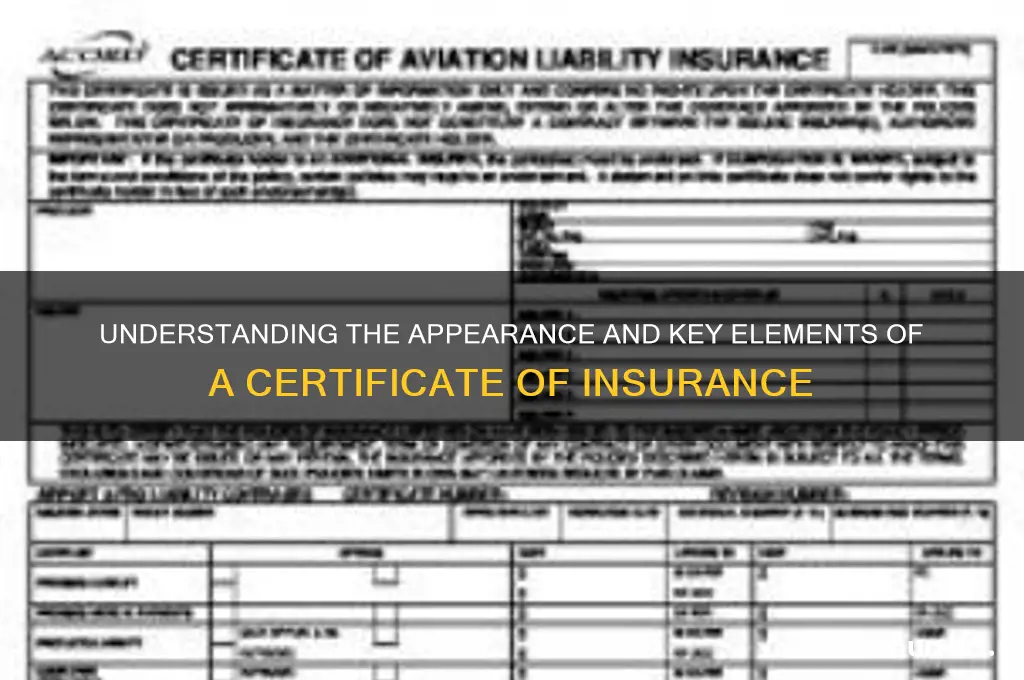

A certificate of insurance (COI) is a crucial document that provides proof of insurance coverage and outlines the key details of an insurance policy. Typically issued by an insurance company or broker, it serves as a concise summary of the policyholder’s coverage, including the policyholder’s name, the insurance provider, policy number, coverage limits, effective and expiration dates, and the type of coverage provided. The COI also lists additional insured parties, if applicable, and may include specific endorsements or exclusions. Designed to be easily understood, it is often required in business transactions, contracts, or regulatory compliance to ensure all parties are protected against potential risks. While the exact format may vary by insurer, a COI generally follows a standardized layout to ensure clarity and consistency.

Explore related products

What You'll Learn

- Key Components: Policy number, coverage details, effective dates, and insured parties listed clearly

- Issuer Information: Insurer’s name, contact details, and logo for authenticity verification

- Coverage Limits: Specific amounts for liability, property, or other insured risks outlined

- Certificate Holder: Name and address of the party requiring proof of insurance

- Additional Insured: Inclusion of other parties protected under the policy if applicable

![]()

Key Components: Policy number, coverage details, effective dates, and insured parties listed clearly

A certificate of insurance (COI) is a snapshot of an insurance policy, distilling complex coverage into a concise, verifiable document. Among its critical elements, the policy number stands as the unique identifier, akin to a social security number for the policy. This alphanumeric code is essential for insurers and insured parties to reference the specific contract, ensuring accuracy in claims processing or policy inquiries. Without it, verifying coverage details becomes a cumbersome, error-prone task.

