Medicaid is a state-run program that provides low-cost or free custodial and medical services to those with low incomes who qualify. It is also intended to be a long-term care safety net, providing care to supplement or replace other long-term care financing when they are insufficient or unavailable. Long-term care insurance, on the other hand, is private insurance available to anyone who can afford it and offers more flexibility and options than Medicaid. This article will explore the interplay between having long-term health insurance and its effects on Medicaid eligibility.

| Characteristics | Values |

|---|---|

| Medicaid eligibility | Low-income families, qualified pregnant women and children, and individuals receiving Supplemental Security Income (SSI) |

| Medicaid coverage | Health coverage to over 77.9 million Americans, including children, pregnant women, parents, seniors, and individuals with disabilities |

| Long-term care insurance coverage | Cost of long-term care in nursing homes, in the beneficiary’s home or in other locations |

| Medicaid long-term care | Coverage of room and board, assistance with Activities of Daily Living (ADL), skilled nursing, and medication administration |

| Medicaid and long-term care insurance | Can be used together to cover long-term care costs |

| Medicaid Estate Recovery | State Medicaid programs must recover certain benefits paid on behalf of the enrollee, including nursing facility services, home and community-based services, and related hospital and prescription drug services |

| Medicaid LTSS | Recipients can retain income sufficient to pay for rent, food, and utilities, while those in nursing homes are allowed to retain a small monthly personal needs allowance |

| Medicaid and long-term care insurance eligibility | Eligibility rules differ in each state, but generally, finances from the last five years are assessed to determine eligibility |

Explore related products

What You'll Learn

- Medicaid is a federal and state program for individuals with limited means

- Long-term care insurance is private and available to anyone who can afford it

- Medicaid eligibility requires the exhaustion of most personal savings

- Long-term care insurance can be purchased while still healthy

- Medicaid eligibility rules vary by state

![]()

Medicaid is a federal and state program for individuals with limited means

Medicaid is a federal and state program that provides health coverage to Americans with limited means. It is the single largest source of health coverage in the United States, covering over 77.9 million people. The program offers low-cost or free custodial and medical services to those who qualify, and beneficiaries have better access to care than uninsured individuals.

Medicaid provides coverage for several special populations, including children with special healthcare needs, nursing home residents, non-elderly adults with mental illnesses, and individuals experiencing homelessness. It also covers services not usually covered by health insurance, such as non-emergency medical transportation and comprehensive benefits for children.

Eligibility for Medicaid is based on financial need, and individuals must meet certain income and asset requirements. Each state has its own rules, but in general, Medicaid considers an individual's finances over the five years preceding their application to determine eligibility for long-term care benefits. This is known as the "look-back rule." If any financial transactions during this period violate Medicaid rules, the individual may be penalized.

Long-term care insurance, on the other hand, is private insurance available to anyone who can afford it. It covers the cost of long-term care in nursing homes, in the beneficiary's home, or in other locations. While long-term care insurance offers more flexibility and options than Medicaid, it may not always be sufficient to cover all care costs. In such cases, Medicaid may step in to cover the deficit for qualified individuals.

Wyomingites' Healthcare: Affordable Insurance Strategies and Secrets

You may want to see also

Explore related products

![]()

