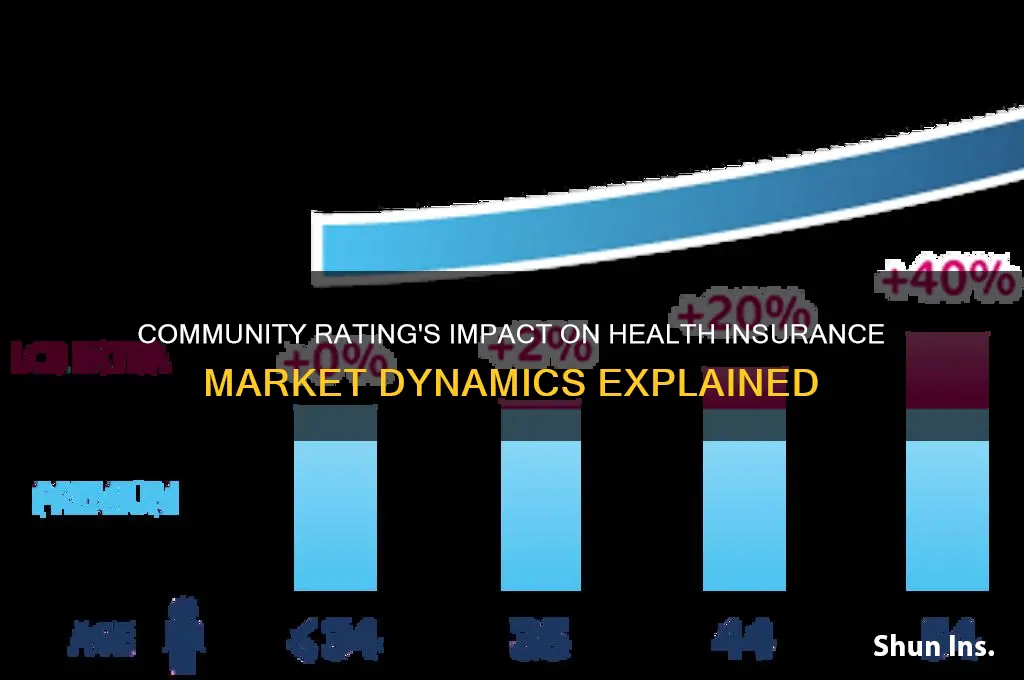

Community rating, a system where health insurance premiums are set based on the average cost of covering a group rather than individual health risks, significantly impacts the health insurance market by promoting fairness and accessibility. Under this model, insurers charge the same rates to all members of a geographic area or demographic group, regardless of age, health status, or medical history. This approach reduces barriers to coverage for individuals with pre-existing conditions, who might otherwise face prohibitively high premiums or be denied insurance altogether. However, community rating can also lead to adverse selection, where healthier individuals opt out of purchasing insurance, driving up costs for those who remain in the pool. To mitigate this, policymakers often pair community rating with mechanisms like guaranteed issue and individual mandates, ensuring a balanced risk pool and stabilizing premiums. While this system fosters inclusivity, it also raises debates about cost distribution and market efficiency, as it shifts financial burdens from high-risk individuals to the broader community. Ultimately, community rating shapes the health insurance market by prioritizing equity over individualized risk assessment, influencing both consumer behavior and insurer strategies.

| Characteristics | Values |

|---|---|

| Definition | Community rating requires insurers to charge the same premium to all individuals within a geographic area, regardless of age, health status, or other risk factors. |

| Impact on Premiums | Younger and healthier individuals often pay higher premiums than they would under an experience-rated system, while older and sicker individuals pay lower premiums. |

| Risk Pooling | Enhances risk pooling by spreading costs across a broader population, reducing financial burden on high-risk individuals. |

| Adverse Selection | Reduces adverse selection by preventing insurers from charging higher premiums to high-risk individuals, encouraging broader enrollment. |

| Market Stability | Promotes market stability by ensuring insurers cannot cherry-pick healthier individuals, leading to a more balanced risk pool. |

| Affordability for High-Risk Individuals | Makes health insurance more affordable for older and sicker individuals, increasing access to coverage. |

| Cost for Low-Risk Individuals | Increases costs for younger and healthier individuals, potentially discouraging them from purchasing insurance. |

| Mandates and Penalties | Often paired with individual mandates or penalties for not having insurance to ensure broad participation and prevent healthy individuals from opting out. |

| Impact on Insurer Behavior | Insurers focus on attracting a large, diverse customer base rather than targeting low-risk individuals, shifting strategies toward customer retention and service quality. |

| Regulatory Environment | Commonly implemented in regulated markets (e.g., ACA in the U.S.) to ensure fairness and accessibility, though it can limit insurer flexibility in pricing. |

| Effect on Competition | May reduce price competition among insurers since premiums are standardized, but competition shifts to areas like customer service, provider networks, and additional benefits. |

