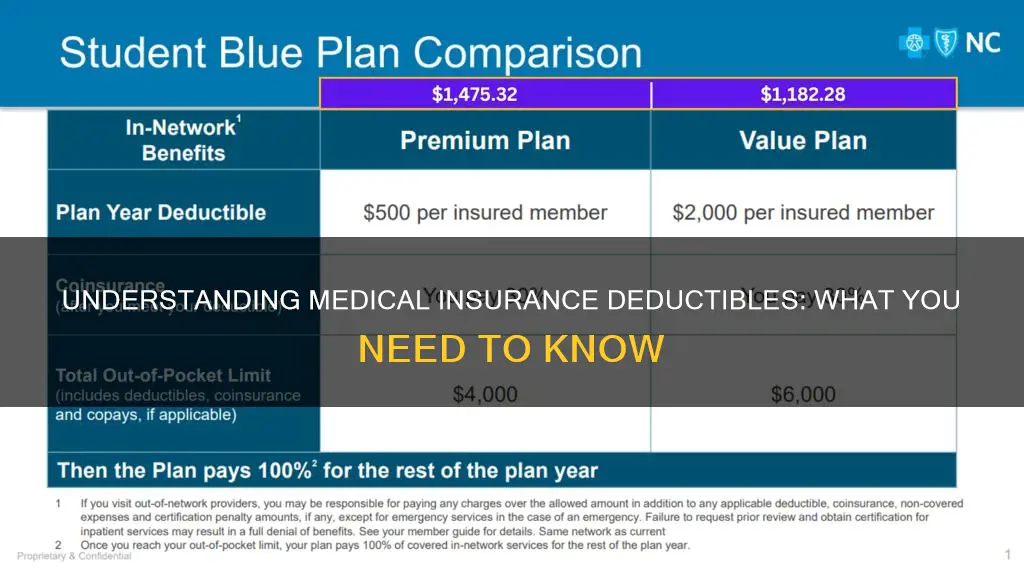

Understanding how deductibles work is essential for choosing a health insurance plan that suits your needs. A deductible is the amount you pay out-of-pocket for covered healthcare services before your insurance plan starts contributing. In other words, you are responsible for paying 100% of the services covered by your insurance plan until you reach your deductible. Once you've met your deductible, you start sharing costs with your insurer, often through coinsurance, where you pay a percentage of the cost. The higher your deductible, the lower your premium (the amount you pay each month for your plan), and vice versa. This means that with a high-deductible plan, you may pay less each month but more for out-of-pocket costs, while a low-deductible plan typically has higher monthly premiums but lower out-of-pocket expenses.

| Characteristics | Values |

|---|---|

| Definition | A deductible is the amount you pay for out-of-pocket costs for your covered health care before your plan begins to pay. |

| Types | Individual deductible, family deductible, high deductible health plan (HDHP), low deductible health plan |

| Average yearly deductible | $5,101 for individuals, $10,310 for families |

| Average deductible for marketplace plans | $7,481 for Bronze plans, $4,890 for Silver plans, $1,650 for Gold plans, $45 for Platinum plans |

| High deductible health plans | High deductibles can be a good fit for people who are generally healthy and rarely see a doctor. |

| HDHPs typically have higher deductibles but come with lower monthly premiums. | |

| HDHPs can be paired with a health savings account (HSA) where individuals can contribute pre-tax money to use for eligible medical expenses. | |

| Low deductible health plans | Low deductible plans have a lower upfront cost but higher monthly premiums. |

| Low deductible plans are a good option for people with chronic health conditions or a high risk of sports injuries. | |

| Coinsurance | The portion of the medical cost you pay after your deductible has been met. |

| Copay | A fixed amount you pay out of pocket for a health care service, usually when you receive the service. |

Explore related products

What You'll Learn

![]()

High-deductible health plans (HDHPs)

A deductible is the amount you pay for out-of-pocket costs before your insurance plan begins to pay. A health insurance policy is considered a High-Deductible Health Plan (HDHP) when it has a deductible of at least $1,400 for individual coverage or $2,800 for family coverage. These plans typically have higher deductibles but come with lower monthly premiums. They are designed to offer more significant cost-sharing responsibilities to the insured individuals.

HDHPs are of high interest to employers, policy-makers, and insurers because of potential benefits and risks of this fundamentally new coverage model. Some of the advantages of HDHPs include the option to pair with a Health Savings Account (HSA), where individuals can contribute pre-tax money to be used for eligible medical expenses. If the funds aren't spent, they roll over year to year.

HDHPs may be a good fit if you are generally healthy and rarely need to see a doctor. On the other hand, if you have a chronic health condition or a high risk of sports injuries, a low-deductible plan may be a better option. With a low-deductible plan, you pay more each month for your premium and less of your out-of-pocket costs until you pay off your lower deductible.

It's important to note that even after reaching your deductible, you may still have to pay some out-of-pocket costs, which don't count towards your deductible. These include the premium, copay or coinsurance, and the out-of-pocket maximum.

Adult Children's Medical Insurance Coverage Under Parents' Plans

You may want to see also

Explore related products

![]()

Low-deductible health plans

A health insurance deductible is the amount you pay for out-of-pocket costs before your insurance plan begins to pay. A low-deductible health plan (LDHP) is one in which the deductible is less than $1,650 for self-only coverage or $3,300 for family insurance coverage.