Long-term care insurance is private and available to anyone who can afford it

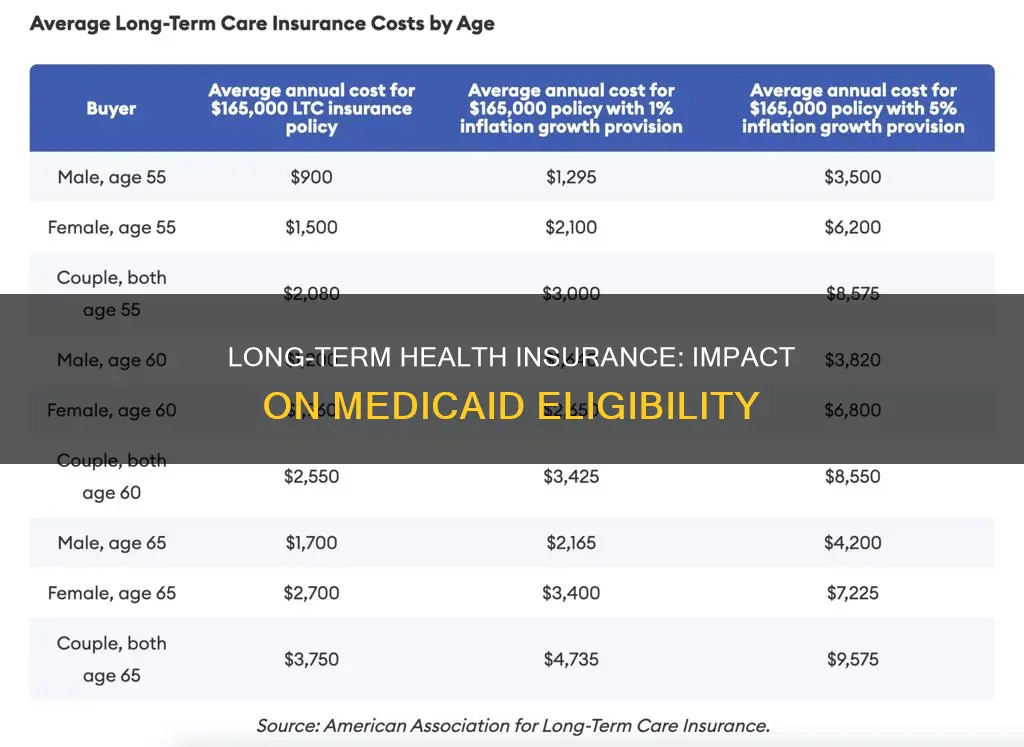

Long-term care insurance is private insurance available to anyone who can afford it. It offers more flexibility and options than Medicaid and covers all or part of nursing home care, home healthcare, and personal or adult day care for individuals aged 65 or older or those with a chronic condition requiring constant care. Individuals typically purchase long-term care insurance while they are still healthy, usually in their 50s or 60s, and make monthly or yearly premium payments. When the policy owner needs long-term care, the insurance covers the associated costs as specified in the policy.

Medicaid, on the other hand, is a federal and state program that provides low-cost or free medical and custodial services to those with low incomes who qualify. It is not the same as long-term care insurance, and individuals should not solely rely on Medicaid for long-term care needs without first understanding its coverage and differences from long-term care insurance. While Medicaid does cover long-term care, it often only includes nursing home stays for non-skilled custodial care in many states. Additionally, Medicaid eligibility has stringent requirements, including income and asset limits, and most personal savings must be exhausted before an individual becomes eligible for long-term care services.

The eligibility rules for Medicaid vary across states, and each state has its own set of benefits and provider payment rates. Some states have adopted the Medicaid expansion, providing coverage for individuals experiencing homelessness or transitioning out of carceral settings. Medicaid also offers benefits beyond long-term care, such as non-emergency medical transportation and comprehensive services for children.

Long-term care insurance and Medicaid can work together to cover an individual's care costs. For example, if an individual's long-term care insurance policy does not fully cover their nursing home expenses, Medicaid can step in to cover the deficit through programs like Nursing Home Medicaid. Similarly, for individuals receiving care at home, long-term care insurance and Medicaid can both contribute to covering the costs of in-home services and supports.

It is important to note that long-term care insurance policyholders may still struggle to afford their care costs, and in such cases, Medicaid can provide additional financial support. However, individuals should carefully consider their options and consult with a Medicaid Planning professional due to the complex nature of Medicaid eligibility and the potential pitfalls in the application process.

Medical Practitioners' Insurance: Who Files Claims and Benefits?

You may want to see also

Explore related products

![]()

Medicaid eligibility requires the exhaustion of most personal savings

Medicaid is a federal and state program that provides low-cost or free custodial and medical services to those with low incomes who qualify. It is intended to be a safety net for long-term care, supplementing or replacing other sources of funding when they are insufficient or unavailable.

Medicaid eligibility is complex and determined at multiple levels, with each state having its own requirements. These requirements include financial eligibility, which changes annually, and non-financial eligibility criteria. For example, individuals must meet residency requirements and may be required to be either citizens of the United States or certain qualified non-citizens.

Financial eligibility for Medicaid often requires the exhaustion of most personal savings. This is because Medicaid has strict asset limits, which vary depending on the state and eligibility group. For example, in most states, an individual can have up to $2,000 in countable assets, while couples can have up to $3,000. These limits are quite low and do not allow for much flexibility in savings and emergencies.

If an individual has too many countable assets to qualify for Medicaid, they can consider options to spend down their liquid wealth and meet eligibility requirements. This involves using or reallocating liquid assets to reduce countable resources. For example, individuals can spend money on debt repayment or purchase exempt services like final expense insurance, which covers end-of-life care while reducing current liquid assets. It is important to note that Medicaid has a look-back period, typically five years, during which it evaluates all asset transfers made by the applicant.

