Health insurance in New Hampshire is a critical component of the state’s healthcare landscape, offering residents access to essential medical services while mitigating the financial burden of unexpected health issues. With a mix of private insurance plans, employer-sponsored coverage, and government programs like Medicaid and Medicare, New Hampshire residents have several options to meet their healthcare needs. The state’s insurance marketplace, facilitated through the Affordable Care Act (ACA), provides individuals and families with a platform to compare and purchase plans tailored to their budgets and medical requirements. Additionally, New Hampshire has made strides in expanding coverage, particularly through Medicaid expansion, ensuring more low-income individuals and families can access affordable care. However, challenges remain, including rising premiums, limited provider networks, and disparities in access, particularly in rural areas. Understanding the nuances of health insurance in New Hampshire is essential for residents to make informed decisions and secure the coverage that best fits their health and financial circumstances.

Explore related products

$17.48 $18.95

What You'll Learn

- NH Health Insurance Providers: Overview of major insurers offering plans in New Hampshire

- Affordable Care Act in NH: How ACA impacts health insurance options and subsidies in the state

- Medicaid Expansion in NH: Eligibility and benefits of expanded Medicaid under Granite Advantage

- Short-Term Health Plans: Temporary coverage options, limitations, and availability in New Hampshire

- NH Health Insurance Costs: Average premiums, deductibles, and factors affecting plan prices

![]()

NH Health Insurance Providers: Overview of major insurers offering plans in New Hampshire

New Hampshire residents have access to a variety of health insurance providers, each offering distinct plans tailored to different needs and budgets. Among the major players, Anthem Blue Cross and Blue Shield of New Hampshire stands out as the largest insurer in the state, covering a significant portion of the population. Anthem offers a wide range of plans, including HMO, PPO, and high-deductible health plans (HDHPs) with Health Savings Account (HSA) options. Their network includes most major hospitals and healthcare providers in the state, making it a reliable choice for comprehensive coverage. For families, Anthem’s plans often include pediatric care and preventive services, which are essential for maintaining long-term health.

Another prominent insurer is Harvard Pilgrim Health Care, known for its focus on customer satisfaction and preventive care. Harvard Pilgrim offers plans with robust wellness programs, including discounts on gym memberships and access to telehealth services. Their plans are particularly appealing to individuals and families who prioritize proactive health management. For example, their “ElevateHealth” program provides personalized health coaching and resources to help members manage chronic conditions like diabetes or hypertension. This insurer also stands out for its high provider satisfaction ratings, which can be a deciding factor for those seeking seamless healthcare experiences.

Ambetter from NH Healthy Families is a key player in the Affordable Care Act (ACA) marketplace, offering subsidized plans for low- to moderate-income individuals and families. These plans are designed to be cost-effective while still providing essential health benefits, such as emergency care, maternity care, and prescription drug coverage. Ambetter’s plans are particularly beneficial for those who qualify for premium tax credits, as they can significantly reduce out-of-pocket costs. For instance, a family of four earning up to $100,000 annually may be eligible for subsidies, making Ambetter a financially viable option.

For those seeking alternatives to traditional insurance, UnitedHealthcare offers short-term health plans and Medicare Advantage options in New Hampshire. Short-term plans are ideal for individuals experiencing gaps in coverage, such as recent graduates or those transitioning between jobs. These plans typically last up to 12 months and cover unexpected medical expenses, though they may exclude pre-existing conditions. UnitedHealthcare’s Medicare Advantage plans, on the other hand, provide additional benefits like dental, vision, and hearing coverage, making them a comprehensive choice for seniors.

When comparing these providers, it’s essential to consider factors like network size, out-of-pocket costs, and additional benefits. Anthem’s extensive network may appeal to those who prioritize flexibility, while Harvard Pilgrim’s wellness programs are ideal for health-conscious individuals. Ambetter’s affordability makes it a strong contender for budget-conscious families, and UnitedHealthcare’s specialized plans cater to specific demographics. By evaluating these options based on personal health needs and financial circumstances, New Hampshire residents can select a plan that offers the best value and coverage.

