Health insurance rates are determined through a complex interplay of factors, including individual demographics, lifestyle choices, geographic location, and broader market trends. Insurers assess risk by evaluating age, medical history, occupation, and habits like smoking, then adjust premiums accordingly. Additionally, regional healthcare costs, state regulations, and the overall economic climate significantly influence pricing. Policy type, coverage level, and deductible choices also play a role, with comprehensive plans typically costing more. Understanding these dynamics is crucial for consumers to navigate the market effectively and secure affordable, adequate coverage.

Explore related products

What You'll Learn

- Factors influencing premium costs: age, location, lifestyle, and medical history impact health insurance rates significantly

- Types of plans: HMOs, PPOs, and EPOs differ in costs and coverage flexibility

- Deductibles and copays: higher deductibles often lower premiums but increase out-of-pocket expenses

- Network restrictions: in-network providers usually cost less than out-of-network services

- Government subsidies: ACA marketplace subsidies reduce premiums for eligible low-income individuals

![]()

Factors influencing premium costs: age, location, lifestyle, and medical history impact health insurance rates significantly

Health insurance premiums are not arbitrary; they are meticulously calculated based on a variety of personal and environmental factors. Among these, age, location, lifestyle, and medical history stand out as the most influential determinants. Understanding how these elements interplay can help individuals anticipate and potentially mitigate their insurance costs.

Age: The Inevitable Escalator

As individuals age, their health insurance premiums tend to rise steadily. Insurers categorize policyholders into age brackets, with rates increasing incrementally after age 30 and more sharply after 50. For example, a 25-year-old might pay $200 monthly, while a 60-year-old could face premiums exceeding $800. This is because older adults statistically require more medical care, from routine screenings to chronic disease management. To offset this, younger individuals should consider locking in lower rates early and exploring health savings accounts (HSAs) to build a financial cushion for future expenses.

Location: Geography Matters More Than You Think

Where you live plays a surprising role in premium costs. Urban areas with higher costs of living and greater access to specialized care often see steeper insurance rates. For instance, a resident of New York City might pay 30% more than someone in a rural Midwest town. State regulations also vary; some mandate coverage for specific services, driving up costs. To navigate this, research state-specific insurance trends and consider relocating to areas with lower healthcare costs if feasible. Alternatively, explore telemedicine options to reduce reliance on local providers.

Lifestyle: Choices That Count

Insurers scrutinize lifestyle habits, such as smoking, alcohol consumption, diet, and exercise, to assess risk. Smokers, for instance, can expect premiums up to 50% higher than non-smokers due to increased risks of cancer, heart disease, and respiratory issues. Similarly, a sedentary lifestyle or obesity can lead to higher rates. To lower costs, adopt healthier habits: quitting smoking, maintaining a BMI under 30, and exercising regularly can reduce premiums by 10-20%. Some insurers even offer discounts for policyholders who participate in wellness programs or achieve fitness milestones.

Medical History: The Long Shadow of Past Health

Pre-existing conditions, such as diabetes, hypertension, or cancer, significantly impact premiums. Insurers review medical records to gauge future healthcare needs, often charging higher rates for individuals with chronic illnesses. For example, a person with managed diabetes might pay $400 more annually than someone without. To manage this, ensure consistent treatment adherence and document health improvements, as some insurers may adjust rates over time. Additionally, explore government subsidies or state-specific programs designed to cap premiums for those with pre-existing conditions.

By dissecting these factors, individuals can take proactive steps to manage their health insurance costs. While some variables, like age, are uncontrollable, others, such as lifestyle and location, offer opportunities for intervention. Armed with this knowledge, policyholders can make informed decisions to optimize their coverage and financial well-being.

Contacting Medicare Health Insurance in Pennsylvania: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Types of plans: HMOs, PPOs, and EPOs differ in costs and coverage flexibility

Health insurance plans are not one-size-fits-all, and understanding the differences between HMOs, PPOs, and EPOs is crucial for managing costs and coverage flexibility. Each plan type has distinct features that cater to different healthcare needs and financial situations. Let’s break down these options to help you make an informed decision.

