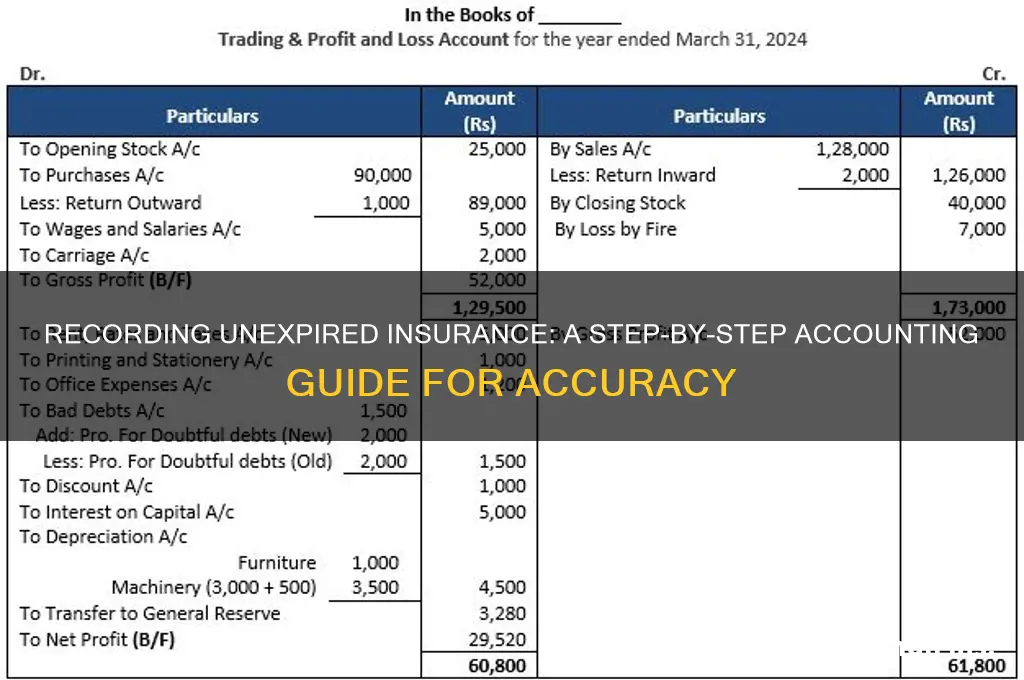

Recording unexpired insurance is a critical accounting process that ensures accurate financial reporting by recognizing the portion of prepaid insurance that has not yet been used or expired. When a business pays for insurance coverage in advance, the full amount is initially recorded as a prepaid asset. As time passes and the insurance coverage is consumed, a portion of the prepaid insurance is systematically transferred to an expense account, typically on a monthly basis. This process aligns with the matching principle in accounting, which requires expenses to be recognized in the same period as the revenues they help generate. To record unexpired insurance, an adjusting journal entry is made at the end of each accounting period, debiting the insurance expense account and crediting the prepaid insurance account for the amount corresponding to the coverage used during that period. Properly managing unexpired insurance ensures that financial statements reflect the true financial position and operational costs of the business.

| Characteristics | Values |

|---|---|

| Definition | Unexpired insurance refers to the portion of a prepaid insurance premium that has not yet been used or expired. It represents the amount of insurance coverage that remains in effect for a future period. |

| Accounting Treatment | Recorded as a current asset on the balance sheet under the "Prepaid Expenses" or "Other Current Assets" section. |

| Recognition | Recognized when insurance premiums are paid in advance for a period extending beyond the current accounting period. |

| Calculation | Calculated as the total prepaid insurance premium multiplied by the fraction of the coverage period that remains unexpired. |

| Formula | Unexpired Insurance = Total Prepaid Premium × (Remaining Months / Total Months of Coverage) |

| Journal Entry (Initial) | Debit: Prepaid Insurance (Asset) / Credit: Cash (or Bank) |

| Journal Entry (Adjustment) | Debit: Insurance Expense (Expense) / Credit: Prepaid Insurance (Asset) |

| Reporting Frequency | Adjusted periodically (e.g., monthly, quarterly) to reflect the portion of insurance consumed during the accounting period. |

| Example | If a $1,200 annual insurance premium is paid in January for coverage from January to December, $1,000 would be unexpired insurance at the end of February ($1,200 × 10/12). |

| Purpose | Ensures accurate matching of expenses with revenues in the accounting period when the insurance benefit is actually consumed. |

| Compliance | Follows the matching principle and GAAP/IFRS guidelines for prepaid expenses. |

