Trip cancellation insurance is a type of travel insurance that covers travellers in the event they need to cancel their trip for a covered reason. This can include unforeseen illnesses or injuries, inclement weather, natural disasters, and other unforeseen events. The specific covered reasons vary by plan and provider, so it is important to carefully review the policy before purchasing. In addition to trip cancellation coverage, some providers offer comprehensive plans that include additional protections such as medical coverage, emergency evacuation, lost baggage, and travel delays. These comprehensive plans typically offer coverage for a wider range of concerns and may be more suitable for travellers seeking more extensive protection. It is worth noting that trip cancellation insurance does not cover all reasons for cancellation and may exclude pre-existing medical conditions or foreseeable events.

Characteristics and Values

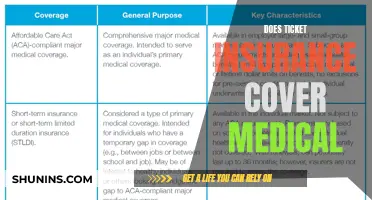

| Characteristics | Values |

|---|---|

| Reimbursement amount | Up to 75% to 80% of covered trip costs |

| Coverage | Medical and medical evacuation, trip cancellation, trip interruption, travel delays, lost baggage, emergency medical situations, 24/7 assistance via phone |

| Time limit to purchase | Within 10-21 days of making the initial trip payment |

| Time limit to redeem | 48 to 72 hours before the trip |

| Pre-existing medical conditions | Excluded from coverage unless requirements for a Pre-Existing Condition Exclusion Waiver are met |

| Foreseeable events | Not covered |

Explore related products

![[*Mini Size*] TIRTIR Mask Fit Ai Filter Cushion Foundation | AI-Like Semi-Matte Finish - Up to 72-Hour Medium to Full Coverage Korean BB Cushion Make up Beauty, #21W Natural Ivory, 0.15 Fl Oz](https://m.media-amazon.com/images/I/71L1tmXgk4L._AC_UL320_.jpg)

What You'll Learn

- Trip cancellation insurance covers unforeseen illness or injury

- Pre-existing conditions are excluded unless requirements for a waiver are met

- Trip cancellation insurance does not cover losses from expected or foreseeable events

- Cancel for Any Reason (CFAR) coverage offers partial reimbursement for non-covered reasons

- CFAR coverage must be purchased within a certain time frame of the initial trip payment

![]()

Trip cancellation insurance covers unforeseen illness or injury

Trip cancellation insurance is a common feature of comprehensive travel insurance policies. It covers unforeseen illness or injury, including epidemics and pandemics, that may force you to cancel your trip. The severity of the illness, injury, or medical condition must be such that it is considered life-threatening or requires hospitalisation. Pre-existing medical conditions are typically excluded from coverage unless you meet the requirements for a Pre-Existing Condition Exclusion Waiver.

The specific covered reasons for trip cancellation vary by plan, so it is important to refer to your plan documents to understand what is covered. For example, some plans may cover unforeseen natural disasters at your destination, while others may not. Additionally, trip cancellation insurance does not cover losses that arise from expected or reasonably foreseeable events or problems, even if they are listed as covered reasons.

It is worth noting that trip cancellation insurance is different from "cancel for any reason" coverage, which is an optional upgrade that allows you to cancel your trip for almost any reason and still receive partial reimbursement, typically between 50% and 80% of your prepaid, non-refundable costs. This add-on typically comes with eligibility requirements and may increase your travel insurance premium.

When purchasing trip cancellation insurance, it is important to carefully review the terms and conditions, including any exclusions and requirements for reimbursement, to ensure that you have the coverage you need.

