The stock market and the health insurance marketplace are interconnected in ways that may not be immediately apparent, yet their relationship significantly impacts both individual consumers and the broader economy. Fluctuations in the stock market can influence the financial stability of health insurance companies, many of which are publicly traded, affecting their ability to manage risk, set premiums, and invest in healthcare innovations. Additionally, economic conditions driven by stock market performance can shape consumer behavior, as individuals may opt for lower-cost health plans during downturns or prioritize comprehensive coverage in more prosperous times. Furthermore, the stock market’s impact on employer-sponsored health insurance—a cornerstone of the U.S. healthcare system—cannot be overlooked, as corporate financial health directly ties to the benefits they can offer employees. Understanding this dynamic interplay is crucial for policymakers, insurers, and consumers alike, as it highlights how financial markets indirectly shape access to and the affordability of healthcare.

| Characteristics | Values |

|---|---|

| Investment in Health Insurance Companies | Stock market performance directly impacts the valuation and investment in health insurance companies. Higher stock prices can increase capital for expansion, technology adoption, and improved services. |

| Consumer Confidence and Spending | A strong stock market often boosts consumer confidence, leading to higher discretionary spending, including on health insurance premiums and out-of-pocket healthcare costs. |

| Employer-Sponsored Insurance | Stock market gains can improve corporate profitability, encouraging employers to offer more comprehensive health insurance benefits or contribute more to employee premiums. |

| Interest Rates and Investment Returns | Stock market trends influence interest rates, affecting health insurers' investment returns on reserves. Higher returns can stabilize premiums or fund new initiatives. |

| Mergers and Acquisitions (M&A) | A robust stock market facilitates M&A activity in the health insurance sector, leading to consolidation, cost efficiencies, and potentially lower premiums for consumers. |

| Regulatory and Policy Impact | Stock market volatility can influence government policies related to healthcare and insurance, as lawmakers may respond to economic pressures affecting the industry. |

| Innovation and Technology Adoption | Higher stock valuations enable health insurers to invest in telemedicine, AI, and data analytics, improving service delivery and reducing long-term costs. |

| Individual Market Behavior | Stock market performance affects individual financial health, impacting decisions to purchase or maintain health insurance, especially in the private market. |

| Global Economic Influence | International stock market trends can affect multinational health insurers' operations, supply chains, and financial stability, indirectly impacting local markets. |

| Risk and Uncertainty | Stock market volatility introduces uncertainty, potentially increasing demand for health insurance as a hedge against unexpected medical expenses. |

Explore related products

What You'll Learn

- Stock volatility impacts insurer investment returns, affecting policy pricing and coverage options

- Market performance influences employer-sponsored health plans and employee benefits

- Insurer stock trends reflect industry stability, shaping consumer trust and choices

- Economic downturns reduce disposable income, increasing demand for affordable health plans

- High stock returns enable insurers to invest in technology, improving service efficiency

![]()

Stock volatility impacts insurer investment returns, affecting policy pricing and coverage options

