USAA homeowners insurance may cover broken water lines, depending on the policy and circumstances. USAA offers sewer line insurance as an add-on to its homeowners insurance coverage, which includes repairs, backups, and sudden damage. Home insurance typically covers water leaks and damage caused by sudden or accidental plumbing issues, but not gradual leaks due to wear and tear. It is important to review the specific terms and conditions of your policy or contact USAA directly to determine if water line replacement or repair is covered.

| Characteristics | Values |

|---|---|

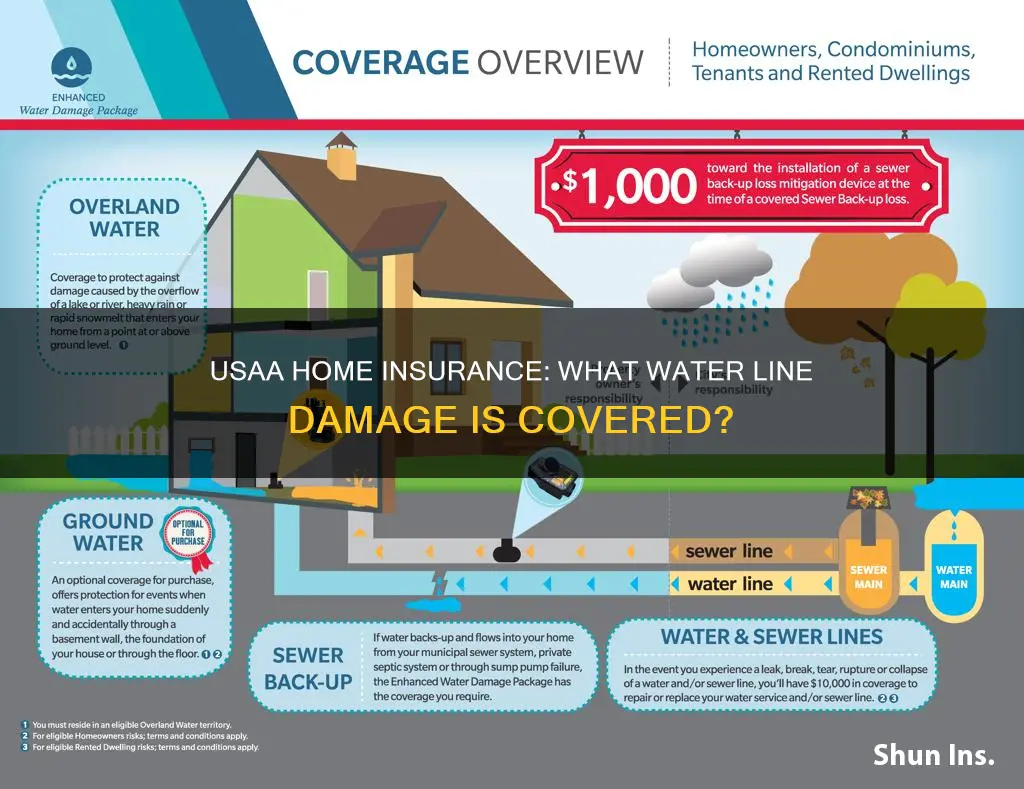

| Sewer line damage covered by USAA | Covered if caused by perils such as accidental discharge or overflow of water, freezing of plumbing, or sudden damage |

| Sewer line replacement covered by USAA | Not typically covered unless caused by a covered peril, such as sudden damage |

| Water damage covered by USAA | Covered for sudden and unforeseen water damage due to plumbing or broken pipes; excludes gradual damage and certain water-related damage, such as mold |

| Sewer backup covered by USAA | Yes |

| Water line insurance offered by USAA | Yes, as an optional add-on to cover damage to underground water lines not included in standard policies |

Explore related products

What You'll Learn

![]()

USAA's sewer line insurance

USAA homeowners insurance may cover sewer line damage and repair, depending on the policy and circumstances. USAA offers sewer line insurance as an add-on to its homeowners insurance coverage options, which will help with repairs, backup, and more. This is because standard homeowners insurance policies, including those offered by USAA, typically do not provide coverage for sewer line replacement unless it is caused by a covered peril, such as sudden damage.

To determine if your USAA homeowners insurance covers sewer line damage and repair, it is important to carefully review the terms and conditions of your specific policy. Contact USAA directly for more information and guidance on understanding your policy coverage and filing a claim.

Home Insurance: Does It Cover Broken Sliding Doors?

You may want to see also

Explore related products

![]()

Coverage for sudden damage

USAA homeowners insurance covers sudden damage caused by plumbing or broken pipes. This includes damage caused by a ruptured water heater or burst pipes. Home insurance typically covers water leaks caused by sudden or accidental damage, but not gradual leaks due to wear and tear. It is important to note that USAA homeowners insurance does not typically cover foundation repairs unless they result from a covered peril, such as sudden collapse.

In the case of sewer line damage, USAA homeowners insurance may cover water line replacement, depending on the policy and circumstances. Sewer line insurance can be added as an optional extra to cover damage to underground water lines not included in standard homeowners policies. This type of insurance covers repairs, backups, and sudden and accidental damage. However, it is important to note that sewer line repairs or replacements typically do not fall under standard homeowner insurance policies, and USAA sewer line insurance may be required as an add-on for incidents to be covered.

