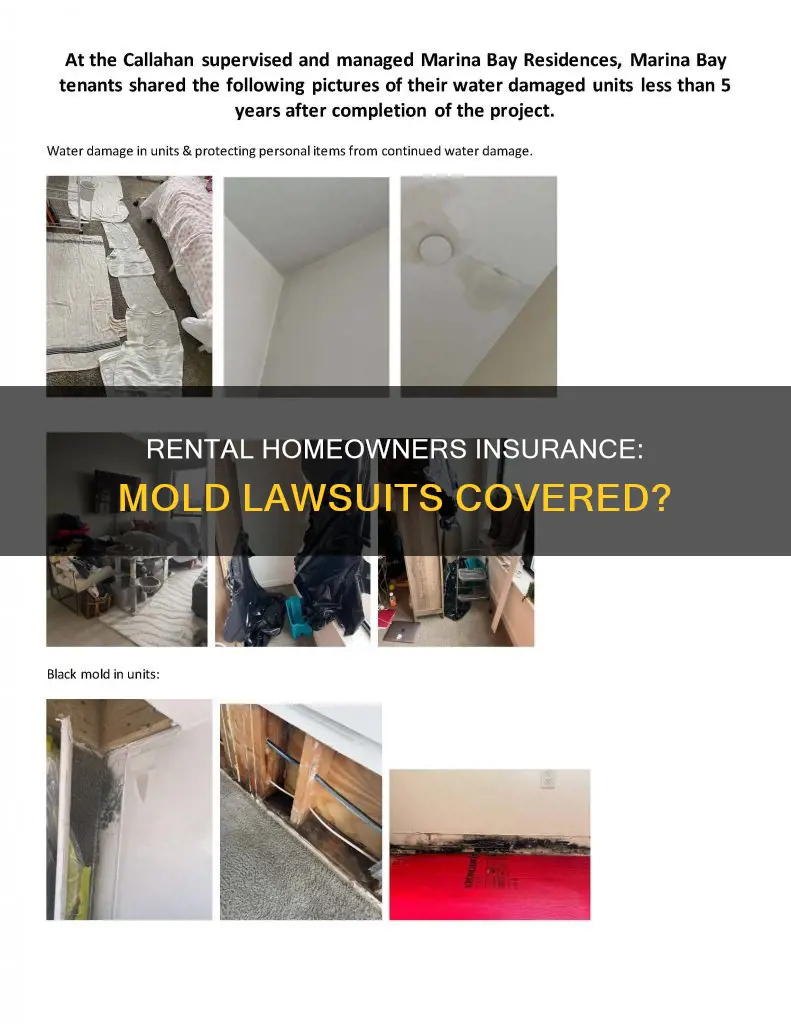

If you're a renter dealing with a mold problem, you might be wondering if your insurance will cover the costs of remediation and damage to your belongings. The answer is, it depends. Most renters' insurance policies will cover mold damage if it's caused by a covered peril, such as a burst pipe or water damage from firefighters putting out a fire. However, if the mold is due to neglect, poor maintenance, or flooding, it is usually not covered. Landlords are generally responsible for keeping rental units safe and habitable, so if they fail to address a serious mold problem, tenants may have legal recourse, such as withholding rent or seeking compensation for health issues related to mold exposure. To ensure you understand your coverage options, it's important to carefully review your insurance policy or consult with a representative from your insurance company.

| Characteristics | Values |

|---|---|

| Rental homeowners insurance cover lawsuit due to mold issues | Rental insurance typically covers mold damage if it is caused by a covered peril, such as a burst pipe or water used by firefighters to combat a fire. It usually does not cover mold damage resulting from neglect, flooding, or lack of maintenance. |

| Homeowners insurance cover lawsuit due to mold issues | Homeowners insurance typically covers mold damage if it occurs due to a sudden and unexpected event, such as a toilet overflow or a leaking pipe. It usually does not cover mold damage resulting from flooding or lack of maintenance. |

| Laws and regulations | Tenants have rights and protections in the case of mold in rental properties. They can refuse to pay rent if the landlord fails to fix a mold issue within a legally specified timeframe. Tenants can also request reimbursement for expenses incurred due to mold remediation. If a tenant experiences health issues due to mold, they may be eligible for compensation through a personal injury claim. |

Explore related products

What You'll Learn

- Renters insurance may cover mold damage if it's a covered peril

- Landlord insurance may cover mold-related expenses if it's a covered peril

- Renters insurance won't cover mold damage if it's due to negligence

- Landlord insurance won't cover mold damage if it's due to negligence

- Renters may refuse rent until landlords fix mold issues

![]()

Renters insurance may cover mold damage if it's a covered peril

Whether renters' insurance covers lawsuits due to mould issues depends on the cause of the mould. If the mould is caused by a covered peril, such as a burst pipe, renters insurance is likely to provide coverage for the damages. However, if the mould is due to neglect or poor maintenance, it is usually not covered.

