Getting car insurance is a relatively straightforward process. It involves gathering information about yourself and your vehicle, choosing the type and amount of coverage you need, and comparing quotes from different companies before buying a policy.

You'll need to provide basic personal details, such as your name, address, date of birth, and driver's license information. Additionally, you'll need to know specific information about your vehicle, including the make, model, vehicle identification number, safety features, and annual mileage. It's also helpful to have your current insurance information, if you have it, as well as details about your driving history, such as accidents or violations.

Once you have this information, you can start comparing quotes from different insurance companies. It's important to ensure that you're comparing similar coverage types and amounts to get an accurate idea of the cost. You can do this by using online comparison tools, contacting companies directly, or working with an insurance agent or broker.

After deciding on the company and coverage that best suits your needs, you can purchase your policy. It's important to ensure that your new policy is active before cancelling your old one to avoid any lapse in coverage.

| Characteristics | Values |

|---|---|

| Driver's information | Name, address, date of birth, driver's license number, driving history, social security number |

| Vehicle information | Make, model, vehicle identification number, safety features, odometer reading, annual mileage, year |

| Coverage options | Liability, collision, comprehensive, uninsured/underinsured motorist, medical payments, personal injury protection, roadside assistance, rental reimbursement, gap insurance, accident forgiveness |

| Policy purchase | Online, phone, independent agent/broker, captive agent, specialty agency |

| Payment methods | Monthly, upfront (discounted) |

Explore related products

What You'll Learn

![]()

What information do I need to get a quote?

To get a car insurance quote, you will need to provide some personal information, as well as details about your vehicle and driving history. Here is a list of the information you will typically need to provide:

- Basic personal details: name, address, date of birth, and Social Security number (optional).

- Driver's license information: driver's license number and driving history, including any accidents, tickets, or violations.

- Vehicle information: make, model, year, vehicle identification number (VIN), safety features, current odometer reading, and annual mileage.

- Current insurance information (if applicable): the name of your current insurance company and your current coverage limits.

Having this information ready will help speed up the process of getting a car insurance quote and ensure that you receive an accurate quote that meets your needs.

In addition to the above, some insurance providers may also ask about the physical address where your vehicle is stored and whether there are any other drivers who will be using your vehicle. It is also worth noting that while some providers will require your Social Security number, others may not.

College Students' Guide to Unlocking Affordable Auto Insurance Rates

You may want to see also

Explore related products

![]()

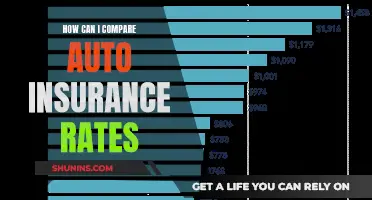

How do I compare quotes?

Comparing quotes from different auto insurance companies is a crucial step in finding the best value for your needs. Here are some detailed steps to help you compare quotes effectively:

Standardize the Coverage Details:

When comparing quotes, ensure that you select the same coverage types and amounts for each quote. This includes standard coverages such as liability, uninsured motorist, comprehensive, and collision insurance. By standardizing the coverage, you can accurately assess the cost differences between insurers.

Policy Limits and Deductibles:

Policy limits refer to the maximum amount an insurer will pay out for a covered loss. When comparing quotes, ensure that the policy limits for each coverage type are the same across all quotes. Additionally, consider the deductible amount you are comfortable with. The deductible is the portion you will have to pay out of pocket before the insurance company covers the rest. A higher deductible can lower your insurance bill, but make sure it is an amount you can afford to pay if needed.

Discounts and Special Offers:

Different insurers offer various discounts, so it's essential to explore these when comparing quotes. Common discounts include those for students, federal employees, members of the armed forces, bundling policies, or having safety features in your vehicle. When obtaining quotes, provide detailed information about yourself and your vehicle to identify all the discounts you may be eligible for.

Compare Rates Using Tools:

Take advantage of online comparison tools and rate calculators offered by insurance companies and third-party websites. These tools allow you to input your information once and quickly generate quotes from multiple insurers, making it easier to compare rates and coverages side by side.

Research Insurers' Reputation:

While cost is an important factor, it's not the only consideration. Research the reputation of the insurance companies you're comparing. Look into their customer service, claims handling process, customer satisfaction ratings, and financial stability. Choosing a reputable company with a history of fair claims handling will give you peace of mind and ensure a smoother experience if you ever need to file a claim.

By following these steps, you'll be able to compare auto insurance quotes effectively and make an informed decision about which policy offers the best value and protection for your specific needs.

Amica Auto Insurance: Good or Bad?

You may want to see also

Explore related products

![]()

What are the different types of coverage?

There are several types of car insurance coverage, and not all of them are mandatory. The type of coverage you need depends on your state's laws, the age and value of your car, and your financial situation. Here are the most common types of coverage:

Required Coverage

Although it varies by state, most states require drivers to carry liability coverage, including bodily injury liability and property damage liability. Liability coverage protects you financially if you are found at fault in an accident by covering the cost of damages to another person's property or for their medical expenses. This coverage is typically written as split limits, with a maximum payout per person and a maximum total payout per accident.

Some states also require drivers to carry first-party medical coverage, such as personal injury protection (PIP) or medical payments coverage (MedPay), and/or uninsured/underinsured motorist coverage. PIP covers medical bills for you, your family, or your passengers, regardless of who was at fault in the accident. It may also cover lost wages and necessary expenses like childcare. MedPay is similar but is only required in a few states and does not cover lost wages.

