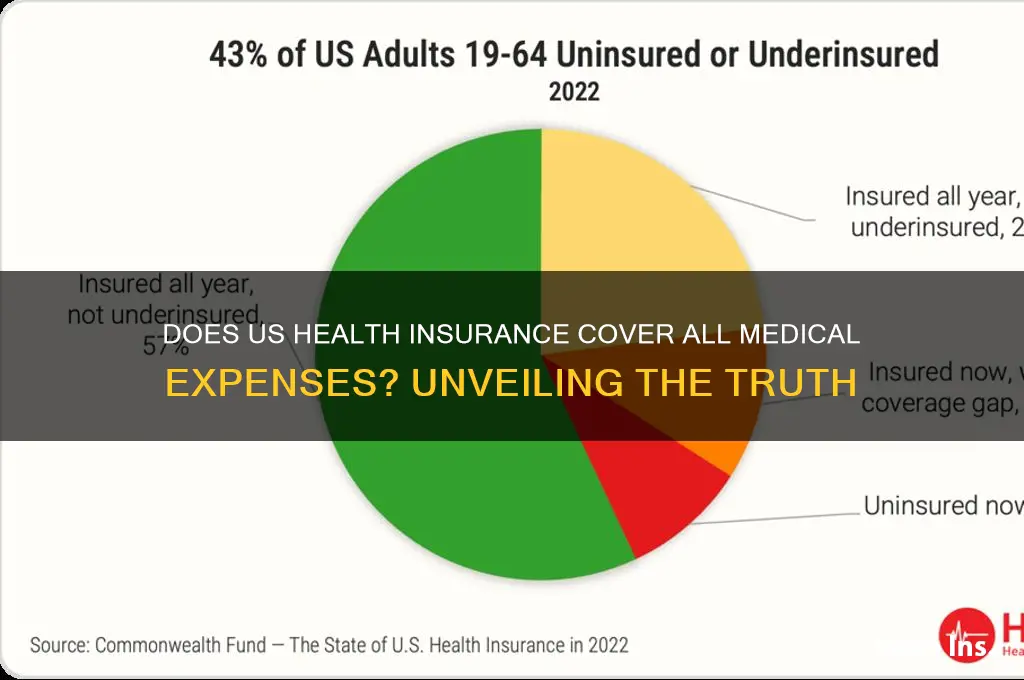

Health insurance in the United States is a complex and often confusing topic, leaving many individuals wondering whether their coverage truly encompasses all medical needs. While health insurance plans aim to provide financial protection against healthcare expenses, the reality is that not all services or treatments are fully covered. The extent of coverage varies significantly depending on the specific policy, provider, and type of insurance, such as private plans, employer-sponsored insurance, or government programs like Medicare and Medicaid. Factors like deductibles, copayments, and exclusions can limit what is covered, often leaving policyholders with out-of-pocket costs. Understanding the intricacies of one's insurance plan is crucial to avoid unexpected expenses and ensure adequate coverage for medical care.

Explore related products

What You'll Learn

![]()

Pre-existing Conditions Coverage

Pre-existing conditions, such as diabetes, asthma, or cancer, historically posed significant challenges for individuals seeking health insurance in the U.S. Before the Affordable Care Act (ACA) of 2010, insurers could deny coverage, charge higher premiums, or exclude treatment for these conditions. The ACA’s landmark provision prohibits insurers from discriminating based on pre-existing conditions, ensuring that millions can access comprehensive coverage regardless of their health history. This shift marked a critical step toward equitable healthcare, but understanding its nuances remains essential for consumers navigating the system.

Consider a 45-year-old with hypertension, a common pre-existing condition affecting nearly half of U.S. adults. Under the ACA, this individual cannot be denied coverage or charged more than a healthy applicant of the same age. However, the type of plan and insurer still matter. Employer-sponsored plans and ACA-compliant marketplace plans must cover pre-existing conditions, but short-term or limited-duration plans—often marketed as affordable alternatives—may exclude them. For instance, a short-term plan might cover emergency care but exclude ongoing treatment for hypertension, leaving the individual responsible for costly medications like lisinopril (typically $10–$50/month) or doctor visits.