Analytical Perspective:

HMOs (Health Maintenance Organizations) typically offer the lowest premiums but require you to choose a primary care physician (PCP) who acts as a gatekeeper for specialist referrals. This structured approach reduces administrative costs, making HMOs cost-effective for those who prioritize affordability over flexibility. However, out-of-network care is rarely covered, except in emergencies. PPOs (Preferred Provider Organizations), on the other hand, provide greater flexibility by allowing you to see any in-network provider without a referral. While premiums are higher than HMOs, PPOs cover a portion of out-of-network costs, appealing to those who value choice and access. EPOs (Exclusive Provider Organizations) combine elements of both, offering lower premiums than PPOs but no out-of-network coverage, except in emergencies. This makes EPOs a middle-ground option for those who want lower costs without the HMO’s referral requirement.

Instructive Approach:

To choose the right plan, assess your healthcare needs and budget. If you’re healthy, rarely visit specialists, and want to minimize monthly costs, an HMO might be ideal. For example, a 30-year-old with no chronic conditions could save hundreds annually by opting for an HMO. If you prefer the freedom to see specialists directly or have a preferred out-of-network provider, a PPO is worth the higher premium. Families with children or individuals managing chronic conditions often benefit from PPOs due to their flexibility. EPOs are best for those who want lower costs than PPOs but don’t need out-of-network coverage. For instance, a 45-year-old with stable health and a trusted in-network doctor could save 20-30% on premiums with an EPO compared to a PPO.

Comparative Analysis:

Consider a scenario where a 50-year-old with diabetes needs frequent specialist visits. An HMO would require a referral for each visit, potentially delaying care. A PPO allows direct access to specialists, though at a higher cost. An EPO, while cheaper than a PPO, might not cover the preferred specialist if they’re out-of-network. Here, the PPO’s flexibility outweighs its higher premium. Conversely, a 25-year-old with no health issues might find an HMO’s low premiums more appealing, as they’re unlikely to need extensive care. The key is aligning the plan’s structure with your specific needs.

Persuasive Argument:

Don’t let the complexity of HMOs, PPOs, and EPOs deter you from choosing the right plan. Start by listing your healthcare priorities: cost, flexibility, or a balance of both. If affordability is paramount, an HMO or EPO could save you money without sacrificing essential coverage. If flexibility is non-negotiable, a PPO’s higher premium is a worthwhile investment. Remember, the goal is to avoid overpaying for unused benefits or being underinsured when you need care. Take the time to compare plans during open enrollment, and don’t hesitate to consult a broker or use online tools to simplify the process.

Practical Tips:

When evaluating plans, check the provider network to ensure your preferred doctors are included. Review the prescription drug coverage, as formularies vary widely. For example, an HMO might cover generic medications at a lower cost, while a PPO may offer better coverage for brand-name drugs. Finally, consider the out-of-pocket maximum—the most you’ll pay annually for covered services. A plan with a lower premium but higher out-of-pocket maximum might not be the best value if you anticipate significant medical expenses. By focusing on these details, you can select a plan that aligns with your health and financial goals.

Top Homeowner Insurance Companies for Efficient and Fair Claims Handling

You may want to see also

Explore related products

![]()

Deductibles and copays: higher deductibles often lower premiums but increase out-of-pocket expenses

Health insurance plans often present a trade-off between upfront costs and potential out-of-pocket expenses. One key mechanism driving this balance is the relationship between deductibles and premiums. Higher deductibles—the amount you pay before insurance coverage kicks in—typically result in lower monthly premiums. For instance, a plan with a $6,000 deductible might have a premium of $200 per month, while a plan with a $1,000 deductible could cost $400 monthly. This structure appeals to individuals who prioritize lower recurring costs and are willing to assume more financial risk if they require significant medical care.

However, the allure of reduced premiums comes with a caveat: higher deductibles shift more financial responsibility to the policyholder. Consider a scenario where a 35-year-old individual with a high-deductible plan ($5,000) visits the emergency room for a minor injury, incurring a $2,500 bill. Without meeting the deductible, they must pay the full amount out-of-pocket. In contrast, someone with a lower deductible ($1,000) would only pay $1,000, with insurance covering the remainder. This example underscores how higher deductibles can lead to unexpected financial strain, particularly for those with frequent or unforeseen medical needs.

Copays further complicate this dynamic, as they represent fixed amounts paid for specific services, regardless of the deductible. For example, a $30 copay for a doctor’s visit remains consistent across plans. However, in high-deductible plans, copays often apply only after the deductible is met, meaning policyholders may pay full price for services until they reach their deductible threshold. This can create confusion and frustration, especially for individuals who require regular medical attention, such as those managing chronic conditions like diabetes or hypertension.

