The question of whether the United States has national health insurance is a complex and often debated topic. Unlike many other developed nations, the U.S. does not have a universal, government-funded healthcare system that covers all citizens. Instead, healthcare coverage in the U.S. is a mix of private insurance, employer-sponsored plans, and government programs like Medicare and Medicaid, which primarily serve specific populations such as the elderly, disabled, and low-income individuals. This fragmented system leaves millions of Americans uninsured or underinsured, sparking ongoing discussions about the feasibility and desirability of implementing a national health insurance program to ensure comprehensive and equitable access to healthcare.

| Characteristics | Values |

|---|---|

| National Health Insurance System | The U.S. does not have a universal national health insurance system. |

| Primary Healthcare Coverage | Employer-based insurance (59.1% in 2022), Medicaid, Medicare, and private plans. |

| Government-Funded Programs | Medicare (seniors/disabled), Medicaid (low-income), CHIP (children). |

| Uninsured Rate (2022) | 8.0% of the population (approximately 26.4 million people). |

| Affordable Care Act (ACA) | Expanded Medicaid and established health insurance marketplaces (2010). |

| Public vs. Private Mix | Predominantly private insurance with government programs for specific groups. |

| Single-Payer System | No federal single-payer system; proposals like Medicare for All exist but not implemented. |

| Healthcare Spending (2021) | 18.8% of GDP ($4.3 trillion), highest globally. |

| State-Level Variations | States have autonomy in Medicaid expansion and insurance regulations. |

| Recent Trends (2023) | Increased enrollment in Medicaid/ACA plans post-pandemic; debates on healthcare reform persist. |

Explore related products

What You'll Learn

![]()

Medicare and Medicaid Overview

The United States does not have a single, universal national health insurance program, but it does provide public health coverage through two major federal initiatives: Medicare and Medicaid. These programs, while not encompassing all citizens, play a critical role in ensuring healthcare access for specific demographics. Understanding their distinct purposes, eligibility criteria, and coverage options is essential for navigating the complexities of the U.S. healthcare system.

Medicare, established in 1965, primarily serves individuals aged 65 and older, as well as younger people with certain disabilities or end-stage renal disease. It operates as a federal program, funded through payroll taxes, premiums, and general revenue. Medicare is divided into parts, each addressing different healthcare needs: Part A covers hospital stays, Part B includes doctor visits and outpatient services, Part C (Medicare Advantage) offers private insurance plans, and Part D provides prescription drug coverage. Beneficiaries typically pay premiums for Parts B and D, with costs varying based on income. For instance, in 2023, the standard Part B premium is $164.90 per month, while Part D premiums average around $30 to $70 monthly, depending on the plan.

