Navigating access to health insurance can be an overwhelming and complex process, often leaving individuals feeling frustrated and confused. With a myriad of plans, providers, and policies to choose from, understanding the intricacies of health insurance coverage is no easy feat. The system is riddled with jargon, fine print, and varying levels of coverage, making it challenging for people to determine what they truly need and what they can afford. This complexity is further exacerbated by the constant changes in healthcare policies, leaving many unsure of their rights and options. As a result, accessing adequate health insurance becomes a daunting task, particularly for those with limited resources or knowledge, ultimately impacting their ability to receive necessary medical care.

Explore related products

What You'll Learn

- Complex Eligibility Criteria: Varying rules across plans and providers make qualification confusing and difficult

- High Costs: Premiums, deductibles, and copays often render insurance unaffordable for many individuals

- Limited Provider Networks: Narrow networks restrict access to preferred doctors and specialists

- Bureaucratic Red Tape: Lengthy paperwork and approval processes delay or deny necessary care

- Lack of Transparency: Hidden fees and unclear coverage terms make informed decisions challenging

![]()

Complex Eligibility Criteria: Varying rules across plans and providers make qualification confusing and difficult

One of the most daunting aspects of securing health insurance is deciphering the labyrinthine eligibility criteria that differ wildly across plans and providers. For instance, while Plan A might require applicants to meet specific income thresholds, Plan B could prioritize age brackets or pre-existing conditions. This patchwork of rules forces individuals to become amateur detectives, scouring policy documents for hidden clauses that could disqualify them. Imagine a 35-year-old freelancer earning $40,000 annually—they might qualify for a state-run plan but be ineligible for employer-sponsored insurance due to their part-time status. Such inconsistencies create a frustrating maze where even the most diligent applicants can get lost.

Consider the case of Medicaid, where eligibility varies drastically by state. In Texas, for example, adults without children are often excluded unless they meet stringent disability criteria, while New York offers broader coverage under its Medicaid expansion. These disparities mean that a person’s ability to access care can hinge on their zip code rather than their medical need. Similarly, private insurers often impose waiting periods or exclude coverage for certain conditions, such as mental health or maternity care, unless the applicant has been insured for a minimum of six months. Such fine print turns what should be a straightforward process into a minefield of potential rejections.

To navigate this complexity, start by identifying your key demographics: age, income, employment status, and health conditions. Use online tools like Healthcare.gov’s eligibility calculator to narrow down options based on your state and financial situation. For example, if you’re under 30 and healthy, a catastrophic plan might offer lower premiums but higher out-of-pocket costs. Conversely, families with chronic illnesses should prioritize plans with robust prescription drug coverage. Always verify provider networks—a plan with low premiums may exclude your preferred doctors or hospitals, rendering it less practical.

A cautionary tale: relying solely on insurance brokers or provider websites can lead to oversights. Brokers may push plans with higher commissions, while provider sites often oversimplify eligibility rules. Instead, cross-reference information with state health departments or nonprofit advocacy groups like the Kaiser Family Foundation. Keep a checklist of required documents, such as tax returns, pay stubs, and medical records, to streamline the application process. If denied, don’t despair—appeal the decision with specific evidence of why you meet the criteria.

Ultimately, the complexity of eligibility criteria underscores the need for systemic reform. Until then, arm yourself with knowledge, patience, and persistence. Treat the process as a puzzle rather than a barrier, and remember that securing the right coverage is worth the effort. By understanding the nuances of each plan and provider, you can turn confusion into clarity and ensure access to the care you deserve.

Travel Insurance: Understanding Pre-Existing Medical Conditions

You may want to see also

Explore related products

![]()

High Costs: Premiums, deductibles, and copays often render insurance unaffordable for many individuals

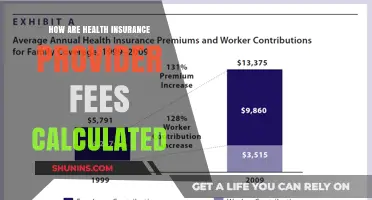

Health insurance is often touted as a safeguard against financial ruin in the face of medical emergencies, yet for many, the very costs associated with it create a barrier to access. Premiums, the monthly fees paid to maintain coverage, can be prohibitively expensive, especially for low-income individuals and families. For instance, in the United States, the average annual premium for employer-sponsored family coverage exceeded $21,000 in 2021, with employees contributing over $5,500 of that amount. For someone earning minimum wage, this represents nearly 40% of their annual income, leaving little room for other essentials like rent, food, and transportation.

Consider the case of a 35-year-old single parent working part-time at a retail job. Earning $15 per hour, they bring home approximately $24,000 annually. If their employer offers health insurance with a monthly premium of $300, that’s $3,600 per year—15% of their income. Even if they opt for a lower-tier plan with a $200 monthly premium, the $2,400 annual cost still strains their budget. Add to this the burden of deductibles, the amount paid out-of-pocket before insurance kicks in, and the situation becomes dire. A typical deductible for an individual can range from $1,000 to $5,000, depending on the plan. For someone living paycheck to paycheck, saving for such expenses is nearly impossible.