Optional Coverage

Collision and comprehensive insurance are the two primary types of physical damage coverage and are optional in every state. However, they may be required by lenders or leasing companies if you are financing or leasing your vehicle. Collision coverage pays for damage to your vehicle regardless of who is at fault in an accident, while comprehensive coverage pays for damage to your car from something other than a collision, such as theft, vandalism, or natural disasters. Both types of coverage typically come with deductibles, which is the amount you must pay out of pocket before your insurance company covers the rest.

Other optional coverage types include:

- Roadside assistance: Covers towing, flat tires, battery jumpstarts, and locksmith services.

- Rental car reimbursement: Covers the cost of a rental car while your vehicle is being repaired.

- New car replacement coverage: Pays for a brand-new car if your vehicle is totaled and is only a few years old or under a certain mileage.

- Full glass coverage: Pays to repair or replace chipped or broken window glass.

- Rideshare insurance: Covers you when driving for a rideshare company, as most only provide coverage when you have a passenger.

- Mechanical breakdown coverage: Pays for repairs or replacement parts if your vehicle breaks down due to no external cause.

- Custom parts and equipment value coverage: Covers repairs or replacement of modifications to your vehicle.

- Classic car insurance: Provides coverage for classic or antique cars and insures the vehicle for its full appreciated value.

- Business or commercial auto insurance: Covers you when using your vehicle for commercial or business purposes.

Does Your Auto Insurance Cover Canada: Understanding the Cross-Border Confusion

You may want to see also

Explore related products

![]()

How do I buy a policy?

There are several ways to buy an auto insurance policy. You can buy directly from an insurance company, either online or over the phone, or you can work with an agent or broker. You can also use an online marketplace to compare multiple quotes at once.

Buying directly from an insurance company

Many companies allow you to get a quote and buy coverage online or over the phone. This option gives you control over the process and allows you to get a quote and purchase a policy quickly and conveniently. However, you will only see quotes from one company at a time, so you will need to compare costs yourself to find the cheapest rate.

Buying through an agent

Agents have physical offices where you can buy insurance in person. They can guide you through the process, especially if you are unsure about what you need, and they can help you manage multiple policies. However, some agents may charge additional fees or only show you quotes from certain companies.

Buying through an online marketplace

Online marketplaces allow you to compare quotes from multiple companies at once, without having to enter your information repeatedly. This option is best for those who are comfortable shopping online or over the phone, as you won't be able to visit an office in person.

Information you'll need to provide

Regardless of how you choose to buy auto insurance, you will need to provide certain information to get a quote and purchase a policy. This includes:

- Names, birthdays, and driver's license numbers for all drivers in the household

- Social Security numbers for all drivers in the household

- Vehicle Information Numbers (VINs) or make and model years for all vehicles

- An address for the insured (where you live and where the car is garaged)

- Your current insurer, if you have one, and your current coverage limits

- Driving history for all drivers, including accidents, tickets, or violations

Choosing a policy

When choosing a policy, it's important to compare quotes from multiple companies to find the most competitive rates. Consider not just the cost but also the company's reputation, customer service, and available products. You should also think about your specific needs—for example, whether you need coverage for a family or as a single adult.

Finalising your purchase

Once you've chosen a company and a policy, you'll need to set a start date for your policy and pay your first premium. You'll typically receive proof of coverage and a welcome package from your insurer. Remember to cancel your old policy, if you have one, to ensure there is no lapse in coverage.

Cargo Conundrum: Unraveling the Auto Insurance Coverage Mystery

You may want to see also

Explore related products

![]()

How do I cancel my old policy?

To cancel your old auto insurance policy, you should first purchase a new policy to avoid a lapse in coverage, which could cause your insurance rates to increase. Auto insurance is legally required in nearly every state, so it is important to have a new policy in place before cancelling your old one.

Next, contact your insurance provider. You may be able to do this by phone, mail, or in person, depending on the company. Ask to speak with an agent about cancellation, as each provider will have different requirements. For example, some may require you to pay a cancellation fee or give 30 days' notice. You may also be required to sign a cancellation letter or form. This will include your policy number, name, and the date you want your policy to be cancelled. If you have paid for your policy upfront, you can also request a refund for the unused portion.

Once your cancellation is finalized, your carrier will send a notice confirming that your policy has been cancelled. If you do not receive this, ask your insurer to provide one so that you have a written record of the transaction.

Zander Insurance: Unlocking Home and Auto Protection

You may want to see also

Frequently asked questions

To get a car insurance quote, you will need to provide basic information about yourself and any other drivers, including names, addresses, dates of birth, and driver's license numbers. You will also need to provide information about your vehicle, such as the make, model, and year, vehicle identification number (VIN), safety features, and annual mileage.

The amount of coverage you need depends on factors such as the value of your car, where you live, and your financial situation. Most states require liability insurance, but you may want to consider additional coverage such as comprehensive, collision, and uninsured motorist insurance.

When comparing insurance quotes, ensure you are comparing like-for-like by selecting the same coverage, policy limits, and deductibles. You can use online tools or work with an agent to compare quotes from different providers.

Once you have chosen a company and policy, you can usually pay upfront or in monthly installments. The insurance company will provide proof of insurance, which is required in most states before driving a vehicle.

Yes, if you are switching insurance companies, cancel your old policy after the new one is in place to avoid a lapse in coverage. You should receive a refund for any unused portion of your previous policy.