To navigate this trade-off effectively, assess your healthcare usage patterns and financial resilience. If you’re generally healthy and rarely visit the doctor, a high-deductible plan paired with a health savings account (HSA) could save you money in the long run. Conversely, if you anticipate frequent medical visits or have a history of high healthcare costs, a lower-deductible plan may provide better value despite higher premiums. Practical tips include reviewing your previous year’s medical expenses, considering potential future needs (e.g., planned surgeries or family expansions), and comparing out-of-pocket maximums across plans to cap your financial exposure.

Ultimately, the decision hinges on balancing affordability and risk. While lower premiums may ease monthly budgets, they require careful consideration of how much you can afford to pay out-of-pocket in a worst-case scenario. By understanding the interplay between deductibles, copays, and premiums, you can select a plan that aligns with your health needs and financial priorities, ensuring you’re neither overpaying nor underinsured.

Switching Insurance: Do Medical Records Transfer?

You may want to see also

Explore related products

$27 $45

$19.95

![]()

Network restrictions: in-network providers usually cost less than out-of-network services

Health insurance plans often create networks of healthcare providers to control costs and ensure quality care. These networks are essentially groups of doctors, hospitals, and specialists who have agreed to provide services at pre-negotiated rates. When you choose an in-network provider, your insurance company has already established a contract with them, typically resulting in lower out-of-pocket costs for you. This is a fundamental aspect of how health insurance rates are structured and can significantly impact your healthcare expenses.

The Cost Disparity: In-Network vs. Out-of-Network

Imagine you need a routine check-up. Visiting an in-network primary care physician might cost you a $20 copay, a fixed amount you pay at the time of service. However, if you decide to see a doctor outside your insurance network, the scenario changes drastically. Out-of-network providers often charge higher fees, and your insurance may only cover a portion of the cost, leaving you with a substantial balance to pay. For instance, that same check-up could result in a $150 bill, with your insurance covering 70%, and you being responsible for the remaining $45, plus any deductible or coinsurance amounts. This example illustrates how network restrictions can directly affect your wallet.

Insurance companies negotiate discounted rates with in-network providers, ensuring that services are more affordable for their members. These providers agree to accept the insurance company's allowed amount as full payment, reducing the overall cost of care. In contrast, out-of-network providers have no such agreement, allowing them to charge their usual fees, which are often higher. This disparity is a strategic move by insurance companies to encourage members to utilize in-network services, thereby managing overall healthcare costs.

Navigating Network Restrictions: A Practical Approach

To make the most of your health insurance, it's crucial to understand your plan's network. Here's a step-by-step guide:

- Review Your Network Directory: Familiarize yourself with the list of in-network providers. Most insurance companies provide an online directory, making it easy to search for doctors, hospitals, and specialists within your network.

- Plan Ahead for Specialist Visits: If you require specialized care, ensure you obtain referrals or pre-authorizations from your primary care physician to stay within the network. This step is essential to avoid unexpected out-of-network charges.

- Understand Emergency Exceptions: In emergency situations, you may not have the luxury of choosing an in-network provider. Fortunately, most insurance plans cover emergency services at an in-network cost-sharing level, regardless of the provider's network status.

- Consider Network Size: When selecting a health insurance plan, compare the size and accessibility of their provider networks. Larger networks offer more choices, reducing the chances of accidentally incurring out-of-network costs.

By understanding and utilizing in-network providers, you can effectively manage your healthcare expenses. This strategy is a powerful tool in navigating the complex world of health insurance rates, ensuring you receive quality care without breaking the bank. Remember, being informed about your insurance network is a proactive step towards financial well-being in healthcare.

Does the VA Offer Health Insurance? Understanding Veterans' Benefits

You may want to see also

Explore related products

![]()

