The relationship between income increases and health insurance subsidies is a critical aspect of healthcare policy, particularly in systems where government assistance is tied to financial need. As individuals experience a rise in income, their eligibility for health insurance subsidies often undergoes significant changes. Typically, subsidies are designed to taper off as earnings grow, ensuring that support is directed towards those with the greatest financial need. However, this dynamic can create a complex interplay between economic advancement and healthcare affordability. While higher income may reduce subsidy amounts, it also potentially exposes individuals to higher insurance premiums or out-of-pocket costs, raising questions about the sustainability of healthcare access for those transitioning out of lower-income brackets. Understanding this mechanism is essential for policymakers and individuals alike, as it directly impacts financial planning and the overall accessibility of healthcare services.

| Characteristics | Values |

|---|---|

| Subsidy Eligibility | Higher income may reduce or eliminate eligibility for subsidies. |

| Subsidy Calculation | Subsidies are based on a percentage of the federal poverty level (FPL). |

| Income Thresholds | For 2023, subsidies are available for incomes up to 400% of FPL. |

| Subsidy Reduction | As income increases, the subsidy amount decreases proportionally. |

| Cliff Effect | Small income increases can lead to significant subsidy reductions. |

| ACA Marketplace | Applies to plans purchased through the Affordable Care Act (ACA) marketplace. |

| Medicaid Impact | Higher income may disqualify individuals from Medicaid in some states. |

| Tax Credits | Premium tax credits decrease as income rises above subsidy thresholds. |

| Cost-Sharing Reductions | Eligibility for cost-sharing reductions may also decrease with higher income. |

| Annual Reconciliation | Subsidies are reconciled during tax filing based on actual income. |

| Income Verification | Income changes must be reported to the marketplace to adjust subsidies. |

| State Variations | Some states have expanded Medicaid, affecting subsidy eligibility rules. |

| 2023 FPL Example | For a family of 4, 400% of FPL is $111,000 (subsidy cutoff). |

| Subsidy Phase-Out | Subsidies phase out gradually as income approaches the threshold. |

| Impact on Premiums | Higher income means paying a larger share of the premium. |

| Special Enrollment | Income changes may qualify individuals for a special enrollment period. |

Explore related products

![The Economics of Inequality, Poverty, and Discrimination in the 21st Century: [2 volumes]](https://m.media-amazon.com/images/I/81lTzmz+N4L._AC_UY218_.jpg)

What You'll Learn

- Eligibility Changes: Higher income may reduce subsidy eligibility under ACA income limits

- Subsidy Calculation: Decreased subsidies as income rises, based on MAGI thresholds

- Premium Impact: Higher premiums with reduced subsidies, increasing out-of-pocket costs

- Coverage Options: Shift to non-subsidized plans or employer-based insurance alternatives

- Policy Adjustments: Annual subsidy recalculations to reflect updated income levels

![]()

Eligibility Changes: Higher income may reduce subsidy eligibility under ACA income limits