Medicaid Insurance: Moving States, What You Need to Know

You may want to see also

Explore related products

![]()

Affordable Care Act in NH: How ACA impacts health insurance options and subsidies in the state

New Hampshire residents have seen significant changes in their health insurance landscape since the implementation of the Affordable Care Act (ACA). One of the most notable impacts is the expansion of Medicaid, which has provided coverage to thousands of low-income individuals who previously fell into the "coverage gap." Under the ACA, New Hampshire’s Medicaid program, known as NH Medicaid, now covers adults with incomes up to 138% of the federal poverty level (FPL). For a single individual in 2023, this translates to an annual income of approximately $18,754. This expansion has been a lifeline for many, reducing the uninsured rate in the state by nearly half since 2014.

For those who don’t qualify for Medicaid but still need affordable coverage, the ACA’s health insurance marketplace offers subsidized plans. Subsidies, in the form of premium tax credits, are available to individuals and families with incomes between 100% and 400% of the FPL. For example, a family of four earning up to $106,000 annually in 2023 may qualify for these credits, significantly reducing their monthly premiums. To determine eligibility, residents can use the marketplace’s online calculator, which factors in income, household size, and location. Applying during the annual open enrollment period (typically November 1 to January 15) is crucial, though special enrollment periods are available for those experiencing life changes like marriage, divorce, or job loss.

The ACA has also standardized health insurance plans in New Hampshire, categorizing them into four metal tiers: Bronze, Silver, Gold, and Platinum. Each tier offers a different balance of premiums and out-of-pocket costs. Silver plans are particularly popular because they are the only tier eligible for cost-sharing reductions (CSRs), which lower deductibles and copays for those earning up to 250% of the FPL. For instance, a Silver plan with CSRs might have a deductible of $200 instead of $6,000 for someone at 200% FPL. This makes healthcare more accessible for moderate-income individuals who might otherwise struggle with high out-of-pocket expenses.

Despite these benefits, challenges remain. New Hampshire’s individual insurance market has seen premium increases in recent years, partly due to the ACA’s elimination of cost-sharing reduction payments to insurers. However, the American Rescue Plan Act of 2021 temporarily expanded subsidies, capping premiums at 8.5% of income for benchmark plans and increasing eligibility for financial assistance. These changes have made coverage more affordable for many, but they are set to expire after 2025 unless extended by Congress. Residents should stay informed about policy changes and explore all available options, including short-term health plans or employer-sponsored insurance, to find the best fit for their needs.

In summary, the ACA has transformed health insurance in New Hampshire by expanding Medicaid, offering subsidized marketplace plans, and standardizing coverage options. While challenges like rising premiums persist, the act’s provisions have made healthcare more accessible and affordable for thousands. By understanding eligibility criteria, plan tiers, and available subsidies, residents can navigate the system effectively and secure the coverage they need.

Public School Medical Insurance: Who Chooses the Provider?

You may want to see also

Explore related products

![]()

Medicaid Expansion in NH: Eligibility and benefits of expanded Medicaid under Granite Advantage

New Hampshire's Medicaid expansion, known as the Granite Advantage program, has significantly broadened access to healthcare for low-income adults since its implementation in 2014. Under this initiative, individuals aged 19 to 64 with incomes up to 138% of the federal poverty level (FPL) are eligible for coverage. For context, in 2023, this translates to an annual income of approximately $18,754 for a single individual and $38,295 for a family of four. Eligibility is not limited to parents or pregnant individuals, as it includes childless adults, a group previously excluded from traditional Medicaid programs in many states.

To enroll in Granite Advantage, applicants must meet residency and citizenship requirements, such as being a U.S. citizen, lawful permanent resident, or qualified immigrant. The application process can be completed online through the NH Easy system, in person at a local Department of Health and Human Services office, or by phone. Once enrolled, beneficiaries are required to pay modest premiums, ranging from $0 to $20 per month, depending on income. Failure to pay premiums may result in temporary suspension of benefits, so it’s crucial to stay current with payments.

The benefits of Granite Advantage are comprehensive, covering essential health services such as preventive care, hospitalization, prescription drugs, mental health treatment, and substance use disorder services. Notably, the program includes dental and vision care for adults, which are often excluded from other Medicaid plans. For individuals struggling with opioid addiction, Granite Advantage provides access to medication-assisted treatment (MAT), including FDA-approved medications like buprenorphine and methadone. This aligns with New Hampshire’s efforts to combat the opioid crisis, offering a lifeline to those in need.