Billing Patients with Dual Insurance: Commercial and Medicaid

You may want to see also

Explore related products

![[*Mini Size*] TIRTIR Mask Fit Red Cushion Foundation | Full coverage, Weightless, Skin fit, Satin Glow Finish, Korean Makeup BB Foundation, beauty, Tattoo cover up, Buildable (#21N Ivory, 0.15 Fl Oz)](https://m.media-amazon.com/images/I/61E8xkyaRnL._AC_UL320_.jpg)

![]()

Pre-existing conditions are excluded unless requirements for a waiver are met

Pre-existing medical conditions are generally not covered by travel insurance. However, you can purchase a pre-existing condition exclusion waiver to be covered for problems related to pre-existing conditions during your trip. This waiver is offered by some travel insurance companies and can be included in your policy if you meet certain requirements.

To be eligible for the waiver, you typically need to purchase your travel insurance policy within a specific timeframe, often within 14 to 21 days of booking your trip or making your initial trip deposit. This timeframe requirement varies depending on the insurer, so it is essential to review the specific policy details. Additionally, to qualify for the waiver, you must be medically cleared to travel at the time of purchasing the insurance and provide a letter from your doctor confirming your fitness to travel. Your medical condition must also be stable, with no changes or new developments within a certain timeframe before taking out the insurance, usually between 60 and 180 days.

It is important to note that the pre-existing condition waiver only applies if the amount of coverage purchased equals the total prepaid, non-refundable cost of your trip. This includes subsequent arrangements added to the trip, which must be insured by the date of payment or deposit for those additional arrangements. The waiver ensures that your travel insurance company cannot use your recent medical history as a reason to deny your claim.

While the pre-existing condition waiver can provide valuable coverage, it is essential to carefully review the terms and conditions of your travel insurance policy. Understand the specific requirements and limitations of the waiver to ensure you are adequately protected during your trip.

In summary, while pre-existing medical conditions are typically excluded from travel insurance coverage, obtaining a pre-existing condition exclusion waiver can provide coverage for issues related to your pre-existing condition during your travels. Be sure to review the eligibility criteria and purchase your insurance and waiver in a timely manner to ensure you meet the requirements for this additional protection.

Riverview Medical Center: Cigna Insurance Acceptance and Benefits

You may want to see also

Explore related products

![]()

Trip cancellation insurance does not cover losses from expected or foreseeable events

Trip cancellation insurance is a popular benefit that reimburses prepaid, non-refundable expenses if you cancel your trip due to unexpected events. However, it's important to note that trip cancellation insurance does not cover losses from expected or foreseeable events. This includes situations that were known at the time of purchasing the plan, such as an already-announced airline strike, named storm, or terrorist attack. For example, if you buy travel insurance for a trip to the Bahamas while a hurricane is heading towards your destination, your insurance won't cover the loss if your beach house loses its roof. Similarly, if you have a foreseen medical procedure, it won't be covered under trip cancellation insurance.

For trip cancellation insurance to apply, the cancellation must be due to unforeseen circumstances. These can include unforeseen illnesses, injuries, or deaths of the insured person, a travelling companion, or a family member, as deemed by a licensed physician. Some policies may also cover unforeseen hospitalizations of non-travelling family members. It's important to note that pre-existing medical conditions are typically excluded from coverage unless you meet the requirements for a Pre-Existing Condition Exclusion Waiver.

Additionally, trip cancellation insurance may cover a range of other unforeseen events, such as inclement weather, natural disasters, terrorism, financial default of travel companies, work-related emergencies, and mandatory evacuations due to natural disasters. It's important to carefully review the specific terms and conditions of your chosen plan, as covered reasons can vary.

To ensure you have the option to cancel for any reason, including expected or foreseeable events, you may need to purchase a comprehensive plan with optional "Cancel For Any Reason" coverage. This add-on is offered by several insurance providers and typically allows for reimbursement of up to 75-80% of trip costs. However, eligibility requirements may apply, such as insuring 100% of prepaid, non-refundable trip costs and purchasing the coverage within a specified timeframe after your initial trip payment.

Hormone Replacement Therapy: Is It Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

Cancel for Any Reason (CFAR) coverage offers partial reimbursement for non-covered reasons

CFAR is an optional upgrade that must be purchased in addition to primary travel insurance. It is not available as a standalone policy. To be eligible for reimbursement, you must cancel your trip within a certain timeframe, usually 48 to 72 hours before your scheduled departure. The specific timeframe varies by policy, so it is important to review the details of your chosen plan carefully.