| Long-Term Market Effects | Can lead to higher overall premiums if healthy individuals opt out, but with mandates, it stabilizes the market and ensures sustainable funding for high-risk populations. |

| Consumer Perception | Mixed perceptions: high-risk individuals view it positively, while low-risk individuals may feel it is unfair due to higher costs. |

| International Examples | Implemented in countries like the Netherlands, Switzerland, and parts of the U.S. (ACA marketplaces), with varying degrees of success in achieving universal coverage and cost control. |

| Latest Trends (2023) | Continued debate in the U.S. about balancing community rating with risk-based pricing to address affordability concerns, with some states exploring reinsurance programs to offset costs for high-risk pools. |

Explore related products

What You'll Learn

- Impact on premium costs for individuals with pre-existing conditions

- Effect on risk pooling and insurer profitability in competitive markets

- Influence on consumer behavior and plan selection preferences

- Role in reducing adverse selection and market stability

- Comparison of community rating vs. experience rating systems

![]()

Impact on premium costs for individuals with pre-existing conditions

Community rating, a system where insurers charge the same premium to all applicants regardless of health status, fundamentally reshapes the financial landscape for individuals with pre-existing conditions. Under traditional underwriting, these individuals often faced exorbitant premiums or outright denials due to their higher expected medical costs. Community rating eliminates this disparity by pooling risk across the entire insured population, effectively subsidizing the care of those with chronic illnesses through contributions from healthier enrollees. For example, a 45-year-old with diabetes, who might have paid $1,200 monthly under medical underwriting, could see premiums drop to $600 under community rating, making coverage more accessible.

However, this leveling of costs is not without trade-offs. While individuals with pre-existing conditions benefit from lower premiums, healthier individuals may experience rate increases to offset the shared burden. This dynamic can create friction in the market, as younger, healthier consumers may perceive their premiums as unfairly inflated. For instance, a 25-year-old with no chronic conditions might see their monthly premium rise from $200 to $300, potentially discouraging enrollment. Such shifts underscore the delicate balance between equity and affordability in community-rated systems.

To mitigate adverse selection—where only high-risk individuals purchase insurance—community rating is often paired with mandates requiring everyone to enroll. This broadens the risk pool, ensuring that healthier individuals remain part of the system. For example, in states with robust individual mandates, premiums for a 50-year-old with hypertension might stabilize at $700 monthly, compared to $1,500 in markets without such mandates. Practical tips for individuals with pre-existing conditions include comparing plans during open enrollment periods and leveraging subsidies available under the Affordable Care Act, which can further reduce out-of-pocket costs.

Despite its benefits, community rating is not a panacea. Insurers may respond to the inability to price based on risk by narrowing provider networks or increasing cost-sharing, indirectly shifting costs to consumers. For instance, a plan covering a 60-year-old with heart disease might offer lower premiums but require higher copays for specialist visits. Individuals should carefully review plan details, focusing on out-of-pocket maximums and prescription drug coverage, to ensure comprehensive protection. Ultimately, while community rating improves premium affordability for those with pre-existing conditions, it requires complementary policies to sustain market stability and consumer satisfaction.

Applying for Medicare in New Jersey: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Effect on risk pooling and insurer profitability in competitive markets

Community rating, a pricing mechanism that prohibits insurers from varying premiums based on individual health risks, fundamentally reshapes risk pooling dynamics in competitive health insurance markets. By mandating uniform rates across all enrollees within a geographic area, this approach forces insurers to aggregate risks collectively rather than segmenting them. This collective risk pooling can stabilize premiums for high-risk individuals, as their costs are subsidized by healthier policyholders. However, it also creates a moral hazard: healthier individuals may opt out of coverage if they perceive premiums as disproportionately high relative to their expected medical expenses. This adverse selection weakens the risk pool, driving up costs for remaining enrollees and potentially triggering a death spiral of escalating premiums and declining enrollment.

To mitigate adverse selection, community rating is often paired with guaranteed issue and renewal policies, which require insurers to accept all applicants regardless of health status. While this ensures access for high-risk individuals, it intensifies the challenge of maintaining a balanced risk pool. Insurers must adapt by focusing on administrative efficiency, negotiating provider discounts, or investing in preventive care programs to manage costs. For instance, a study in the *New England Journal of Medicine* found that community-rated markets with robust preventive care initiatives reduced claims by 15% among high-risk populations aged 50–64. Such strategies can partially offset profitability pressures, but they require significant upfront investment and long-term commitment.

In competitive markets, the profitability of insurers under community rating hinges on their ability to attract and retain a diverse enrollee base. Insurers with strong brand recognition or superior customer service may fare better, as these factors can mitigate price sensitivity among healthier individuals. However, smaller insurers with limited resources may struggle to compete, potentially leading to market consolidation. For example, in states like New York and Massachusetts, where community rating has been in place for decades, the top three insurers control over 60% of the market share. This concentration raises concerns about reduced competition and higher premiums in the long run.