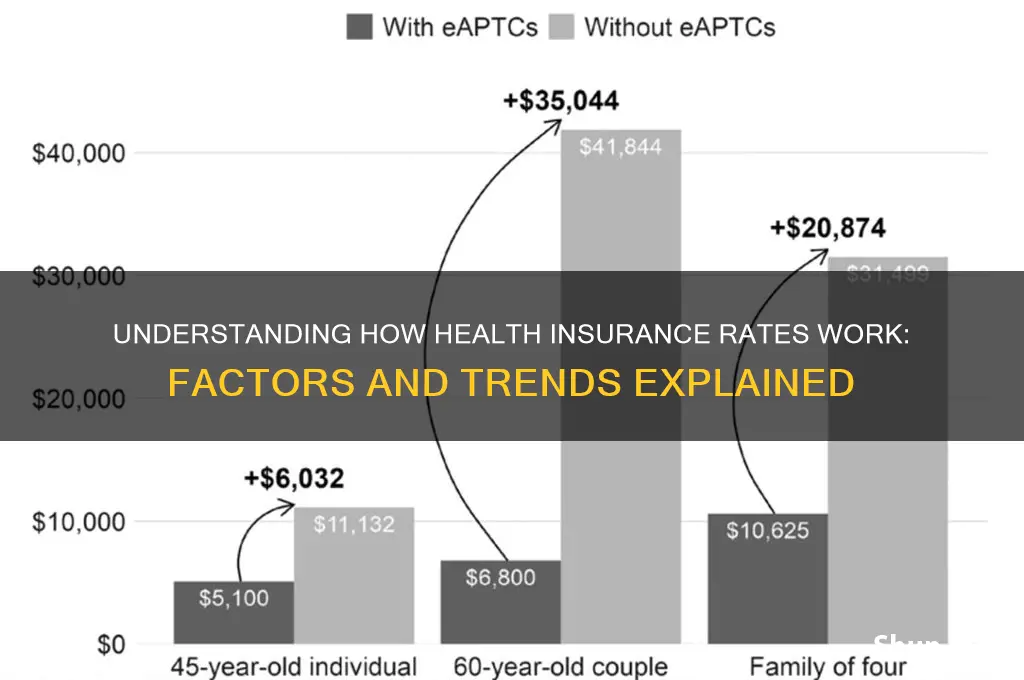

Government subsidies: ACA marketplace subsidies reduce premiums for eligible low-income individuals

Health insurance premiums can feel like a moving target, fluctuating based on factors like age, location, and health status. But for millions of Americans, the Affordable Care Act (ACA) marketplace subsidies act as a stabilizing force, significantly reducing the cost of coverage. These subsidies, designed to assist low-income individuals and families, operate on a sliding scale, meaning the lower your income, the larger the subsidy you receive.

Imagine earning $30,000 annually. Without subsidies, a benchmark silver plan might cost you $400 per month. However, with ACA subsidies, your monthly premium could shrink to $150 or even less, making comprehensive health insurance accessible.

The subsidy calculation isn't a simple percentage discount. It's a nuanced process that considers your Modified Adjusted Gross Income (MAGI) relative to the federal poverty level (FPL). For 2023, individuals earning up to 400% of the FPL qualify for subsidies. This translates to roughly $54,360 for an individual and $111,000 for a family of four. The subsidy amount is determined by the difference between your expected contribution towards premiums (capped at a percentage of your income) and the actual cost of the benchmark plan in your area.

The ACA marketplace website (Healthcare.gov) provides a user-friendly subsidy calculator to estimate your potential savings. Simply input your income, household size, and location to get a personalized estimate.

While subsidies primarily target premiums, they also indirectly impact out-of-pocket costs. By making lower-cost plans more affordable, individuals can choose plans with lower deductibles and copays, reducing their overall healthcare expenses. This is particularly beneficial for those with chronic conditions or anticipating frequent medical needs.

It's crucial to remember that subsidy eligibility is determined annually during open enrollment. Life changes like income fluctuations or additions to your household can impact your subsidy amount. Regularly updating your information on Healthcare.gov ensures you receive the maximum subsidy you're entitled to. By leveraging ACA marketplace subsidies, eligible individuals can navigate the often-complex world of health insurance with greater financial security and peace of mind.

Extending Veterans Health Insurance: A Step-by-Step Guide to Submitting Forms

You may want to see also

Frequently asked questions

Health insurance rates are determined by factors such as age, location, health status, lifestyle, coverage level, and the insurer’s assessment of risk. Insurers calculate premiums based on the likelihood of claims and the cost of providing care, often using actuarial data and historical trends.

Health insurance rates often increase annually due to rising healthcare costs, inflation, advancements in medical technology, increased utilization of services, and changes in regulations. Insurers adjust premiums to cover these expenses and maintain profitability.

Yes, your personal health can impact your rates. Factors like pre-existing conditions, smoking status, weight, and medical history may lead to higher premiums, as insurers consider these indicators of potential healthcare costs. However, in some regions, laws like the Affordable Care Act (ACA) limit how much health status can affect rates.