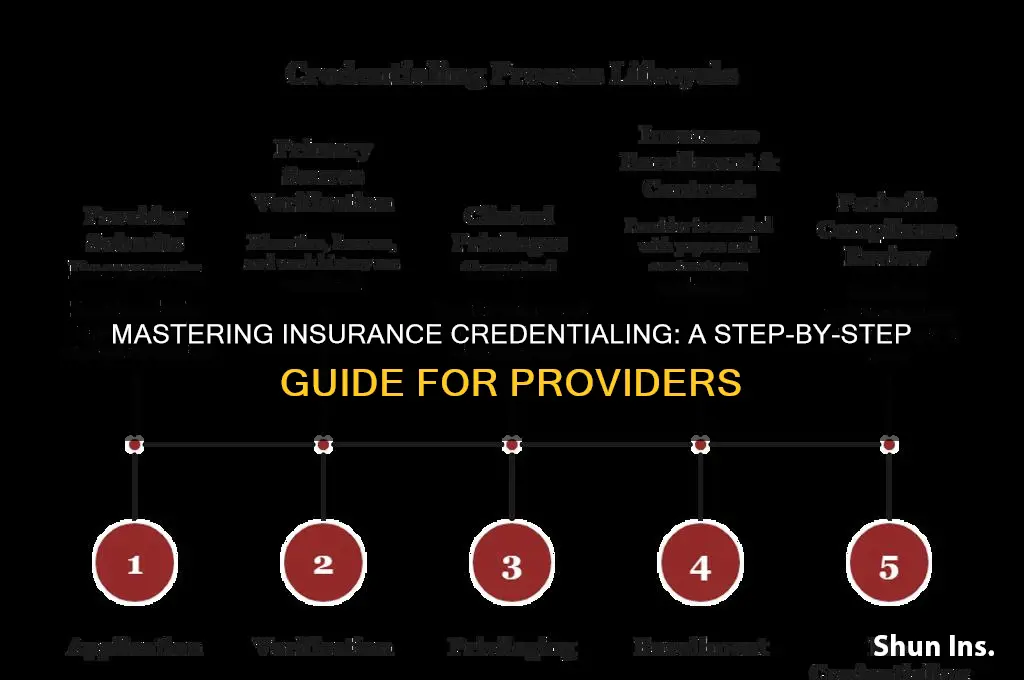

Insurance credentialing is a critical process for healthcare providers to establish and maintain their ability to accept insurance payments from specific carriers. It involves submitting detailed information about the provider’s qualifications, education, training, and practice history to insurance companies for verification and approval. This process ensures that providers meet the insurer’s standards and are eligible to participate in their network, allowing them to bill for services rendered to insured patients. Credentialing typically includes primary source verification, background checks, and compliance with state and federal regulations. While time-consuming and often complex, successful credentialing is essential for providers to expand their patient base, streamline reimbursement, and ensure long-term practice sustainability.

| Characteristics | Values |

|---|---|

| Definition | Process of verifying a healthcare provider’s qualifications to join an insurance network. |

| Purpose | Ensures providers meet insurer standards for patient care and billing. |

| Key Steps | 1. Application Submission 2. Documentation Verification 3. Background Checks 4. Contract Negotiation 5. Final Approval |

| Required Documents | - Medical license - DEA registration - CV/resume - Malpractice insurance - Education/training certificates |

| Timeframe | Typically 90–120 days, varies by insurer. |

| Cost | Application fees range from $0 to $500+ per insurer. |

| Primary Organizations Involved | CAQH (Council for Affordable Quality Healthcare), Insurance Companies |

| Common Challenges | Delays in documentation, incomplete applications, insurer-specific requirements. |

| Renewal Frequency | Every 1–3 years, depending on insurer policies. |

| Impact of Non-Compliance | Ineligibility to bill insurance, loss of in-network status. |

| Tools/Platforms | CAQH ProView, PECOS (Provider Enrollment, Chain, and Ownership System) |

| Regulatory Bodies | State Medical Boards, CMS (Centers for Medicare & Medicaid Services) |

| Outsourcing Option | Credentialing services available to streamline the process. |

| Importance | Ensures provider legitimacy, reduces claim denials, and expands patient base. |