A critical takeaway for policymakers is the need to balance equity and sustainability in community-rated markets. Implementing individual mandates, as seen in the Affordable Care Act, can broaden the risk pool by requiring healthy individuals to participate. Alternatively, offering premium subsidies or reinsurance programs can alleviate financial strain on insurers while keeping premiums affordable. For instance, Switzerland’s health insurance system combines community rating with a robust subsidy framework, achieving near-universal coverage with stable premiums. Such models demonstrate that with careful design, community rating can enhance risk pooling without sacrificing insurer profitability.

Step-by-Step Guide to Applying for Government Health Insurance Coverage

You may want to see also

Explore related products

![]()

Influence on consumer behavior and plan selection preferences

Community rating, a system where insurers charge the same premium to all members of a geographic area regardless of health status, reshapes consumer behavior by altering the calculus of plan selection. Under this model, healthy individuals, who might otherwise opt for minimal coverage or none at all, face a stronger incentive to enroll in comprehensive plans. This is because the premium they pay no longer reflects their personal risk level but subsidizes the costs of sicker individuals in the same community. For instance, a 30-year-old with no chronic conditions might choose a gold-tier plan over a bronze-tier one, knowing their premium supports a shared risk pool rather than their individual health needs. This shift in behavior can lead to broader coverage but also raises questions about long-term sustainability as healthier individuals may still perceive the value proposition as misaligned with their personal risk.

Analyzing the impact on plan selection preferences reveals a paradox: while community rating promotes solidarity, it can also distort consumer choices. Risk-averse individuals, particularly those with higher incomes, may opt for more expensive plans with lower deductibles to maximize their perceived return on investment. Conversely, younger, healthier consumers might feel overinsured and seek ways to minimize costs, such as pairing high-deductible plans with health savings accounts (HSAs). For example, a 25-year-old freelancer might choose a bronze plan with a $6,000 deductible, contributing $3,000 annually to an HSA to offset out-of-pocket costs while maintaining affordability. Insurers must therefore design plans that balance actuarial soundness with consumer preferences, ensuring options cater to diverse risk tolerances and financial situations.

Persuasively, community rating can foster a sense of collective responsibility, influencing consumers to prioritize plans that offer robust preventive care and chronic disease management. This is particularly evident in communities with high rates of diabetes or hypertension, where consumers recognize the value of early intervention. For instance, a family with a history of heart disease might select a plan with comprehensive cardiac screenings and wellness programs, even if the premium is higher, to mitigate future healthcare costs. This behavior aligns with public health goals but requires insurers to communicate the long-term benefits of such plans effectively, using tools like personalized cost-benefit analyses or community health reports.

Comparatively, the influence of community rating on consumer behavior differs significantly across age groups. Older adults, who typically have higher healthcare utilization, benefit directly from the system and tend to favor plans with extensive coverage. In contrast, younger consumers, who often underestimate their health risks, may require nudges such as premium discounts for wellness activities or simplified plan comparisons to encourage enrollment. A practical tip for insurers is to segment marketing efforts by age, offering 20-somethings mobile app-based plan comparisons and 50-somethings detailed brochures on coverage for age-related conditions. Such tailored approaches can enhance consumer engagement and satisfaction while aligning plan selection with individual needs.

Descriptively, the interplay between community rating and consumer behavior highlights the importance of transparency in plan design. Consumers increasingly demand clarity on how their premiums contribute to the community pool and what services they receive in return. For example, a plan that explicitly allocates 20% of premiums to subsidizing high-risk members while offering free preventive care might appeal to socially conscious consumers. Insurers can leverage this by providing detailed breakdowns of premium usage and showcasing success stories of community-wide health improvements. This not only builds trust but also reinforces the value proposition of community rating, encouraging sustained enrollment and informed plan selection.

Get Medical Insurance via AMAC: What You Need to Know

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Role in reducing adverse selection and market stability

Community rating, a pricing strategy in health insurance where premiums are set uniformly regardless of individual health status, plays a pivotal role in mitigating adverse selection. Adverse selection occurs when high-risk individuals are more likely to purchase insurance, driving up costs for insurers and leading to higher premiums for all. By standardizing premiums, community rating reduces the incentive for healthier individuals to opt out of coverage, thereby maintaining a balanced risk pool. This mechanism ensures that the insurance market remains viable for both insurers and policyholders, fostering stability and accessibility.

