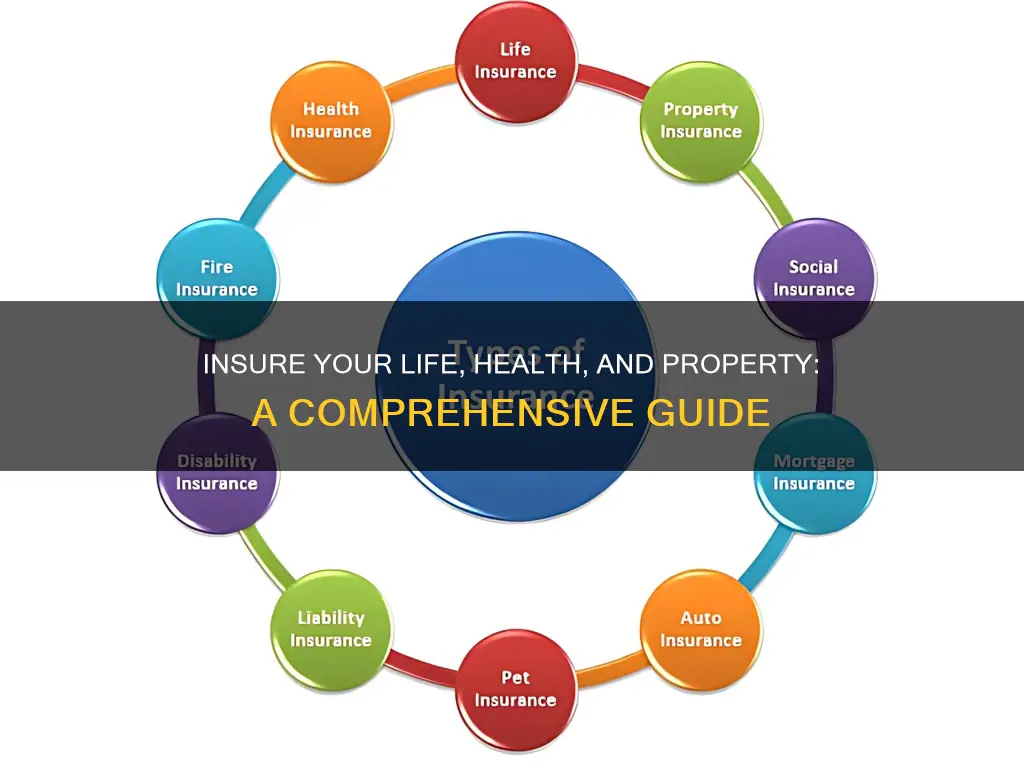

Life, health, and property insurance are essential components of financial planning. Life insurance provides financial protection for loved ones in the event of an insured person's death, with permanent and term policies offering varying levels of coverage. Health insurance, while legally mandated, can be obtained through an employer or self-insured with a high-deductible plan. Property insurance encompasses homeowners, renters, and flood insurance, safeguarding against structural damage, theft, and liability. Understanding these insurance types is crucial for comprehensive risk management.

| Characteristics | Values |

|---|---|

| Purpose of Life Insurance | Provide financial support to surviving dependents or beneficiaries after the death of the insured policyholder |

| Who Needs Life Insurance? | Parents with minor children, adults who own property together, young adults whose parents incurred private student loan debt, married pensioners, etc. |

| Types of Life Insurance | Permanent, Term |

| Factors Affecting Life Insurance Premiums | Age, gender, smoking, health, lifestyle, family medical history, driving record |

| Self-Insurance | Acting as your own insurer; setting money aside to be used in the event of an incident |

| Property Insurance | Provides financial reimbursement to the owner or renter of a structure and its contents in case of damage or theft |

| Types of Property Insurance | Homeowners insurance, renters insurance, flood insurance, earthquake insurance |

| Factors Affecting Property Insurance Premiums | Age of the home, location, risk of natural disasters, etc. |

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

What You'll Learn

![]()

How to choose the right health insurance plan for you

Choosing the right health insurance plan can be confusing and overwhelming. There are many companies, plans, and networks to evaluate and consider. However, by following a few steps, you can make an informed decision about which plan is best for you and your family. Here is a guide on how to choose the right health insurance plan:

Step 1: Know Where to Go

If you are 65 or older, you are eligible for Medicare, a federally run program that covers most of your health care costs. You may also be eligible for Medicare if you have certain disabilities. For those under 65, most people get their health insurance coverage through their employer, as employers typically cover a significant portion of the insurance premiums. If your employer does not offer health insurance, you can shop for insurance in the marketplaces created by the Affordable Care Act (also known as Obamacare). These marketplaces can be found on Healthcare.gov. Additionally, if your income is low enough, you may be eligible for Medicaid, a government insurance program that provides health coverage for low-income individuals and families.

