid expenses are made at the end of an accounting period to record all revenues and expenses that have been earned or incurred but are not yet recorded. In the case of prepaid insurance, the insurance expense is recognized over the period of the insurance coverage. The adjusting entry will depend on the method used when the initial entry was made. There are two ways of recording prepayments: the asset method and the expense method. Under the asset method, a prepaid expense account (an asset) is recorded when the amount is paid. Under the expense method, the initial entry is a decrease in the insurance expense by the amount that has not yet been incurred.

For example, if a company pays $60,000 for a year of liability insurance upfront, that full amount initially goes on the books as an asset called "prepaid insurance." Then, each month, it moves $5,000 from that prepaid account into the company's expense column, reflecting that month's portion of insurance coverage. These monthly moves are the adjusting entries, ensuring that the financial statements accurately reflect how much of the prepaid expense remains as an asset and how much has been consumed.

Third-Party Insurance: Who Benefits?

You may want to see also

Explore related products

![]()

Benefits of prepaid insurance

Prepaid insurance is a premium payment made upfront by businesses or individuals to insurers for future insurance coverage. It is considered a prepaid expense, which is a payment made in advance for goods or services that will be received in the future. Prepaid insurance offers several benefits to both the insurer and the insured.

One of the main benefits of prepaid insurance is financial stability. By paying premiums in advance, individuals and businesses can lock in rates and manage their cash flow more effectively. Prepaid insurance also aids in budgeting and financial planning. Since the cost of insurance is predetermined, it becomes easier to allocate funds and plan for future expenses. This is especially beneficial for businesses, as it helps them make more accurate financial statements and projections.

Another advantage of prepaid insurance is risk mitigation. By paying for insurance coverage in advance, individuals and businesses can ensure that they are protected against potential risks and uncertainties. This provides peace of mind and helps to safeguard against unforeseen events.

Prepaid insurance also offers flexibility and convenience. Many insurance companies offer discounts or better rates for customers who pay premiums upfront. This can result in significant cost savings over time. Additionally, prepaid insurance helps to streamline financial operations by eliminating the need for monthly premium payments, reducing administrative burdens, and improving overall efficiency.

From an accounting perspective, prepaid insurance is considered a current asset. It is recorded as a prepaid expense on the balance sheet and is gradually charged to expense over the period covered by the insurance contract. This allows businesses to accurately track and manage their expenses, ensuring compliance with accounting regulations and providing a clear picture of their financial health.

Landlords: Insist on Tenant Insurance

You may want to see also

Frequently asked questions

Prepaid insurance is when a company pays for insurance coverage in advance. It is considered a prepayment and is recorded as a current asset on the balance sheet.

Prepaid insurance is initially recorded as an asset on the balance sheet. As the insurance coverage is used, the expired portion is moved from the current asset account to the income statement account as an expense. This is usually done at the end of each accounting period through an adjusting entry.

Prepaid insurance provides financial stability, budgeting precision, and risk mitigation. It allows businesses to manage their cash flows better, reduce administrative burden, and protect against potential liabilities.

Prepaid expenses are payments made in advance for goods or services to be received in the future. Accrued expenses, on the other hand, are costs of goods or services that a company consumes before paying for them. Prepaid expenses are initially recorded as assets, while accrued expenses are recorded as current liabilities.

Prepaid insurance is initially debited to the prepaid insurance account and credited to the cash account. At the end of each period or when the expense is incurred, an adjusting entry is made to debit the insurance expense account and credit the prepaid insurance account, reflecting the portion of the insurance coverage used.