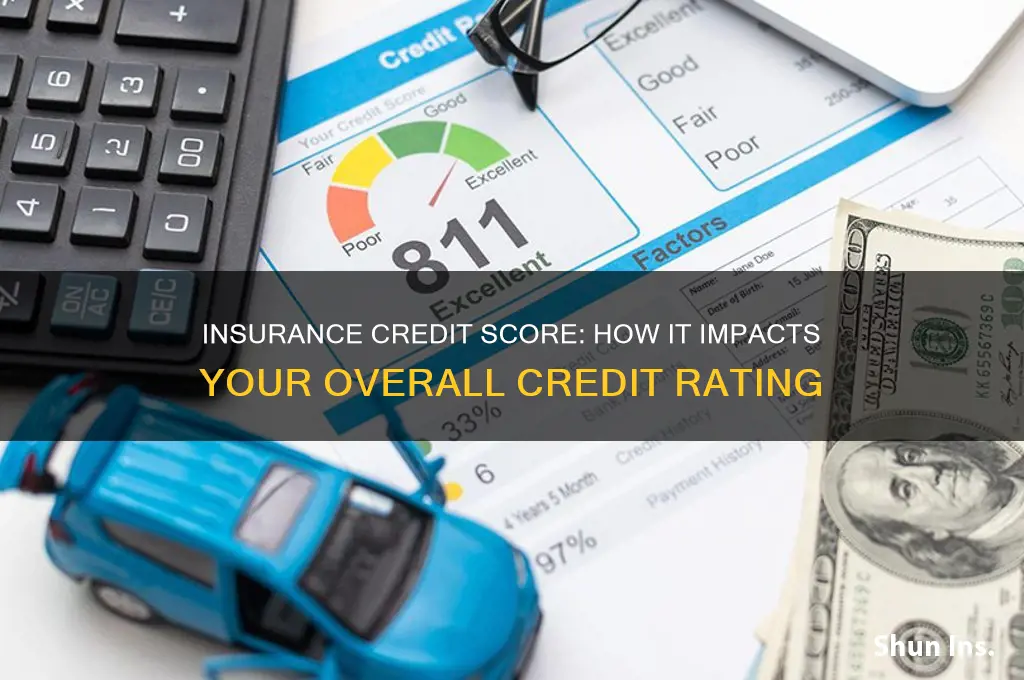

The relationship between insurance credit scores and traditional credit scores is a topic of significant interest and confusion for many consumers. An insurance credit score, also known as an insurance score, is a numerical rating used by insurance companies to predict the likelihood of a policyholder filing a claim. While it is derived from similar data as a traditional credit score, such as payment history and debt levels, it is calculated differently and used exclusively for insurance purposes. A common concern is whether checking or using an insurance credit score negatively impacts one's traditional credit score. Importantly, insurance credit score inquiries are considered soft pulls, meaning they do not affect your credit score. However, maintaining good financial habits remains crucial, as both scores reflect overall financial health and responsibility. Understanding this distinction can help consumers navigate insurance decisions without unnecessary worry about their credit standing.

| Characteristics | Values |

|---|---|

| Impact on Credit Score | Checking your insurance credit score does not directly impact your traditional credit score. Insurance credit scores are calculated separately and do not involve a "hard inquiry," which is what typically affects credit scores. |

| Data Used | Insurance credit scores use similar data to traditional credit scores, including payment history, debt levels, and credit age, but they weigh factors differently, emphasizing financial stability and insurance-related behaviors. |

| Purpose | Insurance credit scores are used by insurers to assess risk and determine premiums, not by lenders for credit decisions. |

| Reporting Agencies | Insurance credit scores are often provided by specialized agencies like LexisNexis Risk Solutions or Verisk Analytics, not the major credit bureaus (Equifax, Experian, TransUnion). |

| Regulation | Insurance credit scores are regulated by state laws, which may restrict their use or require transparency in how they are applied. |

| Consumer Access | Consumers can request a free copy of their insurance credit report annually, similar to traditional credit reports, to review accuracy and dispute errors. |

| Score Range | Insurance credit scores typically range from 200 to 997, with higher scores indicating lower risk and potentially lower insurance premiums. |

| Factors Not Considered | Unlike traditional credit scores, insurance credit scores do not consider factors like income, employment history, or race. |

| State Variations | Some states, like California, Maryland, and Massachusetts, prohibit the use of insurance credit scores for auto and home insurance underwriting. |

| Correlation with Claims | Studies show a correlation between lower insurance credit scores and higher insurance claims, which is why insurers use them to predict risk. |

