Having health insurance is a critical aspect of financial and personal well-being, as it provides essential protection against the high costs of medical care. Whether it’s routine check-ups, emergency treatments, or chronic condition management, health insurance ensures access to necessary healthcare services without the burden of overwhelming expenses. It also promotes preventive care, encouraging individuals to seek early interventions that can prevent more serious health issues down the line. Beyond individual benefits, health insurance contributes to a healthier society by reducing the strain on public health systems and fostering a more productive workforce. In many countries, it is also a legal requirement, making it a fundamental responsibility for citizens and residents alike. Investing in health insurance is not just a financial decision but a proactive step toward safeguarding one’s health and future.

Explore related products

What You'll Learn

- Types of Plans: HMO, PPO, EPO, and POS plans offer different coverage and provider networks

- Coverage Benefits: Includes doctor visits, hospitalization, prescriptions, preventive care, and emergency services

- Cost Factors: Premiums, deductibles, copays, and coinsurance determine out-of-pocket expenses

- Enrollment Periods: Open enrollment, special enrollment, and Medicaid/Medicare deadlines for signing up

- Provider Networks: In-network vs. out-of-network providers impact costs and coverage availability

![]()

Types of Plans: HMO, PPO, EPO, and POS plans offer different coverage and provider networks

Choosing the right health insurance plan can feel like navigating a maze. Four common types—HMO, PPO, EPO, and POS—each offer distinct coverage and provider network structures, catering to different needs and preferences. Understanding these differences is crucial to ensuring you get the care you need without unexpected costs.

HMOs, or Health Maintenance Organizations, prioritize cost-effectiveness and coordinated care. You’ll select a primary care physician (PCP) who acts as your healthcare quarterback, managing referrals to specialists within the network. While HMOs typically have lower premiums and out-of-pocket costs, they require in-network care except in emergencies. This structure works well for individuals who value affordability and are comfortable with a managed care approach.

PPOs, or Preferred Provider Organizations, offer more flexibility in choosing providers. You can see any doctor or specialist within the network without a referral, and even visit out-of-network providers, though at a higher cost. Premiums and out-of-pocket expenses are generally higher than HMOs, but the trade-off is greater freedom in accessing care. PPOs are ideal for those who prioritize choice and are willing to pay more for it.

EPOs, or Exclusive Provider Organizations, combine elements of HMOs and PPOs. Like HMOs, they require you to stay within the network for coverage, but they don’t mandate a PCP or referrals to specialists. EPOs often have lower premiums than PPOs, making them a cost-effective option for those who don’t need out-of-network flexibility. However, coverage is typically limited to in-network care, except in emergencies.

POS plans, or Point of Service plans, blend HMO and PPO features. You’ll choose a PCP and need referrals for specialists, but you can also access out-of-network providers at a higher cost. While POS plans offer more flexibility than HMOs, they often come with higher premiums and out-of-pocket costs than EPOs. This plan suits individuals who want a balance between managed care and the option to seek out-of-network treatment.

When selecting a plan, consider your healthcare needs, budget, and preference for provider flexibility. For instance, if you have a chronic condition requiring frequent specialist visits, a PPO might be worth the higher cost. Conversely, if you’re generally healthy and prioritize affordability, an HMO or EPO could be a better fit. Always review the plan’s provider network, coverage details, and cost-sharing structure to ensure it aligns with your lifestyle and medical requirements.

Malpractice Insurance: A Requirement for New York's Medical Professionals?

You may want to see also

Explore related products

![]()

Coverage Benefits: Includes doctor visits, hospitalization, prescriptions, preventive care, and emergency services

Health insurance isn't just a financial safety net; it's a gateway to essential healthcare services. At its core, comprehensive coverage ensures access to a spectrum of benefits, from routine check-ups to life-saving interventions. These benefits—doctor visits, hospitalization, prescriptions, preventive care, and emergency services—form the backbone of a robust health insurance plan, addressing both immediate and long-term health needs. Without them, individuals risk delaying care, facing exorbitant out-of-pocket costs, or forgoing treatment altogether. Understanding these coverage benefits is the first step in maximizing the value of your health insurance.

Consider the practicality of doctor visits, often the first line of defense in maintaining health. Whether it’s an annual physical, a sick visit, or a specialist consultation, these appointments are critical for early detection and management of health issues. For instance, a 45-year-old with a family history of diabetes can benefit from regular blood glucose screenings, which, when covered, cost nothing out-of-pocket. Similarly, a child’s immunizations, typically included in preventive care, ensure protection against diseases like measles and whooping cough. Without insurance, these visits could cost hundreds of dollars each, creating a barrier to consistent care.