Explore related products

What You'll Learn

- Gather Provider Information: Collect NPI, licenses, education, and work history details for credentialing

- Verify Credentials: Confirm licenses, certifications, and education through primary sources and databases

- Complete Applications: Fill out payer-specific forms accurately and submit required documents

- Primary Source Verification: Contact schools, boards, and hospitals to validate provider credentials

- Monitor Re-Credentialing: Track expiration dates and update credentials periodically to maintain compliance

![]()

Gather Provider Information: Collect NPI, licenses, education, and work history details for credentialing

The foundation of insurance credentialing lies in meticulous provider data collection. Think of it as assembling a puzzle: each piece – the National Provider Identifier (NPI), licenses, education, and work history – is crucial for a complete picture of a provider's qualifications. Missing even one fragment can delay or derail the entire credentialing process.

Every provider, regardless of specialty or experience, must have a unique NPI. This 10-digit identifier acts as a universal key, unlocking access to insurance networks. Verify its accuracy through the National Plan and Provider Enumeration System (NPPES) database to avoid rejections due to typos or outdated information.

Licenses are the legal backbone of a provider's practice. Collect state-specific licenses, ensuring they are current and unrestricted. Be mindful of expiration dates and renewal requirements, as lapsed licenses are a red flag for insurers. Don't forget to gather DEA registration numbers for providers prescribing controlled substances, another critical credential.

Education and training history paint a picture of a provider's expertise. Request detailed transcripts, residency completion certificates, and board certifications. For specialists, verify fellowship training and any subspecialty qualifications. This documentation demonstrates a provider's competency and adherence to industry standards.

Work history provides context and continuity. A chronological record of employment, including dates, positions held, and supervising physicians (if applicable), is essential. Gaps in employment should be explained, and any disciplinary actions or malpractice claims must be disclosed. Transparency is key; omissions can lead to serious consequences during the credentialing review.

Life Insurance for Seniors: Choosing the Right Policy

You may want to see also

Explore related products

![]()

Verify Credentials: Confirm licenses, certifications, and education through primary sources and databases

Credential verification is the backbone of insurance credentialing, ensuring providers meet regulatory standards and deliver competent care. Begin by identifying primary sources for each credential type. For licenses, consult state medical or professional boards, which maintain up-to-date records of active, suspended, or revoked statuses. For certifications, verify through issuing organizations like the American Board of Medical Specialties (ABMS) or the American Heart Association (AHA). Education credentials require direct confirmation from accredited institutions, often via the National Student Clearinghouse or university registrars. Cross-reference these sources against databases such as the National Practitioner Data Bank (NPDB) to uncover malpractice claims or disciplinary actions. This multi-layered approach minimizes errors and ensures compliance with payer requirements.

The process demands meticulous attention to detail. Start by requesting signed releases from providers to access their credentials legally. For licenses, note expiration dates and renewal requirements, as some states mandate continuing education units (CEUs) for renewal. Certifications often have recertification cycles, such as the 10-year requirement for many ABMS specialties. When verifying education, confirm degree types (e.g., MD, DNP) and graduation dates, as discrepancies can flag potential fraud. Use standardized forms to document findings, ensuring consistency across all verifications. Tools like the Council for Higher Education Accreditation (CHEA) database can streamline verification of educational institutions.

A comparative analysis reveals the risks of skipping primary source verification. Relying solely on self-reported data or third-party aggregators can lead to oversight of critical issues, such as expired licenses or falsified certifications. For instance, a 2022 study found that 12% of provider credentials contained inaccuracies when verified through primary sources. Payers often reject applications with unverified credentials, delaying enrollment and revenue. Conversely, thorough verification not only satisfies payer requirements but also protects patients by ensuring providers are qualified. The investment in time and resources pays dividends in credibility and compliance.

Persuasively, consider the ethical and legal implications of inadequate verification. Providers with lapsed licenses or fraudulent certifications pose significant risks, from denied claims to malpractice lawsuits. Payers may hold credentialing entities liable for insufficient due diligence, leading to financial penalties or reputational damage. By prioritizing primary source verification, organizations demonstrate a commitment to integrity and patient safety. Implement a checklist system to track each verification step, ensuring no credential is overlooked. Regular audits of verified credentials further safeguard against oversight, creating a robust credentialing process.