Explore related products

What You'll Learn

- Insurance Credit Score Basics: Understanding how insurers calculate credit-based scores differently from traditional credit scores

- Impact on Credit Reports: Clarifying if insurance inquiries or payments affect your credit report or score

- Soft vs. Hard Inquiries: Explaining how insurance checks typically use soft inquiries, which don’t lower credit scores

- Payment History Role: Discussing how missed insurance payments can indirectly harm your credit if reported

- State Regulations: Highlighting states where using credit scores for insurance is banned or restricted

![]()

Insurance Credit Score Basics: Understanding how insurers calculate credit-based scores differently from traditional credit scores

When it comes to understanding how insurers calculate credit-based scores, it's essential to recognize that these scores differ significantly from traditional credit scores used by lenders. While both types of scores are derived from your credit report, insurers use a unique model tailored to predict insurance risk rather than creditworthiness. Traditional credit scores, such as FICO or VantageScore, focus on your ability to repay debt, whereas insurance credit scores assess the likelihood of you filing a claim. This distinction is crucial because it means that factors influencing your insurance credit score may not necessarily impact your traditional credit score in the same way.

Insurers calculate credit-based insurance scores using data from your credit report, but they weigh certain factors differently. For example, payment history remains important, but insurers may place more emphasis on outstanding debt and credit utilization. A high credit card balance or maxed-out credit limits could negatively affect your insurance credit score more than your traditional credit score. Additionally, insurers often consider the length of your credit history and the mix of credit types, but they may prioritize stability and consistency over recent credit inquiries or new accounts, which are more critical in traditional scoring models.

Another key difference lies in how insurers use credit-based scores. Unlike lenders, who primarily use credit scores to determine loan eligibility and interest rates, insurers use these scores to gauge the risk of insuring you. Studies have shown that individuals with lower insurance credit scores tend to file more claims, which can lead to higher premiums. However, it's important to note that checking your insurance credit score does not impact your traditional credit score, as these are separate assessments. Insurers typically use soft inquiries, which do not affect your credit, to evaluate your risk profile.

It's also worth mentioning that not all insurers use credit-based scores in the same way, and some states even restrict or prohibit their use in determining premiums. For instance, California, Massachusetts, and Hawaii have banned the use of credit-based insurance scores. If you live in a state where these scores are used, understanding how they are calculated can help you take steps to improve your standing. Paying bills on time, reducing debt, and maintaining a healthy credit mix are general practices that can positively influence both your traditional credit score and your insurance credit score.

In summary, while insurance credit scores and traditional credit scores share a common foundation in your credit report, they serve different purposes and are calculated with distinct priorities. Insurers focus on predicting insurance risk, which means certain financial behaviors may have a greater impact on your insurance credit score than on your traditional score. By understanding these differences, you can better manage your financial habits to maintain favorable scores across both systems. Remember, improving your overall credit health benefits you in multiple aspects of your financial life, from securing loans to obtaining affordable insurance premiums.

Birla Sun Life Insurance: Branch Network Across India

You may want to see also

Explore related products

$47.32 $54.99

![]()

Impact on Credit Reports: Clarifying if insurance inquiries or payments affect your credit report or score

When considering the impact of insurance on your credit reports, it's essential to distinguish between different types of insurance-related activities and their potential effects. Firstly, insurance inquiries occur when an insurance company checks your credit report as part of their underwriting process. These inquiries are typically classified as "soft inquiries," which do not affect your credit score. Soft inquiries are visible only to you and the entity making the inquiry, not to lenders or other third parties. Therefore, shopping around for insurance or having an insurer review your credit report will not lower your credit score.

However, insurance payments or lack thereof can have a more significant impact on your credit report. If you pay your insurance premiums on time, this generally does not directly improve your credit score, as insurance payments are not typically reported to the major credit bureaus (Equifax, Experian, and TransUnion). But if you fail to pay your premiums and your account goes into collections, the collection account will likely be reported to the credit bureaus, negatively affecting your credit score. Unpaid insurance bills can remain on your credit report for up to seven years, making it crucial to manage these payments responsibly.