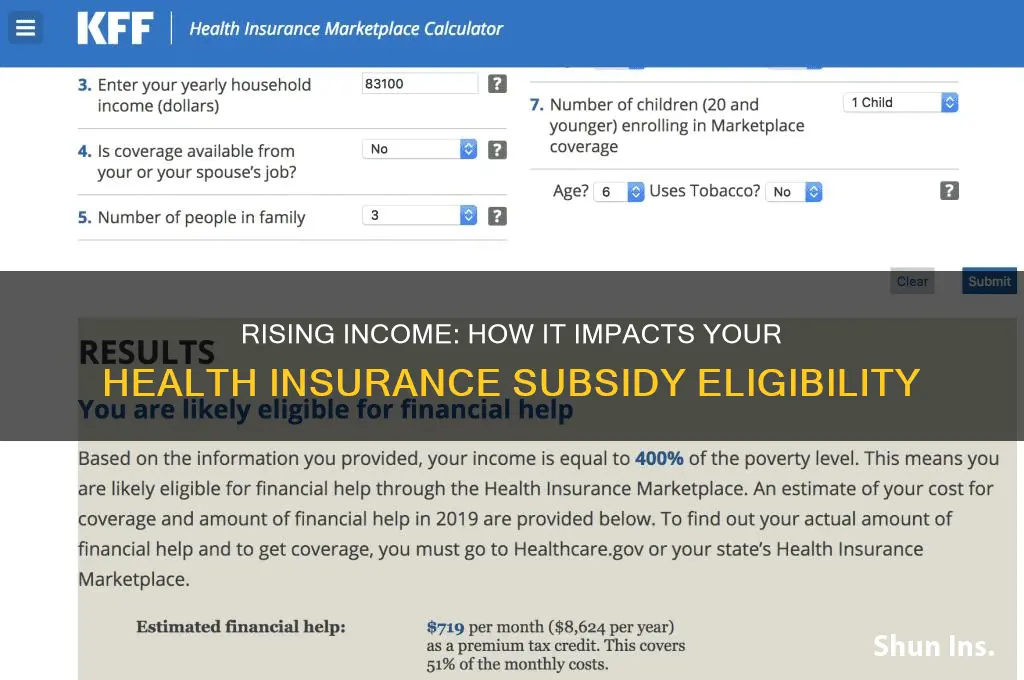

Under the Affordable Care Act (ACA), health insurance subsidies are designed to make coverage more affordable for individuals and families with moderate incomes. However, these subsidies are not static; they are directly tied to your income level. As your income rises, it can trigger a reduction in subsidy eligibility, potentially leading to higher out-of-pocket costs for your health insurance. This dynamic relationship between income and subsidies is a critical aspect of the ACA's financial assistance framework.

Understanding the ACA Income Limits

The ACA sets income limits for subsidy eligibility based on the Federal Poverty Level (FPL). For 2023, individuals with incomes between 100% and 400% of the FPL may qualify for premium tax credits, which reduce the cost of monthly premiums. For a single individual, 400% of the FPL translates to an annual income of approximately $54,360. As your income approaches or exceeds this threshold, your subsidy amount decreases, and you may eventually become ineligible for assistance altogether.

Scenario Analysis: Income Increase and Subsidy Reduction

Consider a 35-year-old individual earning $40,000 annually, which falls within the 300% FPL range. They currently receive a premium tax credit of $200 per month, reducing their monthly premium from $450 to $250. If their income increases to $55,000, surpassing the 400% FPL threshold, their subsidy eligibility is reduced or eliminated. As a result, they may face a significant premium increase, potentially rising to $450 or more per month, depending on their plan and location.

Practical Tips for Managing Income Changes

- Monitor Your Income: Regularly review your income to anticipate potential changes in subsidy eligibility. Use online calculators or consult with a tax professional to estimate your modified adjusted gross income (MAGI) for the year.

- Adjust Withholding: If possible, adjust your tax withholding to account for income increases, minimizing the risk of a large tax bill or reduced subsidy eligibility.

- Explore Alternative Coverage Options: If your income exceeds the ACA subsidy limits, consider alternative coverage options, such as employer-sponsored insurance or short-term health plans, to maintain affordable coverage.

- Plan for Tax Implications: Be aware that subsidy reductions may result in higher tax liabilities, as you may need to repay a portion of the advanced premium tax credit if your income exceeds the eligibility threshold.

Long-Term Strategies for Income and Subsidy Management

To mitigate the impact of income increases on subsidy eligibility, consider long-term strategies such as:

- Income Smoothing: Distribute income more evenly across tax years to avoid sudden jumps that may affect subsidy eligibility.

- Tax-Advantaged Savings: Contribute to tax-advantaged accounts, such as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs), to reduce taxable income and potentially maintain subsidy eligibility.

- Consultation with Professionals: Work with financial advisors, tax professionals, or ACA navigators to develop a comprehensive plan for managing income changes and subsidy eligibility.

By understanding the relationship between income and subsidy eligibility, and implementing practical strategies to manage income changes, individuals can navigate the complexities of ACA subsidies and maintain affordable health insurance coverage.

Understanding Medicare and Regular Medical Insurance Compatibility

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UL320_.jpg)

![]()

Subsidy Calculation: Decreased subsidies as income rises, based on MAGI thresholds

As income rises, health insurance subsidies decrease, a mechanism designed to ensure that financial assistance is targeted toward those who need it most. This inverse relationship is rooted in the calculation of Modified Adjusted Gross Income (MAGI), which serves as the primary determinant for subsidy eligibility under the Affordable Care Act (ACA). Understanding how MAGI thresholds influence subsidy amounts is crucial for individuals and families navigating the health insurance marketplace.

The subsidy calculation begins with the federal poverty level (FPL), which varies annually and by household size. Subsidies are available to those earning between 100% and 400% of the FPL, with the amount tapering off as income approaches the upper threshold. For example, a family of four earning $28,000 (100% of the 2023 FPL) would qualify for a higher subsidy than one earning $112,000 (400% of the FPL). The formula ensures that those closer to the poverty line receive more substantial assistance, while those with higher incomes contribute a larger share of their premiums.

To illustrate, consider a single individual earning $30,000 annually. If the FPL for a single person is $14,580, this individual’s income is approximately 206% of the FPL. Using the ACA’s subsidy formula, their benchmark plan (the second-lowest-cost silver plan) might cost $400 per month, but their subsidy could reduce their premium to $200 or less. However, if their income increases to $50,000 (343% of the FPL), their subsidy would decrease significantly, leaving them responsible for a larger portion of the premium.

