Insuring oneself against injury is a critical aspect of financial planning, as it provides a safety net to cover medical expenses, lost wages, and other costs associated with unexpected accidents or disabilities. There are several types of insurance policies designed to address these risks, including health insurance, disability insurance, and personal accident insurance. Health insurance typically covers medical treatments and hospitalization, while disability insurance replaces a portion of lost income if an injury prevents you from working. Personal accident insurance offers lump-sum payouts or coverage for specific injuries, such as fractures or burns. To choose the right coverage, individuals should assess their lifestyle, occupation, and potential risks, as well as compare policies to ensure adequate protection without unnecessary costs. Additionally, understanding policy terms, exclusions, and claim processes is essential to maximize benefits in case of injury.

Explore related products

What You'll Learn

![]()

Understanding Personal Injury Insurance

Personal injury insurance, often overlooked until it’s too late, serves as a financial safety net for unforeseen accidents. Unlike health insurance, which covers medical bills, personal injury insurance compensates for lost wages, rehabilitation costs, and even emotional distress resulting from an injury. For instance, if a 35-year-old accountant breaks their wrist in a car accident and cannot work for six weeks, this policy could replace up to 80% of their lost income, depending on the plan. Understanding its scope is the first step in ensuring you’re adequately protected.

When selecting a personal injury insurance policy, scrutinize the coverage limits and exclusions. Policies typically range from $10,000 to $1 million in benefits, with premiums varying based on age, occupation, and lifestyle. A construction worker, for example, will face higher premiums due to increased risk compared to an office worker. Additionally, some policies exclude injuries from high-risk activities like skydiving or racing. To avoid gaps, compare multiple providers and consider bundling with other insurance types for potential discounts.

One common misconception is that workers’ compensation or auto insurance fully covers personal injuries. While workers’ comp addresses job-related injuries, it doesn’t cover accidents outside the workplace. Similarly, auto insurance liability only pays for damages to others, not your own losses. Personal injury insurance bridges these gaps, offering comprehensive protection regardless of where or how the injury occurs. For instance, a cyclist hit by a car could use this policy to cover physical therapy costs not addressed by other insurances.

Finally, timing matters when filing a claim. Most policies require notification within 30 days of the injury, with detailed documentation of medical treatments and financial losses. Keep a record of all expenses, including transportation to appointments and over-the-counter medications. Prompt action ensures smoother processing and faster payouts. By understanding these nuances, you can transform personal injury insurance from an afterthought into a proactive tool for financial resilience.

Does Tesco Offer Van Insurance? A Comprehensive Guide for UK Drivers

You may want to see also

Explore related products

![]()

Types of Injury Coverage Policies

Injury coverage policies are not one-size-fits-all; they vary widely based on the type of injury, the insured’s lifestyle, and the financial protection needed. For instance, health insurance is the most common form of injury coverage, but it often excludes high-risk activities like extreme sports. If you’re a rock climber or a motocross enthusiast, your standard health plan might leave you exposed to significant out-of-pocket costs. This gap highlights the need for specialized policies tailored to specific risks.

Consider disability insurance, which provides income replacement if an injury prevents you from working. Unlike health insurance, which covers medical bills, disability insurance ensures financial stability during recovery. For example, a 35-year-old software engineer earning $80,000 annually could secure a policy replacing 60–70% of their income. However, premiums vary based on occupation, health, and the waiting period before benefits kick in. Typically, a 90-day waiting period lowers costs but delays support.

For athletes or professionals in physically demanding fields, accident insurance is a critical supplement. This policy pays a lump sum or fixed benefits for specific injuries, such as fractures or concussions, regardless of other coverage. For instance, a policy might offer $5,000 for a broken leg, which can offset deductibles or lost wages. Premiums are relatively low, often $20–$50 monthly, making it an affordable add-on for high-risk individuals.

Travelers and expatriates should explore international health insurance with injury coverage. Standard domestic plans rarely cover medical expenses abroad, and emergency evacuations can cost upwards of $50,000. Policies like those from Cigna Global or GeoBlue include injury treatment, repatriation, and even trip interruption benefits. For a 40-year-old traveler, premiums might range from $100 to $300 monthly, depending on coverage limits and destination risk.

Lastly, critical illness insurance provides a payout upon diagnosis of severe conditions often linked to injuries, such as paralysis or loss of limbs. This coverage is particularly valuable for those without substantial savings, as it can cover non-medical costs like home modifications or experimental treatments. A $50,000 policy for a 30-year-old nonsmoker might cost $30–$50 monthly, offering peace of mind against life-altering injuries.

In summary, selecting the right injury coverage requires assessing your lifestyle, occupation, and financial vulnerabilities. Combining policies—such as health, disability, and accident insurance—creates a robust safety net. Always review exclusions, waiting periods, and benefit limits to ensure comprehensive protection.

