The accuracy of health insurance marketplace rates is a critical concern for consumers, as it directly impacts affordability and coverage decisions. These rates are determined by a complex interplay of factors, including age, location, income, and the level of coverage chosen, with insurers using actuarial data to predict healthcare costs. While regulatory bodies like the Centers for Medicare & Medicaid Services (CMS) oversee rate submissions to ensure compliance with the Affordable Care Act (ACA), variations in pricing can still occur due to differences in provider networks, prescription drug coverage, and regional healthcare costs. Additionally, annual rate adjustments reflect changing medical trends, inflation, and policyholder claims experience, making it essential for consumers to review and compare plans regularly to ensure they are getting the best value. Despite these efforts, the accuracy of marketplace rates remains a dynamic issue, influenced by both market forces and legislative changes, underscoring the need for transparency and informed decision-making.

Explore related products

What You'll Learn

![]()

Factors influencing rate calculations

Health insurance marketplace rates are not arbitrary numbers but the result of complex calculations influenced by a myriad of factors. Understanding these factors can help consumers make informed decisions and anticipate changes in their premiums. One of the primary determinants is age, as older individuals generally face higher rates due to increased health risks and medical needs. For instance, a 60-year-old might pay three times more than a 21-year-old for the same plan, as outlined by the Affordable Care Act’s age rating rules, which allow insurers to charge older adults up to three times more than younger ones.

Location plays a pivotal role in rate calculations, as healthcare costs vary significantly by region. Urban areas with higher living costs and more expensive medical services often see higher premiums compared to rural regions. For example, a silver-level plan in Alaska might cost twice as much as a similar plan in Minnesota due to differences in provider fees, state regulations, and local market competition. Additionally, states with mandated benefits, such as coverage for specific treatments or providers, tend to have higher average premiums.

Another critical factor is tobacco use, which can increase premiums by up to 50% in states that allow tobacco surcharges. Insurers view smokers as high-risk due to the increased likelihood of chronic illnesses like heart disease or cancer. For a 40-year-old nonsmoker, a monthly premium might be $400, while a smoker of the same age could pay $600 for the same coverage. Quitting smoking not only improves health but can also lead to significant savings on health insurance premiums.

The metal tier of a plan—Bronze, Silver, Gold, or Platinum—directly impacts rates, with higher tiers offering more comprehensive coverage but at a steeper cost. For example, a Bronze plan might cover 60% of healthcare costs with a lower premium, while a Gold plan covers 80% but costs substantially more. Consumers must balance their budget with their expected healthcare needs, as choosing a lower-tier plan to save on premiums could result in higher out-of-pocket costs if extensive medical care is needed.

Lastly, income level affects rates through subsidies available to those earning between 100% and 400% of the federal poverty level. For instance, a family of four earning $100,000 annually might qualify for a premium tax credit, reducing their monthly payment by hundreds of dollars. These subsidies are calculated based on the benchmark Silver plan in the consumer’s area, making it essential to estimate income accurately when applying for coverage to maximize savings. Understanding these factors empowers consumers to navigate the marketplace effectively and secure the most accurate and affordable rates.

Applying for Medicaid Insurance in Indiana: A Guide

You may want to see also

Explore related products

![]()

Role of age and location in premiums

Age and location are two of the most significant factors influencing health insurance premiums on the marketplace, often determining the affordability and accessibility of coverage for individuals and families. These variables are not arbitrary; they are rooted in actuarial data that insurers use to predict healthcare costs. For instance, younger individuals typically face lower premiums because they are statistically less likely to require extensive medical services. Conversely, older adults, particularly those over 50, can expect premiums to increase substantially due to higher healthcare utilization rates. The Affordable Care Act (ACA) allows insurers to charge older enrollees up to three times more than younger ones, a ratio that directly impacts affordability for aging populations.

Location plays an equally critical role, as healthcare costs vary dramatically by region. Premiums in urban areas like New York City or San Francisco are often higher due to elevated medical service costs and a higher concentration of specialists. In contrast, rural areas may have lower premiums but limited provider networks, which can reduce the value of coverage. State-specific regulations also influence rates; for example, states with robust insurance mandates may have higher premiums but offer more comprehensive benefits. Geographic rating areas, defined by the ACA, further segment markets, ensuring that even neighboring counties can have significantly different premium structures.