The ACA’s protections extend to essential health benefits, including prescription drugs, hospitalization, and preventive care, which are crucial for managing pre-existing conditions. For example, a patient with type 2 diabetes (affecting 1 in 10 Americans) relies on these benefits for insulin (averaging $200–$500/month without insurance), A1C tests, and specialist visits. Yet, gaps remain. While insurers cannot exclude these services, they can impose high deductibles or copays, making care unaffordable for some. A Silver-level ACA plan might cover insulin after a $3,000 deductible, forcing patients to pay full price until they meet it.

To maximize coverage for pre-existing conditions, follow these steps: First, enroll in an ACA-compliant plan during open enrollment (or within 60 days of a qualifying event like job loss). Second, compare plans using the ACA marketplace’s tools, focusing on out-of-pocket costs for your specific medications and treatments. Third, leverage cost-saving programs like patient assistance programs (e.g., Sanofi’s Insulin Valyou Savings Program, which caps insulin costs at $35/month) or generic drug options. Finally, appeal any denials of coverage for pre-existing conditions, citing the ACA’s protections.

Despite the ACA’s progress, challenges persist. Insurers may still impose waiting periods for pre-existing conditions in group plans (up to 90 days for employer-based coverage), though this is rare. Additionally, the ACA’s future remains uncertain amid political debates. For now, individuals with pre-existing conditions have unprecedented access to coverage, but vigilance is key. Stay informed about policy changes, review plan details annually, and advocate for your rights to ensure continuous, affordable care.

GM Employees: Understanding Your Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Prescription Drug Costs

To navigate these costs, patients must understand their insurance plan’s drug formulary—a list of covered medications tiered by cost. Tier 1 drugs (usually generics) have the lowest copays, while Tier 4 or specialty drugs require higher out-of-pocket expenses. For example, a generic statin like atorvastatin might cost $10 for a 30-day supply, whereas a brand-name biologic like Humira could cost $500 or more. Patients can reduce costs by asking their doctor to prescribe generics or by using manufacturer coupons, though these are often unavailable for specialty drugs. Additionally, programs like Medicare Part D or state-based pharmaceutical assistance programs (SPAPs) can provide financial relief for eligible individuals.

A comparative analysis reveals that U.S. prescription drug prices are significantly higher than in other developed countries, largely due to the lack of government price controls. In Canada, for instance, the same insulin vial that costs $300 in the U.S. might cost $30. While U.S. health insurance plans do cover prescription drugs, the extent of coverage varies widely. High-deductible plans may require patients to pay full price until they meet their deductible, while comprehensive plans might offer immediate coverage with modest copays. Employers often subsidize these costs, but gaps remain, particularly for those on individual plans or Medicare.

Persuasively, policymakers and advocates argue that systemic changes are needed to address this crisis. Proposals include allowing Medicare to negotiate drug prices, capping out-of-pocket costs, and increasing transparency in pricing. Until such reforms are implemented, patients must take proactive steps: compare prices at different pharmacies (apps like GoodRx can help), request 90-day supplies to lower per-dose costs, and appeal insurance denials for medically necessary drugs. While U.S. health insurance does cover prescription drugs, it’s clear that coverage is neither universal nor sufficient, leaving many to grapple with the financial weight of staying healthy.

On-Site Gyms: Reducing Health Insurance Costs Through Workplace Wellness

You may want to see also

Explore related products

![]()

Mental Health Services

Consider the case of medication management, a cornerstone of treatment for conditions like depression or anxiety. While most insurance plans cover FDA-approved medications, the specifics vary widely. Some plans may require patients to try cheaper, generic options before approving brand-name drugs, a process known as step therapy. Others might limit coverage for newer, more expensive medications like esketamine (a nasal spray for treatment-resistant depression), leaving patients to pay out-of-pocket costs that can exceed $1,000 per dose. Knowing your plan’s formulary—its list of covered drugs—can save both time and money.

