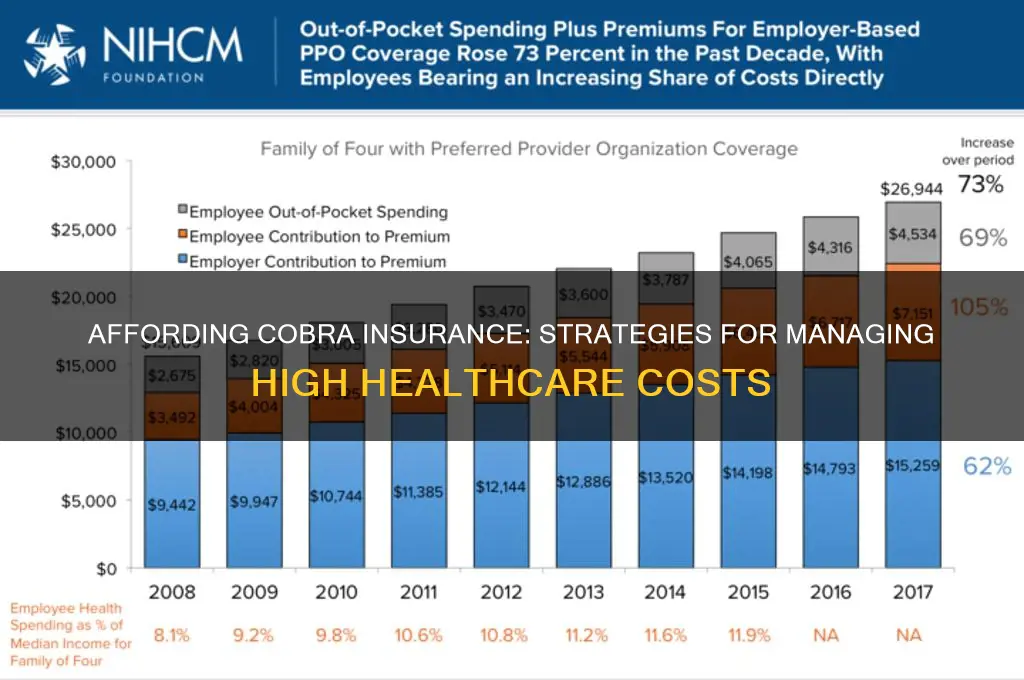

COBRA insurance, which allows individuals to continue their employer-sponsored health coverage after leaving a job, often comes with high premiums that can be financially burdensome. Many people struggle to afford it because, unlike employer-sponsored plans, COBRA requires the individual to pay the full cost of the insurance, including the portion previously covered by the employer, plus an administrative fee. To manage these costs, some individuals rely on savings, severance packages, or temporary employment, while others explore alternatives like Affordable Care Act (ACA) marketplace plans, short-term health insurance, or state-sponsored programs. Understanding eligibility for subsidies or financial assistance can also help make COBRA more affordable for those who need it.

| Characteristics | Values |

|---|---|

| Cost of COBRA Insurance | Typically 102% of the full premium (includes administrative fee). |

| Average Monthly Premium | ~$700 for individuals, ~$2,000 for families (varies by plan and location). |

| Duration of Coverage | Up to 18 months (or longer in certain circumstances). |

| Affordability Strategies | 1. Employer Subsidies: Some employers partially cover COBRA costs. |

| 2. Short-Term Health Plans: Cheaper but less comprehensive. | |

| 3. ACA Marketplace Plans: Subsidies available based on income. | |

| 4. State Continuation Coverage: Lower-cost alternatives in some states. | |

| 5. Health Savings Accounts (HSAs): Use pre-tax funds to pay premiums. | |

| Eligibility Requirements | Must have been covered under an employer-sponsored plan before leaving. |

| Income-Based Assistance | ACA subsidies or Medicaid for low-income individuals. |

| Tax Implications | Premiums are not tax-deductible unless self-employed. |

| Alternatives to COBRA | Medicaid, spouse’s employer plan, or ACA plans. |

| Enrollment Deadline | 60 days after job loss or insurance termination. |

| Prevalence of Usage | Only ~10-20% of eligible individuals opt for COBRA due to high costs. |

| Government Assistance | COBRA premium assistance under ARPA (American Rescue Plan Act) expired in 2021. |

| State-Specific Options | Some states offer mini-COBRA with lower costs for smaller employers. |

| Financial Planning Tips | Budgeting, negotiating with employers, or seeking part-time work with benefits. |