Hospitalization coverage is another non-negotiable component, especially given the staggering costs of inpatient care. A three-day hospital stay for pneumonia, for example, can exceed $30,000 without insurance. With coverage, however, individuals pay only a fraction of this amount, often limited to a deductible or copay. This benefit extends to surgeries, maternity care, and intensive treatments like chemotherapy. For families, this coverage provides peace of mind, knowing that a medical emergency won’t lead to financial ruin. It’s a safeguard that transforms unpredictable expenses into manageable ones.

Prescription drug coverage is equally vital, particularly for chronic conditions. A month’s supply of insulin, for instance, can cost over $300 without insurance. With coverage, this drops to a copay of $10–$50, depending on the plan. Similarly, medications for hypertension, asthma, or mental health conditions become accessible, ensuring adherence to treatment plans. Some plans even offer mail-order options for maintenance medications, reducing costs further. Without this benefit, many would be forced to choose between medication and other essentials, compromising their health in the process.

Preventive care and emergency services round out the essentials, each serving distinct yet interconnected roles. Preventive care, fully covered under most plans, includes screenings like mammograms, colonoscopies, and cholesterol checks, tailored to age and risk factors. For example, a 50-year-old man would benefit from a colonoscopy to detect early signs of colon cancer, a procedure that costs upwards of $3,000 without insurance. Emergency services, on the other hand, provide immediate care for accidents, severe injuries, or sudden illnesses. A trip to the ER for a broken arm, for instance, could cost $2,000–$5,000 without coverage, but with insurance, the expense is significantly reduced. Together, these benefits ensure that health maintenance and crisis management are both within reach.

In essence, the coverage benefits of health insurance are not just add-ons but necessities for a healthy, financially secure life. They empower individuals to seek care proactively, manage chronic conditions effectively, and face emergencies without fear of bankruptcy. By understanding and utilizing these benefits—doctor visits, hospitalization, prescriptions, preventive care, and emergency services—policyholders can navigate the healthcare system with confidence, ensuring that their well-being remains a priority, not a privilege.

Printing Insurance Carriers in Kareo Medical Billing: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

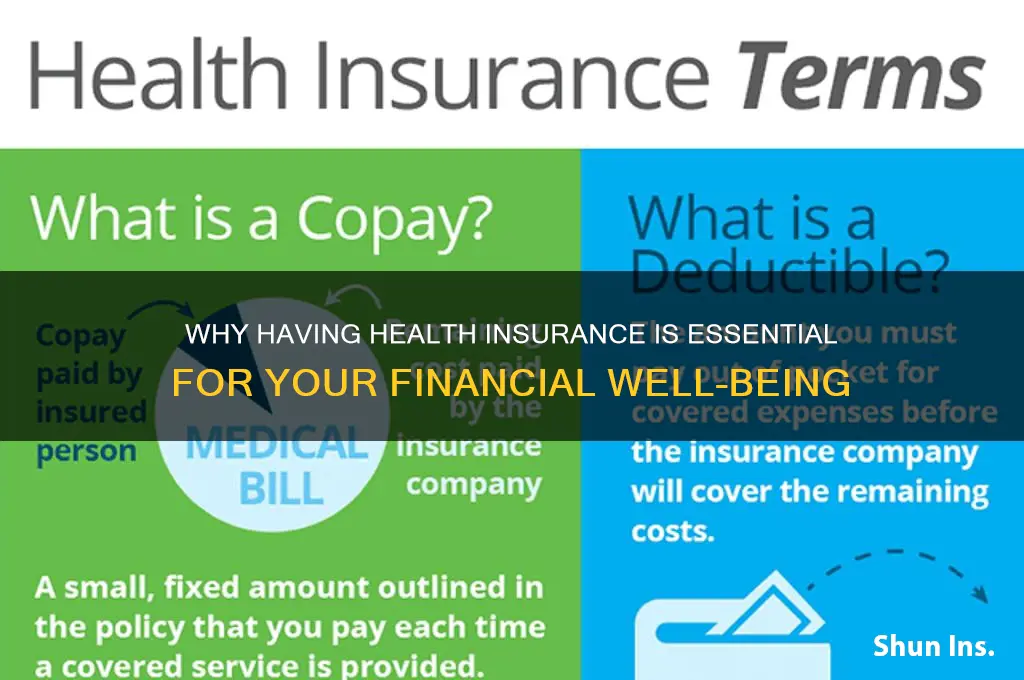

Cost Factors: Premiums, deductibles, copays, and coinsurance determine out-of-pocket expenses