Step 2: Consider Your Health and Financial Situation

Think about your current and future health needs, as well as your financial situation and goals. Ask yourself if you have any chronic health conditions or concerns that require regular medical care or prescription medications. Also, consider if you are expecting any major life changes in the next year, such as having a baby, getting married, or retiring, as these events may impact your insurance needs.

Step 3: Compare Types of Health Insurance Plans

There are several types of health insurance plans, including HMOs, PPOs, EPOs, and POS plans. These plans differ in terms of provider networks, out-of-pocket costs, and referral requirements. HMOs (Health Maintenance Organizations) typically have lower out-of-pocket costs but limit you to a smaller network of providers. PPOs (Preferred Provider Organizations) offer a wider range of providers but usually come with higher out-of-pocket costs. EPOs (Exclusive Provider Organizations) and POS (Point of Service) plans are less common but offer a mix of features from HMOs and PPOs.

Step 4: Compare Health Plan Networks

Consider whether you have preferred doctors, specialists, hospitals, or pharmacies that you would like to continue using. Check if these providers are included in the networks of the insurance plans you are considering. Keep in mind that medical professionals and insurance companies regularly update their contracts, so a provider that was in-network last year may be out-of-network next year.

Step 5: Compare Out-of-Pocket Costs

Out-of-pocket costs, such as copayments, deductibles, and coinsurance, can add up quickly and impact your budget. Consider your anticipated health care needs for the upcoming year and compare the associated costs under each plan. Generally, plans with higher monthly premiums will have lower out-of-pocket costs, while plans with lower monthly premiums will result in higher out-of-pocket costs when you receive health care.

Step 6: Compare Benefits

Review the scope of services covered by each plan, such as physical therapy, fertility treatments, mental health care, and emergency coverage. Also, consider your specific needs, such as medication coverage, maternity services, and travel coverage. Contact the insurance company directly if you have any questions or concerns about a particular plan.

By following these steps, you can make an informed decision about which health insurance plan is right for you and your family. It is important to carefully review and compare the available options to ensure you get the coverage you need at a cost that fits your budget.

Gun Ownership: Impact on Life Insurance Rates

You may want to see also

Explore related products

![]()

What to consider when insuring your property

Property insurance is a broad term for a series of policies that provide either property protection or liability coverage for property owners. It is advisable for anyone who owns an expensive property, such as a house or a car, to carry property insurance. When insuring your property, there are several things to consider:

Understand the Different Types of Property Insurance

Property insurance can include homeowners insurance, renters insurance, flood insurance, and earthquake insurance. It is important to understand the different types of property insurance and what each covers. For example, homeowners insurance typically covers structural losses and personal property, while renters insurance covers tenants from loss of personal property and liability issues.

Know What is Excluded from Coverage

It is essential to understand what is excluded from your property insurance policy. For example, property insurance policies typically exclude damage caused by floods, earthquakes, or acts of war. Knowing what is not covered will help you make an informed decision about your insurance needs.

Decide on the Level of Coverage

There are different levels of coverage available, such as replacement cost, actual cash value, and extended replacement costs. Replacement cost covers the cost of repairing or replacing property at the same or equal value. Actual cash value coverage pays the owner or renter the replacement cost minus depreciation. Extended replacement costs will pay more than the coverage limit if construction costs have increased.

Shop Around and Compare Policies

There are many insurance companies and coverage options available. It is important to shop around and compare policies to find the best one for your needs. You may want to consider working with an insurance agent or broker to help you navigate the different options.

Understand How Your Policy Covers Repairs

It is important to know how your policy covers repairs. Covering the full replacement cost is typically better than just the actual cash value, but it will cost more in premiums. Review the details of your policy to understand how repairs will be handled.

Consider Bundling Policies

If you need to insure multiple items or obtain different types of insurance, consider bundling your policies with a single insurance carrier. This may result in multi-policy discounts or loyalty programs, helping you save money on your overall insurance costs.