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

What You'll Learn

- Understanding COBRA Costs: Break down monthly premiums, compare to employer-subsidized plans, and analyze total expenses

- Eligibility Requirements: Determine who qualifies for COBRA, including employees, spouses, and dependent children

- Alternative Coverage Options: Explore ACA plans, short-term insurance, or state-sponsored programs as cost-effective alternatives

- Financial Assistance: Investigate subsidies, tax credits, or employer-provided support to offset COBRA premiums

- Duration of Coverage: Understand COBRA’s 18-36 month limit and plan for long-term insurance needs

![]()

Understanding COBRA Costs: Break down monthly premiums, compare to employer-subsidized plans, and analyze total expenses

COBRA insurance, while a lifeline for those transitioning between jobs, often comes with a sticker shock. Monthly premiums can be significantly higher than what employees are accustomed to paying under employer-subsidized plans. This is because COBRA requires individuals to cover the full cost of the insurance, including the portion previously paid by the employer, plus a 2% administrative fee. For a family plan, this can easily translate to $1,500 to $2,000 per month, a daunting figure for many. Understanding the breakdown of these costs is the first step in navigating affordability.

Let’s compare COBRA to employer-subsidized plans. Under an employer’s group health plan, the average monthly premium for a single individual is around $450, with the employer typically covering 70-80% of the cost. This means employees often pay only $100 to $150 monthly. COBRA, however, shifts the entire financial burden to the individual. For instance, if a family plan costs $2,000 per month under the employer, the employee might have paid $600, but under COBRA, they’ll owe the full $2,000 plus the administrative fee. This stark difference highlights why COBRA feels unaffordable for many, despite offering the same coverage.

Analyzing total expenses under COBRA requires a holistic view. Beyond monthly premiums, consider out-of-pocket costs like deductibles, copays, and coinsurance, which remain unchanged from the original plan. For a family with frequent medical needs, these costs can add up quickly. For example, a plan with a $3,000 deductible and 20% coinsurance could result in thousands of dollars in additional expenses annually. To afford COBRA, individuals must budget not just for premiums but also for these potential out-of-pocket costs, making it essential to evaluate overall financial health and explore alternatives like ACA marketplace plans or short-term health insurance.

Practical strategies can help mitigate COBRA costs. First, assess eligibility for premium tax credits through the ACA marketplace, which may offer more affordable options. Second, negotiate payment plans with the insurance provider to spread out premiums. Third, consider health savings accounts (HSAs) or flexible spending accounts (FSAs) to cover medical expenses tax-free. Finally, evaluate the necessity of maintaining the same level of coverage—opting for a higher-deductible plan might reduce monthly premiums, though it increases financial risk. By combining these strategies, individuals can make COBRA more manageable, if not entirely affordable.

Life Insurance at 90: Is It Possible to Get Covered?

You may want to see also

Explore related products

![]()

Eligibility Requirements: Determine who qualifies for COBRA, including employees, spouses, and dependent children

COBRA insurance, an acronym for the Consolidated Omnibus Budget Reconciliation Act, is a lifeline for many who face the sudden loss of employer-sponsored health coverage. However, not everyone is eligible for this continuation coverage. Understanding who qualifies is the first step in navigating the affordability challenge. Eligibility hinges on specific criteria, primarily centered around employment status and relationship to the covered employee.

Employees are the cornerstone of COBRA eligibility. To qualify, an employee must have been covered under a group health plan offered by an employer with 20 or more employees. The termination of employment, whether voluntary or involuntary (excluding gross misconduct), triggers the right to elect COBRA. For instance, a software engineer laid off during a company restructuring would qualify, while someone fired for theft would not. The key is the reason for separation—it must not be due to severe misconduct.

Spouses gain eligibility through their relationship to the covered employee. If the employee loses their job or experiences a reduction in hours, the spouse can continue coverage under COBRA. Additionally, divorce or the death of the covered employee also triggers eligibility for the spouse. For example, if a teacher’s spouse passes away, the surviving spouse can elect COBRA to maintain health insurance for themselves and their children.

Dependent children are another critical group. They qualify if they were covered under the employee’s plan and remain dependents as defined by the plan’s rules. This typically includes children under 26 years old, though some plans may have different age limits or include disabled dependents regardless of age. For instance, a college student covered under their parent’s plan would qualify for COBRA if the parent loses their job.