Explore related products

![Audacity - Sound and Music Editing and Recording Software - Download Version [Download]](https://m.media-amazon.com/images/I/B1WE7w810rS._AC_UY218_.png)

![WavePad Audio Editing Software - Professional Audio and Music Editor for Anyone [Download]](https://m.media-amazon.com/images/I/B1fcLEGCs6S._AC_UY218_.png)

What You'll Learn

![]()

Journal Entry for Prepaid Insurance

Recording prepaid insurance in your accounting books is a critical step in accurately reflecting your business’s financial health. When a company pays for insurance coverage in advance, the full amount is not immediately expensed. Instead, it is initially recorded as an asset, recognizing that the benefit of the insurance will be realized over time. The journal entry for prepaid insurance involves debiting the prepaid insurance account (an asset) and crediting the cash account (or the payment method used). For example, if a company pays $12,000 for a one-year insurance policy, the entry would be: *Debit Prepaid Insurance $12,000, Credit Cash $12,000*. This ensures the asset is properly accounted for until the insurance coverage is consumed.

As time passes and the insurance coverage is used, the prepaid insurance asset is gradually converted into an expense. This is done through an adjusting entry at the end of each accounting period. For instance, if one month of the $12,000 policy has been used, the adjusting entry would be: *Debit Insurance Expense $1,000, Credit Prepaid Insurance $1,000*. This process aligns with the matching principle, ensuring expenses are recognized in the same period as the revenue they help generate. Failing to make this adjustment would overstate assets and understate expenses, distorting financial statements.

A common mistake in recording prepaid insurance is treating the entire payment as an immediate expense. This error can lead to an inaccurate portrayal of a company’s liquidity and profitability. To avoid this, businesses should establish a clear system for tracking prepaid expenses and their expiration dates. For example, using accounting software with reminders for adjusting entries can streamline the process. Additionally, segregating prepaid insurance from other expenses in financial reports enhances transparency and simplifies audits.

Comparing prepaid insurance to other prepaid expenses, such as rent or supplies, highlights its unique treatment. While the initial recording is similar (debiting an asset and crediting cash), the periodic adjustment for insurance is often more straightforward because the coverage period is typically fixed. In contrast, prepaid rent may require prorated adjustments based on lease terms. Understanding these nuances ensures consistency and accuracy in financial reporting. By mastering the journal entry for prepaid insurance, businesses can maintain reliable records and make informed financial decisions.

How to Provide Your Insurance Information to CVS: A Step-by-Step Guide

You may want to see also

Explore related products

![Recordpad Professional Sound Recorder Software [PC Online code]](https://m.media-amazon.com/images/I/71e+rLjOPfL._AC_UY218_.jpg)

![]()

Calculating Unexpired Insurance Amount

Recording unexpired insurance is a critical task for businesses to ensure accurate financial reporting and asset management. At the heart of this process lies the calculation of the unexpired insurance amount, which represents the portion of a prepaid insurance policy that has not yet been used or expired. This calculation is essential for allocating the correct value of insurance expense to each accounting period, adhering to the matching principle in accounting.

Understanding the Calculation

To calculate the unexpired insurance amount, start by determining the total cost of the insurance policy and its coverage period. For instance, if a company pays $12,000 for a one-year policy, divide this amount by 12 to find the monthly expense ($1,000). If the policy is recorded in January but only six months have passed, the unexpired amount would be $6,000 ($1,000/month × 6 months remaining). This straightforward prorated method ensures that expenses are recognized evenly over the policy term.

Practical Steps and Tools

Begin by gathering the insurance policy documents, noting the start and end dates, and the total premium paid. Use a spreadsheet or accounting software to automate the calculation, reducing the risk of errors. For example, in QuickBooks, you can set up a prepaid expense account and allocate the cost over the policy period. Always cross-verify the remaining period against the policy schedule to ensure accuracy.