Practical tips for managing this dynamic include monitoring income changes throughout the year, as subsidies are based on projected annual earnings. If income rises mid-year, individuals should update their marketplace application to avoid repaying excess subsidies at tax time. Conversely, if income drops, they may qualify for additional assistance. Tools like the healthcare.gov subsidy calculator can help estimate changes in real time.

In conclusion, the subsidy calculation is a precise, income-driven process that balances affordability with fiscal responsibility. By understanding MAGI thresholds and their impact on subsidies, individuals can make informed decisions to optimize their health insurance coverage as their financial circumstances evolve.

Suing Insurance Companies: Denial of Medication and Your Rights

You may want to see also

Explore related products

![]()

Premium Impact: Higher premiums with reduced subsidies, increasing out-of-pocket costs

As income rises, individuals often face a paradoxical challenge in the realm of health insurance: higher premiums coupled with reduced subsidies, leading to increased out-of-pocket costs. This phenomenon is particularly pronounced in systems like the Affordable Care Act (ACA) marketplace, where subsidies are income-based. For instance, a family of four earning $100,000 annually might receive substantial premium tax credits, but a modest income increase to $104,000 could push them above the subsidy threshold, resulting in a sudden spike in premiums. This "subsidy cliff" can lead to premiums increasing by hundreds or even thousands of dollars annually, depending on the plan and location.

Consider a practical example: a 45-year-old individual in Texas earning $50,000 might pay $200 monthly for a Silver plan with a $1,500 deductible, thanks to subsidies. If their income rises to $55,000, they could lose eligibility for cost-sharing reductions and premium tax credits, causing their monthly premium to jump to $450 or more. This increase is exacerbated if they choose to maintain a similar level of coverage, as higher-tier plans (Gold or Platinum) become significantly more expensive without subsidies. The result is a double financial blow: higher premiums and reduced assistance with out-of-pocket costs like deductibles and copays.

To mitigate this impact, individuals should proactively assess their income changes and insurance options. For example, if an income increase is anticipated, compare plans during open enrollment to find the most cost-effective option, even if it means switching to a Bronze plan with higher deductibles but lower premiums. Additionally, contributing to a Health Savings Account (HSA) can offset out-of-pocket costs, especially if paired with a high-deductible plan. For those near the subsidy threshold, consulting a tax professional or insurance broker can help strategize income reporting or explore alternative coverage options, such as employer-sponsored plans or short-term health insurance.

The takeaway is clear: income increases can trigger a cascade of financial consequences in health insurance, particularly for those reliant on subsidies. By understanding the mechanics of subsidy thresholds and proactively planning, individuals can minimize the premium impact and avoid unexpected out-of-pocket expenses. For example, a family earning $102,000 might strategically delay a bonus or adjust their tax withholdings to stay within the subsidy-eligible income range, ensuring they maintain affordable coverage. This requires vigilance and foresight but can significantly soften the blow of the subsidy cliff.

Get Free Medical Insurance in California: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Coverage Options: Shift to non-subsidized plans or employer-based insurance alternatives

As income rises, individuals often face a reduction or complete phase-out of health insurance subsidies, prompting a strategic reevaluation of coverage options. One immediate consideration is the shift to non-subsidized plans, which, while more expensive, offer greater flexibility in provider networks and coverage limits. For instance, a family earning $70,000 annually might lose access to premium tax credits under the Affordable Care Act (ACA), making a Bronze plan on the marketplace unaffordable. Transitioning to a non-subsidized Silver or Gold plan could provide broader coverage, including lower deductibles and out-of-pocket maximums, albeit at a higher monthly premium. This option is particularly appealing for those with chronic conditions or anticipated high medical expenses.

Employer-based insurance alternatives emerge as another viable pathway, especially for those whose income increase aligns with job advancement. Employers often subsidize a significant portion of premiums, reducing the financial burden compared to individual market plans. For example, a mid-sized company might cover 70% of the premium for a comprehensive PPO plan, which includes access to a wide network of specialists and lower copays. However, this option requires careful comparison of employer-offered plans against individual market options, as some employer plans may have higher deductibles or limited provider networks. Employees should also consider the impact of contributions to Health Savings Accounts (HSAs), which can offset costs through tax-advantaged savings.

A comparative analysis reveals that non-subsidized plans often provide more customization but at a steeper cost, while employer-based plans offer cost-sharing benefits but less portability. For instance, a self-employed individual transitioning to a salaried position might find employer-based insurance more cost-effective, whereas a freelancer with fluctuating income may prefer the stability of a non-subsidized plan. Additionally, individuals nearing Medicare eligibility (age 65) should weigh the long-term benefits of maintaining a non-subsidized plan versus transitioning to employer coverage, as Medicare will eventually become the primary insurer.