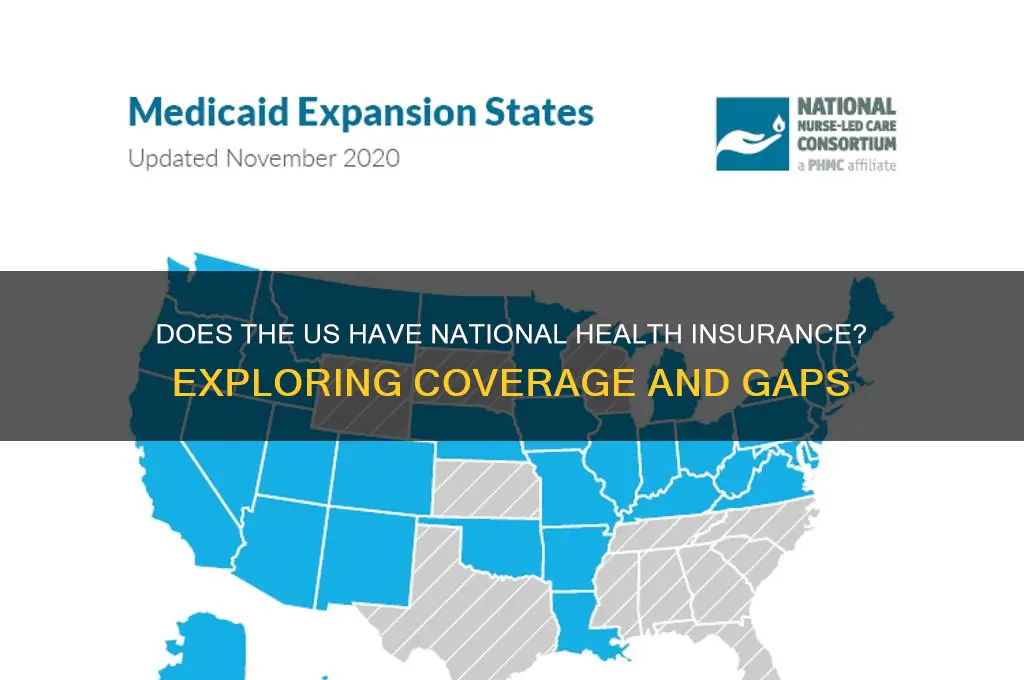

Medicaid, also created in 1965, is a joint federal and state program designed to assist low-income individuals and families, including children, pregnant women, and people with disabilities. Unlike Medicare, Medicaid eligibility and benefits vary by state, as states administer the program within federal guidelines. While the Affordable Care Act (ACA) expanded Medicaid to cover more low-income adults, not all states have adopted this expansion, creating coverage gaps in some regions. Medicaid generally covers a broader range of services than Medicare, including long-term care, which is often excluded from Medicare unless specific conditions are met. For example, Medicaid may cover nursing home care for eligible individuals, whereas Medicare only covers short-term skilled nursing facility stays under certain circumstances.

A key distinction between Medicare and Medicaid lies in their funding and administration. Medicare is entirely federally managed, ensuring consistent benefits across the country, whereas Medicaid’s state-based structure leads to variations in eligibility, coverage, and provider networks. This duality highlights the fragmented nature of U.S. healthcare, where public coverage is tailored to specific groups rather than the population as a whole. For instance, a 66-year-old retiree in Texas would rely on Medicare for their healthcare needs, while a low-income family in the same state might depend on Medicaid, with both programs offering different levels of access and services.

To maximize benefits under these programs, beneficiaries should stay informed about enrollment periods, coverage changes, and cost-saving opportunities. For Medicare, enrolling during the Initial Enrollment Period (three months before and after turning 65) avoids late penalties. Medicaid applicants should check their state’s eligibility rules and apply through the state agency or Healthcare.gov. Practical tips include reviewing the Medicare “Extra Help” program for prescription drug cost assistance and exploring Medicaid waivers for additional services like home-based care. By understanding these programs’ nuances, individuals can better navigate the U.S. healthcare landscape and secure the coverage they need.

A Step-by-Step Guide to Applying for Individual Health Insurance

You may want to see also

Explore related products

![Drug coverage under national health insurance : Proceedings of the national conference, October 5-7, 1977 Editors : Milton Silverman and Mia Lydecker. 1978 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Affordable Care Act Impact

The Affordable Care Act (ACA), often referred to as Obamacare, has significantly reshaped the American healthcare landscape since its enactment in 2010. One of its most notable impacts is the expansion of health insurance coverage to millions of previously uninsured individuals. By introducing health insurance marketplaces, mandating individual coverage, and expanding Medicaid eligibility, the ACA aimed to address the fragmented nature of the U.S. healthcare system. Unlike countries with national health insurance, the U.S. relies on a mix of private and public programs, and the ACA sought to bridge gaps in this hybrid model. For example, as of 2023, over 14 million people have gained coverage through Medicaid expansion alone, demonstrating the ACA’s role in increasing access to care.

However, the ACA’s impact extends beyond coverage numbers; it has also introduced consumer protections that have transformed the insurance market. Prior to the ACA, insurers could deny coverage based on pre-existing conditions or impose lifetime coverage limits. The ACA eliminated these practices, ensuring that individuals with conditions like diabetes, cancer, or asthma could access affordable insurance. Additionally, young adults under 26 can remain on their parents’ plans, a provision that has benefited over 13 million people. These changes have not only improved access but also shifted public expectations of what health insurance should provide.

Critics argue that the ACA has fallen short of creating a universal healthcare system, as the U.S. still lacks a single-payer or national health insurance program. While the ACA reduced the uninsured rate, approximately 8% of Americans remain uninsured, often due to gaps in Medicaid expansion in certain states or affordability issues. Premiums and out-of-pocket costs have continued to rise, leaving some individuals underinsured despite having coverage. This highlights the ACA’s limitations in achieving comprehensive, affordable care for all, a hallmark of national health insurance systems in other countries.

Practically, the ACA’s impact is felt in everyday healthcare decisions. For instance, preventive services like vaccinations, cancer screenings, and annual check-ups are now covered without cost-sharing, encouraging proactive health management. Small businesses have also benefited from tax credits for providing employee insurance, though uptake has been lower than expected. To maximize ACA benefits, individuals should compare plans during open enrollment, consider subsidies if eligible, and utilize preventive services to avoid costly treatments later. While the ACA has made strides, it remains a patchwork solution in a system that still lacks the universality of national health insurance.

