Hospital insurance, also known as hospitalization insurance, is a critical component of healthcare coverage, yet its prevalence varies significantly across different regions and populations. In countries with robust public healthcare systems, such as Canada or the United Kingdom, hospital insurance is often integrated into universal health coverage, making it widely accessible to citizens. Conversely, in nations with privatized healthcare, like the United States, hospital insurance is typically obtained through employer-sponsored plans, individual policies, or government programs like Medicare and Medicaid. Despite its importance, gaps in coverage persist, particularly among low-income individuals and those in developing countries, where out-of-pocket expenses for hospital stays can be financially devastating. Understanding the prevalence of hospital insurance is essential for addressing disparities in healthcare access and ensuring that individuals are protected against the high costs of medical treatment.

Explore related products

What You'll Learn

- Prevalence of Hospital Insurance: Percentage of population with hospital insurance coverage globally and regionally

- Factors Influencing Ownership: Key reasons people choose or skip hospital insurance plans

- Cost of Hospital Insurance: Average premiums and affordability across different demographics

- Employer-Provided Coverage: Role of employers in offering hospital insurance benefits

- Government vs. Private Plans: Comparison of public and private hospital insurance options

![]()

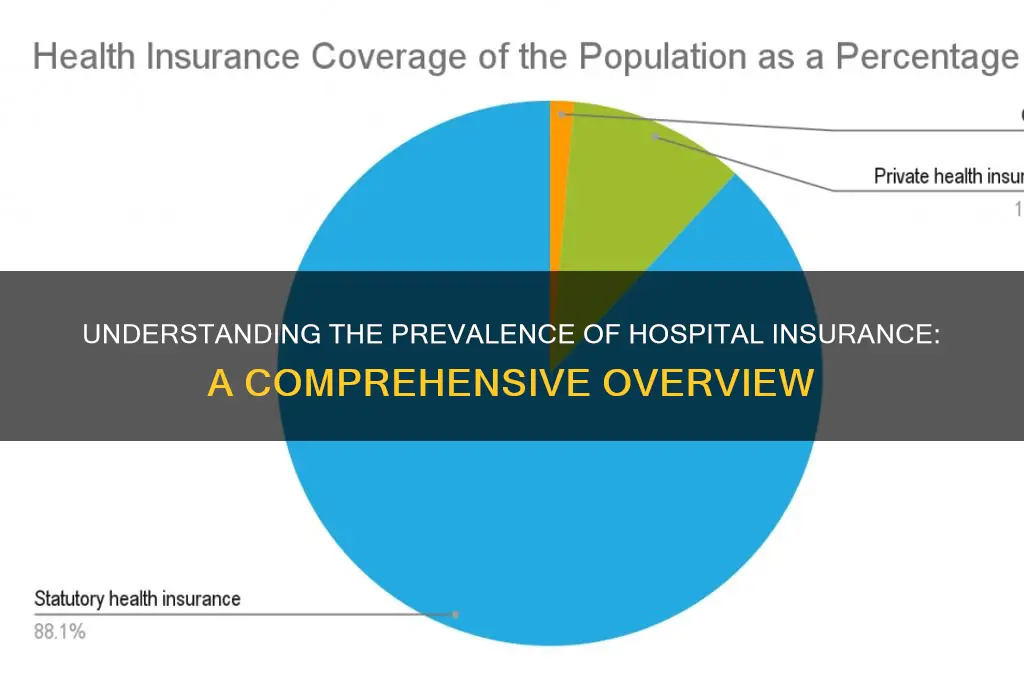

Prevalence of Hospital Insurance: Percentage of population with hospital insurance coverage globally and regionally

The prevalence of hospital insurance varies significantly across the globe, influenced by factors such as economic development, healthcare systems, and government policies. Globally, it is estimated that approximately 54% of the world’s population has some form of health insurance or coverage that includes hospital services, according to the World Health Organization (WHO) and other international health reports. However, this figure masks substantial disparities between high-income and low-income countries. In high-income nations, such as those in North America, Western Europe, and parts of Asia (e.g., Japan and South Korea), hospital insurance coverage is nearly universal, with 80-95% of the population having access to such protection through public or private schemes. These regions often have robust healthcare systems where hospital insurance is either mandated by law or provided as a public service.

In contrast, low- and middle-income countries (LMICs) in regions like sub-Saharan Africa, South Asia, and parts of Southeast Asia exhibit much lower coverage rates. In these areas, less than 30% of the population typically has hospital insurance, primarily due to limited financial resources, inadequate healthcare infrastructure, and a lack of government-funded health programs. For instance, in countries such as Nigeria, India, and Indonesia, hospital insurance is often restricted to urban populations or those employed in the formal sector, leaving rural and informal workers vulnerable to out-of-pocket expenses during hospitalization.

