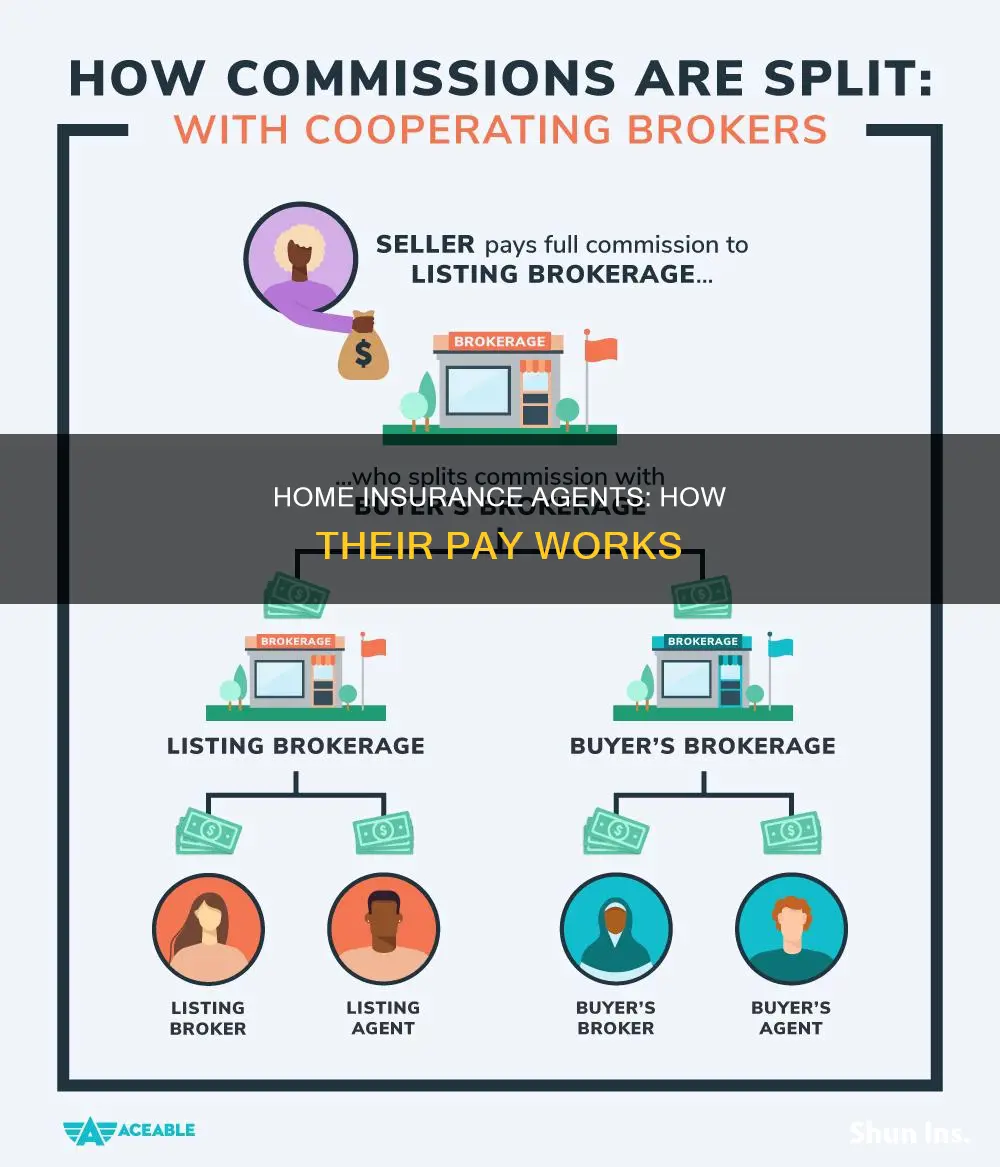

Insurance agents play a crucial role in helping individuals navigate the complex world of homeowners insurance and find the right coverage for their needs. Understanding how these agents are compensated is important for those considering a career in the industry or planning to work with an insurance agency. The most common way insurance agents are paid is through commissions, which are typically calculated as a percentage of the insurance policy premiums. These commissions can vary depending on factors such as the type and quantity of policies sold, the insurance company, and whether the agent is captive or independent. While commissions are the primary source of income for most agents, there may be other ways they can earn an income, such as a fixed salary or bonuses for meeting certain performance targets.