Understanding the cost factors of health insurance is crucial for anyone looking to manage their healthcare expenses effectively. Premiums, deductibles, copays, and coinsurance are the four pillars that determine your out-of-pocket costs, each playing a distinct role in how much you’ll pay for medical services. Premiums are your monthly payments to maintain coverage, regardless of whether you use healthcare services. For instance, a family of four might pay $1,200 monthly for a comprehensive plan, while an individual could pay as little as $300 for a high-deductible plan. Choosing the right premium involves balancing affordability with the level of coverage needed.

Deductibles are the amount you must pay out of pocket before your insurance starts covering costs. A plan with a $2,000 deductible means you’ll cover all expenses up to that amount before insurance kicks in. High-deductible plans often pair with lower premiums, making them attractive for healthy individuals who rarely visit the doctor. However, if you require frequent medical care, a lower deductible plan might save you money in the long run, despite higher monthly premiums. For example, a 30-year-old with no chronic conditions might opt for a high-deductible plan, while a 50-year-old with diabetes may benefit from a lower deductible.

Copays and coinsurance further influence your out-of-pocket expenses once you’ve met your deductible. A copay is a fixed amount you pay for a specific service, such as $25 for a doctor’s visit or $10 for a prescription. Coinsurance, on the other hand, is a percentage of the cost you share with your insurer after the deductible is met. For instance, if your plan has 20% coinsurance, you’ll pay $200 for a $1,000 procedure, while the insurer covers the remaining $800. Understanding these costs helps you budget for unexpected medical needs, like a sudden ER visit or a specialist consultation.

To minimize out-of-pocket expenses, consider your healthcare usage patterns and financial situation. If you anticipate high medical costs, such as pregnancy or ongoing treatment for a chronic condition, a plan with higher premiums but lower deductibles and copays may be more cost-effective. Conversely, if you’re generally healthy and rarely seek medical care, a lower-premium, high-deductible plan paired with a health savings account (HSA) could offer tax advantages while covering catastrophic events. For example, contributing $3,000 annually to an HSA can offset high deductibles while reducing taxable income.

Ultimately, navigating health insurance costs requires a strategic approach. Review your plan’s summary of benefits to understand how premiums, deductibles, copays, and coinsurance interact. Use online calculators to estimate annual expenses based on your expected healthcare needs. For instance, a tool like Healthcare.gov’s subsidy calculator can help determine if you qualify for premium tax credits. By aligning your plan with your health and financial profile, you can avoid unexpected costs and ensure you’re getting the most value from your coverage.

Navigating Medical Insurance: A Student's Guide to Getting Covered

You may want to see also

Explore related products

![]()

Enrollment Periods: Open enrollment, special enrollment, and Medicaid/Medicare deadlines for signing up

Understanding enrollment periods is crucial for securing health insurance coverage without facing penalties or gaps in care. Open Enrollment, typically running from November 1 to December 15 each year, is the designated window for most individuals to sign up for or change their health insurance plans. Missing this deadline means you’ll likely have to wait a full year unless you qualify for a Special Enrollment Period (SEP). SEPs are triggered by life events such as marriage, divorce, birth of a child, loss of job-based coverage, or moving to a new state. Each event grants you a 60-day window to enroll, but documentation proving the qualifying event is required. For example, if you lose employer-sponsored insurance, you’ll need a letter from your former employer confirming the termination date.

Medicaid and Medicare operate on different timelines, offering more flexibility but still requiring attention to deadlines. Medicaid enrollment is open year-round, but eligibility is income-based and varies by state. For instance, in states that expanded Medicaid under the Affordable Care Act, individuals earning up to 138% of the federal poverty level qualify. However, processing times can take weeks, so applying early is advisable. Medicare, on the other hand, has specific enrollment periods: the Initial Enrollment Period (IEP) begins three months before your 65th birthday and ends three months after. Missing the IEP can result in late enrollment penalties, such as a 10% premium surcharge for Part B. The General Enrollment Period (January 1 to March 31) is available for those who missed their IEP but doesn’t include prescription drug coverage.