The complexity deepens with copays, the fixed amounts paid for each doctor’s visit or prescription. While seemingly minor—$20 for a primary care visit, $50 for a specialist—these costs accumulate quickly. A chronic condition requiring monthly specialist visits and medications can easily add up to $1,200 annually in copays alone. For families, these costs multiply. A parent with two children, each needing regular pediatric care, could face $2,000 or more in copays yearly. This financial strain forces many to delay or forgo necessary care, exacerbating health issues and leading to more costly treatments down the line.

To navigate this challenge, individuals must adopt strategic planning. First, evaluate all available options, including employer-sponsored plans, marketplace plans, and government programs like Medicaid. Use online calculators to estimate total annual costs, factoring in premiums, deductibles, and expected copays. For those with predictable medical needs, high-deductible plans paired with health savings accounts (HSAs) can offer tax advantages and flexibility. However, this approach requires disciplined saving, which may not be feasible for everyone. Advocacy is also crucial: push for policy changes that cap out-of-pocket costs and expand subsidies for low-income individuals.

Ultimately, the high costs of health insurance premiums, deductibles, and copays create a paradox: the very tool meant to ensure access to care becomes inaccessible for those who need it most. Without systemic reforms, millions will continue to face impossible choices between financial stability and their health. Until then, individuals must arm themselves with knowledge, creativity, and persistence to navigate this flawed system.

Top Health Insurance Providers in the USA: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Limited Provider Networks: Narrow networks restrict access to preferred doctors and specialists

Health insurance plans with limited provider networks can force patients into a frustrating game of musical chairs, where finding an in-network specialist feels like winning the lottery. Imagine needing a neurologist for chronic migraines, only to discover your plan covers exactly two in your area—both with wait times stretching into months. This scenario isn’t uncommon; narrow networks often prioritize cost-cutting over patient choice, leaving individuals scrambling to find providers who accept their insurance while also meeting their medical needs.

The problem deepens when considering the ripple effects of these restrictions. For instance, a patient with a rare autoimmune disorder might require a rheumatologist with specific expertise. If that specialist isn’t in-network, the patient faces a stark choice: pay out-of-pocket costs that can run into thousands of dollars or settle for a less experienced provider. This isn’t just inconvenient—it’s a barrier to quality care, particularly for those with complex or chronic conditions. Even routine care suffers; a primary care physician in-network might refer you to a specialist who isn’t, creating a bureaucratic maze that delays treatment and exacerbates health issues.

To navigate this challenge, patients must become savvy advocates for their own care. Start by scrutinizing your plan’s provider directory before enrolling, cross-referencing it with your current doctors and any specialists you anticipate needing. If you’re already locked into a narrow network, call your insurance company to request an exception for out-of-network providers, especially if in-network options are inadequate. Document all communications, and don’t hesitate to appeal denials—many patients succeed on appeal when they demonstrate a lack of in-network alternatives.

Comparatively, broader networks offer flexibility but often come with higher premiums, leaving consumers to weigh cost against convenience. For those on limited budgets, narrow networks might seem like the only affordable option, but the hidden costs—delayed care, increased complications, and out-of-pocket expenses—can offset the savings. Employers and policymakers play a role here too; pushing for more transparent network information and advocating for expanded provider lists can help alleviate this burden. Until then, patients must tread carefully, balancing financial constraints with the need for accessible, quality care.

Unemployed and Uninsured: Getting Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Bureaucratic Red Tape: Lengthy paperwork and approval processes delay or deny necessary care

Navigating the labyrinth of health insurance often feels like deciphering an ancient script, but with higher stakes. Bureaucratic red tape—endless forms, convoluted approval processes, and opaque requirements—transforms a lifeline into a hurdle race. Consider this: a 2020 study found that 25% of denied claims were due to administrative errors, not medical ineligibility. For patients, this means weeks or months of delays, during which conditions worsen, treatments are foregone, and stress compounds. A diabetic patient, for instance, might wait 45 days for insulin approval, risking complications like diabetic ketoacidosis, which requires hospitalization and costs $10,000 on average. The irony? The system designed to protect health often undermines it.

Let’s break down the process. Step one: pre-authorization. Your doctor prescribes a medication or procedure, but before proceeding, the insurer demands proof of "medical necessity." This involves submitting detailed medical records, often requiring multiple phone calls and faxes—a relic of the 1990s in a digital age. Step two: waiting. Insurers have 15 to 30 days to respond, but internal backlogs stretch this to 60 days or more. Step three: denial. If rejected, you appeal, a process that takes another 30 to 60 days. For a 65-year-old with heart disease needing a stent, this delay can be catastrophic. Practical tip: keep a log of all communications, including dates, names, and reference numbers. This documentation is your lifeline during appeals.

