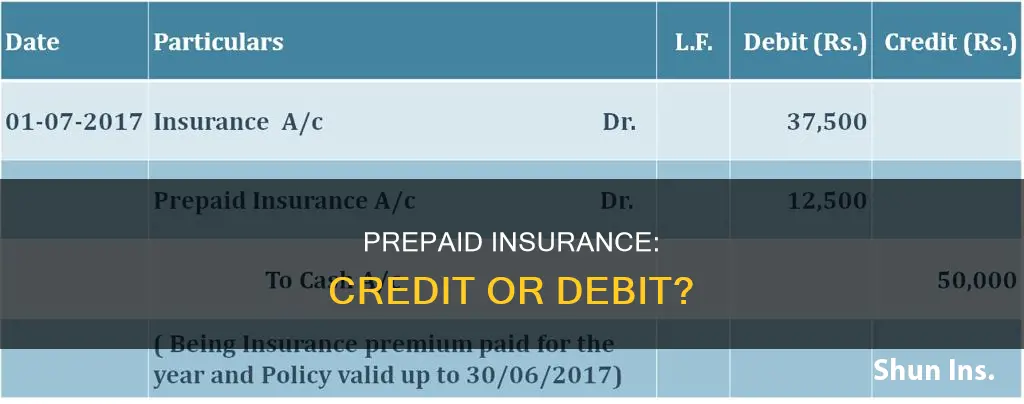

Prepaid insurance is a type of insurance where the policyholder pays the premium for a set period of time upfront, before the coverage begins. It is typically considered a current asset, as it can be converted to cash within a year or less. When a business or individual purchases prepaid insurance, the payment is recorded as a debit to the asset account and a credit to the cash account. Over time, as the insurance is consumed, the asset value decreases, and the entries in the two columns eventually cancel each other out.

| Characteristics | Values |

|---|---|

| Definition | Prepaid insurance is a premium for insurance that is paid in advance. |

| Type of Asset | Prepaid insurance is considered a current asset. |

| Accounting | Prepaid insurance is recorded in the general ledger as a prepaid asset under current assets. |

| Ledger Entry | Prepaid insurance is recorded as a debit to the asset account and as a credit to the cash account. |

| Adjusting Entries | Each month, an adjusting entry is made as a credit to the asset account and as a debit to the insurance expense account. |

| Asset Value | The asset value of prepaid insurance will be reduced to zero at the end of the prepaid period. |

| Expense Value | The expense value will reach the total prepaid amount at the end of the prepaid period. |

Explore related products

What You'll Learn

![]()

Prepaid insurance is a debit on the asset account

Prepaid insurance is a type of insurance in which the premium is paid in advance for a specified period, typically six or twelve months. It is considered a current asset on the balance sheet, reflecting the future economic benefit it provides to the insured party. When a company pays for prepaid insurance, it makes a debit entry to its prepaid insurance asset account, recognising the future value of the insurance coverage.

The full value of the prepaid insurance is initially recorded as a debit to the asset account and a credit to the cash account. This reflects the exchange of one asset (cash) for another (prepaid insurance). As the coverage term progresses, portions of the prepaid insurance are expensed, and the prepaid insurance account is credited to reflect the decrease in the prepaid amount. This process ensures that expenses are matched with the revenue or benefit received in each accounting period.

The adjusting journal entries are made each month, with the current month's expense recorded on the income statement and the unexpired amount of prepaid insurance reduced in the asset account. These entries involve debiting the insurance expense account and crediting the prepaid expense account, effectively swapping one asset for another. By the end of the year, the prepaid insurance balance should be zero, with the full amount charged to the insurance expense account.

Prepaid insurance is considered a debit on the asset account because it is a resource that diminishes over time as it is consumed. The monthly or periodic value of the insurance coverage is recorded as a credit, gradually reducing the value of the prepaid insurance asset. This accounting treatment ensures that the business accurately reflects the true value of the policy over time and matches expenses with revenues.

Affordable Healthcare Act Insurance in North Carolina

You may want to see also

Explore related products

![]()

Prepaid insurance is an advance payment for a future benefit

Prepaid insurance is an advance payment made by a company or individual for insurance coverage over a future period, usually twelve months. It is considered a prepaid expense, which is a type of expenditure paid for before use. Prepaid insurance is typically paid in a lump sum, covering multiple monthly premiums in advance. This type of insurance is often preferred by insurance companies as it generates more working capital and improves customer retention. In exchange, the insurance company may offer the customer a discount on the premium price.

When a company purchases prepaid insurance, it is recorded as a prepaid asset on the balance sheet. This is because it is a resource that will diminish over time. The full value of the prepaid insurance is initially recorded as a debit to the asset account and as a credit to the cash account. As the insurance coverage is consumed each month, the value of the prepaid insurance is reduced, and the corresponding expense account is increased by the same amount. This is done through adjusting journal entries, which are typically made each month or accounting period.

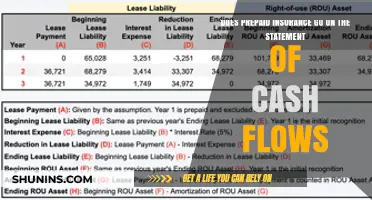

For example, consider a company that pays an annual premium of $2,400 for its liability insurance policy on the first day of each year. The company would record the payment as a debit of $2,400 to prepaid insurance and a credit of $2,400 to cash. Each month, the company would then make an adjusting entry, debiting insurance expense for $200 and crediting prepaid insurance for $200. By the end of the year, the asset account would show a balance of zero for the insurance premium, and the insurance expense account would total $2,400.