Understanding these eligibility requirements is essential, as it determines who can access COBRA and, by extension, who needs to explore affordability options. For those who qualify, the next step is to assess the financial burden and seek strategies to mitigate costs, such as subsidies, alternative plans, or short-term coverage. Eligibility is the gatekeeper—without it, COBRA is not an option, but with it, the journey to affordability begins.

Secure Your Ride: Insuring Your Road Bike Against Outdoor Theft

You may want to see also

Explore related products

![]()

Alternative Coverage Options: Explore ACA plans, short-term insurance, or state-sponsored programs as cost-effective alternatives

COBRA insurance, while a lifeline for many, often comes with a hefty price tag, leaving individuals and families scrambling for more affordable alternatives. Fortunately, the healthcare landscape offers several cost-effective options that can provide adequate coverage without breaking the bank. Among these, Affordable Care Act (ACA) plans, short-term health insurance, and state-sponsored programs stand out as viable alternatives. Each option caters to different needs, financial situations, and coverage durations, making it essential to understand their nuances.

ACA plans, also known as Obamacare, are a cornerstone of affordable health insurance for many Americans. These plans are available through the Health Insurance Marketplace and offer comprehensive coverage, including essential health benefits like preventive care, prescription drugs, and hospitalization. One of the most significant advantages of ACA plans is the availability of subsidies for individuals and families with incomes between 100% and 400% of the federal poverty level. For example, a family of four earning up to $106,000 annually in 2023 may qualify for premium tax credits, drastically reducing monthly premiums. To explore this option, visit Healthcare.gov during the annual Open Enrollment Period (typically November 1 to January 15) or during a Special Enrollment Period if you experience a qualifying life event, such as losing job-based coverage.

Short-term health insurance is another alternative, ideal for those who need temporary coverage while transitioning between jobs or waiting for ACA plan eligibility. These plans typically last up to 12 months (with the option to renew for up to 36 months in some states) and offer lower premiums than COBRA or ACA plans. However, they come with significant trade-offs: they often exclude pre-existing conditions, cap coverage amounts, and may not cover essential health benefits. For instance, a 30-year-old in good health might pay as little as $50–$100 per month for a short-term plan, but it could leave them vulnerable to high out-of-pocket costs if they require extensive medical care. Before choosing this route, carefully assess your health needs and financial risk tolerance.

State-sponsored programs provide a safety net for low-income individuals and families who may not qualify for ACA subsidies or find COBRA unaffordable. Medicaid, for example, is a joint federal and state program that offers free or low-cost health coverage to eligible individuals, including children, pregnant women, parents, and adults with disabilities. Eligibility criteria vary by state, but in states that expanded Medicaid under the ACA, individuals earning up to 138% of the federal poverty level ($18,754 for an individual in 2023) may qualify. Additionally, some states offer their own health insurance programs or subsidies for residents who fall into coverage gaps. For instance, New York’s Essential Plan provides low-cost coverage to individuals earning up to 200% of the federal poverty level. Research your state’s offerings through its health department or marketplace website to determine eligibility and apply.

In conclusion, while COBRA insurance provides continuity of coverage, its cost often makes it impractical for many. By exploring ACA plans, short-term insurance, or state-sponsored programs, individuals can find more affordable alternatives tailored to their specific circumstances. ACA plans offer comprehensive coverage with potential subsidies, short-term insurance provides temporary relief at lower costs (albeit with limitations), and state-sponsored programs ensure that low-income individuals are not left without options. Each alternative requires careful consideration of your health needs, budget, and eligibility, but with the right approach, affordable coverage is within reach.

Employer Life Insurance: Sign-up and Benefits Explained

You may want to see also

Explore related products

![Cobra - Collector's Edition [Blu-ray]](https://m.media-amazon.com/images/I/81mc0ZQlTvL._AC_UY218_.jpg)

![]()

Financial Assistance: Investigate subsidies, tax credits, or employer-provided support to offset COBRA premiums

COBRA insurance, while a lifeline for many, often comes with premiums that can strain even the most carefully planned budgets. Fortunately, financial assistance options exist to help offset these costs, making continued coverage more accessible. One of the most effective strategies involves investigating subsidies, tax credits, and employer-provided support.