Now, compare this to systems with streamlined processes. In Germany, for example, health insurers are legally required to respond to pre-authorization requests within three days. The result? Faster access to care and lower administrative costs. In the U.S., however, profit motives often incentivize delays. Insurers save billions annually by slow-walking approvals, betting patients will abandon claims out of frustration. This isn’t speculation—a 2019 report found that 68% of denied claims were overturned on appeal, revealing denials as a tactic, not a necessity. The takeaway? The system is rigged against patients, prioritizing paperwork over people.

Here’s a persuasive argument: bureaucratic red tape isn’t just inefficient—it’s immoral. Imagine a parent whose child needs chemotherapy but is stuck in approval limbo. Each day wasted is a day lost in the fight against cancer. For low-income families, the stakes are even higher. A denied claim can mean choosing between medical debt and bankruptcy. Advocates argue for policy reforms like standardized approval timelines and penalties for unjustified delays. Until then, patients must become their own advocates, armed with knowledge and persistence. Start by understanding your policy’s fine print, use patient advocacy services, and don’t hesitate to escalate denials to state regulators. The system may be broken, but you don’t have to be its victim.

Finally, consider the human cost. Behind every denied claim is a person in pain, a family in distress. Take Maria, a 42-year-old teacher with rheumatoid arthritis, whose insurer denied coverage for a biologic medication. The alternative? Corticosteroids, which caused weight gain, mood swings, and osteoporosis. After a three-month appeal, she won approval—but at what cost? Her condition had worsened, requiring physical therapy and additional medications. This isn’t an isolated case. Multiply Maria’s story by millions, and you see a system failing its purpose. Bureaucratic red tape doesn’t just delay care—it denies dignity. Until we demand change, the paperwork will continue to pile up, one life at a time.

Rising Demand for Health Insurance Agents: Trends and Opportunities

You may want to see also

Explore related products

![]()

Lack of Transparency: Hidden fees and unclear coverage terms make informed decisions challenging

Hidden fees and ambiguous coverage terms are a pervasive issue in health insurance, turning what should be a straightforward process into a labyrinth of confusion. Consider this: a 45-year-old individual with a chronic condition might select a plan based on its advertised low monthly premium, only to discover later that their specific medications are subject to a high coinsurance rate, effectively doubling their out-of-pocket costs. This lack of transparency not only undermines trust but also forces consumers to make decisions based on incomplete information, often leading to financial strain and inadequate coverage.

To navigate this complexity, start by scrutinizing the Summary of Benefits and Coverage (SBC) document provided by insurers. While it’s legally required to outline key features, many consumers overlook it due to its dense language. For instance, terms like "out-of-network cost-sharing" or "maximum out-of-pocket limit" are rarely explained in plain English. A practical tip: use online tools like Healthcare.gov’s glossary to decode these terms. Additionally, ask insurers directly about specific scenarios, such as "What would my total cost be for a specialist visit if the provider is out-of-network?" to uncover hidden fees.

The problem extends beyond individual plans to systemic issues. A 2022 study found that 60% of consumers struggled to understand their health insurance costs, with hidden fees like "facility fees" or "provider-based billing" adding hundreds of dollars to unexpected bills. For example, a routine blood test in a hospital-affiliated clinic might incur a facility fee, even if the service is identical to an independent lab. Such practices highlight the need for regulatory reforms that mandate clearer fee structures and standardized terminology across insurers.

From a comparative perspective, countries with single-payer systems, like Canada or the UK, demonstrate how transparency can be achieved. In these systems, coverage terms are standardized, and out-of-pocket costs are minimal, eliminating the guesswork for consumers. While a single-payer model may not be feasible in the U.S. context, adopting elements of transparency from these systems—such as requiring insurers to provide personalized cost estimators for common procedures—could significantly improve consumer experience.

In conclusion, addressing the lack of transparency in health insurance requires both individual vigilance and systemic change. Consumers must proactively decode plan documents and ask pointed questions, while policymakers should push for reforms that standardize terminology and mandate clear fee disclosures. Until then, the burden of navigating hidden fees and unclear terms will continue to fall on individuals, perpetuating a cycle of confusion and financial insecurity.

Hotel Management Companies: Ensuring Comprehensive Insurance Responsibility for All

You may want to see also

Frequently asked questions

Health insurance plans often use complex terminology, varying coverage details, and multiple tiers (e.g., bronze, silver, gold), making it hard for individuals to compare and choose the best option for their needs.

High premiums, deductibles, and out-of-pocket costs can make health insurance unaffordable for many, especially low-income individuals or those without employer-sponsored plans.

Many insurance providers do not clearly disclose costs, coverage limits, or network restrictions, leaving consumers confused and unable to make informed decisions.

Enrollment often requires navigating multiple platforms, understanding eligibility criteria, and dealing with strict deadlines, which can be overwhelming and time-consuming for individuals.