Regionally, Europe stands out as a leader in hospital insurance coverage, with over 90% of the population in countries like Germany, France, and the United Kingdom having access to comprehensive hospital insurance through public health systems. Similarly, in North America, approximately 90% of Canadians and 85-90% of Americans are covered, though the U.S. relies more heavily on private insurance compared to Canada’s single-payer system. In Latin America, coverage is more uneven, with countries like Brazil and Chile achieving 70-80% coverage through a mix of public and private schemes, while others, such as Honduras and Guatemala, struggle with rates below 40%.

Asia presents a mixed picture, with Japan and South Korea boasting near-universal coverage (above 95%), while countries like India and the Philippines have coverage rates below 30%. China, however, has made significant strides, with over 95% of its population now covered under its public health insurance schemes, though the extent of hospital coverage varies. In the Middle East, countries with high GDPs, such as the United Arab Emirates and Saudi Arabia, have 70-80% coverage, often through employer-provided insurance, whereas poorer nations like Yemen and Syria have rates below 20%.

In sub-Saharan Africa, hospital insurance remains the least prevalent, with only 5-10% of the population covered in most countries. Exceptions include South Africa, where approximately 17% of the population has private hospital insurance, and Rwanda, which has achieved over 80% coverage through community-based health insurance programs. These regional disparities highlight the critical role of government initiatives, economic stability, and policy frameworks in determining the prevalence of hospital insurance.

Understanding these global and regional trends is essential for policymakers, healthcare providers, and insurers to address gaps in coverage and improve access to hospital services. Efforts to expand hospital insurance, particularly in LMICs, could significantly reduce financial barriers to healthcare and improve health outcomes worldwide.

Insurance Jobs: Recession-Proof or Not?

You may want to see also

Explore related products

![]()

Factors Influencing Ownership: Key reasons people choose or skip hospital insurance plans

Hospital insurance, often a component of broader health insurance plans, is a critical financial safeguard against the high costs of medical care. However, the decision to own hospital insurance varies widely among individuals, influenced by a combination of personal, financial, and societal factors. Understanding these factors is essential to grasp why some people opt for such coverage while others forgo it.

Financial Considerations

One of the primary factors influencing ownership of hospital insurance is an individual’s financial situation. For many, the cost of premiums, deductibles, and copayments can be prohibitive. People with limited disposable income or those living paycheck to paycheck may prioritize immediate expenses over long-term insurance benefits. Conversely, those with stable finances or higher incomes are more likely to invest in hospital insurance as a precautionary measure. Additionally, individuals with substantial savings or assets may feel less compelled to purchase insurance, relying instead on their ability to cover medical expenses out-of-pocket.

Health Status and Risk Perception

Personal health status and risk perception play a significant role in the decision to own hospital insurance. Young, healthy individuals often perceive themselves as low-risk and may skip insurance, assuming they are unlikely to require hospitalization. In contrast, older adults or those with pre-existing conditions are more inclined to purchase coverage due to a higher likelihood of needing medical care. Risk perception is also shaped by family medical history; individuals with a history of chronic illnesses or hereditary conditions are more likely to prioritize hospital insurance.

Access to Employer-Sponsored Coverage

Employer-sponsored health insurance is a major determinant of hospital insurance ownership. Many people rely on workplace plans that include hospitalization coverage, making it a convenient and often subsidized option. In countries with robust employer-based insurance systems, such as the United States, this is a key reason for high ownership rates. Conversely, individuals without access to employer-sponsored plans, such as freelancers or part-time workers, may struggle to afford individual policies, leading to lower ownership rates.

Government Policies and Public Health Systems

Government policies and the strength of public health systems significantly impact hospital insurance ownership. In countries with universal healthcare, such as Canada or the United Kingdom, the need for private hospital insurance is minimal, as most medical expenses are covered by the state. In contrast, nations with limited public healthcare, like India or parts of the United States, often see higher demand for private insurance. Additionally, government subsidies or mandates, such as the Affordable Care Act in the U.S., can increase ownership by making insurance more affordable or compulsory.

Awareness and Education

Lack of awareness and education about the benefits of hospital insurance can deter ownership. Many individuals may underestimate the potential financial burden of hospitalization or misunderstand the coverage provided by existing policies. Effective public awareness campaigns and financial literacy programs can bridge this gap, encouraging more people to invest in insurance. Conversely, misinformation or distrust of insurance providers can lead to skepticism and avoidance of such plans.

In conclusion, the decision to own hospital insurance is shaped by a complex interplay of financial, health-related, societal, and informational factors. Addressing these influences through policy interventions, education, and affordable options can increase ownership rates, ensuring more individuals are protected against the unforeseen costs of hospitalization.