Practically, leverage technology to streamline verification. Automated platforms like CAQH ProView and CredentialStream integrate with primary sources and databases, reducing manual effort and errors. Set reminders for expiring credentials to initiate re-verification proactively. For international providers, use the Educational Commission for Foreign Medical Graduates (ECFMG) to validate medical education and certification equivalency. Train staff on verification protocols and red flags, such as inconsistent dates or unrecognized institutions. By combining human oversight with technological efficiency, organizations can achieve thorough, timely credential verification that meets industry standards.

Insuring Your Teen Driver: Essential Coverage for 16-Year-Olds Explained

You may want to see also

Explore related products

![]()

Complete Applications: Fill out payer-specific forms accurately and submit required documents

Accurate and complete applications are the cornerstone of successful insurance credentialing. Each payer has unique forms and requirements, and even minor errors can lead to delays or denials. For instance, a missing tax identification number or an outdated license can halt the process entirely. To avoid such pitfalls, start by carefully reviewing the payer’s credentialing checklist, which typically includes documents like state licenses, DEA certificates, malpractice insurance, and CVs. Treat this step as a meticulous audit, ensuring every field is filled correctly and every document is current.

Consider the process of filling out payer-specific forms as a tailored task, not a one-size-fits-all approach. For example, Medicare requires a PECOS application, while private insurers like UnitedHealthcare may demand additional contractual agreements. Use the payer’s portal or website to download the latest versions of these forms, as outdated templates often lead to rejections. When inputting data, double-check details like practice addresses, NPI numbers, and taxonomy codes. A single typo in the NPI can render the entire application invalid, so cross-reference with official databases like NPPES to ensure accuracy.

Submitting required documents is equally critical, but it’s not just about attaching files. Payers often have specific formatting and naming conventions for uploads. For instance, some may require PDFs under 2MB, while others accept only JPEGs. Organize documents in a clear folder structure on your computer, labeling files descriptively (e.g., “Smith_MalpracticeInsurance_2023”). If submitting via mail, use certified delivery to track receipt and avoid claims of lost paperwork. Pro tip: Maintain a master credentialing spreadsheet to log submission dates, payer contacts, and follow-up actions for each application.

A common oversight is failing to update documents proactively. Licenses and certifications expire, and payers frequently reject applications with documents nearing their end date. Set calendar reminders 60–90 days before expiration to renew and resubmit. Similarly, if your practice undergoes changes—like adding a new location or provider—notify payers immediately. Failure to do so can result in claims denials or even termination from the network. Think of credentialing as a living process, not a one-time task.

Finally, leverage technology to streamline this process. Credentialing software like MDCredential or Intellicred can auto-fill forms, track deadlines, and flag missing documents. While these tools require an initial investment, they save hours of manual work and reduce errors. Pair this with a dedicated credentialing specialist or team to handle submissions and follow-ups. By combining precision, organization, and technology, you’ll transform a tedious process into a manageable, error-free workflow.

Check Your AT&T Insurance Coverage: A Quick and Easy Guide

You may want to see also

Explore related products

![]()

Primary Source Verification: Contact schools, boards, and hospitals to validate provider credentials

Primary source verification is the backbone of insurance credentialing, ensuring that healthcare providers meet the stringent standards required to participate in payer networks. This process involves directly contacting the institutions that issued or oversee a provider’s credentials—schools, licensing boards, and hospitals—to confirm their qualifications. Without this step, the risk of accepting fraudulent or outdated credentials skyrockets, potentially exposing patients to unqualified care and insurers to legal liabilities. It’s not just a checkbox; it’s a critical safeguard.

To execute primary source verification effectively, start by identifying the key entities to contact. For medical degrees, reach out to the provider’s graduating medical school to confirm the degree and graduation date. Licensing boards are next—verify the provider’s license status, issue date, and any disciplinary actions. Hospitals where the provider has privileges should be contacted to confirm their affiliation and standing. Use standardized forms or direct communication (email, phone, or secure portals) to streamline the process. Pro tip: Maintain a log of all verification attempts, including dates, contacts, and responses, to ensure accountability and compliance with regulatory requirements.