Next, coverage details form the backbone of the COI, outlining the scope and limits of protection. This section typically includes the type of insurance (e.g., general liability, property, or workers’ compensation), coverage limits (e.g., $1 million per occurrence), and any deductibles or exclusions. For instance, a COI for a contractor might specify liability coverage of $2 million aggregate, with a $5,000 deductible for property damage claims. Clarity here is paramount, as ambiguities can lead to disputes or denied claims.

Effective dates are another non-negotiable component, defining the period during which the policy is active. These dates—typically listed as "from" and "to"—must align with the project or contractual requirements. A COI with coverage expiring before a project’s completion is worthless, exposing all parties to risk. For example, a COI for a construction project should extend beyond the anticipated completion date, often including a buffer period to account for delays.

Finally, the insured parties listed on the COI determine who is protected under the policy. This includes the policyholder (first named insured) and any additional insureds, such as clients or partners requiring coverage. For instance, a vendor’s COI might list a retailer as an additional insured to protect against liability arising from the vendor’s products. Omitting a required party renders the COI ineffective for contractual purposes, potentially voiding agreements.

In practice, these components must be presented clearly and consistently. A well-structured COI uses bold fonts for policy numbers, bullet points for coverage details, and distinct sections for dates and insured parties. For added precision, some COIs include a "description of operations" to contextualize the coverage, such as specifying that the policy covers "electrical work up to 120 volts." By adhering to these standards, a COI serves its purpose: providing irrefutable proof of insurance tailored to the needs of all stakeholders.

Whole Life Insurance: Does It Expire With Age?

You may want to see also

Explore related products

![]()

Issuer Information: Insurer’s name, contact details, and logo for authenticity verification

A certificate of insurance is a critical document that verifies coverage, and the issuer’s information is its cornerstone. Prominently displayed at the top or header, the insurer’s name serves as the primary identifier, often in bold or larger font to ensure immediate recognition. This is no mere formality—it’s the first line of defense against fraudulent documents. For instance, a certificate issued by "ABC Insurance Company" should match the name on the policyholder’s agreement, leaving no room for ambiguity. Without this clear, accurate identifier, the document’s legitimacy is instantly suspect.

Equally vital are the insurer’s contact details, typically listed alongside the name. These include a physical address, phone number, and often an email or website. This information isn’t just for show; it’s a practical tool for verification. If a certificate of insurance is presented in a business transaction or legal context, the recipient can directly contact the insurer to confirm its authenticity. For example, a quick call to the provided phone number can verify policy details, ensuring the coverage claimed is real and active. Omitting or obscuring these details raises red flags, as legitimate insurers have nothing to hide.

The insurer’s logo is another critical element, serving as a visual stamp of authenticity. Logos are difficult to replicate accurately, making them a powerful deterrent against fraud. A genuine certificate will feature a high-resolution logo, often in color, that matches the insurer’s branding across other official materials. For instance, the logo of "XYZ Insurance Group" should align with the design on their website, brochures, or policy documents. If the logo appears pixelated, distorted, or inconsistent, it’s a warning sign that the certificate may be counterfeit.

However, relying solely on visual cues isn’t foolproof. Fraudsters can mimic logos and contact details with increasing sophistication. That’s why cross-verification is essential. Recipients should use the provided contact information to confirm the certificate’s details directly with the insurer. For added security, some insurers include unique identifiers, such as policy numbers or QR codes, that link to a verification portal. These measures ensure that even if the logo and name appear legitimate, the document’s authenticity can be independently confirmed.

In practice, scrutinizing the issuer’s information is a simple yet effective way to safeguard against fraud. Start by comparing the insurer’s name and logo to known, official sources. Next, use the contact details to verify the policy’s existence and terms. Finally, look for additional security features, such as watermarks or holograms, that further validate the document. By treating the issuer’s information as more than just boilerplate text, you transform it into a powerful tool for ensuring the certificate of insurance is genuine and reliable.