Pet Insurance: Protecting Your Furry Friends

You may want to see also

Explore related products

![]()

Cost of Hospital Insurance: Average premiums and affordability across different demographics

The cost of hospital insurance varies significantly across different demographics, influenced by factors such as age, location, health status, and the level of coverage chosen. On average, hospital insurance premiums in the United States range from $300 to $700 per month for individual plans, though these figures can be higher or lower depending on specific circumstances. For instance, younger individuals typically pay less due to lower health risks, with premiums starting as low as $200 per month. Conversely, older adults, particularly those over 50, may face premiums exceeding $1,000 per month due to increased health risks and higher healthcare utilization.

Affordability of hospital insurance is a pressing concern, especially for low-income individuals and families. According to the Kaiser Family Foundation, approximately 10% of the U.S. population remains uninsured, often due to the perceived high cost of premiums. Subsidies and tax credits under the Affordable Care Act (ACA) have helped mitigate costs for eligible individuals, reducing average premiums to as low as $100 per month for those earning up to 400% of the federal poverty level. However, for those who do not qualify for subsidies, the financial burden can be substantial, particularly in states with higher insurance costs.

Geographic location also plays a critical role in determining hospital insurance costs. Premiums vary widely by state, with states like Wyoming and Alaska often having higher costs due to limited competition among insurers and higher healthcare expenses. In contrast, states like Minnesota and Massachusetts tend to have lower premiums due to more competitive markets and state-level healthcare reforms. Urban areas may also see higher premiums compared to rural areas, though access to more healthcare providers can sometimes offset these costs.

Demographics such as family size and employment status further impact affordability. Family plans are generally more expensive, with average premiums ranging from $800 to $1,500 per month, depending on the number of members covered. Employer-sponsored insurance, which covers about 50% of the U.S. population, is often more affordable, as employers typically subsidize a portion of the premium. However, self-employed individuals and those working in industries without employer-provided insurance often face higher out-of-pocket costs, making affordability a significant challenge.

Health status and lifestyle choices are additional determinants of hospital insurance costs. Individuals with pre-existing conditions may face higher premiums or limited plan options, though the ACA prohibits insurers from denying coverage based on health status. Similarly, smokers often pay 50% more for premiums compared to non-smokers due to the increased health risks associated with smoking. High-deductible health plans (HDHPs) offer lower premiums but require individuals to pay more out-of-pocket before insurance coverage kicks in, making them a cost-effective option for healthier individuals but potentially burdensome for those with frequent medical needs.

In conclusion, the cost of hospital insurance is shaped by a complex interplay of demographic, geographic, and health-related factors. While average premiums provide a general benchmark, affordability remains a significant issue for many, particularly those without access to subsidies or employer-sponsored plans. Understanding these cost drivers is essential for individuals and families to make informed decisions about their healthcare coverage and financial planning.

Does USAA Offer Insurance Coverage for DoD Civilians? Explained

You may want to see also

Explore related products

![]()

Employer-Provided Coverage: Role of employers in offering hospital insurance benefits

Employer-provided hospital insurance is a cornerstone of healthcare coverage in many countries, particularly in the United States. Employers often play a pivotal role in offering health insurance benefits, including hospital coverage, as part of their employee compensation packages. This practice is so widespread that, according to the Kaiser Family Foundation, approximately 56% of non-elderly Americans receive health insurance through their employer or a family member’s employer. Hospital insurance, which typically covers inpatient care, surgeries, and other hospital-related services, is a critical component of these plans. By providing such coverage, employers not only attract and retain talent but also contribute to the overall health and productivity of their workforce.

The role of employers in offering hospital insurance benefits extends beyond mere financial support. Employers often negotiate with insurance providers to secure comprehensive plans that include hospital coverage at competitive rates. These group plans are generally more affordable than individual policies because the risk is spread across a larger pool of employees. Additionally, employers may subsidize a significant portion of the premiums, making hospital insurance more accessible to employees. This shared cost model ensures that workers can afford necessary medical care without facing financial hardship, fostering a sense of security and loyalty among employees.

Another key aspect of employer-provided hospital insurance is the administrative role employers play. They manage the enrollment process, provide educational resources to help employees understand their benefits, and act as intermediaries between employees and insurance providers. Many employers also offer wellness programs and preventive care initiatives that complement hospital insurance by reducing the likelihood of severe illnesses requiring hospitalization. These efforts not only enhance employee health but also help control healthcare costs for both the employer and the workforce.

Despite its prevalence, employer-provided hospital insurance is not without challenges. Rising healthcare costs and regulatory changes can make it difficult for employers, especially small businesses, to maintain robust coverage. Some employers may opt for high-deductible plans or limit the extent of hospital coverage to manage expenses, which can shift more financial burden onto employees. However, many organizations recognize the long-term benefits of investing in comprehensive health insurance, including hospital coverage, as it directly impacts employee satisfaction, retention, and overall business success.