Another aspect to consider is insurance credit scores, which are different from traditional credit scores. Insurance companies use these specialized scores to assess risk and determine premiums. Insurance credit scores are based on your credit report but are calculated differently from the scores used by lenders. Importantly, checking your own credit score or having an insurer generate an insurance credit score does not impact your traditional credit score. However, the factors that contribute to a poor insurance credit score (e.g., late payments, high debt) may also negatively affect your traditional credit score.

It's also worth noting that bundling insurance policies or paying premiums in full upfront does not directly influence your credit report or score. These actions may save you money or simplify your finances, but they do not factor into credit scoring models. Conversely, using a credit card to pay insurance premiums can impact your credit score if it increases your credit utilization ratio or leads to missed payments. Responsible credit card usage is key to maintaining a healthy credit profile.

In summary, insurance inquiries do not affect your credit score, as they are treated as soft inquiries. However, unpaid insurance bills that go into collections can significantly harm your credit report and score. While insurance payments themselves are not typically reported to credit bureaus, managing them responsibly is crucial to avoid negative consequences. Understanding the distinction between insurance credit scores and traditional credit scores can also help clarify how insurance-related activities impact your financial health. Always monitor your credit report regularly to ensure accuracy and address any discrepancies promptly.

Insurance Recoveries: Operating Assets or Not?

You may want to see also

Explore related products

![]()

Soft vs. Hard Inquiries: Explaining how insurance checks typically use soft inquiries, which don’t lower credit scores

When it comes to understanding how insurance checks impact your credit score, it's essential to differentiate between soft and hard inquiries. Soft inquiries are a type of credit check that occurs when a person or organization reviews your credit report without the intention of extending credit. These inquiries are typically used for informational purposes and do not affect your credit score. In contrast, hard inquiries happen when a financial institution, such as a lender or credit card company, checks your credit report as part of a credit application. Hard inquiries can temporarily lower your credit score, as they indicate that you're seeking new credit.

In the context of insurance, most checks are conducted using soft inquiries. Insurance companies often review your credit report to assess your risk profile and determine your insurance premiums. This practice, known as insurance scoring, helps insurers predict the likelihood of you filing a claim. Since insurance checks are not related to extending credit, they are considered soft inquiries and do not impact your credit score. This is a crucial distinction, as it means that shopping around for insurance or having multiple insurers check your credit report will not harm your creditworthiness.

The use of soft inquiries in insurance checks is a standard industry practice, and it's regulated by the Fair Credit Reporting Act (FCRA). Under the FCRA, insurance companies are permitted to access your credit report for underwriting purposes without your explicit permission, but they must use the information responsibly. This includes ensuring that their inquiries do not negatively affect your credit score. As a result, you can feel confident that obtaining insurance quotes or switching providers will not result in a marked-down credit score due to hard inquiries.

It's worth noting that while soft inquiries from insurance companies won't lower your credit score, they may still appear on your credit report. However, these inquiries are only visible to you and do not affect your creditworthiness in the eyes of lenders or other financial institutions. This transparency allows you to monitor your credit report and ensure that all inquiries are accurate and authorized. If you notice any discrepancies or unauthorized hard inquiries, you have the right to dispute them with the credit reporting agencies.

In summary, when it comes to insurance checks and your credit score, the key takeaway is that soft inquiries are the norm. These inquiries enable insurance companies to assess your risk profile without impacting your creditworthiness. By understanding the difference between soft and hard inquiries, you can make informed decisions about shopping for insurance and managing your credit score. Remember, insurance checks are a routine part of the underwriting process, and they're designed to help insurers determine your premiums, not to lower your credit score. By being aware of these practices, you can navigate the insurance landscape with confidence and peace of mind.

Life Insurance: No Net Worth, No Problem?

You may want to see also

Explore related products

![]()

Payment History Role: Discussing how missed insurance payments can indirectly harm your credit if reported

When it comes to understanding the relationship between insurance and credit scores, the role of payment history is crucial. While insurance companies primarily use their own credit-based insurance scores to assess risk and determine premiums, missed insurance payments can still have an indirect impact on your traditional credit score. This occurs when insurance companies report delinquent accounts to collection agencies, which then report them to the major credit bureaus. Payment history is the most significant factor in your credit score, accounting for approximately 35% of the total. Therefore, any negative marks resulting from missed insurance payments can substantially harm your creditworthiness.