For children and adolescents, mental health coverage often hinges on age-specific needs. Insurers typically cover diagnostic evaluations, such as psychological testing for ADHD or autism, but the extent of therapy coverage can differ. For example, applied behavior analysis (ABA) therapy for autism is mandated in many states but may be capped at a certain number of hours per week. Parents should also be aware of telehealth options, which have expanded significantly since the pandemic, offering convenient access to child psychologists or counselors without the need for in-person visits.

When navigating mental health coverage, proactive steps can make a significant difference. First, review your plan’s summary of benefits to understand copays, deductibles, and out-of-network costs. Second, keep detailed records of all communications with your insurer, including denial letters or prior authorization requests. Third, if coverage is denied, appeal the decision—many denials are overturned upon review. Finally, consider supplemental insurance or employee assistance programs (EAPs), which often provide additional mental health resources not covered by standard plans.

Despite progress, gaps in mental health coverage persist, particularly for specialized treatments like intensive outpatient programs (IOPs) or residential care. For example, while some plans cover IOPs for substance use disorders, coverage for eating disorder treatment may be limited to short-term hospitalization. Advocacy groups like the National Alliance on Mental Illness (NAMI) offer resources to help individuals understand their rights and challenge unfair denials. Ultimately, while insurance may not cover everything, informed persistence can unlock access to essential mental health services.

Understanding Your Company's Latest Insurance Switch: Reasons and Impact

You may want to see also

Explore related products

![]()

Out-of-Network Expenses

Consider this scenario: A 35-year-old with a PPO plan visits an out-of-network specialist for a complex procedure. The total cost is $10,000, but the insurer only covers 60% after meeting the deductible. If the deductible is $2,000, the patient’s responsibility could exceed $4,000. To mitigate such risks, always verify a provider’s network status before scheduling appointments. Use your insurer’s online directory or call their customer service line for confirmation. If an out-of-network provider is unavoidable, request a detailed cost estimate upfront and explore payment plans or financial assistance programs.

From a comparative standpoint, HMOs are stricter than PPOs regarding out-of-network coverage, often requiring a referral and limiting reimbursement to emergencies only. For example, an HMO policyholder seeking out-of-network mental health care might receive no coverage unless it’s deemed medically necessary and pre-approved. In contrast, PPOs offer more flexibility but at a higher premium cost. For those on high-deductible health plans (HDHPs), out-of-network expenses can be particularly burdensome, as the deductible must be met before any coverage kicks in. Pairing an HDHP with a Health Savings Account (HSA) can help offset these costs, allowing tax-free savings for medical expenses.

Persuasively, it’s worth advocating for transparency in out-of-network billing practices. Legislation like the No Surprises Act, effective January 2022, protects patients from surprise bills for emergency services and certain out-of-network care at in-network facilities. However, gaps remain, especially for non-emergency procedures. Patients should actively engage with their insurers, asking about balance billing policies and appealing denied claims when appropriate. Additionally, consider negotiating directly with providers for reduced rates or payment plans, particularly for elective procedures.

In conclusion, out-of-network expenses are a critical blind spot in U.S. health insurance coverage, demanding proactive management. By understanding your plan’s limitations, verifying provider networks, and leveraging available resources, you can minimize financial surprises. Treat out-of-network care as a last resort, and when unavoidable, approach it with informed caution and strategic planning.