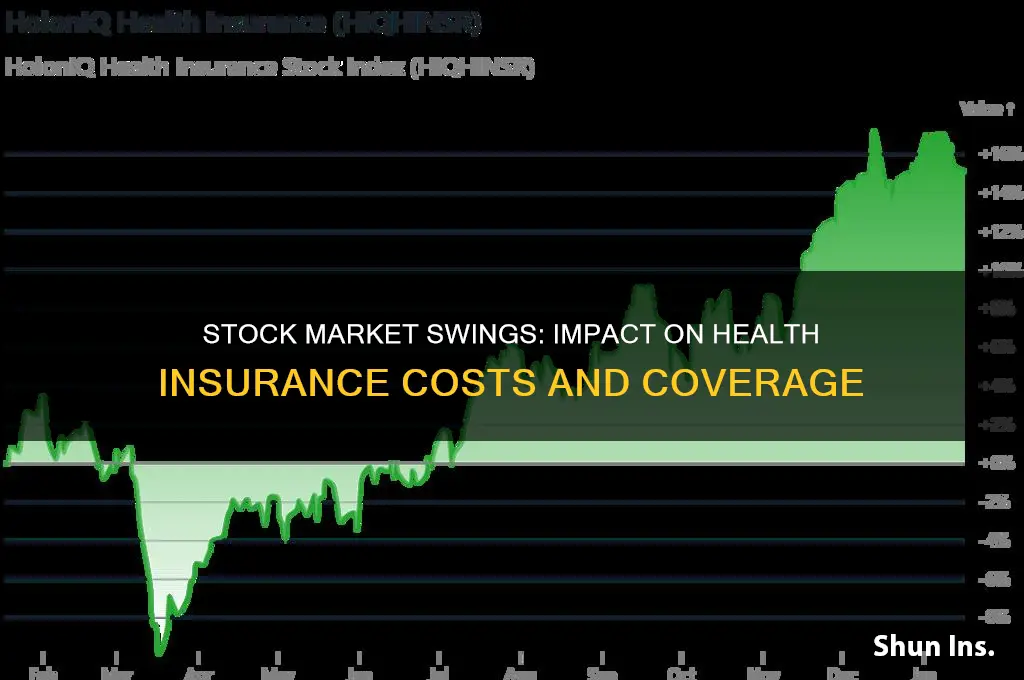

Stock market volatility directly affects the investment portfolios of health insurance companies, which in turn influences their financial stability and operational decisions. Insurers often invest policyholder premiums in stocks, bonds, and other assets to generate returns that offset claims payouts and administrative costs. When stock markets experience significant fluctuations, the value of these investments can decline rapidly, reducing insurers' overall capital. This diminished financial cushion forces companies to reassess their risk exposure, often leading to adjustments in policy pricing and coverage options to maintain profitability.

Consider a scenario where a major market downturn causes a 20% drop in an insurer's investment portfolio. To compensate for the loss, the insurer might raise premiums for policyholders, particularly in high-risk categories such as older adults or individuals with pre-existing conditions. Alternatively, they may reduce coverage for expensive treatments like specialized cancer therapies or mental health services. For instance, a family plan that previously covered 80% of chemotherapy costs might be adjusted to cover only 60%, shifting more financial burden onto the policyholder. These changes are not arbitrary but are calculated responses to ensure the insurer remains solvent in a volatile economic environment.

From a strategic perspective, insurers may also alter their investment strategies during periods of high volatility. Instead of relying heavily on equities, they might shift toward more stable but lower-yield assets like government bonds or treasury bills. While this reduces exposure to market risk, it also lowers potential returns, creating a ripple effect that further pressures policy pricing. For example, a mid-sized insurer with a $500 million portfolio might reduce its stock allocation from 60% to 30%, accepting a 2% decrease in annual returns. To offset this, they could increase premiums by 5% across all plans, a decision that directly impacts affordability for consumers.

Policyholders can mitigate the impact of these changes by proactively reviewing their coverage and exploring alternatives. For instance, individuals with employer-sponsored plans might opt for high-deductible health plans (HDHPs) paired with health savings accounts (HSAs), which offer tax advantages and greater control over healthcare spending. Those in the individual market could consider joining healthcare sharing ministries or short-term health plans, though these options often exclude pre-existing conditions. Additionally, negotiating directly with providers for discounted rates or payment plans can help offset higher out-of-pocket costs resulting from reduced coverage.

In conclusion, stock market volatility creates a chain reaction that permeates the health insurance marketplace, from insurer investment strategies to policyholder premiums and coverage. Understanding this dynamic empowers consumers to make informed decisions, such as diversifying their own investments to build a financial buffer or advocating for policy reforms that stabilize healthcare costs. While insurers must navigate economic uncertainty to remain viable, transparency and adaptability are key to balancing their financial health with the needs of policyholders.

Affordable Health Insurance Strategies for Small Business Owners

You may want to see also

Explore related products

![]()

Market performance influences employer-sponsored health plans and employee benefits

The stock market's volatility directly impacts the funding and sustainability of employer-sponsored health plans. When markets perform well, companies often see increased profits, which can lead to more generous health benefits for employees. For instance, during bull markets, employers might expand coverage options, reduce employee premiums, or introduce wellness programs. Conversely, during downturns, cost-cutting measures may include scaling back benefits, increasing deductibles, or shifting more costs to employees. This dynamic highlights how market performance is a critical factor in shaping the scope and quality of health insurance offered through workplaces.

Consider the role of self-insured employer plans, which cover over 60% of workers in the U.S. These plans are funded directly by employers, making them highly sensitive to market fluctuations. In prosperous times, companies may reinvest surplus funds into richer benefits, such as lower copays or expanded mental health services. However, during economic contractions, employers might reduce contributions to health plans, forcing employees to shoulder a larger financial burden. For example, a 2020 survey by the Kaiser Family Foundation found that 41% of employers reconsidered their health benefits due to pandemic-related financial pressures, illustrating the immediate impact of market downturns on employee coverage.

From a strategic perspective, employers often tie health benefits to recruitment and retention goals, which are influenced by their financial health. In competitive job markets, robust health plans can be a differentiator, but only if the company’s stock performance supports such investments. For instance, tech companies with high stock valuations frequently offer comprehensive benefits, including fertility treatments and on-site health clinics, to attract top talent. In contrast, industries hit hard by market declines, such as retail or manufacturing, may struggle to maintain even basic health coverage, leading to higher employee turnover and reduced productivity.