Prepaid insurance is important for businesses to correctly record all their transactions and resources to ensure accurate financial statements. By recording prepaid insurance as an asset and adjusting it as the policy is consumed, businesses can accurately track the true value of the policy over time. This helps to prevent misclassification and reconciliation errors and provides a clear picture of the company's financial position.

Next Insurance: Admitted Carrier Status

You may want to see also

Explore related products

![]()

Prepaid insurance is a current asset

Prepaid insurance is usually considered a current asset. It is an expenditure that a business or individual pays for before using it. It is a type of premium, a regular, recurring payment made to an insurance provider for the benefit of having insurance coverage. When a business policyholder pays the premium in advance, the total amount is shown as a current asset and is carried as an asset until the coverage is used.

Prepaid insurance is recorded in the general ledger as a prepaid asset under current assets. It is considered a debit on the asset account because it is a resource that will diminish over time. The full value of the prepaid insurance is recorded as a debit to the asset account and as a credit to the cash account. Each month, as a portion of the prepaid premiums are applied, an adjusting journal entry is made as a credit to the asset account and as a debit to the insurance expense account. In this way, the asset value of the prepaid insurance will be reduced to zero at the end of the prepaid period.

A current asset is a financial resource that can be easily liquidated, or converted to cash, in a year or less. Prepaid insurance is usually considered a current asset as it becomes converted to cash or used within a fairly short time. However, if a prepaid expense is not consumed within the year after payment, it becomes a long-term asset, which is not a very common occurrence.

Prepaid insurance is important because a business should correctly record all of its transactions and resources to have accurate financial statements. Recording prepaid insurance as an asset and adjusting that asset as the policy is consumed on a monthly basis ensures that the business is accurately recording the true value of the policy over time, and in particular, how paying for the policy in advance affects the business’s finances from one month to the next.

People's Trust Insurance: Is It Going Bust?

You may want to see also

Explore related products

![]()

Prepaid insurance is charged to the expense side when coverage comes into effect

Prepaid insurance is a type of insurance in which premiums for insurance are paid in advance. It is considered a prepaid expense, which is an expenditure paid for before it is utilised. Prepaid insurance is usually paid in a lump sum for six or twelve months of premiums. It is considered a current asset as it can be easily converted to cash within a year.

When prepaid insurance is purchased, the full amount is initially recorded as an asset called "prepaid insurance". However, when the insurance coverage comes into effect, it is charged to the expense side of the company's balance sheet. This means that it is moved from an asset to an expense. Each month, as a portion of the prepaid premiums is used, an adjusting journal entry is made, reducing the asset value of the prepaid insurance and increasing the expense. This ensures that the business accurately records the true value of the policy over time.

For example, if a company pays $60,000 for a year of liability insurance upfront, the full amount is initially recorded as an asset. Then, each month, $5,000 is moved from the prepaid account into the company's expense column, reflecting that month's insurance coverage. These monthly moves are called "adjusting entries" and represent the progress of the prepaid service being used.

Prepaid insurance is important for businesses to correctly record all transactions and resources, ensuring accurate financial statements. By recording prepaid insurance as an asset and adjusting it as the policy is consumed, businesses can effectively manage their finances and track their expenses.

How Listing Additional Drivers Impacts Your Insurance Rates

You may want to see also

Explore related products

![]()

Prepaid insurance is recorded in the general ledger

When a company pays for prepaid insurance, it is recorded as a debit to the asset account and as a credit to the cash account. This is because the company has traded one asset (cash) for another (prepaid insurance). As the policy is consumed from month to month, the policy's value for those months will be recorded as a credit, and the entries in the two columns will eventually cancel each other out, resulting in a balance of zero.

For example, if a company pays $60,000 for a year of liability insurance upfront, that full amount is initially recorded as a debit to the asset account and a credit to the cash account. Each month, the company will make an adjusting journal entry, moving $5,000 from the prepaid account (debit) to the expense column (credit). These regular adjustments ensure financial statements accurately reflect how much of the prepaid expense remains as an asset and how much has been consumed.

Prepaid insurance is important because a business should correctly record all of its transactions and resources to have accurate financial statements. Investors and auditors look at how companies handle their prepaid expenses to gauge financial health and compliance with accounting standards.

Gain Insurance Carrier Appointments: Strategies for Success

You may want to see also

Frequently asked questions

Prepaid insurance refers to premiums for insurance that are paid in advance. A premium is a recurring payment made to an insurance provider for coverage.

Prepaid insurance is recorded as a debit to the asset account and a credit to the cash account. As the insurance is used, the value of the prepaid insurance is reduced and the insurance expense account is debited.

Prepaid insurance is considered a debit because it is a resource that will diminish over time. The debit balance indicates the amount that remains prepaid.

Prepaid insurance is the amount paid in advance for insurance coverage. Insurance expense is the amount that has been used or expired.

A company with a monthly insurance premium of $1,000 would record a prepaid insurance asset of $12,000. Each month, an adjusting entry of $1,000 is made, representing the expense for that month. At the end of twelve months, the asset account will show a balance of zero.