In conclusion, employer-provided coverage, particularly hospital insurance, remains a vital component of the healthcare landscape. Employers serve as key facilitators by offering, subsidizing, and administering these benefits, ensuring that employees have access to essential medical care. While challenges exist, the widespread adoption of employer-sponsored hospital insurance underscores its importance in both employee well-being and organizational health. As healthcare systems continue to evolve, the role of employers in providing hospital insurance benefits will likely remain a critical factor in shaping access to care.

Understanding Social Insurance: Key Programs and Their Impact on Society

You may want to see also

Explore related products

![]()

Government vs. Private Plans: Comparison of public and private hospital insurance options

When considering hospital insurance, one of the most critical decisions is choosing between government-sponsored plans and private insurance options. Both have distinct advantages and limitations, and understanding these differences is essential for making an informed choice. Government hospital insurance, often referred to as public insurance, is typically funded by taxpayers and administered by federal or state agencies. Examples include Medicare in the United States, the National Health Service (NHS) in the UK, and similar programs in other countries. These plans are designed to provide universal or near-universal coverage, ensuring that healthcare is accessible to all citizens, regardless of income or pre-existing conditions. In contrast, private hospital insurance is offered by for-profit or non-profit companies and is usually purchased individually or provided through employers. Private plans often offer more flexibility in terms of coverage options, provider networks, and additional benefits, but they can be more expensive and may exclude individuals with certain health conditions.

One of the primary differences between government and private hospital insurance lies in cost and accessibility. Government plans are generally more affordable because they are subsidized by taxes, making them an attractive option for low-income individuals and families. For instance, Medicare in the U.S. covers seniors and certain disabled individuals with minimal out-of-pocket costs. Private insurance, however, often comes with higher premiums, deductibles, and copayments, though it may provide more comprehensive coverage for specialized treatments or elective procedures. Additionally, private plans frequently allow policyholders to choose their healthcare providers, whereas government plans may restrict access to specific hospitals or doctors within a designated network.

Coverage scope is another critical factor in comparing government and private hospital insurance. Government plans typically focus on essential healthcare services, such as hospital stays, emergency care, and preventive services, but may exclude certain treatments like cosmetic surgery or alternative therapies. Private insurance, on the other hand, often includes a broader range of benefits, such as dental, vision, and mental health care, depending on the policy. Private plans may also cover advanced treatments or medications that are not available under public insurance, making them a preferred choice for individuals with specific health needs or those seeking more extensive protection.

Enrollment and eligibility criteria also differ significantly between government and private plans. Government hospital insurance is usually available to specific groups, such as seniors, low-income individuals, or those with disabilities, and enrollment periods are often limited. For example, Medicare eligibility begins at age 65 in the U.S., and missing the initial enrollment window can result in penalties. Private insurance, however, can be purchased at any time, provided the individual meets the insurer’s underwriting criteria. This flexibility makes private plans a viable option for those who do not qualify for government coverage or need insurance outside of designated enrollment periods.

Finally, the claims and administration process varies between government and private hospital insurance. Government plans are often criticized for their bureaucratic inefficiencies, leading to longer processing times for claims and limited customer support. Private insurers, while sometimes accused of prioritizing profits over policyholders, generally offer more streamlined claims processes and better customer service. Additionally, private plans may provide tools and resources to help policyholders navigate their benefits, such as online portals or wellness programs, which are less common in government-sponsored insurance.

In conclusion, the choice between government and private hospital insurance depends on individual needs, financial situation, and healthcare priorities. Government plans offer affordability and universal access but may come with limitations in coverage and provider choice. Private insurance provides greater flexibility and comprehensive benefits but at a higher cost. By carefully evaluating these factors, individuals can select the hospital insurance option that best aligns with their circumstances and ensures adequate protection for their health needs.

Borrowing Against Globe Life Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Hospital insurance, often part of health insurance plans, is very common in the United States. Over 90% of Americans have some form of health coverage, which typically includes hospital benefits through employer-sponsored plans, Medicaid, Medicare, or individual policies.

It varies by country. In nations with universal healthcare systems, like Canada or the UK, hospital coverage is mandatory and provided by the government. In other countries, such as the U.S., it is not mandatory but highly recommended due to the high cost of medical care.

Among younger adults, hospital insurance is less common compared to older age groups. Many young adults rely on employer-provided plans or stay on their parents’ insurance until age 26. However, awareness of the importance of coverage is increasing, especially due to the Affordable Care Act (ACA) in the U.S.

Yes, hospital insurance plans are widely available globally, though their prevalence depends on the country’s healthcare system. In countries without universal healthcare, private insurance is more common, while in countries with universal coverage, supplemental private plans are often purchased for additional benefits.