A comparative analysis reveals that small and medium-sized businesses (SMBs) are particularly vulnerable to market-driven benefit changes. Unlike large corporations with diversified revenue streams, SMBs often rely heavily on market performance for profitability. For example, a small tech startup with stock-based funding might offer lavish health benefits during a funding boom but drastically cut them if investor confidence wanes. Employees in such environments must be proactive, negotiating benefits packages that include safeguards against sudden reductions or exploring supplemental insurance options to mitigate risk.

In conclusion, market performance acts as a barometer for the generosity and stability of employer-sponsored health plans. Employees should monitor their company’s financial health and industry trends to anticipate potential changes in benefits. Practical steps include diversifying personal health coverage, such as purchasing short-term health plans or health savings accounts (HSAs), and staying informed about policy changes during earnings reports or economic forecasts. By understanding this link, individuals can better navigate the intersection of financial markets and healthcare, ensuring they remain protected regardless of economic conditions.

Top Flood Insurance Providers in North Carolina: Your Comprehensive Guide

You may want to see also

Explore related products

![]()

Insurer stock trends reflect industry stability, shaping consumer trust and choices

The performance of health insurance stocks serves as a barometer for industry stability, influencing consumer perceptions and decisions in subtle yet profound ways. When insurer stocks trend upward, it signals financial health and operational efficiency, reassuring policyholders and prospective buyers about the company’s ability to meet long-term obligations. For instance, UnitedHealth Group’s consistent stock growth over the past decade has positioned it as a trusted leader, attracting consumers seeking reliability in an unpredictable market. Conversely, sudden stock declines, as seen with some regional insurers during economic downturns, can erode trust, prompting consumers to switch providers or seek alternatives like government-backed plans.

Analyzing stock trends requires more than a glance at price charts; it demands an understanding of underlying factors. A rise in stock value often correlates with successful cost-management strategies, such as negotiating lower drug prices or streamlining administrative processes. For example, CVS Health’s acquisition of Aetna in 2018 initially caused stock volatility but ultimately demonstrated the benefits of vertical integration, stabilizing its market position and consumer confidence. Consumers can leverage this insight by monitoring quarterly earnings reports and analyst ratings to gauge an insurer’s stability before renewing policies or enrolling in new plans.

The psychological impact of stock trends on consumer behavior cannot be overstated. Behavioral economics suggests that individuals equate financial performance with operational competence, even if the two are not always directly linked. A study by J.P. Morgan found that 62% of consumers are more likely to trust insurers with consistently high stock performance. To capitalize on this, insurers often highlight their stock performance in marketing campaigns, framing it as evidence of their ability to provide affordable, comprehensive coverage. Consumers should, however, balance this information with other metrics, such as customer satisfaction scores and claims processing efficiency, to make informed choices.

Practical steps for consumers include setting up alerts for insurer stock movements and correlating these trends with industry news. For instance, a sudden drop in stock value might indicate regulatory challenges or a major claim payout, warranting further investigation. Additionally, diversifying health insurance investments—such as pairing traditional plans with health savings accounts (HSAs)—can mitigate risks associated with insurer instability. For older adults (ages 55+), who often prioritize stability, focusing on insurers with a history of steady stock performance and high credit ratings (e.g., A.M. Best ratings of A++ or A+) can provide added peace of mind.

In conclusion, insurer stock trends are more than financial indicators; they are proxies for industry stability that shape consumer trust and decision-making. By interpreting these trends critically and combining them with other data points, consumers can navigate the health insurance marketplace with greater confidence. Whether renewing a policy or exploring new options, understanding the link between stock performance and insurer reliability is a valuable tool in securing optimal coverage.

Marketplace Insurance vs. Medicaid: What's the Difference?

You may want to see also

Explore related products

![]()

Economic downturns reduce disposable income, increasing demand for affordable health plans

Economic downturns, characterized by declining stock markets and reduced consumer spending, directly impact household finances. As disposable income shrinks, individuals and families reevaluate their budgets, often prioritizing essential expenses over discretionary spending. Health insurance, while critical, becomes a line item subject to scrutiny. During these periods, the demand for affordable health plans surges as consumers seek to balance protection against financial strain. For instance, during the 2008 financial crisis, enrollment in high-deductible health plans (HDHPs) increased by 14% as Americans sought lower premiums, even if it meant higher out-of-pocket costs.

This shift in demand forces health insurance providers to adapt their offerings. Insurers may introduce or expand low-cost plans, such as catastrophic coverage or short-term policies, to attract budget-conscious consumers. However, these plans often come with limitations, such as narrower networks or exclusions for pre-existing conditions, which can compromise care quality. Policymakers also play a role, as seen in the expansion of Medicaid during the Great Recession, which provided a safety net for millions of low-income individuals. Yet, eligibility criteria and state-level variations in Medicaid programs highlight the uneven distribution of benefits.