Missed insurance payments typically do not appear directly on your credit report unless they are severely past due and sent to collections. Insurance companies generally do not report on-time payments to credit bureaus, but they may report accounts that are 60 to 90 days delinquent. Once an account is in collections, it becomes a red flag on your credit report, signaling to lenders that you have failed to meet your financial obligations. This negative entry can remain on your credit report for up to seven years, significantly lowering your credit score and making it harder to secure loans, credit cards, or favorable interest rates in the future.

The indirect harm caused by missed insurance payments underscores the importance of maintaining a consistent payment history. Even though insurance payments themselves are not usually factored into your credit score, the consequences of non-payment can be severe. For instance, a single collection account can drop your credit score by 50 to 100 points, depending on your overall credit profile. This drop can be particularly damaging if you have a limited credit history or a borderline credit score, as it may push you into a lower credit tier and limit your financial options.

To avoid these negative outcomes, it is essential to prioritize timely insurance payments. Setting up automatic payments or reminders can help ensure you never miss a due date. If you are facing financial difficulties, contact your insurance provider immediately to discuss potential payment arrangements or extensions. Proactive communication can often prevent an account from being sent to collections, thereby protecting your credit score. Additionally, regularly monitoring your credit report allows you to catch any inaccuracies or unexpected collection accounts early, giving you the opportunity to dispute them before they cause long-term damage.

In summary, while insurance payments do not directly impact your credit score, missed payments that result in collections can have a significant and lasting negative effect. Understanding the role of payment history and taking steps to maintain timely payments are key to safeguarding your creditworthiness. By staying vigilant and addressing issues promptly, you can minimize the risk of indirect harm to your credit score and maintain a healthy financial profile.

Autonation's Warranties: Self-Insured or Not?

You may want to see also

Explore related products

![]()

State Regulations: Highlighting states where using credit scores for insurance is banned or restricted

Several states in the U.S. have implemented regulations to limit or ban the use of credit scores in insurance underwriting, recognizing the potential for unfair practices and disparities in premiums. California, for instance, has enacted strict laws prohibiting the use of credit-based insurance scores for both auto and homeowners insurance. This means insurers operating in California cannot factor in an individual’s credit history when determining premiums or eligibility, ensuring that consumers are not penalized for financial hardships unrelated to their driving or claims history.

Another state taking a firm stance is Massachusetts, which has banned the use of credit scores in auto insurance underwriting since 2006. This regulation was implemented to promote fairness and prevent discrimination, as credit scores were found to disproportionately affect low-income individuals and communities of color. Massachusetts insurers must rely on driving records, claims history, and other relevant factors instead of credit information when setting rates.

Maryland has also restricted the use of credit scores in insurance, particularly for auto insurance. The state’s regulations limit how much weight insurers can give to credit-based insurance scores, ensuring that credit history does not become the primary factor in determining premiums. This approach strikes a balance between allowing insurers to assess risk and protecting consumers from excessive reliance on credit data.

In Michigan, while not a complete ban, the state has imposed significant restrictions on the use of credit scores in insurance. Michigan’s regulations require insurers to provide clear justifications for using credit information and mandate that credit-based scores cannot be the sole factor in denying coverage or setting rates. This ensures greater transparency and accountability in the underwriting process.

Washington is another state moving toward restricting credit score usage in insurance. Recent legislative efforts aim to limit or ban the practice, particularly for auto insurance, to address concerns about fairness and equity. These proposed regulations reflect a growing trend among states to reevaluate the role of credit scores in insurance and prioritize consumer protection.

These state-level regulations highlight a broader movement to decouple credit scores from insurance underwriting, addressing concerns that such practices can perpetuate financial inequality. Consumers in these states benefit from greater protection against unfair premium increases or denials based on credit history, ensuring that insurance remains accessible and affordable for all.

American Life Insurance: What's in a Name?

You may want to see also

Frequently asked questions

No, checking your insurance credit score does not impact your regular credit score. Insurance credit scores are based on credit reports but are calculated differently and do not involve a hard inquiry.

Your insurance credit score can influence your insurance premiums. Insurers use it to assess risk, and a lower score may result in higher premiums, while a higher score may lead to lower rates.

No, your insurance credit score is different from your regular credit score. It focuses on factors insurers believe predict insurance risk, such as payment history and debt levels, rather than overall creditworthiness.

Yes, improving your insurance credit score involves similar steps to improving your regular credit score, such as paying bills on time, reducing debt, and correcting errors on your credit report.

No, not all insurance companies use credit scores. Usage varies by state and insurer, and some states restrict or prohibit the use of credit scores in determining insurance premiums.