Subsidies can significantly reduce COBRA premiums, particularly for those who qualify for government assistance programs. For instance, individuals who have experienced a reduction in work hours or job loss might be eligible for subsidies through the Consolidated Omnibus Budget Reconciliation Act (COBRA) itself, especially during periods of economic downturn. Additionally, state-specific programs may offer further relief, so it’s crucial to research local resources.

Tax credits are another powerful tool to offset COBRA costs. The Premium Tax Credit, available through the Affordable Care Act (ACA), can be claimed if your income falls within certain thresholds. For example, a family of four earning up to $106,000 annually in 2023 might qualify for this credit. To maximize this benefit, consult a tax professional or use online calculators to estimate your eligibility and potential savings.

Employer-provided support is often overlooked but can be a game-changer. Some employers offer partial or full coverage of COBRA premiums as part of severance packages or transitional benefits. Even if not explicitly offered, it’s worth negotiating with your former employer, especially if you’ve been a long-term or high-performing employee. Additionally, some companies provide Health Reimbursement Arrangements (HRAs) that can be used to cover COBRA costs.

To navigate these options effectively, start by reviewing your eligibility for subsidies and tax credits through government portals or healthcare marketplaces. Simultaneously, reach out to your former employer’s HR department to inquire about any available support. Combining these strategies can dramatically reduce the financial burden of COBRA, ensuring you maintain essential health coverage during transitions.

In conclusion, while COBRA premiums may seem daunting, subsidies, tax credits, and employer-provided support offer viable pathways to affordability. Proactive research and strategic planning can turn these options into tangible savings, making continued coverage not just possible, but manageable.

Life Flight Insurance: Worth the Cost?

You may want to see also

Explore related products

![Cobra Special Edition [Blu-Ray, Region Free]](https://m.media-amazon.com/images/I/71576GZ1TvL._AC_UY218_.jpg)

![]()

Duration of Coverage: Understand COBRA’s 18-36 month limit and plan for long-term insurance needs

COBRA insurance, while a lifeline for many, comes with a built-in expiration date. Understanding the 18- to 36-month coverage limit is crucial for anyone relying on it. This finite window demands proactive planning to avoid a sudden loss of coverage.

Let’s break down the timeline. COBRA typically lasts 18 months, but certain qualifying events (like a spouse’s death or divorce) can extend it to 36 months. For individuals with pre-existing conditions or those in transitional periods, this extension can be invaluable. However, even 36 months is a temporary solution. The clock starts ticking from the date of the qualifying event, not when you enroll, so timely action is essential.

Planning for the end of COBRA coverage requires a multi-pronged approach. First, research alternative insurance options well before the cutoff date. This includes employer-sponsored plans (if available), Affordable Care Act (ACA) marketplace plans, or short-term health insurance. Second, factor in costs. COBRA premiums are often high because you pay the full cost plus a 2% administrative fee. Transitioning to a more affordable plan can significantly ease financial strain.

For those with ongoing medical needs, timing is critical. If you’re in the middle of treatment, ensure your new plan covers your providers and medications. The ACA prohibits denying coverage for pre-existing conditions, but specific treatments or specialists may not be included in every plan. Use the annual Open Enrollment Period (typically November 1 to December 15) to explore ACA options, or qualify for a Special Enrollment Period if you lose COBRA coverage mid-year.

Finally, consider long-term strategies. Building an emergency fund to cover out-of-pocket costs during transitions can provide peace of mind. Additionally, if you’re self-employed or between jobs, joining a professional association or union may offer group health insurance at reduced rates. COBRA’s time limit is non-negotiable, but with careful planning, you can bridge the gap to sustainable coverage.

How to Get Life Insurance for Your Uncle

You may want to see also

Frequently asked questions

COBRA (Consolidated Omnibus Budget Reconciliation Act) insurance allows individuals to continue their employer-sponsored health insurance after leaving a job, but the individual must pay the full premium, including the portion previously covered by the employer, plus an administrative fee.

People afford COBRA insurance by budgeting carefully, using savings, or exploring alternatives like ACA marketplace plans, which may offer subsidies based on income. Some also seek short-term health plans or state-specific programs for lower costs.

While COBRA itself does not offer financial assistance, individuals may qualify for premium tax credits through the ACA marketplace if they meet income eligibility requirements. Additionally, some states offer programs to help offset COBRA costs.