Marriage and Life Insurance: What Changes and What Stays the Same

You may want to see also

Explore related products

![]()

The different types of life insurance

Life insurance is a contract under which an insurance company agrees to pay a specified amount, known as a death benefit, after the death of an insured party, as long as the premiums are paid. There are two main types of life insurance: permanent and term. Here is a more detailed breakdown of the different types of life insurance:

Term Life Insurance

Term life insurance is a temporary type of policy that provides coverage for a set number of years, typically 10, 15, 20, or 30 years. It is a simple, low-cost policy, and its main purpose is to replace your income when you die. Term life insurance is usually the cheapest option and is sufficient for most people. However, if you outlive your policy, your beneficiaries won't receive a payout.

Whole Life Insurance

Whole life insurance is a permanent coverage type that lasts your entire life, as long as you keep paying the premiums. It includes a savings component, known as the cash value, that grows over time at a fixed interest rate. Whole life insurance is usually more expensive than term life insurance but offers more secure benefits in the long run. It is best suited for those seeking lifelong coverage and long-term financial planning.

Universal Life Insurance

Universal life insurance is a type of permanent policy that offers more flexibility than whole life insurance. It allows you to adjust your premiums and death benefit over time, within certain limits. The cash value of a universal life policy grows at a variable interest rate based on market conditions. This type of insurance is typically less expensive than whole life insurance but does not guarantee the death benefit or cash value growth.

Variable Life Insurance

Variable life insurance is a riskier type of permanent life insurance. It has a fixed death benefit and a variable cash value that rises and falls based on the performance of selected investments. Variable life insurance offers the potential for higher gains but also carries higher fees and costs than other types of life insurance. It is best suited for those with a higher risk tolerance who want more control over their investments.

Final Expense Life Insurance

Final expense life insurance, also known as burial or funeral insurance, is a type of whole life insurance with a smaller death benefit designed to cover end-of-life expenses such as funeral costs, medical bills, and outstanding debts. It is easier for older or less healthy individuals to qualify for and typically does not require a medical exam. The coverage amount is usually capped at a lower limit, and there may be a waiting period before the full death benefit is paid out.

Other Types of Life Insurance

In addition to the main types mentioned above, there are several other life insurance options:

- Group life insurance: Offered by employers as part of workplace benefits, providing coverage for employees or members of an organization.

- Mortgage life insurance: Covers the current balance of your mortgage and pays out to the lender if you die.

- Credit life insurance: Pays off a specific loan, such as a home equity loan, in the event of your death.

- Accidental death and dismemberment insurance (AD&D): Covers death or serious injuries, such as loss of limbs, resulting from an accident.

- Joint life insurance: Insures two lives under one policy, with the payout triggered by the first or second death, depending on the policy type.

Life Insurance: When Less is More

You may want to see also

Explore related products

$39.99 $119.95

![]()

How to calculate your life insurance needs

Life insurance is a contract under which an insurance company agrees to pay a specified amount after the death of an insured party, as long as the premiums are paid. The payout amount is called a death benefit. Policies give insured people the assurance that their loved ones will have financial protection and peace of mind after their death.

There are two main types of life insurance: permanent and term. Permanent life insurance policies do not have an expiration date, meaning you’re covered for life as long as your premiums are paid. Term life insurance, on the other hand, only covers you for a set number of years and does not accumulate cash value.

The younger and healthier you are, the less you’ll pay for premiums. However, older people can still get life insurance.

- Standard-of-Living Method: This method is based on the amount of money survivors would need to maintain their standard of living if the insured party dies. If your age is between 41-50, you take that amount and multiply it by 20. From 51 to 60, multiply it by 15. The thought here is that survivors can take a 5% withdrawal from the death benefit each year while investing the death benefit principal and earning 5% or better. This type of calculation is sometimes known as the human life value (HLV) approach.

- Years-Until-Retirement Method: Another way to calculate the amount of life insurance needed is to multiply your annual salary by the number of years left until retirement. For example, if a 40-year-old currently makes $20,000 a year, they will need $500,000 (25 years × $20,000) in life insurance to reach the age of 65.

- Debt, Income, Mortgage, Education (DIME) Method: This methodology is meant for a minimal amount of coverage that will cover family expenses in the event of an untimely death. With the DIME approach, your coverage should be enough to cover all your outstanding debts (including your mortgage), pay for your children's education, and replace your income for the years until your children turn 18.