In conclusion, while Medicaid provides valuable support for long-term care, eligibility requirements can be stringent, and individuals may need to exhaust most of their personal savings to qualify. It is essential to carefully consider one's options and consult a qualified financial advisor to navigate the complexities of Medicaid eligibility and make informed decisions.

Breast Implants: Are They Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

Long-term care insurance can be purchased while still healthy

Long-term care insurance is a policy that you buy to cover the costs of long-term care services, which aren't covered by regular health insurance. These services include assistance with routine daily activities like bathing, dressing, or getting in and out of bed, and are often required by individuals with chronic medical conditions, disabilities, or disorders like Alzheimer's disease. Long-term care insurance is available to anyone who can afford it, and it offers more flexibility and options than Medicaid.

When considering long-term care insurance, it's important to note that it is typically purchased while the individual is still healthy. This is because long-term care insurance carriers will not approve applicants with debilitating or pre-existing conditions, and approval rates drop significantly for applicants over 75. Additionally, the cost of long-term care insurance increases with age and health deterioration, so purchasing it while young and healthy can result in significant savings over time.

The decision to purchase long-term care insurance should be made based on an individual's situation and preferences. It is important to consider factors such as budget, assets, and overall financial condition before committing to a policy. For those with substantial assets, long-term care insurance can be a way to protect their wealth and ensure they have access to necessary care services in the future. However, for those with limited budgets, adding an LTC insurance premium may not be a feasible option.

While long-term care insurance can provide peace of mind and financial protection, it is not the only option for funding long-term care. Medicaid, a federal and state program, offers long-term care benefits to individuals with low incomes who have exhausted most of their savings and assets. In some states, individuals may qualify for Medicaid even if they have not depleted all their resources, but this varies depending on income limits and eligibility requirements specific to each state. Therefore, it is crucial to understand the eligibility criteria and benefits offered by both long-term care insurance and Medicaid before making a decision.

Prescription Refills: Understanding Insurance Coverage for Controlled Medications

You may want to see also

Explore related products

![]()

Medicaid eligibility rules vary by state

Medicaid is a federal and state program that provides health coverage to low-income families and individuals. It is the single largest source of health coverage in the United States, serving over 77.9 million Americans. While it is a federal program, each state operates its own Medicaid program within federal guidelines, and eligibility rules vary among states.

In all states, Medicaid gives health coverage to some individuals and families, including children, parents, people who are pregnant, elderly people with certain incomes, and people with disabilities. However, the specific eligibility criteria and benefits offered can vary widely from state to state. For example, some states have expanded their Medicaid programs to cover other adults below a certain income level, while others have not. Additionally, some states have more restrictive eligibility criteria than others, and certain states are known as 209(b) states, which use more restrictive eligibility criteria than the SSI program administered by the Social Security Administration.

The federal government provides financial support for part of the cost of state Medicaid programs, but states have broad discretion in determining who is eligible, what services they will cover, and how much they will pay for covered services. This flexibility allows states to design and administer their own programs to meet the unique needs and characteristics of their residents. As a result, there can be significant variation in the percentage of Medicaid spending across states, with some states spending more on certain populations or services than others.

It's important to note that Medicaid is not synonymous with long-term care insurance. While it does provide some long-term care benefits, these benefits may be limited, and the availability of coverage for long-term care can vary depending on the state. Before an individual is eligible for long-term services and supports (LTSS) from Medicaid, most personal savings must be exhausted. Additionally, there is a five-year look-back rule that allows Medicaid to review and recoup asset transfers that occurred in the five years prior to Medicaid LTSS eligibility. This rule helps ensure that individuals do not transfer assets for less than fair market value to qualify for Medicaid coverage.

Medical Associations: Lobbying Insurers for Money?

You may want to see also

Frequently asked questions

Medicaid is a federal and state program that provides health coverage to over 77.9 million Americans, including children, pregnant women, parents, seniors, and individuals with disabilities.

Long-term care insurance is private insurance that covers the cost of long-term care in nursing homes, in the beneficiary’s home, or in other locations. It is available to anyone who can afford to pay for it and offers more flexibility and options than Medicaid.

Long-term care insurance can help protect assets from Medicaid Estate Recovery. However, individuals with long-term care insurance may still be unable to afford their care costs, and in these cases, Medicaid can cover the deficit.

Medicaid long-term care can be provided in a number of settings, including nursing homes, the beneficiary's home, and assisted living residences. It can also provide benefits such as case management, assistance with activities of daily living, and respite care.

To be eligible for Medicaid long-term care, individuals must meet their state's specific income and asset requirements. In general, applicants' finances going back five years from the date of their application are assessed to determine eligibility.