Is My Transamerica Life Insurance Active?

You may want to see also

Explore related products

![]()

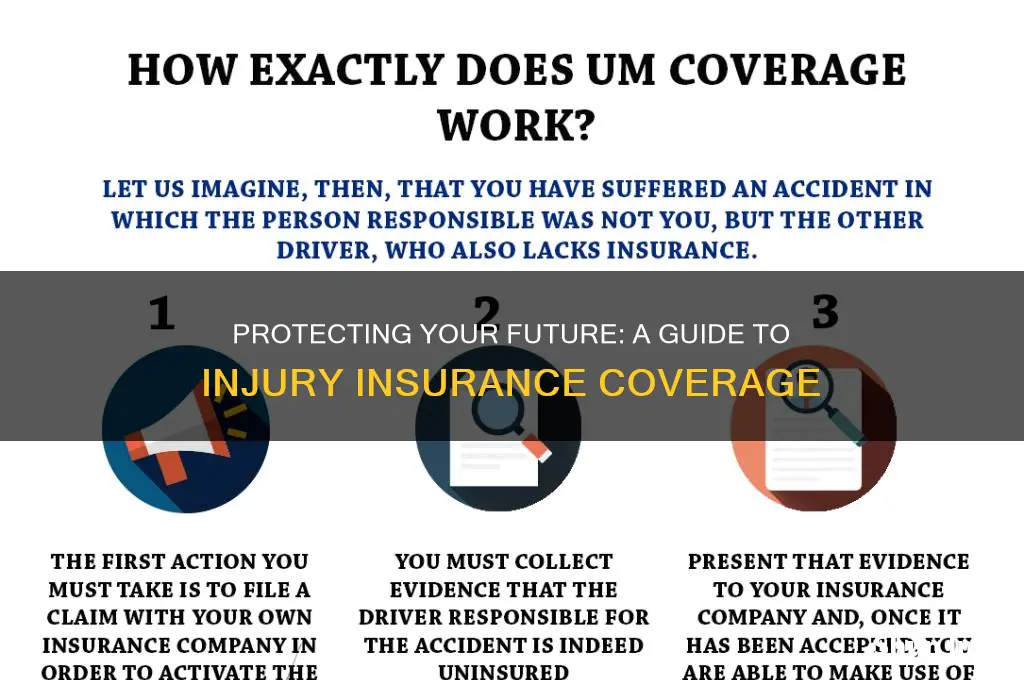

Steps to File an Injury Claim

Filing an injury claim can feel overwhelming, especially when you're already dealing with the physical and emotional aftermath of an accident. However, understanding the process can significantly reduce stress and increase your chances of a fair settlement. Here’s a step-by-step guide to navigating the claims process effectively.

Step 1: Seek Medical Attention Immediately

Your health is the top priority. Even if injuries seem minor, some symptoms, like whiplash or internal bleeding, may not manifest immediately. Documenting your injuries through medical records is crucial for your claim. Delaying treatment can not only worsen your condition but also weaken your case, as insurers may argue that your injuries aren’t severe or related to the incident. For instance, if you’re in a car accident, visit an emergency room or urgent care facility within 24 hours, even if you feel fine.

Step 2: Report the Incident Promptly

Notify the relevant parties as soon as possible. If it’s a workplace injury, inform your employer within the timeframe specified by your state’s workers’ compensation laws (typically 30 days). For car accidents, file a police report at the scene if possible. If you’re injured on someone else’s property, report it to the owner or manager and ensure they document the incident. Delays in reporting can raise doubts about the legitimacy of your claim.

Step 3: Gather and Organize Evidence

Evidence is the backbone of your claim. Collect photos of the accident scene, your injuries, and any property damage. Obtain contact information from witnesses and keep a detailed journal of your symptoms, treatments, and how the injury impacts your daily life. For example, note if you’re unable to perform household chores or miss work. Save all receipts for medical expenses, prescriptions, and transportation to appointments. This documentation will help prove the extent of your losses.

Step 4: Notify Your Insurance Company

Contact your insurer promptly to initiate the claims process. Provide accurate, concise details about the incident but avoid admitting fault. Stick to the facts. For instance, if you’re filing a health insurance claim, submit medical bills and a doctor’s note outlining the treatment needed. If it’s a liability claim (e.g., a slip-and-fall), your insurer will likely investigate before approving coverage. Be prepared for follow-up questions and requests for additional documentation.

Step 5: Consult an Attorney if Necessary

While not every injury claim requires legal representation, complex cases—such as those involving severe injuries, disputed liability, or large settlements—often benefit from an attorney’s expertise. A personal injury lawyer can negotiate with insurers, ensure compliance with legal deadlines, and represent you in court if needed. Most attorneys offer free consultations, so you can assess your options without upfront costs. For example, if an insurer offers a settlement that doesn’t cover your long-term medical needs, an attorney can help you pursue a fairer outcome.