Common Pitfalls to Avoid

One common mistake is failing to adjust for partial months or irregular policy periods. For instance, if a policy starts mid-month, prorate the first month’s expense accordingly. Another error is neglecting to update the unexpired amount if the policy is canceled or modified. Regularly review the insurance ledger to reflect any changes, ensuring compliance with accounting standards like GAAP or IFRS.

Real-World Application and Takeaway

Consider a small business that purchases a $3,000 six-month insurance policy in April. By October, $1,500 would remain unexpired. Recording this amount in the balance sheet as a current asset ensures the business accurately reflects its prepaid expenses. This practice not only maintains financial transparency but also aids in budgeting and cash flow management. Mastering this calculation is a cornerstone of sound financial stewardship, enabling businesses to align their insurance costs with the periods they benefit from the coverage.

Understanding SR22 Insurance Requirements in Alabama: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Adjusting Entries for Insurance Expense

Recording unexpired insurance is a critical task in accounting, ensuring that financial statements accurately reflect the portion of prepaid insurance that hasn’t yet been used. Adjusting entries for insurance expense are essential to this process, as they allocate the cost of insurance over the periods it benefits. Without these adjustments, expenses would be misstated, leading to distorted financial results. For instance, if a company pays $12,000 annually for insurance in January, only $1,000 should be expensed each month, with the remaining $11,000 recorded as a prepaid asset. This principle aligns with the matching principle in accounting, which requires expenses to be recognized in the same period as the revenues they help generate.

To make an adjusting entry for insurance expense, follow these steps: first, determine the total cost of the insurance policy and its coverage period. Next, calculate the monthly or periodic expense by dividing the total cost by the number of months covered. For example, a $6,000 policy covering six months would result in a $1,000 monthly expense. Then, debit the Insurance Expense account for the appropriate amount and credit the Prepaid Insurance account. This reduces the prepaid asset while recognizing the expense in the current period. Failing to make this adjustment would overstate assets and understate expenses, violating accounting standards.

A common mistake in recording unexpired insurance is treating the entire payment as an immediate expense. This error is particularly prevalent in small businesses or those without robust accounting systems. To avoid this, maintain a clear schedule of prepaid expenses, noting the start and end dates of each policy. For example, if a policy begins on October 1 and covers 12 months, the adjusting entry should be made monthly until September 30. Additionally, leverage accounting software that automates these entries, reducing the risk of human error. Regularly reviewing these entries ensures consistency and accuracy in financial reporting.

Comparing the treatment of unexpired insurance with other prepaid expenses highlights its unique challenges. While rent or supplies may have straightforward consumption patterns, insurance often spans multiple accounting periods, requiring precise allocation. For instance, a quarterly rent payment is typically expensed evenly over three months, but an annual insurance policy demands monthly adjustments. This complexity underscores the need for meticulous record-keeping and a deep understanding of accounting principles. By mastering adjusting entries for insurance expense, businesses can maintain financial integrity and make informed decisions based on accurate data.

In conclusion, adjusting entries for insurance expense are a cornerstone of proper accounting, ensuring that prepaid insurance is recognized systematically over time. By following structured steps, avoiding common pitfalls, and leveraging technology, businesses can streamline this process. The result is not only compliance with accounting standards but also a clearer financial picture that supports strategic planning and transparency. Whether you’re a small business owner or a seasoned accountant, mastering this adjustment is indispensable for financial accuracy.

Columbus Life Insurance: Where is it Located?

You may want to see also

Explore related products

![]()

Recording Insurance in Balance Sheet

Unexpired insurance represents the portion of a prepaid insurance policy that hasn’t yet been consumed by the passage of time. Recording it correctly on the balance sheet ensures financial statements reflect the true value of assets and liabilities. This is achieved by separating the expired portion, which is expensed, from the unexpired portion, which remains as an asset. For example, if a company pays $12,000 annually for insurance in January, only $1,000 should be expensed each month, while the remaining $11,000 is recorded as a prepaid asset.