A unique feature of Granite Advantage is its emphasis on wellness incentives. Beneficiaries can earn rewards, such as reduced premiums or gift cards, by completing healthy activities like annual check-ups, flu shots, or participating in smoking cessation programs. This approach not only encourages preventive care but also empowers individuals to take an active role in their health. However, it’s important to note that these incentives are optional, and failure to participate does not affect core coverage.

Despite its benefits, Granite Advantage has faced criticism for its work and community engagement requirements, which mandate that able-bodied adults aged 19 to 64 complete at least 100 hours of work, education, or volunteer activities per month to maintain coverage. Exemptions apply to individuals with disabilities, caregivers, and those in treatment for substance use disorders. While proponents argue this promotes self-sufficiency, critics worry it may create barriers for vulnerable populations. As of 2023, New Hampshire continues to evaluate the impact of these requirements on enrollment and health outcomes.

In summary, Granite Advantage has been a game-changer for low-income adults in New Hampshire, offering robust benefits and innovative incentives while addressing critical health needs like substance use disorder. However, navigating its eligibility criteria and requirements demands attention to detail. For those who qualify, the program provides a vital pathway to affordable, comprehensive healthcare, making it a cornerstone of the state’s health insurance landscape.

Orthotics and Medical Insurance: What's Covered?

You may want to see also

Explore related products

![]()

Short-Term Health Plans: Temporary coverage options, limitations, and availability in New Hampshire

Short-term health plans in New Hampshire offer a temporary safety net for individuals facing gaps in coverage, such as those transitioning between jobs or waiting for employer-sponsored insurance to begin. These plans, typically lasting up to 12 months, provide basic medical coverage at a lower cost than traditional health insurance. However, they come with significant limitations, including exclusions for pre-existing conditions, limited provider networks, and caps on benefits. For instance, a short-term plan might cover emergency room visits but exclude prescription drugs or maternity care. Before enrolling, carefully review the policy’s terms to ensure it aligns with your immediate healthcare needs.

One of the key advantages of short-term health plans is their flexibility and accessibility. In New Hampshire, these plans are available year-round without the restrictions of open enrollment periods, making them a viable option for individuals who miss the ACA marketplace deadlines. Premiums are generally lower, often ranging from $50 to $200 per month, depending on age and coverage level. However, this affordability comes at a cost: short-term plans are not required to comply with ACA regulations, meaning they may not cover essential health benefits like mental health services or preventive care. For example, a 30-year-old in Manchester might find a short-term plan for $80/month, but it could leave them responsible for thousands in out-of-pocket costs if they require specialized treatment.

When considering a short-term health plan in New Hampshire, it’s crucial to weigh the risks against your health status and financial situation. These plans are best suited for healthy individuals who rarely require medical care and need temporary coverage. For those with chronic conditions or ongoing medical needs, the exclusions and limitations could lead to significant financial strain. Additionally, short-term plans do not satisfy the ACA’s individual mandate, meaning you may still face a tax penalty for not having qualifying coverage. To mitigate risks, pair a short-term plan with a health savings account (HSA) or supplemental insurance, such as accident or critical illness coverage, to address potential gaps.

Availability of short-term health plans in New Hampshire is widespread, with several insurers offering these products. Companies like UnitedHealthcare and National General provide options tailored to different budgets and coverage needs. However, the state’s regulatory environment is less restrictive than in some other states, allowing insurers to offer plans with fewer consumer protections. To find the best option, use online comparison tools or consult a licensed insurance broker who can help navigate the nuances of each plan. For instance, a broker might highlight a plan with a $5,000 deductible but robust emergency coverage, ideal for someone seeking catastrophic protection without long-term commitments.

In conclusion, short-term health plans in New Hampshire serve as a temporary solution for those in need of immediate coverage but come with trade-offs that require careful consideration. While they offer affordability and flexibility, their limitations make them unsuitable for everyone. By understanding the specifics of these plans—from exclusions to premiums—individuals can make informed decisions that balance cost and coverage. Always read the fine print and consider your long-term health needs before committing to a short-term plan.

Top Health Insurance Providers: Who Leads the Industry in 2023?