Does the ID Waiver Cover Health Insurance? Understanding Your Benefits

You may want to see also

Explore related products

![]()

Private vs. Public Coverage

The United States does not have a universal national health insurance system, unlike many other developed nations. Instead, it operates a hybrid model where private and public coverage coexist, each with distinct advantages and limitations. This duality shapes access, cost, and quality of care for millions of Americans. Understanding the differences between private and public coverage is essential for navigating the complexities of the U.S. healthcare system.

Private health insurance, typically obtained through employers or purchased individually, offers flexibility and choice. Plans vary widely in terms of coverage, provider networks, and out-of-pocket costs. For instance, a high-deductible health plan (HDHP) paired with a Health Savings Account (HSA) can be cost-effective for healthy individuals under 40, allowing them to save pre-tax dollars for medical expenses. However, private insurance often excludes pre-existing conditions or charges higher premiums for them, leaving vulnerable populations at a disadvantage. Additionally, administrative costs in private insurance are significantly higher, with estimates suggesting they account for up to 12% of premiums, compared to 2% in Medicare.

Public coverage, primarily through Medicare and Medicaid, serves specific demographics: Medicare for those over 65 or with disabilities, and Medicaid for low-income individuals and families. These programs provide more standardized benefits and lower out-of-pocket costs but often come with restricted provider networks and longer wait times. For example, while Medicare Part A covers hospital stays, Part B requires a monthly premium and still leaves beneficiaries responsible for 20% of outpatient costs unless they purchase supplemental insurance. Medicaid, though comprehensive, varies drastically by state, with some states imposing work requirements or limiting eligibility, creating disparities in access.

A critical comparison lies in cost control. Public programs like Medicare negotiate drug prices more effectively, while private insurers often face higher rates due to fragmented bargaining power. For instance, the average cost of insulin in the U.S. is $98.70 per unit under private insurance, compared to $13.77 in Medicare Part D. This disparity highlights the inefficiencies of private coverage in controlling costs. Conversely, private insurance often provides faster access to specialists and innovative treatments, which public programs may delay due to budget constraints.

In practice, the choice between private and public coverage depends on individual circumstances. For a 55-year-old with chronic conditions, Medicare may offer better financial protection, while a 30-year-old freelancer might opt for a private plan with a broader network. Employers play a pivotal role, with 56% of Americans receiving insurance through work, though this ties coverage to employment status. Policymakers must address these gaps, potentially through reforms like a public option or expanded Medicaid eligibility, to ensure equitable access. Ultimately, the private-public divide reflects broader debates about the role of government in healthcare, balancing individual choice with collective responsibility.

DuPage Medical Group: Understanding Your Health Insurance Options

You may want to see also

Explore related products

![]()

Uninsured Population Statistics

The United States stands out among developed nations for its lack of universal health coverage, leaving a significant portion of its population uninsured. As of 2023, approximately 8.5% of Americans, or around 28 million people, lack health insurance. This figure, while lower than the pre-Affordable Care Act (ACA) era, still represents a substantial gap in access to healthcare. The uninsured rate varies widely by state, with states that expanded Medicaid under the ACA generally reporting lower uninsured rates. For instance, Texas has an uninsured rate of 18%, one of the highest in the nation, while Massachusetts boasts a rate of just 3%, largely due to its early adoption of health reform measures.

Analyzing the demographics of the uninsured reveals stark disparities. Young adults aged 19 to 34 make up a disproportionate share of the uninsured population, often due to perceived good health and the high cost of premiums. However, this age group is not immune to accidents or sudden illnesses, making their lack of coverage a significant risk. Low-income individuals are another heavily affected group, with many falling into the "coverage gap" in states that did not expand Medicaid. These individuals earn too much to qualify for traditional Medicaid but too little to afford private insurance, even with subsidies. Racial and ethnic minorities also face higher uninsured rates, with Hispanic Americans being the most likely to lack coverage, at 19%, compared to 6% of non-Hispanic whites.

To address these disparities, policymakers must consider targeted interventions. Expanding Medicaid in the 10 remaining non-expansion states could cover up to 4 million uninsured adults, significantly reducing the national uninsured rate. Additionally, increasing awareness of ACA subsidies could help more low-income individuals enroll in affordable plans. For young adults, public health campaigns emphasizing the importance of preventive care and the financial risks of being uninsured could shift perceptions. Employers also play a critical role; offering more affordable health insurance options or promoting health savings accounts (HSAs) could encourage greater enrollment among workers.