- 10x Annual Salary: Most insurance companies say a reasonable amount for life insurance is at least 10 times the amount of annual salary. If you multiply an annual salary of $50,000 by 10, for instance, you'd opt for $500,000 in coverage. Some recommend adding an additional $100,000 in coverage per child.

Property insurance is a broad term for a series of policies that provide either property protection or liability coverage for property owners. It provides financial reimbursement to the owner or renter of a structure and its contents in the case of damage or theft, and to a person other than the owner or renter if that person is injured on the property.

Life Insurance: Geico's Accelerated Rider Option Explained

You may want to see also

Explore related products

![Property: [Connected eBook with Study Center] (Aspen Casebook)](https://m.media-amazon.com/images/I/61tDfTMq9EL._AC_UY218_.jpg)

![]()

How to insure your health if you're self-employed

If you're self-employed, you can use the individual Health Insurance Marketplace to enroll in flexible, high-quality health coverage. This is also known as private coverage, as opposed to a group plan offered by an employer. You can also use the SHOP Marketplace for small businesses if your business has at least one employee (other than yourself, a spouse, family member, or owner).

The Individual Marketplace offers flexible, quality coverage for people who:

- Run their own businesses

- Are self-employed with no employees

- Work as freelancers or consultants

All plans in the Marketplace cover the same categories of essential health benefits, including doctors' services, inpatient and outpatient hospital care, prescription drug coverage, pregnancy and childbirth, and mental health services. Some plans cover more services.

The cost of self-employed health insurance depends on who you need to cover (e.g., a spouse or kids), the level of coverage you need, whether you smoke, your age, and where you live. Plans start at around $350 a month.

You can also consider the following options for health coverage if you're self-employed:

- Short-term medical plans: These plans cover you for three months up to a year and allow you to sign up outside of the usual enrollment period. However, they have high out-of-pocket costs and usually don't cover pre-existing conditions.

- Catastrophic health insurance: This type of insurance covers major health expenses like accidents, sudden illnesses, or injuries, as well as preventative care services and annual checkups. It is an option for those who qualify for a personal hardship or an affordability exemption.

- Membership organizations: Some industry-specific groups, such as freelancers' unions or college alumni associations, offer discounted health insurance plans.

- Independent insurance agents or brokers: These agents can help you find plans customized for self-employed individuals, offering a range of benefits at an affordable rate.

- Direct enrollment or private exchanges: You can buy a plan directly from an insurance company through a private online exchange, but these plans may be more expensive and have fewer options.

- COBRA health insurance: If you recently lost your job, you can keep your previous employer's health insurance plan for up to 36 months through COBRA.

- Health care sharing ministries: These groups are not technically "health insurance," but they pool money together to cover major health care costs for members. They are usually less expensive but may not cover pre-existing conditions.

Xanax and Life Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Life insurance is a contract between an individual and an insurance company, where the company agrees to pay a sum of money to beneficiaries upon the individual's death, in exchange for premium payments made by the individual during their lifetime. The two main types of life insurance are permanent and term. Permanent life insurance policies do not have an expiration date, whereas term life insurance policies are designed to last a certain number of years and then end.

The amount of life insurance coverage you need depends on your financial goals and family situation. If you have dependents, you may want to ensure they are financially provided for in the event of your death. It is recommended that you calculate the lump sum that can satisfy any potential expenses, such as mortgage payments, college tuition, credit card debt, and funeral expenses.

Property insurance is a broad term for a series of policies that provide either property protection or liability coverage for property owners and renters. It typically covers structural damage, theft of personal belongings, and liability in case someone is injured on the property. Property insurance can include homeowners insurance, renters insurance, flood insurance, and earthquake insurance.

Self-insuring means acting as your own insurance company by setting money aside to cover any potential losses, instead of purchasing insurance coverage. The benefit of self-insuring is that you keep more money in your pocket by avoiding insurance premiums. However, the risk is that you may not have enough money to cover losses in the event of an accident or natural catastrophe. It is recommended that you always carry some form of insurance to protect yourself and your family.

![Property Law: Rules, Policies, and Practices [Connected eBook with Study Center] (Aspen Casebook) (Aspen Casebook Series)](https://m.media-amazon.com/images/I/61hxQJz9u9L._AC_UY218_.jpg)