Exam Duration for Life Insurance License: Coaching Essentials

You may want to see also

Explore related products

![]()

Coverage Limits: Specific amounts for liability, property, or other insured risks outlined

A certificate of insurance (COI) is a snapshot of an insurance policy, distilling complex coverage details into a concise, standardized format. Among its critical components, coverage limits stand out as the backbone of financial protection. These limits define the maximum amount an insurer will pay for a covered claim, whether it’s for liability, property damage, or other insured risks. Without clear limits, a COI loses its utility, leaving stakeholders vulnerable to misunderstandings or underinsurance.

Consider a commercial general liability policy with a $1 million per occurrence limit and a $2 million aggregate limit. These figures aren’t arbitrary—they reflect the policyholder’s risk exposure and the insurer’s commitment. For instance, if a contractor causes $1.5 million in property damage at a job site, the $1 million per occurrence limit would cap the insurer’s payout, leaving the contractor responsible for the remaining $500,000. This example underscores why verifying coverage limits on a COI is non-negotiable for anyone relying on the policy.

When reviewing a COI, look for limits in the "Coverage" or "Limits of Insurance" section. They’re typically broken down by coverage type, such as general liability, property, or workers’ compensation. For example, a COI might list $2 million for general liability, $500,000 for property damage, and $100,000 for medical payments. These figures should align with contractual requirements or industry standards. If a vendor’s COI shows a $500,000 liability limit but your project requires $1 million, request an endorsement to increase coverage or find another vendor.

One common pitfall is confusing aggregate limits with per-occurrence limits. The former caps total payouts over the policy period, while the latter limits payouts per claim. For instance, a policy with a $1 million per occurrence limit and a $2 million aggregate limit could cover two $1 million claims but would stop paying after that. Understanding this distinction is crucial for businesses with multiple claims risks, such as property managers or event organizers.

Finally, coverage limits aren’t static—they can be tailored to meet specific needs. Additional insureds, for example, may require higher limits to protect their interests. Similarly, businesses in high-risk industries might opt for umbrella policies to extend coverage beyond primary limits. When requesting a COI, specify the required limits to ensure compliance. A well-structured COI with accurate coverage limits isn’t just a document—it’s a safeguard against financial ruin.

Does the Ignis Include Free Insurance? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Certificate Holder: Name and address of the party requiring proof of insurance

A certificate of insurance is a critical document that verifies the existence of an insurance policy, and one of its most vital sections is the Certificate Holder. This field identifies the party requiring proof of insurance, ensuring clarity and compliance in contractual or regulatory relationships. Typically, the certificate holder is not the policyholder but an external entity—such as a landlord, lender, or client—that needs assurance of coverage. For instance, a construction company might list a property owner as the certificate holder to demonstrate liability insurance before starting a project. This section must include the holder’s full legal name and complete address, as inaccuracies can render the certificate invalid or delay approvals.

When completing this section, precision is paramount. Start by verifying the certificate holder’s legal name, avoiding nicknames or abbreviations. For businesses, use the registered corporate name, not a DBA (Doing Business As) title, unless explicitly requested. The address should include street, city, state, and ZIP code, with international addresses formatted according to local standards. For example, if the holder is a government agency, ensure the address matches official records, as discrepancies can lead to rejection. Always double-check details with the holder directly, as relying on outdated information from previous certificates can cause errors.

From a practical standpoint, the certificate holder section serves as a safeguard for both parties. For the insured, it ensures compliance with contractual obligations, reducing the risk of disputes or penalties. For the holder, it provides tangible proof of coverage, enabling informed decision-making. Consider a scenario where a small business owner leases commercial space. The landlord, listed as the certificate holder, requires general liability insurance to protect against potential claims. By clearly identifying the landlord in this section, the business owner fulfills a lease requirement while the landlord gains confidence in the tenant’s financial responsibility.