The interplay between age and location creates unique challenges for certain demographics. A 60-year-old in Miami, for instance, might face premiums exceeding $1,200 monthly, while a 25-year-old in the same city could pay as little as $300. Subsidies through the ACA can mitigate these disparities, but eligibility depends on income and family size, leaving some individuals in high-cost areas with limited options. Practical tips for navigating these variations include using the marketplace’s subsidy calculator, exploring Medicaid eligibility in states that have expanded coverage, and considering health savings accounts (HSAs) to offset out-of-pocket costs.

To illustrate, a comparative analysis of premiums across age groups and locations reveals stark differences. In 2023, a 40-year-old in Wyoming paid an average of $450 monthly for a silver plan, while a peer in Alaska paid over $800 for similar coverage. Age-based increases compound these disparities; a 60-year-old in Wyoming faced premiums of $1,100, compared to $1,800 in Alaska. These examples underscore the importance of researching local markets and understanding how age-based pricing affects individual budgets.

In conclusion, while age and location are non-negotiable factors in premium calculations, consumers can take proactive steps to manage costs. Shopping during open enrollment, comparing plans annually, and leveraging available subsidies are essential strategies. Additionally, advocating for policy changes that address age-based pricing disparities or regional cost variations could lead to more equitable marketplace rates in the future. Understanding these dynamics empowers individuals to make informed decisions in an often complex insurance landscape.

Become a California Health Insurance Agent: Step-by-Step Guide

You may want to see also

Explore related products

![]()

Impact of health status on costs

Health insurance marketplace rates are often presented as standardized premiums, but they can vary significantly based on an individual's health status. This variability stems from the fact that insurers assess risk differently for each applicant, factoring in pre-existing conditions, lifestyle, and medical history. For instance, a 45-year-old with hypertension and diabetes may face premiums 30-50% higher than a healthy peer, even for the same plan. This disparity highlights the critical role health status plays in determining costs, making it essential for consumers to understand how their medical profile influences what they pay.

Consider the impact of chronic conditions on insurance rates. Conditions like asthma, arthritis, or heart disease require ongoing management, including regular doctor visits, medications, and diagnostic tests. Insurers account for these anticipated expenses by adjusting premiums upward. For example, a person with uncontrolled asthma requiring monthly specialist visits and daily inhalers (e.g., Advair at $300/month) will likely incur higher costs than someone without such needs. To mitigate this, individuals can explore plans with lower deductibles but higher monthly premiums if they anticipate frequent medical care, balancing immediate out-of-pocket costs with long-term expenses.

Age and health status often intersect to amplify insurance costs. As individuals age, the likelihood of developing chronic conditions increases, leading to higher premiums. For example, a 60-year-old with high cholesterol and obesity might pay twice as much as a 30-year-old in excellent health. However, preventive measures can offset some of these costs. Adopting a healthier lifestyle—such as reducing salt intake to below 2,300 mg/day, exercising 150 minutes weekly, and quitting smoking—can lower the risk of chronic diseases, potentially reducing insurance costs over time. Insurers may reward such efforts through wellness programs or premium discounts.

The accuracy of marketplace rates also depends on how transparently health status is disclosed. Inaccurate or incomplete information during enrollment can lead to underestimating costs. For instance, failing to disclose a recent cancer diagnosis might result in lower initial premiums, but insurers may deny coverage for related treatments later, leaving the individual with unexpected bills. To avoid this, applicants should meticulously review their medical history and consult with healthcare providers to ensure all relevant conditions are reported. This transparency ensures rates reflect true health risks, preventing financial surprises down the line.