One common pitfall in primary source verification is relying solely on secondary sources, such as CVs or third-party databases, which can contain errors or omissions. For instance, a provider might list a board certification that expired years ago, or a hospital affiliation that ended due to performance issues. Direct verification eliminates these risks. Another challenge is the time-consuming nature of the process, as institutions may take weeks to respond. To mitigate delays, prioritize verifications based on urgency (e.g., licenses over CME credits) and use automated tools where possible. Remember, thoroughness trumps speed—rushing this step can lead to costly mistakes.

Comparing primary source verification to other credentialing methods highlights its superiority. While self-reported data or database checks are faster, they lack the reliability of direct confirmation. For example, the Federation Credentials Verification Service (FCVS) offers a centralized repository of verified credentials, but even this requires initial primary source verification. Similarly, the National Practitioner Data Bank (NPDB) flags disciplinary actions but doesn’t confirm qualifications. By anchoring your process in primary source verification, you build a credentialing foundation that’s both robust and defensible.

In conclusion, primary source verification is non-negotiable in insurance credentialing. It transforms uncertainty into assurance, ensuring providers meet the highest standards of care. By systematically contacting schools, boards, and hospitals, you not only protect patients and insurers but also streamline the credentialing process for the long term. Invest the time upfront—the payoff in trust, compliance, and risk mitigation is immeasurable.

Life Insurance: Protecting Your Family's Future

You may want to see also

![]()

Monitor Re-Credentialing: Track expiration dates and update credentials periodically to maintain compliance

Re-credentialing is a critical yet often overlooked aspect of insurance credentialing. Unlike the initial credentialing process, which establishes a provider’s eligibility to participate in a payer network, re-credentialing ensures ongoing compliance with evolving standards and regulations. Failure to monitor and update credentials periodically can result in network termination, revenue loss, and legal liabilities. For instance, a 2022 study by the American Medical Association found that 22% of providers faced delays in reimbursement due to outdated credentials. This underscores the need for a proactive approach to re-credentialing.

To effectively monitor re-credentialing, start by creating a centralized tracking system for expiration dates. Utilize credentialing software or a spreadsheet to log key dates, such as license renewals, DEA registrations, and malpractice insurance expirations. Set automated reminders 90, 60, and 30 days before each deadline to allow ample time for renewal. For example, if a provider’s state medical license expires on December 31, the first reminder should be sent by October 1. Additionally, assign a dedicated staff member to oversee this process, ensuring accountability and consistency.

A common pitfall in re-credentialing is relying solely on providers to self-report updates. Instead, implement a verification process that cross-references primary sources, such as state licensing boards and the National Practitioner Data Bank. This dual-check system minimizes errors and ensures compliance with payer requirements. For instance, a payer may mandate that providers submit proof of CME credits within 60 days of re-credentialing. By verifying these details independently, you reduce the risk of non-compliance and potential audits.

Finally, treat re-credentialing as an opportunity to reassess provider qualifications and network fit. Periodically review performance metrics, patient satisfaction scores, and disciplinary histories to ensure providers align with organizational standards. For example, if a provider has received multiple malpractice claims in the past year, this may warrant further investigation or corrective action. By integrating re-credentialing into a broader quality management framework, you not only maintain compliance but also enhance the overall integrity of your network.

How Insurance Companies Determine Value: A Comprehensive Guide

You may want to see also

Frequently asked questions

Insurance credentialing is the process of verifying a healthcare provider’s qualifications, education, training, and licenses to ensure they meet the standards required by insurance companies. It is necessary because it allows providers to participate in insurance networks, enabling them to accept and bill insurance plans for patient services.

The credentialing process can take anywhere from 60 to 120 days, depending on the insurance company, the completeness of the application, and the complexity of the provider’s background. Delays often occur due to missing documentation or backlogs at the insurance company.

Required documents typically include a completed credentialing application, a copy of the provider’s medical license, DEA registration (if applicable), malpractice insurance certificate, CV or resume, education and training certificates, and board certification documentation.

While it’s possible to handle credentialing independently, many providers opt to hire credentialing services to save time and avoid errors. Professionals are familiar with the process, requirements, and common pitfalls, which can expedite approval and reduce frustration.