To record unexpired insurance, follow these steps: First, determine the total cost of the insurance policy. Next, calculate the monthly or periodic expense based on the policy term. Then, debit the Prepaid Insurance account (an asset) for the full amount paid and credit Cash for the same amount. Each period, debit Insurance Expense and credit Prepaid Insurance for the portion of the policy that has expired. This method ensures the balance sheet accurately reflects the unexpired insurance as a current asset until it is fully consumed.

A common mistake in recording unexpired insurance is treating the entire premium as an immediate expense. This distorts both the income statement and balance sheet, overstating expenses and understating assets. For instance, expensing the full $12,000 in January instead of amortizing it over 12 months would misrepresent the company’s financial health. Proper allocation requires discipline and a clear understanding of the policy’s term and payment structure.

Comparatively, unexpired insurance is similar to other prepaid expenses like rent or supplies, but its treatment is unique due to its direct impact on risk management. Unlike supplies, which deplete irregularly, insurance expires uniformly over time. This predictability allows for straightforward amortization, making it easier to track and record. However, companies must remain vigilant to adjust entries if the policy term changes or is canceled, ensuring accuracy in financial reporting.

In conclusion, recording unexpired insurance on the balance sheet is a critical task that requires precision and consistency. By treating it as a prepaid asset and systematically expensing the consumed portion, businesses maintain transparency and compliance with accounting standards. Practical tips include using accounting software to automate amortization schedules and regularly reviewing policies to align with reporting periods. This approach not only ensures accuracy but also provides a clear snapshot of the company’s financial obligations and resources.

Choosing Lemonade Insurance: A Smart Guide to Coverage and Benefits

You may want to see also

Explore related products

![]()

Amortization of Prepaid Insurance Over Time

Prepaid insurance represents a unique accounting challenge, as it embodies a future benefit paid for in advance. Amortization, the process of allocating this cost over time, ensures financial statements accurately reflect the expense incurred during a specific period. This method aligns with the matching principle, a cornerstone of accrual accounting, which dictates that expenses should be recognized in the same period as the revenues they help generate.

For instance, consider a company that purchases a 12-month insurance policy for $12,000 in January. Instead of recording the entire $12,000 as an expense in January, amortization spreads this cost evenly across the year, resulting in a monthly expense of $1,000. This approach provides a more accurate representation of the company's financial health by matching the insurance expense with the periods benefiting from the coverage.

The amortization process involves a straightforward journal entry. At the time of purchase, the prepaid insurance is recorded as an asset on the balance sheet. Each month, an adjusting entry is made to transfer a portion of the prepaid insurance to the insurance expense account. This entry debits insurance expense and credits prepaid insurance. The prepaid insurance account is reduced by the amortized amount each period until it reaches zero, at which point the entire prepaid amount has been expensed.

While the concept is simple, practical application requires careful consideration. The amortization period should align with the coverage period of the insurance policy. For example, a policy covering a specific project should be amortized over the project's duration, not necessarily over a calendar year. Additionally, businesses should review their prepaid insurance balances regularly to ensure accuracy and make adjustments for any changes in coverage or policy terms.

In conclusion, amortizing prepaid insurance over time is a crucial accounting practice that ensures financial statements accurately reflect the matching principle. By spreading the cost of insurance over the period it benefits, businesses provide a clearer picture of their financial performance and position. Understanding and correctly applying amortization techniques is essential for maintaining accurate financial records and making informed business decisions.

Understanding EI Insurable Earnings: A Step-by-Step Calculation Guide

You may want to see also

Frequently asked questions

Unexpired insurance refers to the portion of a prepaid insurance policy that has not yet expired or been used up. Recording it is important because it ensures that expenses are recognized in the correct accounting period, adhering to the matching principle and providing an accurate financial statement.

Unexpired insurance is recorded by initially recognizing the full prepaid amount as an asset. As the insurance coverage period progresses, the expired portion is periodically transferred to an expense account, reducing the prepaid asset balance.

At the time of payment, the journal entry is:

Debit: Prepaid Insurance (Asset)

Credit: Cash/Bank (Asset)

This reflects the payment made for the insurance policy.

Each month, the expired portion is recorded with the following journal entry:

Debit: Insurance Expense (Expense)

Credit: Prepaid Insurance (Asset)

This adjusts the prepaid asset and recognizes the expense for the period.