Finally, understanding the impact of health status on costs empowers consumers to make informed decisions. Tools like the Health Insurance Marketplace’s subsidy calculator can estimate premiums based on income and health needs, but individuals must also consider their medical profile. For those with significant health concerns, plans with robust coverage for specialist visits, prescriptions, and preventive care may offer better value despite higher premiums. Conversely, healthier individuals might opt for high-deductible plans with lower monthly costs, paired with a health savings account (HSA) to cover unexpected expenses. By aligning plan choice with health status, consumers can optimize both coverage and affordability.

Medical Insurance: Understanding Your Lifetime Benefits Cap

You may want to see also

Explore related products

![]()

Subsidy eligibility and rate reductions

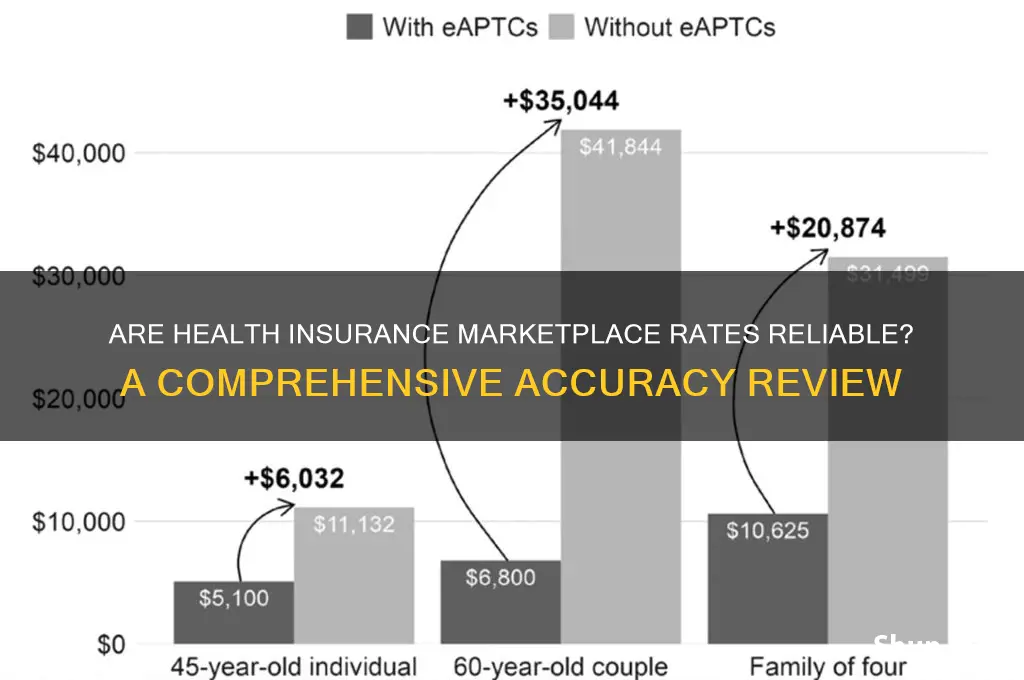

Health insurance marketplace rates are often adjusted through subsidies, which can significantly reduce premiums for eligible individuals and families. Understanding subsidy eligibility is crucial for maximizing affordability, as these reductions are directly tied to income and household size. For instance, in 2023, individuals earning up to $58,344 or a family of four earning up to $120,060 may qualify for premium tax credits under the Affordable Care Act (ACA). These credits are applied directly to monthly premiums, often lowering costs by hundreds of dollars annually.

To determine subsidy eligibility, the marketplace compares your household income to the Federal Poverty Level (FPL). For example, if your income falls between 100% and 400% of the FPL, you’re likely eligible for subsidies. However, eligibility isn’t solely income-based; factors like citizenship status, access to employer-sponsored insurance, and state of residence also play a role. For instance, in states that expanded Medicaid, the eligibility threshold for subsidies starts at incomes above 138% of the FPL, whereas non-expansion states begin at 100% FPL.

A practical tip for maximizing subsidy benefits is to update your income information annually during open enrollment. Life changes—such as a job loss, marriage, or the birth of a child—can alter your eligibility, potentially increasing your subsidy amount. Additionally, the American Rescue Plan Act (ARPA) temporarily expanded subsidies through 2025, capping premiums at 8.5% of income for all eligible enrollees, regardless of income level. This means even higher earners may qualify for reduced rates, making it essential to reevaluate your eligibility each year.