A comparative look at other countries highlights the urgency of reducing the uninsured population in the U.S. Nations with universal health coverage, such as Canada and the United Kingdom, report uninsured rates near 0%. Even countries with multi-payer systems, like Germany and France, achieve near-universal coverage through mandatory insurance requirements. The U.S. could draw lessons from these models by exploring policies that combine public and private solutions to ensure broader access. For instance, a public option or automatic enrollment systems could reduce barriers to coverage while maintaining a competitive insurance market.

Ultimately, the uninsured population statistics in the U.S. underscore the need for systemic change. While incremental improvements have been made, millions remain at risk due to gaps in the current system. Addressing this issue requires a multi-faceted approach that tackles affordability, awareness, and accessibility. By learning from both domestic successes and international examples, the U.S. can move closer to ensuring that all its citizens have access to the healthcare they need.

Step-by-Step Guide to Applying for Kaiser Health Insurance Coverage

You may want to see also

Explore related products

$35.24 $37.99

![]()

Global Healthcare Comparisons

The United States stands as one of the few developed nations without a universal, single-payer healthcare system. Instead, it relies on a complex mix of private insurance, employer-sponsored plans, and government programs like Medicare and Medicaid. This fragmented approach contrasts sharply with systems in countries like Canada, the United Kingdom, and Germany, where national health insurance ensures coverage for all citizens. For instance, Canada’s single-payer system provides comprehensive care with no out-of-pocket costs for essential services, while Germany uses a multi-payer model with mandatory insurance contributions, ensuring universal access. These global examples highlight the diversity of healthcare structures and raise questions about equity, cost, and outcomes.

Analyzing healthcare systems globally reveals stark differences in cost and accessibility. In the U.S., healthcare expenditures per capita are nearly double those of countries with universal coverage, yet outcomes such as life expectancy and infant mortality lag behind. For example, the U.S. spends approximately $12,000 per person annually on healthcare, compared to $5,000 in the UK or $6,000 in Germany. Despite this investment, Americans face higher rates of chronic conditions and lower preventive care utilization. This disparity underscores the inefficiencies of a system reliant on private insurance, where profit motives often prioritize revenue over patient care.

To understand the impact of national health insurance, consider the case of Japan, where a universal system has achieved some of the highest life expectancies globally. Japanese citizens pay into a national insurance scheme, with premiums based on income, and receive comprehensive coverage for medical services. This model ensures that even low-income individuals access quality care without financial barriers. In contrast, the U.S. system often leaves uninsured or underinsured individuals delaying care due to cost, leading to worse health outcomes. Implementing a national insurance program could address these gaps by prioritizing preventive care and reducing administrative waste.

A persuasive argument for national health insurance lies in its potential to improve equity and reduce disparities. Countries with universal coverage, such as Sweden and Australia, report lower rates of health inequality compared to the U.S. In Sweden, for instance, healthcare is funded through progressive taxation, ensuring that wealthier individuals contribute proportionally more. This redistributive approach aligns with principles of social justice, providing equal access regardless of income. By adopting a similar model, the U.S. could mitigate the financial strain on vulnerable populations and foster a healthier, more productive society.

Finally, transitioning to a national health insurance system requires careful planning and stakeholder engagement. Steps include assessing current infrastructure, designing a sustainable funding mechanism, and phasing in coverage to minimize disruption. Cautions include avoiding one-size-fits-all solutions, as cultural and economic contexts vary widely. For example, a hybrid model combining public and private elements, as seen in France, could offer flexibility while ensuring universal access. The takeaway is clear: global comparisons provide valuable lessons for the U.S. as it grapples with healthcare reform, emphasizing the need for a system that prioritizes equity, efficiency, and outcomes.

Medicare: The Largest Insurance Provider in the US?

You may want to see also

Frequently asked questions

The US does not have a universal national health insurance program like those in many other developed countries. Instead, it relies on a mix of private insurance, employer-sponsored plans, and government programs like Medicare and Medicaid.

The closest programs to national health insurance in the US are Medicare, which covers individuals aged 65 and older and some younger people with disabilities, and Medicaid, which provides coverage for low-income individuals and families. These are government-funded but not universal.

The lack of a national health insurance system in the US is due to historical, political, and economic factors. Early reliance on employer-based insurance, strong opposition from private insurers, and ideological debates about the role of government in healthcare have prevented the adoption of a universal system.

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61ilSrOeMoL._AC_UL320_.jpg)

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61wrmwXah3L._AC_UL320_.jpg)