It is also crucial to note that CFAR only covers eligible expenses. Most policies require travelers to insure 100% of their prepaid, non-refundable trip costs to qualify for CFAR. Additionally, CFAR typically offers a partial refund, with reimbursement levels ranging from 50% to 75% of your insured trip cost, depending on the plan.

While CFAR provides flexibility and peace of mind, it is important to understand the limitations. For example, if you accept a voucher, credit, or partial reimbursement from a travel supplier, your claim may not be eligible for CFAR reimbursement. Furthermore, CFAR does not cover costs associated with travel arrangements that are not provided by your travel supplier.

When considering CFAR, carefully review the terms and conditions of the policy, including eligibility requirements, reimbursement levels, and any exclusions or limitations. It is also advisable to compare multiple CFAR plans from different providers to find the one that best suits your needs.

Understanding Medical Insurance: Employer Responsibilities and Obligations

You may want to see also

Explore related products

![]()

CFAR coverage must be purchased within a certain time frame of the initial trip payment

When purchasing CFAR coverage, there is a limited timeframe to do so. Typically, CFAR coverage must be purchased within 10 to 21 days of making the initial trip payment. This timeframe is crucial, as it determines your eligibility for CFAR benefits. Some policies may offer a shorter or longer window, with the shortest being 10 days and the longest being 21 days. It's important to carefully review the specific requirements of your chosen policy to ensure you don't miss the deadline.

The time-sensitive nature of CFAR coverage is a key factor to consider. It is designed to provide travellers with greater flexibility and peace of mind. By purchasing CFAR coverage within the specified timeframe, you can take advantage of the ability to cancel your trip for reasons beyond those listed as "covered reasons" in a standard trip cancellation policy. This added flexibility is especially valuable if you have concerns or uncertainties about your travel plans that may not be covered by standard trip cancellation insurance.

The reimbursement rates for CFAR coverage vary, typically ranging from 50% to 75% of your insured prepaid non-refundable trip cost. It's important to note that CFAR coverage usually does not provide 100% reimbursement. However, some companies, like Allianz Travel Insurance, offer a Cancel Anytime policy that reimburses up to 80% of prepaid non-refundable trip costs.

In addition to the timeframe for purchasing CFAR coverage, it's important to be mindful of the cancellation timeframe. Most CFAR policies require you to cancel your plans and notify your travel suppliers at least 48 hours before your scheduled departure. Some policies may require cancellation up to 72 hours in advance. These timeframes are crucial to ensuring your eligibility for reimbursement under CFAR coverage.

CFAR coverage is a valuable option for travellers who want the flexibility to cancel their trip for any reason. By understanding the timeframes and reimbursement rates associated with CFAR coverage, you can make informed decisions about your travel insurance choices and gain peace of mind for your journey.

Latisse Treatment: What Does Medical Insurance Cover?

You may want to see also

Frequently asked questions

Trip cancellation insurance covers a wide range of reasons for cancellation, including unforeseen illnesses, injuries, or medical conditions, inclement weather, natural disasters, and travel delays. It also covers situations like the death of a travelling companion, jury duty, or hospitalization of a family member.

Trip cancellation insurance covers specific unforeseen reasons for cancellation, while CFAR allows you to cancel for any reason, even those not typically covered. CFAR provides partial reimbursement, usually 50-80% of prepaid, non-refundable trip costs.

CFAR must be purchased within a specific timeframe of your initial trip deposit, typically within 10-21 days. It is important to review the eligibility requirements and specific timeframes of your chosen policy.

CFAR can provide coverage in various situations, such as when you don't feel comfortable travelling due to COVID-19 cases, safety concerns about your destination, family or work obligations, or if your travel companion can no longer join you.

Yes, CFAR plans often include emergency medical coverage and medical evacuation services. However, it is important to carefully review the specific details of your chosen policy, as coverage may vary.