Cautions and Practical Tips

Avoid posting about your injury on social media, as insurers may use your posts against you. Be cautious when speaking to insurance adjusters; they may try to minimize your claim. Always review settlement offers carefully—once accepted, you typically can’t seek additional compensation later. Finally, keep all communication professional and factual. Emotional outbursts or exaggerated claims can undermine your credibility.

By following these steps, you’ll be better equipped to navigate the injury claims process and secure the compensation you deserve. Preparation and persistence are key to a successful outcome.

Mastering Darius: Strategies to Secure Ultimate Kills in Every Match

You may want to see also

Explore related products

![]()

Choosing the Right Insurance Provider

Selecting an insurance provider is akin to choosing a long-term partner—reliability, trust, and compatibility are non-negotiable. Start by evaluating the provider’s financial stability through ratings from agencies like A.M. Best or Standard & Poor’s. A company with an A+ or A rating ensures they can meet claims obligations, even in economic downturns. For instance, providers like State Farm and USAA consistently rank high in financial strength, offering peace of mind for injury-related policies.

Next, scrutinize the policy’s coverage limits and exclusions. Injury insurance often varies in scope, from accidental death and dismemberment (AD&D) to disability coverage. For example, a 30-year-old professional might prioritize a policy with a $500,000 payout for severe injuries, while a freelancer may opt for income replacement benefits. Ensure the provider offers customizable plans to align with your lifestyle and risk exposure.

Customer service is another critical factor. In the aftermath of an injury, the last thing you need is a bureaucratic nightmare. Look for providers with 24/7 claims support, digital claim filing, and a history of quick settlements. Progressive and Allstate, for instance, are praised for their user-friendly apps and responsive service teams. Read reviews and ask for recommendations to gauge real-world experiences.

Finally, compare costs without compromising quality. Premiums for injury insurance typically range from $20 to $100 monthly, depending on coverage and risk factors. Use online comparison tools like Policygenius or The Zebra to evaluate quotes from multiple providers. Remember, the cheapest option may skimp on coverage or service, so balance affordability with value.

Joining Insurance Panels: A Psychologist's Guide to Credentialing Success

You may want to see also

Explore related products

![]()

Preventive Measures to Reduce Injury Risks

Injury prevention begins with awareness of your environment and the activities you engage in. For instance, slips and falls account for over 1 million hospital visits annually in the U.S. alone. A simple yet effective preventive measure is to ensure proper lighting in your home, especially on staircases and in hallways. Installing handrails and using non-slip mats in bathrooms and kitchens can significantly reduce the risk of falls. Additionally, wearing appropriate footwear with good traction, both indoors and outdoors, is a small but impactful habit that can prevent accidents.

Consider the role of physical conditioning in injury prevention, particularly for those who engage in sports or physically demanding jobs. Strengthening muscles and improving flexibility can act as a natural buffer against injuries. For example, athletes who incorporate dynamic stretching into their warm-up routines experience 50% fewer injuries compared to those who skip this step. Adults over 30 should focus on exercises that enhance core stability and balance, such as yoga or Pilates, to mitigate age-related declines in coordination. Even a 20-minute daily routine can make a substantial difference in reducing injury risks.

Technology offers innovative tools to minimize injury risks, especially in high-risk environments. Wearable devices like smart helmets for cyclists or construction workers can detect falls or impacts and alert emergency contacts. Similarly, ergonomic assessments in workplaces can identify potential hazards and suggest adjustments to reduce strain. For instance, using an adjustable standing desk can alleviate back pain and prevent long-term spinal issues. Investing in such preventive technologies is not just a cost but a long-term strategy to safeguard health and productivity.

Finally, education and consistent practice of safety protocols are paramount. Whether it’s following traffic rules while cycling or adhering to safety guidelines in a gym, knowledge combined with action is key. For families, teaching children basic safety measures, such as looking both ways before crossing the street or wearing helmets while riding bikes, instills lifelong habits. Regularly updating oneself on safety standards and best practices ensures that preventive measures remain effective in evolving environments. Small, consistent efforts in these areas collectively create a robust defense against injuries.

Life Insurance: A Family's Path to Wealth and Security

You may want to see also

Frequently asked questions

Common types include health insurance, disability insurance, workers' compensation, and personal accident insurance, each covering different aspects of injury-related expenses.

Health insurance typically covers medical bills, but may not include lost wages, long-term care, or non-medical expenses unless supplemented with additional policies.

Disability insurance provides income replacement if you're unable to work due to an injury, ensuring financial stability during recovery.

Workers' compensation is typically for employees, but self-employed individuals can purchase similar coverage through private insurers to protect against work-related injuries.

Personal accident insurance provides a lump-sum payout or specific benefits for accidental injuries, regardless of medical costs, while health insurance covers treatment expenses.