LDHPs have a higher upfront monthly premium and a lower deductible, meaning that insurance payments start earlier. This can be beneficial for individuals who expect to need regular medical care or have chronic health conditions. The higher monthly premiums are a trade-off for lower out-of-pocket costs, which can be helpful during unexpected health emergencies or illnesses. This type of plan may be suitable for those who are generally less healthy, have a high risk of sports injuries, or anticipate high-cost care.

The main advantage of LDHPs is that they provide quicker access to insurance coverage. Since the deductible is lower, insurance benefits kick in sooner, reducing the financial burden during unexpected health events. This can provide peace of mind and predictability in terms of healthcare expenses. LDHPs may also be preferable for those who want to avoid the potential high costs associated with high-deductible plans if they end up needing extensive medical care.

It is important to note that even after reaching your deductible, there may still be separate "out-of-pocket" expenses that don't count toward your deductible. These may include premiums, copays, and coinsurance. Therefore, when considering an LDHP, it is essential to also look at the out-of-pocket maximum, which represents the total amount of medical expenses you may pay for the year, excluding premiums.

Medical Insurance Premiums: AGI Impact and Exclusions

You may want to see also

Explore related products

$17.99 $17.99

![]()

Individual deductible

An individual deductible is a specific type of deductible that applies to individual health insurance plans, providing coverage for one person. It represents the amount that the insured individual must pay out-of-pocket before their insurance coverage begins to share the costs of medical expenses. This means that the individual must pay 100% of the services covered by their insurance plan until they reach their deductible amount. Once the deductible is met, the insurance company will start paying for their insurance-covered medical expenses.

For example, if an individual has a $1,000 deductible and they receive a medical bill for $1,300, they would be responsible for paying the first $1,000 out-of-pocket, and their insurance would cover the remaining $300. It is important to note that the individual may still be responsible for a copayment or coinsurance, even after the deductible is met. A copayment is a fixed amount that the individual pays at the time of their appointment, while coinsurance is a percentage of the total cost that the individual is responsible for paying.

The individual deductible is an important consideration when choosing a health insurance plan, as it can impact the monthly premiums and out-of-pocket expenses. Typically, a high-deductible plan comes with lower monthly premiums, while a low-deductible plan has a higher upfront monthly premium. Individuals with chronic medical conditions or those who require frequent medical care may prefer a low-deductible plan to help manage their out-of-pocket expenses. On the other hand, individuals with a healthy lifestyle and infrequent need for medical care may opt for a high-deductible plan to save on their monthly premiums.

It is worth noting that some health insurance plans have separate deductibles for medical services and prescription drugs, and different deductibles for in-network and out-of-network services. It is crucial to carefully review the terms of a health plan before making a decision to ensure a clear understanding of the deductibles and how they apply.

Medicaid and Spousal Insurance: Can I Keep Both?

You may want to see also

Explore related products

![]()

Family deductible

A health insurance deductible is the amount you pay before your insurance coverage starts sharing the costs. A family deductible is a type of deductible that applies to family health insurance plans, providing coverage for the entire family. It represents the total amount that the family members must collectively pay out-of-pocket before their insurance coverage begins to share the costs of medical expenses.

The family deductible can be met by a combination of two or more family members' costs. For example, if you have a family deductible of $3,000 and you meet this amount through a combination of two or more family members' medical expenses, then the after-deductible benefits kick in for the entire family, and you save up to $4,500 in deductible costs if each family member needs extensive medical treatment.

The family deductible is often double the individual deductible amount. For instance, in 2024, the average individual yearly deductible was $5,101, while for families, it was $10,310. In 2023, the average deductible for marketplace plans for medical and prescription drugs was $7,481 for Bronze plans, $4,890 for Silver plans, $1,650 for Gold plans, and $45 for Platinum plans.

It is important to note that the family deductible only applies to family members who are covered under the same policy. If family members are covered by more than one health policy, each policy will have its own separate deductibles and out-of-pocket maximums.

When choosing a family health insurance plan, it is essential to consider the health needs of your family. Family deductibles can vary depending on the plan, and you may want to opt for a low or high-deductible plan based on your family's health status and anticipated medical expenses.

Medicaid and Life Insurance: What Happens After Death?

You may want to see also

Explore related products

![]()

Out-of-pocket costs

If you use out-of-network providers, your out-of-pocket costs can be considerably higher than the stated limits. On some plans, they're double the in-network limits, but on other plans, out-of-pocket costs can be unlimited for care from providers that aren't in the health plan's network. It's increasingly common to see plans that simply don't cover out-of-network care at all, unless it's an emergency.

You can estimate your out-of-pocket costs by reviewing your insurance coverage, annual deductible, and out-of-pocket maximum. The out-of-pocket maximum is the most you'll pay for allowed health care costs in a plan year. If you reach this amount, your plan pays 100% of your care.

California Tax Deductions: Medical Insurance Claims and Benefits

You may want to see also

Frequently asked questions

A deductible is the amount you pay for covered health care services before your insurance plan begins to pay. It is different from a premium, which is the amount you pay to have health insurance, usually every month.

Deductibles may be low or high, depending on the plan you choose. With a high-deductible plan, you pay less each month for your premium but more for your out-of-pocket costs until you pay 100% of your deductible. On the other hand, with a low-deductible plan, you pay a higher premium each month and lower out-of-pocket costs.

Out-of-pocket costs are expenses that you pay for covered medical services before your insurance plan starts contributing. These include things like copays, coinsurance, and the deductible itself. Once you reach your out-of-pocket maximum, your insurance plan will pay for your covered medical and prescription costs for the rest of the year.