Comparing these enrollment periods highlights the importance of planning ahead. Open Enrollment is rigid, while SEPs and Medicaid offer more flexibility but require prompt action after a qualifying event. Medicare’s structure is age-based and less forgiving for latecomers. For instance, if you’re turning 65 and still working, you might delay Medicare enrollment if your employer’s insurance is credible coverage, but you’ll need to enroll within eight months of leaving that job to avoid penalties. Understanding these nuances can save you from unnecessary stress and financial burden.

Practical tips can make navigating these deadlines smoother. Set calendar reminders for Open Enrollment and Medicare IEP dates. Keep a file of life event documents, such as marriage certificates or job termination letters, to expedite SEP applications. If you’re nearing Medicare age, consult the Social Security Administration or a healthcare navigator to understand how your current coverage interacts with Medicare. For Medicaid, use state-specific resources to estimate eligibility and gather required income documentation beforehand. Proactive planning ensures you’re covered when you need it most, avoiding the pitfalls of missed deadlines or inadequate insurance.

Medical Insurance: Understanding Death Benefits and Payouts

You may want to see also

Explore related products

![]()

Provider Networks: In-network vs. out-of-network providers impact costs and coverage availability

Health insurance plans often come with a designated provider network, a critical factor that directly influences both costs and coverage. In-network providers have agreements with your insurer, offering services at pre-negotiated rates. This means you typically pay less out-of-pocket for visits, procedures, and prescriptions. For instance, a routine check-up with an in-network doctor might cost you a $20 copay, while the same visit with an out-of-network provider could result in a $150 bill after insurance adjustments. Understanding this distinction is essential for maximizing your plan’s benefits and minimizing unexpected expenses.

Consider the scenario of a 35-year-old individual with a PPO (Preferred Provider Organization) plan. While PPOs offer flexibility to see out-of-network providers, the cost difference is significant. An in-network MRI might cost $500, with insurance covering 80% after a $50 copay. The same MRI out-of-network could cost $2,000, with insurance covering only 60% after a $200 deductible. Over time, these disparities add up, making in-network care a financially prudent choice. However, if you require a specialist not in your network, weigh the cost against the necessity of the care.

For those with HMO (Health Maintenance Organization) plans, the stakes are even higher. HMOs typically require you to stay in-network for all non-emergency care, except in rare cases with prior authorization. Going out-of-network without approval can result in the insurer denying coverage entirely, leaving you responsible for the full cost. For example, a $5,000 surgery covered in-network might cost you $10,000 or more out-of-network, with no insurance contribution. Always verify a provider’s network status before scheduling appointments to avoid such pitfalls.

Practical tips can help navigate these complexities. First, use your insurer’s online provider directory to confirm network status before booking appointments. Second, if you need an out-of-network specialist, ask for a detailed cost estimate upfront and check if your plan offers any out-of-network coverage. Third, consider negotiating rates with out-of-network providers, as some may offer discounts for self-pay patients. Finally, if you frequently require out-of-network care, evaluate whether switching to a PPO or a plan with broader network coverage would be more cost-effective in the long run.

In conclusion, provider networks are a cornerstone of health insurance, shaping both affordability and accessibility. While in-network care generally offers lower costs and seamless coverage, out-of-network services can be financially burdensome and require careful planning. By understanding these dynamics and leveraging available tools, you can make informed decisions that align with your healthcare needs and budget.

Labor in Cedar Sinai: Insurance Coverage Experience

You may want to see also

Frequently asked questions

Health insurance is a type of coverage that pays for medical and surgical expenses incurred by the insured. It is important because it helps protect individuals from high healthcare costs, ensures access to necessary medical care, and provides financial security in case of unexpected illnesses or accidents.

Qualification for health insurance depends on factors like your income, employment status, age, and location. You can qualify through employer-sponsored plans, government programs like Medicaid or Medicare, or purchase individual plans through the Health Insurance Marketplace.

Health insurance typically covers doctor visits, hospital stays, emergency care, prescription medications, preventive services (like vaccinations and screenings), and mental health services. Coverage specifics vary by plan, so it’s important to review your policy details.

Yes, self-employed individuals can purchase health insurance through the Health Insurance Marketplace, private insurers, or professional associations. They may also qualify for subsidies based on income to help reduce costs.

Without health insurance, you may face high out-of-pocket costs for medical care, limited access to healthcare services, and potential financial hardship in case of serious illness or injury. Additionally, you may be subject to penalties in some regions, though this varies by country and state.