Renters' insurance policies typically cover mould damage if it is caused by a covered peril. A covered peril is an event that is listed in the insurance policy as being covered. For example, if a pipe bursts and causes mould to form inside the walls, this would typically be covered by renters insurance. On the other hand, if the mould is caused by flooding or a lack of maintenance, it is unlikely to be covered.

It is important to note that renters' insurance policies typically do not cover mould testing or inspection. If mould is present when a tenant moves into a property, the landlord or rental company may be liable for the cost of remediation and damage to belongings. In this case, renters' insurance would not cover the cost of a lawsuit.

The process of filing a claim for mould damage can vary depending on the insurance company. However, it generally involves stopping the leak, reporting the damage to the insurance company, documenting the damaged property, and making temporary repairs. It is also important to review the insurance policy to understand the specific inclusions and exclusions.

If a claim for mould damage is denied by the insurance company, it may be possible to file an appeal. This is typically only successful if the damage is caused by a covered peril and the insurance company has wrongfully denied the claim. If the mould is due to normal wear and tear or flood damage without a flood policy, appealing is unlikely to be successful.

The Cost of Cultivating Protection: Unraveling Farmers Insurance Membership Fees

You may want to see also

Explore related products

![]()

Landlord insurance may cover mold-related expenses if it's a covered peril

Landlord insurance may cover mold-related expenses if the mold is caused by a covered peril. Covered perils typically include sudden or accidental events, such as burst pipes, water leaks, or sewer backups. For example, if a pipe bursts and causes water damage, leading to mold growth, landlord insurance may cover the cost of remediation and repairs. However, it's important to note that landlord insurance policies usually have mold exclusions and may not cover mold if it results from maintenance issues, flooding, or neglect.

To ensure coverage for mold-related issues, landlords can consider purchasing an all-risk policy, which provides broader coverage for perils that may not be specifically listed. Additionally, adding a mold endorsement or add-on to the policy can provide specific protection against mold-related expenses. This is important because mold can cause extensive damage to rental properties and lead to financial losses for landlords.

On the other hand, renters should be aware that their insurance policies typically cover mold damage to personal property if it is caused by a covered peril. Renters insurance may also provide temporary lodging expenses while mold remediation is in progress. However, renters insurance usually does not cover mold inspection or removal costs unless they are specifically included in the policy.

In summary, both landlords and renters should carefully review their insurance policies to understand their coverage for mold-related issues. Landlord insurance may cover mold-related expenses if the mold is caused by a covered peril, such as a sudden plumbing issue or water leak. Renters insurance, on the other hand, typically covers mold damage to personal belongings in such cases.

To prevent mold issues, landlords should maintain their properties and promptly address any leaks or water damage. Tenants should also be vigilant in reporting any potential sources of moisture to their landlords and taking preventive measures to avoid mold growth. By working together, landlords and tenants can minimize the impact of mold and reduce the likelihood of insurance claims.

Homeowners Insurance: Underground Water Leaks Covered?

You may want to see also

Explore related products

![]()

Renters insurance won't cover mold damage if it's due to negligence

Renters' insurance may cover mould damage, but only under certain circumstances. If the mould is caused by a covered peril, such as a burst pipe, your insurance company will likely cover the cost of replacing damaged items and mould remediation. However, if the mould is a result of negligence or neglect, your insurance company will typically not cover the damage.

Negligence in this context refers to instances where the tenant could have prevented the mould. For example, if there was an internal flood in your apartment and you used towels to dry the area, but then left those towels in a corner for weeks, resulting in mould growth, your insurance would not cover any damage to your possessions. In this case, the insurance company would view your failure to remove the towels as the ultimate cause, rather than the flood.

Similarly, mould growth from rain due to not keeping your windows closed is generally not covered by insurance. This is because landlords and tenants share responsibility for preventing mould, and leaving windows open during heavy rain could be considered negligent behaviour.

If mould is caused by a landlord's neglect, they may be liable for the cost of mould remediation and damage to your belongings. For example, if mould is present due to a failure to maintain the property's plumbing, resulting in an ongoing leak, the landlord may be responsible for the cost of removal and any damaged items. However, most leases will state that the landlord is not responsible for damage to your personal property. In this case, your only recourse may be to demand compensation from the landlord, which could require legal action.