| Characteristics | Values |

|---|---|

| Primary source of income | Commissions |

| Commission rates for auto and home policies | Captive insurance agents: 5% to 10% |

| Independent agents: 10% to 20% | |

| Commission rates for life insurance | 40% to 115% of the first year's premiums |

| Commission rates for health insurance | 5% to 10% of the total premiums in the first year |

| Commission rates for group health insurance | 3% to 6% |

| Commission rates vary based on | State, carrier, policy, and agent |

| Salaried insurance agents | Fixed wages with potential for commissions |

| Independent insurance agents | May have more flexibility with commission rates |

Explore related products

What You'll Learn

- Home insurance agents are paid via commissions

- Commission rates vary by state, insurance carrier, policy, and agent

- Captive agents exclusively represent one insurance carrier

- Independent agents may have more flexibility with commission rates

- Agents' earnings are influenced by the quantity of successful sales

![]()

Home insurance agents are paid via commissions

Home insurance agents are typically paid via commissions. Commissions are a percentage of the insurance premium that the policyholder pays. For instance, if a homeowner pays an annual premium of $1000, the agent may receive a commission of $100. This commission may be paid upfront when the policy is sold, or it may be paid in instalments over the course of the policy. The commission structure can vary depending on the insurance company and the type of policy.

For auto and home insurance policies, captive insurance agents typically earn a commission of 5% to 10% of the entire premium paid during the first year, while independent agents may earn a higher commission of 10% to 20%. These rates can vary depending on the state, carrier, policy, and individual agent. In some cases, independent agents may have more flexibility in negotiating their commission rates since they can represent multiple insurance companies.

In addition to upfront commissions, home insurance agents may also receive residual or renewal commissions. These commissions are earned on an ongoing basis as long as the policy remains active and the policyholder continues to pay their premiums. Residual commissions promote long-term relationships between agents and policyholders, as the agent has an incentive to ensure client satisfaction.

Some insurance companies also offer supplemental and contingent commissions as incentives for agents who help them achieve certain business targets. These commissions are based on performance metrics such as sales targets or claim ratios. Overall, the commission structure can greatly impact an agent's income, and it is important for both agents and policyholders to understand these structures.

Farmers Insurance Uncovered: Examining the Pyramid Scheme Allegations

You may want to see also

Explore related products

![]()

Commission rates vary by state, insurance carrier, policy, and agent

Commission rates for insurance agents vary depending on the state, insurance carrier, policy, and agent. The type of insurance, the insurance company, the agent's experience, and the specific policies sold all influence the commission structure. For example, in North Carolina, commission ranges tend to start at around 5% and can reach up to 20%, with an average of roughly 10%.

Independent agents, who are not tied to a single insurance provider, typically earn higher commissions of around 15%. They have the freedom to work with various insurance companies and sell different types of policies. However, they also incur higher business expenses, such as rent and marketing costs.

On the other hand, captive agents usually sell for a single insurance company and may receive a salary supplemented with a smaller commission of 5% to 10%. While it may be easier to become a captive agent, independent agents have more flexibility and earning potential.

The commission structure also differs between insurance types. For instance, life insurance agents may receive front-loaded commissions of up to 120% of the first year's premiums, while health insurance agents earn an average of 5% to 10%.

Additionally, insurance agents can be paid through residual or renewal commissions. Residual commissions are earned on policies with ongoing premiums and promote long-term relationships between agents and policyholders. Upfront commissions provide a quick boost to an agent's income, especially when starting, but not all insurance types offer upfront commissions.

Stucco Homes: Insurance Coverage

You may want to see also

Explore related products

![]()

Captive agents exclusively represent one insurance carrier

Captive insurance agents exclusively represent a single insurance carrier. They are effectively in-house advocates for that insurance company's products and typically receive a salary from the insurance company or agency they work for. Their performance is dependent on the number of policies they can sell.

Captive agents are usually paid a fixed wage or salary, but depending on their contract, they may also receive commissions on top of their fixed wages. These commissions are typically lower than those of independent agents, who have the flexibility to represent multiple insurance companies and can earn higher commissions as a result. Captive agents earn commissions from selling insurance policies, and their income is not directly impacted by whether a client files a claim.

The commission structure for captive agents can vary depending on the insurance company and the type of insurance policy. For auto and home insurance policies, captive agents typically earn a commission of 5% to 10% of the entire premiums paid during the first year, with renewal commissions for subsequent years. Life insurance policies can have much higher first-year commissions, ranging from 50% to 100% of the first-year premiums, but these rates drop significantly for renewals.