One common misconception is that subsidies only benefit low-income individuals. In reality, middle-income households often see substantial rate reductions. For example, a 45-year-old earning $60,000 annually might pay $400 monthly for a benchmark plan without subsidies but only $200 with them. To ensure accuracy, use the marketplace’s subsidy calculator during enrollment, inputting precise income and household details. This tool provides a real-time estimate of your potential savings, helping you select the most cost-effective plan.

Finally, while subsidies reduce premiums, they don’t always lower out-of-pocket costs like deductibles or copays. For comprehensive savings, consider pairing a subsidized plan with a cost-sharing reduction (CSR) subsidy if your income is below 250% of the FPL. CSRs reduce out-of-pocket expenses for silver-tier plans, making healthcare more affordable overall. By understanding both subsidy eligibility and additional reductions, you can navigate the marketplace with confidence, ensuring rates align with your financial needs.

Understanding Primary Insurance: Medicare vs. ChampVA

You may want to see also

Explore related products

![]()

Comparison of metal plan pricing tiers

Health insurance marketplace rates are often scrutinized for their accuracy, but one critical aspect that demands attention is the comparison of metal plan pricing tiers. These tiers—Bronze, Silver, Gold, and Platinum—are designed to categorize plans based on cost-sharing and premiums, yet their pricing accuracy can vary significantly. Understanding these differences is essential for consumers aiming to balance affordability with coverage.

Consider the Bronze plan, typically the most affordable in terms of monthly premiums but with higher out-of-pocket costs. For a healthy 30-year-old, a Bronze plan might offer premiums as low as $250 per month, but the deductible could exceed $7,000. This tier is ideal for those who rarely visit the doctor and want to minimize monthly expenses. However, its accuracy in reflecting actual healthcare costs can be questionable, as unexpected medical needs could lead to substantial out-of-pocket expenses.

In contrast, Silver plans strike a middle ground, often attracting subsidies for eligible individuals. Premiums for a Silver plan might range from $350 to $500 per month, with deductibles around $4,000. This tier is particularly appealing for those with moderate healthcare needs, as it balances premiums and out-of-pocket costs more effectively. For instance, a family of four with an income of $70,000 might qualify for cost-sharing reductions, making Silver plans more accurate in predicting overall healthcare expenses.

Gold and Platinum plans, while more expensive in premiums—often $600 to $1,000 per month—offer lower deductibles, typically under $2,000. These tiers are accurate for individuals with chronic conditions or frequent medical needs, as they minimize out-of-pocket costs. For example, a 55-year-old with diabetes might find a Gold plan more cost-effective in the long run, despite higher monthly premiums, due to reduced copays and coinsurance.

When comparing these tiers, it’s crucial to evaluate your healthcare usage patterns. A persuasive argument for Bronze plans might appeal to the young and healthy, but a descriptive analysis of Gold plans highlights their value for those with ongoing medical needs. Practical tips include using the marketplace’s estimation tools to predict annual costs and considering potential subsidies. Ultimately, the accuracy of metal plan pricing tiers lies in aligning your choice with your health needs and financial situation.

Top Medicare Insurance Providers: Who Offers the Best Coverage?

You may want to see also

Frequently asked questions

The rates displayed on Healthcare.gov are based on the information you provide, such as age, location, and income. They are generally accurate but may vary slightly depending on final verification of details like income and household size.

Yes, rates can change if there are updates to your income, household size, or other eligibility factors during the coverage year. Premiums may also adjust annually based on market trends.

No, under the Affordable Care Act (ACA), insurers cannot charge higher rates based on pre-existing conditions. The rates you see are standardized for your age and location.

Subsidies (premium tax credits) are calculated based on your income and the cost of benchmark plans. The rates you see after applying subsidies are accurate for your financial situation, assuming your income information is correct.

The rates shown typically include premiums but may not reflect additional costs like deductibles, copays, or coinsurance. Review plan details carefully to understand the full cost of coverage.