It's important to note that renters' insurance policies vary, and the only way to confirm whether your policy covers mould damage is to consult your policy documents or speak with a representative of your insurance company. Additionally, you may be able to add mould coverage to your policy as an endorsement for an additional premium if your current policy does not cover mould.

Mortgage Disability Insurance: Keep or Discard?

You may want to see also

Explore related products

![]()

Landlord insurance won't cover mold damage if it's due to negligence

Landlord insurance typically covers mold damage if it occurs due to a sudden and unexpected event, such as a burst pipe or an overflowing toilet. However, landlord insurance generally won't cover mold damage if it's due to negligence or lack of maintenance. Negligence refers to situations where the tenant or landlord fails to take reasonable care, resulting in mold growth. For example, if a tenant doesn't properly ventilate a bathroom, or a landlord ignores a long-term water leak, it is considered negligence, and landlord insurance won't cover the mold damage.

In the case of tenant negligence, the landlord may be able to deduct the expenses from the tenant's security deposit. Additionally, if the mold is caused by the tenant's negligence, the landlord's insurance company may deny the claim, leaving the landlord responsible for the cost of remediation. It's important for landlords to maintain their properties and address any water issues promptly to prevent mold growth and ensure insurance coverage.

On the other hand, if the mold is a result of landlord negligence, the landlord may be liable for the cost of mold remediation and damage to tenants' belongings. In such cases, tenants can file a claim with their renters insurance, which may cover mold damage if it's caused by a covered peril, such as a burst pipe or a fire. However, renters insurance typically doesn't cover mold inspection or testing, and mold damage caused by flooding or lack of maintenance may not be covered.

To confirm whether mold damage is covered by landlord insurance or renters insurance, it's essential to carefully review the policy documents or consult with a representative of the insurance company. Each insurance company and policy may have different coverage limitations and exclusions regarding mold damage. Additionally, the process of filing a claim for mold damage may vary, but it typically involves stopping the leak, reporting the damage, documenting the affected property, and making temporary repairs to prevent further damage.

Protecting Your Wealth: Choosing High Net Worth Insurance

You may want to see also

Explore related products

$25.99 $33.98

![]()

Renters may refuse rent until landlords fix mold issues

In most cases, renters' insurance will not cover the cost of mold removal, as it does not cover structural damage to the home. However, renters' insurance may cover mold damage if it is caused by a covered peril, such as a burst pipe. Even with an endorsement, coverage is typically limited to mold remediation, such as repairing the affected wall or structure. If the mold is a result of neglect or poor maintenance, it is generally not covered by renters' insurance.

On the other hand, landlords are generally held liable for mold removal and should be covered by landlord insurance to mitigate their risks. Landlords are responsible for maintaining habitable living spaces, and exposed mold is considered a failure to meet these requirements. If a renter can show evidence of mold growth after repeated requests for landlord extermination, the landlord has breached their duty under state law. In such cases, renters have the right to withhold rent until these issues are resolved.

Before withholding rent, renters should provide written notice to their landlord, allowing them at least seven days to respond and address the issue. If the condition has not been fixed within this timeframe, the renter may choose to stop paying rent, provided they give one month's notice. Additionally, renters can seek legal advice and may be able to file a personal injury claim if their health has been negatively impacted by hazardous mold exposure.

To ensure proper handling of mold issues, landlords can take several proactive steps. These include checking if their insurance policy covers mold damage, requiring a mold inspection in the lease, and asking tenants to carry renters' insurance. By following these tips, landlords can reduce their chances of being held accountable for mold-related issues.

Medi-Cal Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

Homeowners insurance typically doesn't cover mold damage due to flooding or lack of home maintenance. However, it may cover mold damage if it occurs due to a sudden and unexpected event, such as a toilet overflow or a leaking pipe.

Renters insurance generally does not cover mold damage unless it is caused by a covered peril, such as a burst pipe or water damage from firefighting. Even with a covered peril, coverage may be limited to mold remediation and may not include personal property damage.

If the mold is caused by the landlord's negligence, such as a failure to fix a leaky pipe or roof, the landlord may be liable for the cost of mold remediation and damage to the tenant's belongings. Tenants may also be eligible for compensation through a personal injury claim if they experience health issues due to mold contamination.

To prevent mold growth, it is important to control moisture levels and keep the property well-ventilated and dry. Leaks should be repaired promptly, and tenants should report any water damage immediately. Regular inspections for signs of water damage, such as peeling paint or discolored walls, can also help identify potential issues.

Homeowners insurance may cover legal expenses and liability claims arising from tenant occupancy, including mold-related issues. However, it depends on the specific policy and whether mold is listed as a covered peril or included as an add-on. Consulting the policy documents or speaking with a representative is necessary to confirm coverage.