The interplay between economic downturns and health insurance demand underscores a broader challenge: affordability versus adequacy. While affordable plans alleviate immediate financial pressure, they may lead to underinsurance, where individuals forgo necessary care due to high out-of-pocket costs. For example, a study found that 44% of HDHP enrollees delayed or skipped care due to cost concerns. This trade-off between cost and coverage has long-term implications, as deferred care can exacerbate health issues, ultimately increasing healthcare costs for both individuals and society.

To navigate this landscape, consumers should carefully assess their health needs and financial situation when selecting a plan. Practical tips include comparing premiums, deductibles, and out-of-pocket maximums, as well as checking if preferred providers are in-network. Additionally, leveraging health savings accounts (HSAs) can offset costs for those in HDHPs. Employers can also play a role by offering flexible benefits packages or contributing to employee premiums. Ultimately, while economic downturns drive demand for affordable health plans, informed decision-making is crucial to avoid compromising long-term health for short-term savings.

Cook Insurance: Annual Salary Requirements Explored

You may want to see also

Explore related products

![]()

High stock returns enable insurers to invest in technology, improving service efficiency

The correlation between stock market performance and health insurance innovation is a fascinating aspect of the industry's evolution. High stock returns provide insurers with a unique opportunity to reinvest profits into technological advancements, ultimately enhancing the customer experience. This strategic move not only improves operational efficiency but also positions insurance companies as forward-thinking, tech-savvy entities in a highly competitive market.

A Financial Boost for Technological Transformation

When stock returns are favorable, health insurance companies find themselves with increased financial flexibility. This surplus allows them to allocate resources towards technology upgrades, a critical aspect of modernizing the insurance sector. For instance, insurers can invest in advanced data analytics platforms, enabling them to process vast amounts of healthcare data efficiently. By analyzing trends and patterns, companies can develop more accurate risk assessment models, leading to better-priced policies and reduced costs for consumers. This is particularly beneficial for older adults, aged 50 and above, who often require more comprehensive health coverage and can benefit from tailored insurance plans.

Enhancing Customer Experience Through Digital Innovation

The impact of technology investment is most evident in the customer journey. Insurers can develop user-friendly mobile applications, offering policyholders instant access to their insurance information. These apps can provide features such as digital ID cards, claims tracking, and even telemedicine services, allowing users to consult healthcare professionals remotely. For instance, a simple video call feature within the app can connect patients with doctors for minor ailments, reducing the need for in-person visits and potentially lowering healthcare costs. This level of accessibility and convenience is a direct result of insurers' ability to fund such technological initiatives through stock market gains.

Streamlining Operations for Efficiency

Behind the scenes, technology investments streamline insurance operations. Automated systems can handle routine tasks, such as policy administration and claims processing, with greater speed and accuracy. For example, optical character recognition (OCR) technology can extract data from medical documents, reducing manual entry errors. This not only speeds up claim settlements but also frees up resources, allowing insurers to focus on complex cases and customer support. As a result, policyholders experience faster response times and more efficient service, fostering trust and satisfaction.

A Competitive Edge in a Digital Age

In a market where consumer expectations are shaped by digital experiences, insurers with robust technological capabilities gain a significant advantage. High stock returns enable companies to stay ahead of the curve, continuously innovating to meet evolving demands. This might involve developing AI-powered chatbots for instant customer support or implementing blockchain technology for secure, transparent transactions. By embracing these advancements, insurers not only improve service efficiency but also attract tech-savvy consumers, ensuring long-term growth and sustainability.

In summary, the stock market's influence on the health insurance marketplace is a powerful catalyst for technological progress. Insurers, armed with high stock returns, can strategically invest in innovations that revolutionize the industry. From enhanced data analytics to customer-centric digital solutions, these investments create a more efficient, responsive, and competitive health insurance landscape, ultimately benefiting both providers and policyholders.

Understanding Medical Insurance Premiums: What's the Cost of Coverage?

You may want to see also

Frequently asked questions

The stock market influences health insurance premiums indirectly through its effect on the economy. When the stock market performs well, it often indicates a strong economy, which can lead to higher healthcare costs due to increased demand and inflation. Insurers may raise premiums to cover these rising expenses. Conversely, a poor-performing market may lead to lower premiums as economic uncertainty reduces healthcare utilization.

Yes, stock market volatility can impact the health insurance marketplace by influencing insurer profitability and investment strategies. Insurers often invest premiums in the stock market to generate returns. During periods of high volatility, insurers may face financial uncertainty, leading them to reduce the number of plans offered or exit certain markets to mitigate risks.

The stock market affects employer-sponsored health insurance through its impact on corporate finances. When the market performs well, companies may have more resources to allocate to employee benefits, including health insurance. Conversely, during market downturns, employers may cut costs by reducing health insurance contributions or shifting more expenses to employees, potentially decreasing coverage quality or accessibility.