Consider the practical implications of this approach. In markets without community rating, insurers often engage in medical underwriting, charging higher premiums to those with pre-existing conditions. This practice discourages healthier individuals from enrolling, as they perceive insurance as unnecessary or overpriced. Community rating flips this dynamic by spreading risk across a diverse population, making insurance more affordable for high-risk individuals while preventing low-risk individuals from exiting the market. For example, in states like New York and Massachusetts, community rating has been instrumental in achieving near-universal coverage, demonstrating its effectiveness in reducing adverse selection.

However, implementing community rating requires careful design to avoid unintended consequences. One critical step is pairing community rating with guaranteed issue—a policy mandating insurers to accept all applicants regardless of health status. Without guaranteed issue, high-risk individuals might delay purchasing insurance until they need it, undermining the risk pool. Additionally, policymakers must consider reinsurance programs or risk adjustment mechanisms to compensate insurers for covering high-cost enrollees. These safeguards ensure that community rating does not lead to financial strain for insurers, which could destabilize the market.

A comparative analysis highlights the contrast between markets with and without community rating. In the individual market prior to the Affordable Care Act (ACA), adverse selection was rampant, with premiums spiking for those with pre-existing conditions. The ACA’s introduction of community rating and guaranteed issue significantly reduced these disparities, though challenges remain in states with weaker enforcement. Conversely, countries like Switzerland and the Netherlands have successfully implemented community rating alongside robust regulatory frameworks, achieving high coverage rates and market stability. This comparison underscores the importance of complementary policies in maximizing the benefits of community rating.

In conclusion, community rating serves as a cornerstone for reducing adverse selection and enhancing market stability in health insurance. By standardizing premiums and spreading risk, it encourages broader participation and ensures affordability for high-risk individuals. However, its success hinges on thoughtful implementation, including guaranteed issue and risk-sharing mechanisms. Policymakers and insurers must collaborate to refine these strategies, leveraging lessons from successful models to create sustainable insurance markets. For consumers, understanding community rating’s role empowers them to make informed decisions, contributing to a healthier, more equitable system.

Medical Insurance: A Necessary Evil or a Welcome Safety Net?

You may want to see also

Explore related products

$92.95

![]()

Comparison of community rating vs. experience rating systems

Community rating and experience rating systems represent two fundamentally different approaches to pricing health insurance, each with distinct implications for market dynamics, consumer behavior, and equity. At their core, these systems determine how premiums are calculated: community rating sets uniform prices based on a broad population, while experience rating tailors costs to individual risk profiles. This comparison highlights their contrasting effects on accessibility, affordability, and market stability.

Consider a 45-year-old nonsmoker with no chronic conditions. Under an experience rating system, their premium might be $300/month, reflecting their low risk. However, under community rating, the same individual could pay $450/month, subsidizing higher-risk members in the pool. This example illustrates how community rating redistributes costs across the population, ensuring that those with pre-existing conditions or higher health risks aren’t priced out of the market. The trade-off? Healthier individuals may perceive their premiums as unfairly high, potentially leading to adverse selection if they opt out of coverage altogether.

From a market stability perspective, community rating fosters broader risk pooling, reducing volatility in premiums. For instance, in states like New York and Massachusetts, where community rating is mandated, insurers report more predictable claims costs compared to states with experience-based pricing. However, this stability comes at the expense of individualized fairness. Experience rating, by contrast, incentivizes healthy behaviors—a 30-year-old who quits smoking might see their premium drop by 15–20% within a year. Yet, this system can create affordability barriers for those with chronic conditions, who may face premiums exceeding $1,000/month, effectively locking them out of the market.

A critical takeaway is that the choice between these systems reflects societal values. Community rating prioritizes equity and accessibility, ensuring that health insurance serves as a social safety net. Experience rating, meanwhile, aligns costs with personal risk, rewarding low-risk behaviors but potentially exacerbating health disparities. Policymakers must weigh these trade-offs carefully, as the wrong balance can lead to market collapse—either through adverse selection in community-rated systems or through exclusion in experience-rated ones. Practical tips for consumers include understanding state regulations, leveraging subsidies where available, and considering health savings accounts to offset higher premiums in community-rated markets.

Filing Taxes While on Parents' Health Insurance: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Community rating is a system where insurers charge the same premium to all individuals in a geographic area, regardless of their age, health status, or medical history. This approach reduces disparities in premiums but can lead to higher costs for younger, healthier individuals, potentially causing them to opt out of coverage. This may shrink the risk pool, increasing premiums for those who remain insured.

Community rating makes health insurance more affordable for high-risk individuals by spreading their costs across the entire insured population. Without it, these individuals might face prohibitively expensive premiums or be denied coverage altogether. However, this can also lead to adverse selection if healthier individuals exit the market, destabilizing the insurance pool.

Community rating can reduce competition among insurers since they cannot differentiate premiums based on risk. This may limit innovation in plan design and customer service, as insurers focus less on attracting low-risk individuals. However, it also ensures that insurers compete on factors like provider networks and customer experience rather than risk selection.