You may want to see also

Explore related products

![]()

NH Health Insurance Costs: Average premiums, deductibles, and factors affecting plan prices

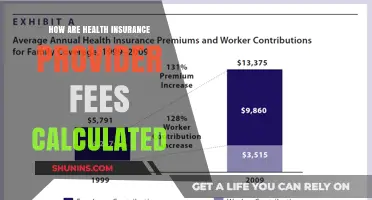

New Hampshire residents face a complex landscape when it comes to health insurance costs, with premiums and deductibles varying widely based on several key factors. Understanding these elements is crucial for anyone looking to navigate the state’s health insurance market effectively. On average, New Hampshire’s monthly premiums for individual health plans hover around $500, though this figure can fluctuate significantly depending on the plan type, insurer, and coverage level. For families, the average monthly premium can exceed $1,500, making it essential to weigh the costs against the benefits offered. Deductibles, another critical component, typically range from $1,000 to $6,000 annually, with higher deductibles often correlating with lower monthly premiums.

Several factors influence the price of health insurance plans in New Hampshire. Age is a primary determinant, as older individuals generally face higher premiums due to increased health risks. For example, a 40-year-old in Manchester might pay 20% more than a 25-year-old for the same plan. Location within the state also plays a role, with urban areas like Nashua or Portsmouth often having higher costs compared to rural regions. Lifestyle choices, such as smoking, can add a surcharge of up to 50% to premiums. Additionally, the metal tier of a plan—Bronze, Silver, Gold, or Platinum—directly impacts costs, with Bronze plans offering lower premiums but higher out-of-pocket costs, while Platinum plans provide comprehensive coverage at a steeper price.

To manage these costs, New Hampshire residents can take advantage of subsidies through the Affordable Care Act (ACA) marketplace. For instance, a family of four earning up to $106,000 annually may qualify for premium tax credits, significantly reducing their monthly expenses. Another strategy is to compare plans during the annual Open Enrollment Period, typically from November 1 to January 15, to find the best balance between premiums and deductibles. High-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs) can also be a cost-effective option for those with fewer health needs, allowing them to save pre-tax dollars for medical expenses.

When evaluating deductibles, it’s important to consider not just the upfront cost but also the potential long-term savings. For example, a plan with a $2,000 deductible and a $400 monthly premium might be more affordable than a $1,000 deductible plan with a $600 premium if you rarely require medical services. Conversely, individuals with chronic conditions or frequent healthcare needs may benefit from lower deductibles despite higher premiums. Tools like the NH Insurance Department’s rate review process can help consumers understand how insurers justify their pricing, ensuring transparency in the market.

In conclusion, navigating New Hampshire’s health insurance costs requires a strategic approach. By understanding average premiums, deductibles, and the factors that influence pricing, residents can make informed decisions tailored to their financial and health needs. Whether leveraging subsidies, comparing plans, or opting for an HDHP, the goal is to find a balance that provides adequate coverage without breaking the bank. With careful planning and research, securing affordable and comprehensive health insurance in New Hampshire is well within reach.

Medical Insurance: Cheaper to Go Solo?

You may want to see also

Frequently asked questions

In New Hampshire, the main types of health insurance plans include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Exclusive Provider Organizations (EPOs), and High-Deductible Health Plans (HDHPs) with Health Savings Accounts (HSAs).

You can enroll in a health insurance plan in New Hampshire through the Health Insurance Marketplace (Healthcare.gov) during the Open Enrollment Period, or qualify for a Special Enrollment Period if you experience a life event like marriage, birth, or loss of coverage.

Yes, New Hampshire offers Medicaid (known as NH Medicaid) and the Children’s Health Insurance Program (CHIP) for eligible low-income individuals and families. Additionally, the state has expanded Medicaid under the Affordable Care Act.

The average cost of health insurance in New Hampshire varies based on factors like age, plan type, and coverage level. As of recent data, premiums range from $400 to $800 per month for individual plans, with subsidies available for eligible individuals through the Marketplace.

It depends on your plan. Some out-of-state plans may not provide coverage in New Hampshire, especially if they are not compliant with the state’s insurance regulations. It’s best to check with your insurer or consider enrolling in a New Hampshire-based plan.

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)