One common mistake to avoid is confusing the certificate holder with additional insured parties. While both may require proof of insurance, their roles differ. An additional insured is added to the policy for specific protections, whereas the certificate holder merely receives documentation. For example, a vendor might list a retailer as the certificate holder to prove product liability coverage, but the retailer may also request to be named as an additional insured for broader protection. Understanding this distinction ensures the correct information is included in each section of the certificate.

In conclusion, the Certificate Holder section is more than a formality—it’s a cornerstone of effective risk management. By accurately identifying the party requiring proof of insurance, all stakeholders benefit from transparency and accountability. Whether you’re issuing or receiving a certificate, treat this section with the attention it deserves. Verify details, understand its purpose, and avoid common pitfalls to ensure the document serves its intended function seamlessly.

How Does Cash Value Life Insurance Work?

You may want to see also

Explore related products

![]()

Additional Insured: Inclusion of other parties protected under the policy if applicable

A certificate of insurance often includes a section detailing additional insured parties, a critical component that extends the policy's protection beyond the primary policyholder. This provision is particularly vital in contractual relationships where multiple parties share risks, such as in construction, leasing, or vendor agreements. For instance, a general contractor might require subcontractors to name them as an additional insured on their liability policy to ensure coverage for claims arising from the subcontractor’s work. This inclusion is typically documented in the certificate under a designated field, often labeled "Additional Insured" or "Certificate Holder," with specific details about the scope and duration of the coverage.

Analyzing the practical implications, adding an additional insured is not merely a formality but a strategic risk management tool. It ensures that if a claim arises, the additional insured party can seek coverage under the policy, potentially avoiding costly litigation or out-of-pocket expenses. However, the language used in the endorsement is crucial. For example, a blanket additional insured endorsement provides broad coverage, while a more limited endorsement might restrict protection to specific activities or timeframes. Policyholders must carefully review these terms to ensure they align with contractual obligations and risk exposure.

From an instructive standpoint, requesting to be named as an additional insured involves clear communication and documentation. Parties should explicitly outline this requirement in contracts, specifying the exact name and address to be listed on the certificate. Additionally, they should request a copy of the endorsement itself, not just the certificate, to verify the terms of coverage. For instance, a landlord requiring a tenant to add them as an additional insured should confirm whether the endorsement includes completed operations coverage, which protects against claims arising after the tenant’s work is completed.

Comparatively, the inclusion of additional insured parties differs across industries and policy types. In the construction sector, it’s standard practice to extend coverage to project owners, managers, and other contractors. In contrast, in a retail leasing scenario, the landlord might require the tenant’s liability policy to include them as an additional insured for premises-related claims. Understanding these industry-specific norms is essential for both policyholders and those seeking additional insured status, as it ensures compliance and adequate protection.

Finally, a persuasive argument for prioritizing additional insured status lies in its role as a safeguard against unforeseen liabilities. Without this provision, parties exposed to risks through contractual relationships may find themselves financially vulnerable. For example, a business hiring a delivery vendor could face liability if the vendor causes an accident while performing services. By ensuring the vendor names them as an additional insured, the business protects itself from potential claims. This proactive approach not only mitigates risk but also fosters trust and stability in professional relationships.

Mastering Subrogation Requests: A Step-by-Step Guide for Insurance Claims

You may want to see also

Frequently asked questions

A Certificate of Insurance (COI) is a document issued by an insurance company or broker that provides proof of insurance coverage. It outlines key details such as the policyholder, coverage limits, policy period, and the type of insurance held.

A COI usually includes the insured’s name, policy number, coverage type (e.g., general liability, property), policy limits, effective and expiration dates, and the name of the insurance company or broker issuing the certificate.

A COI can be requested by third parties, such as clients, landlords, or contractors, who need proof of insurance coverage before entering into a business agreement or allowing work to begin.

While the core elements are consistent, the layout and design of a COI may vary depending on the insurance company or broker issuing it. However, all COIs must include the essential details to serve as valid proof of coverage.