Understanding the Governing Body for Insurance Companies: Roles and Responsibilities

You may want to see also

Explore related products

$9.97

![]()

Preventive Care Inclusions

US health insurance plans often highlight preventive care as a cornerstone of their coverage, but what does this actually mean for policyholders? Preventive care inclusions typically encompass services designed to detect and mitigate health risks before they escalate into costly treatments. Under the Affordable Care Act (ACA), most plans are required to cover a range of preventive services without charging a copay or deductible. These services include vaccinations, screenings, and check-ups tailored to age, gender, and risk factors. For instance, adults aged 18–60 are entitled to blood pressure screenings annually, while women over 21 can access cervical cancer screenings every three years. Understanding these inclusions is crucial, as they not only promote long-term health but also reduce out-of-pocket expenses.

Consider the practical implications of these inclusions. For a 45-year-old man, preventive care might involve a colonoscopy to screen for colorectal cancer, covered at no cost under ACA-compliant plans. Similarly, a 30-year-old woman could receive a mammogram every one to two years starting at age 40, depending on her risk profile. Vaccinations, such as the annual flu shot or the Tdap vaccine for tetanus, diphtheria, and pertussis, are also included. However, not all preventive services are created equal. Some plans may require pre-authorization or limit coverage to in-network providers, so policyholders should verify details with their insurer. Proactive engagement with these benefits can lead to early detection of conditions like diabetes or hypertension, where timely intervention can significantly alter health outcomes.

A comparative analysis reveals that while preventive care inclusions are standard, their scope can vary. For example, some plans may cover nutritional counseling for individuals at risk of obesity-related diseases, while others might exclude it. Similarly, mental health screenings for depression or anxiety are often included, but the frequency and depth of these assessments can differ. Employers offering self-funded plans may also have flexibility in defining preventive care, potentially limiting coverage compared to ACA-compliant plans. This variability underscores the importance of reviewing plan documents carefully. For families, ensuring children receive age-appropriate vaccinations and developmental screenings is non-negotiable, as these services are universally covered but often underutilized.

Persuasively, investing time in understanding and utilizing preventive care inclusions is one of the smartest moves a policyholder can make. For instance, a 50-year-old individual who undergoes a covered lung cancer screening might detect early-stage disease, where survival rates are dramatically higher. Similarly, a 25-year-old with a family history of heart disease could benefit from lipid disorder screenings, enabling lifestyle changes before cholesterol levels become dangerous. The financial argument is equally compelling: preventive care reduces the likelihood of expensive emergency room visits or chronic disease management. Insurers benefit too, as healthier policyholders mean lower claims costs. Thus, preventive care is not just a covered benefit—it’s a strategic tool for both individuals and the healthcare system.

Finally, a descriptive approach highlights the human element of preventive care inclusions. Imagine a mother scheduling her child’s well-child visit, where immunizations, growth assessments, and developmental milestones are reviewed at no cost. Or a senior citizen accessing an annual wellness visit to discuss fall prevention strategies and medication management. These scenarios illustrate how preventive care is woven into the fabric of everyday health management. Yet, awareness remains a barrier; many policyholders are unaware of the full extent of their benefits. Insurers and healthcare providers must bridge this gap through education and outreach, ensuring that preventive care is not just an inclusion but a utilized lifeline. In this way, the promise of comprehensive coverage becomes a lived reality.

Skin Biopsy: Is Medical Insurance Coverage Guaranteed?

You may want to see also

Frequently asked questions

No, U.S. health insurance typically does not cover all medical expenses. Coverage varies by plan, and most policies have exclusions, deductibles, copays, and coinsurance that limit what is covered.

Yes, under the Affordable Care Act (ACA), U.S. health insurance plans cannot deny coverage or charge more for pre-existing conditions. However, coverage specifics depend on the plan.

Most U.S. health insurance plans cover prescription medications, but the extent of coverage depends on the plan’s formulary, which lists covered drugs and their cost-sharing tiers.

Dental and vision care are often not included in standard U.S. health insurance plans. Separate dental and vision insurance policies or add-ons are typically required for coverage.

Coverage for out-of-network providers varies by plan. Some plans offer partial coverage, while others may not cover out-of-network services at all, leading to higher out-of-pocket costs.