It's important to note that captive agents' earnings are influenced by their sales performance, and they may experience challenges in predicting their income due to the variability in commission structures and sales targets. Additionally, captive agents often have access to a full range of employee benefits, including paid time off, which can impact their overall compensation package.

Understanding Post-Issue Underwriting for Homeowners Insurance

You may want to see also

Explore related products

![]()

Independent agents may have more flexibility with commission rates

Independent insurance agents typically earn income through commissions, which are influenced by the type and quantity of insurance policies they sell. These commissions can be higher than those of captive agents, incentivizing independent agents to find the most suitable and valuable coverage for their clients. Independent agents have more flexibility with commission rates because they can represent multiple insurance companies. They may also have the opportunity to earn supplemental and contingent commissions by helping insurance companies achieve certain business targets.

While independent agents may have more flexibility with commission rates, they often have to find customer leads on their own, which can be challenging in a competitive market. They may experience rejection and disdain from potential clients, and they typically have limited paid time off as they are not always entitled to the full range of employee benefits.

The commission structure for independent agents can vary depending on the insurance company and the type of insurance policy. For auto and home policies, independent agents typically earn first-year commissions between 5% and 20% of the total premiums paid. Life insurance agents may earn higher upfront commissions of 40% to 115% of the first year's premiums, but these rates drop significantly for renewals.

Overall, independent insurance agents have the potential to earn attractive commissions, especially if they can successfully navigate the challenges of finding leads and making sales. Their flexibility with commission rates allows them to represent multiple companies and maximize their earning potential.

Navigating the Farmers Insurance Interview: Strategies for Success

You may want to see also

Explore related products

![]()

Agents' earnings are influenced by the quantity of successful sales

The income of insurance agents is influenced by the number of policies they sell. Agents typically earn through commissions, which are calculated as a percentage of the policy's premium. For instance, independent agents can earn commissions of 10-20% of the premium, depending on the carrier, while captive agents may earn 5-10% for auto and home policies. Life insurance agents may receive up to 120% of the first year's premiums, but this drops significantly in subsequent years. Health insurance agents earn an average of 5-10% in commissions, with group policies earning slightly lower commissions of around 3-6%.

The variability in commission rates across different types of insurance and carriers makes it challenging to predict an agent's earnings accurately. Their income is heavily influenced by the quantity of successful sales, and their earnings reflect their drive to pursue and close deals. Independent agents, in particular, may have more flexibility with commission rates as they can represent multiple insurance companies. They often have to find their own leads, which can be challenging in a competitive market. Captive agents, on the other hand, exclusively represent a single insurance carrier and typically receive a salary from the company, with the possibility of additional commissions.

While commissions are the primary source of income for agents, there are other ways they can boost their earnings. Some insurance companies offer supplemental and contingent commissions as incentives for agents to meet specific business targets. These additional commissions are based on performance metrics such as sales targets or maintaining low claim ratios. Furthermore, some insurance agencies provide bonuses if the company achieves certain profit targets.

It is worth noting that the presence of an insurance agent does not directly impact the premium paid by the policyholder. While online insurance companies may advertise that removing the middleman can save costs, they allocate a significant portion of their funds to advertising. The premium paid by the policyholder is typically distributed to cover various expenses, including the agent's commission, agency expenses, and other operational costs.

Ring Devices: Do They Meet Home Insurance Criteria?

You may want to see also

Frequently asked questions

Homeowners insurance agents are typically paid through commissions. The commission amount varies depending on the insurance company, type of policy, and agent. For auto and home policies, captive insurance agents earn about 5% to 10% of the entire premiums paid for the first year, while independent agents receive about 15%.

A commission is a percentage of the premium paid by the policyholder that goes to the agent as compensation for their work. Commissions can be structured in different ways, such as upfront commissions, residual commissions, or contingent commissions.

Having an insurance agent does not directly increase your premium. The cost of the premium is determined by the insurance company, and the agent's commission is typically built into the price. However, the agent's recommendation may be influenced by the commission they receive, so it is important to consider any potential conflicts of interest.

The earnings of insurance agents can vary significantly depending on various factors, such as the number of policies sold, the type of policies, and the agent's experience. Independent insurance agents may have more flexibility in their earnings as they can represent multiple insurance companies.

Yes, some insurance agents may also be salaried employees of insurance companies or agencies. Their earnings may be based on a fixed wage, or they may receive commissions on top of their salaries. Additionally, some companies provide bonuses or implement profit-sharing programs.