USAA's dwelling coverage clause covers any water damage to the foundation of your home, including the roof, walls, and floorboards. If a leak damages part of your building or you need to remove part of a barrier to repair a leak, your dwelling coverage will reimburse you. Additionally, property coverage under USAA homeowners insurance will compensate for any personal property lost when a plumbing failure causes damage to your house. Certain luxury items, such as watches, may have limited coverage, and additional coverage may be purchased through optional riders.

It is important to review your specific policy or contact USAA directly to understand the coverage provided by your homeowners insurance. Understanding the limitations of your policy can help you determine if additional coverage options are necessary to protect against sudden damage.

Ryanair Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Water damage from inside the home

USAA homeowners insurance covers water damage from sources originating from inside the home. This includes sudden and accidental water damage, such as a burst pipe or ruptured water heater. It's important to note that not all water damage is covered, and gradual damage from persistent leaks may be excluded. Additionally, flooding, defined as water rising from outside the home, typically requires separate flood insurance.

USAA's dwelling coverage clause covers the home's foundation, roof, walls, and floorboards, as well as built-in appliances like water heaters. Property coverage compensates for any personal property lost due to plumbing failures. Additional Living Expenses (ALE) coverage reimburses temporary relocation expenses, including hotel, transport, and food costs.

To file a water damage claim with USAA, you can log in to your online account, use the mobile app, or call their claims line. You'll need to provide details about the damage, including when it happened, the cause (if known), and any steps taken to minimize further impact. USAA will assign a claim number and connect you with an adjuster to assess the damage and finalize the claim.

Before filing a claim, it's essential to understand your policy's coverage and deductible for water damage claims. The deductible is the amount you pay out of pocket before your policy coverage begins. Once the deductible is met, USAA typically provides an initial payment based on the Actual Cash Value (ACV) of the damage. If you have replacement cost coverage, you'll receive additional funds to cover remaining repair costs after submitting final invoices.

To maximize your insurance payout, consider the following:

- Document the damage properly and quickly to prevent further damage.

- Don't toss out any damaged items until a USAA adjuster has inspected them.

- Install a leak detection system to alert you to small leaks before they become bigger problems.

Earthquake Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Flood insurance for external water damage

Water damage and flood damage are distinct concepts in the context of insurance, and they require different types of coverage. Water damage typically refers to damage caused by internal sources of water within the home, such as burst pipes, leaks, or accidental overflows from appliances. This type of damage is usually covered by standard homeowners insurance policies. On the other hand, flood damage refers to damage caused by external sources of water, such as overflowing rivers, heavy rain, storm surges, or other natural events that cause water to enter a home. Flood damage is not typically covered by standard homeowners insurance and requires a separate flood insurance policy.

The National Flood Insurance Program (NFIP), managed by FEMA, is the largest single-line insurance program in the nation, providing nearly $1.3 trillion in coverage against floods. The NFIP defines a flood as "a general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties from overflow of inland or tidal waters, unusual and rapid accumulation or runoff of surface waters from any source, or mudflow." This definition establishes the boundary between flood damage and water damage in insurance terms.

Flood insurance is available to property owners, renters, and businesses through the NFIP and can cover buildings, contents, or both. It is important to note that there is typically a 30-day waiting period for an NFIP policy to go into effect. Homes and businesses in high-risk flood areas with mortgages from government-backed lenders are required to have flood insurance.

In the case of USAA homeowners insurance, it may cover water line replacement depending on the specific policy and circumstances. USAA offers sewer line insurance as an add-on to its homeowners insurance coverage, which can help with repairs, backups, and sudden and accidental damage. However, traditional homeowners insurance policies, including those offered by USAA, typically do not cover sewer line replacement unless you pay extra for this specific coverage.

It is always important to carefully review the terms and conditions of your insurance policy to understand what is covered and what is not. In the case of water damage and flood damage, the distinction can be subtle but crucial in determining whether your insurance will provide coverage.

Houston Homeowners: Tornado Damage and Your Insurance

You may want to see also

Explore related products

![]()

Additional living expenses (ALE) coverage

ALE coverage is designed to pay for out-of-pocket expenses and temporary housing similar to the current home. It does not cover any costs that are part of regular expenses, such as utility bills or groceries. It is meant to cover the difference between temporary and usual costs. For example, if a family is displaced from their home due to a fire and has to move to a hotel, ALE coverage would reimburse them for the hotel costs, boarding costs for their dog, and the increase in their food bill due to eating out.

ALE coverage is typically included in homeowners insurance policies, but it is important to check the policy's terms. There may be a limit to the amount that can be paid out, and it is important to keep all receipts for any additional costs incurred during displacement.

Gun Ownership: Impact on Home Insurance Rates

You may want to see also

Frequently asked questions

USAA homeowners insurance may cover broken water lines, depending on the policy and circumstances.

USAA homeowners insurance typically covers damage to your home and personal belongings caused by covered perils such as fire, theft, vandalism, and certain natural disasters.

USAA homeowners insurance does not typically cover foundation repairs or sewer line replacement unless they result from a covered peril, such as sudden damage or collapse.

Review your policy documents or contact USAA directly to determine if your specific policy covers broken water lines.

Contact USAA as soon as possible to report the issue and initiate the claims process.