Practical tips for navigating this shift include using online tools like Healthcare.gov or private insurance marketplaces to compare plan costs and benefits. Consulting a licensed insurance broker can provide personalized guidance, especially when evaluating employer plans. For those with dependents, consider family plans versus individual policies, as employer-based family coverage often offers better value. Finally, monitor income changes annually to reassess subsidy eligibility, as even slight fluctuations can reopen access to subsidized plans or necessitate a return to non-subsidized options. This proactive approach ensures continuous, affordable coverage despite income-driven subsidy adjustments.

Medicaid Insurance: Reporting Additional Coverage?

You may want to see also

Explore related products

![]()

Policy Adjustments: Annual subsidy recalculations to reflect updated income levels

Income fluctuations can significantly impact health insurance subsidies, often leaving individuals under or over-subsidized. To address this disparity, annual subsidy recalculations based on updated income levels have emerged as a crucial policy adjustment. This approach ensures that subsidies remain aligned with current financial circumstances, promoting fairness and efficiency in the healthcare system. By periodically reassessing income, policymakers can prevent subsidy overpayments to higher earners and ensure adequate support for those with reduced income.

Implementing Annual Recalculations: A Step-by-Step Guide

- Establish a Recalculation Schedule: Set a fixed date or period, such as the start of each calendar year or tax season, for subsidy recalculations. This provides a consistent timeline for individuals to update their income information.

- Streamline Reporting Processes: Develop user-friendly platforms or tools that enable individuals to report income changes accurately and efficiently. Consider integrating with existing tax or employment systems to minimize administrative burden.

- Define Income Verification Methods: Determine acceptable forms of income verification, such as pay stubs, tax returns, or employer statements, to ensure the accuracy of reported income levels.

- Adjust Subsidy Formulas: Modify subsidy calculation formulas to account for updated income data, ensuring that adjustments are proportional and reflect current financial situations.

Cautions and Considerations

While annual recalculations offer numerous benefits, policymakers must navigate potential challenges. Frequent subsidy adjustments may lead to confusion or frustration among individuals, particularly those with volatile income streams. To mitigate this, consider implementing a grace period or phase-in approach for significant subsidy changes. Additionally, ensure that recalculation processes are transparent and easily understandable, providing clear explanations for any adjustments made.

Real-World Examples and Best Practices

Countries like the United States and Singapore have implemented annual subsidy recalculations with varying degrees of success. In the US, the Affordable Care Act's subsidy system requires individuals to report income changes annually, with adjustments made during open enrollment periods. Singapore's MediShield Life scheme, on the other hand, automatically recalibrates subsidies based on updated income tax assessments, reducing administrative burden and ensuring timely adjustments. By examining these examples, policymakers can identify best practices and tailor recalculation approaches to their specific healthcare contexts.

Maximizing Impact: Practical Tips for Individuals

To make the most of annual subsidy recalculations, individuals should:

- Stay Informed: Regularly review subsidy eligibility criteria and recalculation schedules to ensure timely updates.

- Maintain Accurate Records: Keep detailed income records, including pay stubs, tax returns, and employer statements, to facilitate smooth recalculations.

- Report Changes Promptly: Notify relevant authorities of significant income changes, such as job loss or promotion, to avoid subsidy discrepancies.

- Seek Assistance: Consult healthcare navigators or financial advisors for guidance on subsidy recalculations and income reporting requirements.

By embracing annual subsidy recalculations and adopting best practices, policymakers and individuals can work together to create a more responsive and equitable health insurance subsidy system. This approach not only ensures that subsidies remain aligned with current income levels but also promotes long-term sustainability and fairness in healthcare financing.

Minimum Wage Workers: Medical Insurance Coverage?

You may want to see also

Frequently asked questions

An increase in income may reduce or eliminate your eligibility for health insurance subsidies, as subsidies are typically income-based and phase out above certain thresholds.

Yes, as your income rises, your health insurance subsidy will likely decrease, as subsidies are calculated to cover a portion of the premium based on your income level.

If your income exceeds the eligibility threshold for subsidies, you will no longer qualify for financial assistance and will need to pay the full premium for your health insurance plan.

Yes, if your income decreases in the future, you can reapply for subsidies during the open enrollment period or through a special enrollment period if you qualify.

![Property and Casualty Insurance License Exam Study Guide - Property and Casualty Exam Secrets, Practice Test Questions, Detailed Answer Explanations [2nd Edition]](https://m.media-amazon.com/images/I/71fBYXIP4iL._AC_UL320_.jpg)