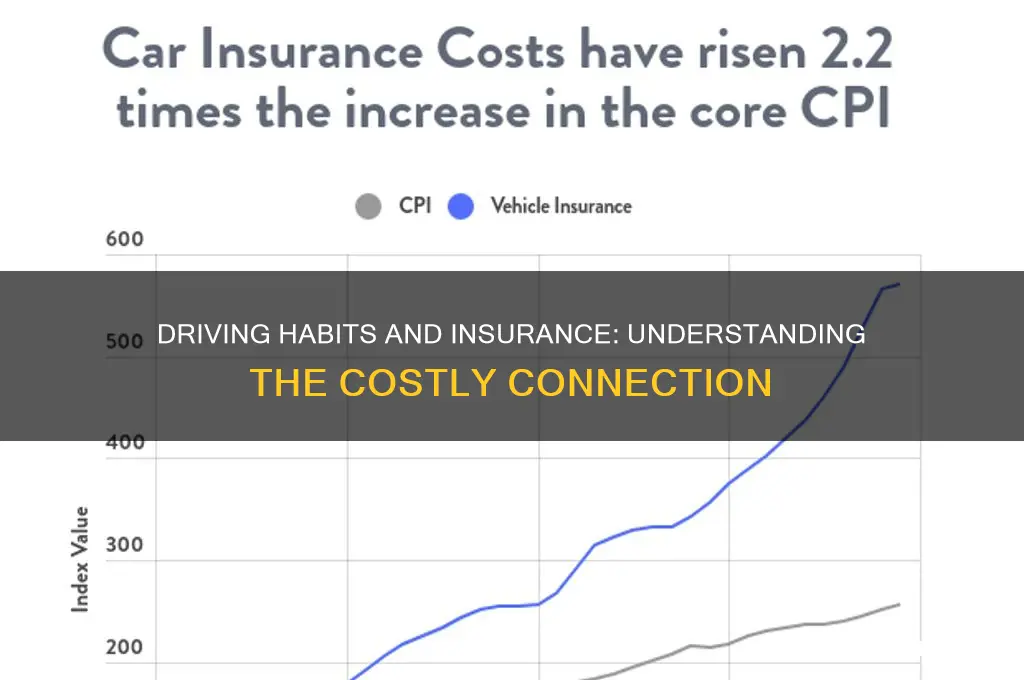

Driving behavior plays a pivotal role in determining insurance premiums and coverage, as insurers rely heavily on data related to a driver's habits to assess risk. Factors such as speed, braking patterns, mileage, and adherence to traffic laws are closely monitored through telematics devices or mobile apps, allowing companies to offer personalized rates. Safe driving behaviors, such as maintaining consistent speeds and avoiding sudden stops, can lead to lower premiums and discounts, while reckless habits like speeding or frequent hard braking may result in higher costs or even policy cancellations. Additionally, driving behavior data helps insurers identify high-risk individuals, encouraging safer practices on the road and reducing accident rates. Ultimately, understanding this connection empowers drivers to make informed choices that can positively impact their insurance expenses and overall road safety.

Explore related products

What You'll Learn

- Aggressive Driving: Speeding, sudden braking, and rapid acceleration increase accident risk, raising insurance premiums significantly

- Mileage Impact: Higher annual mileage correlates with greater accident likelihood, leading to higher insurance costs

- Time of Day: Nighttime driving increases accident risk, often resulting in higher insurance rates for frequent night drivers

- Distracted Driving: Phone use or multitasking while driving boosts accident chances, impacting insurance premiums negatively

- Claims History: Frequent claims due to poor driving behavior lead to higher premiums and policy restrictions

![]()

Aggressive Driving: Speeding, sudden braking, and rapid acceleration increase accident risk, raising insurance premiums significantly

Aggressive driving behaviors such as speeding, sudden braking, and rapid acceleration are red flags for insurance companies. These actions significantly increase the likelihood of accidents, which directly translates to higher claims and financial risk for insurers. Studies show that speeding alone contributes to nearly one-third of all fatal crashes in the U.S., making it a critical factor in premium calculations. When insurers detect these behaviors through telematics or driving records, they adjust rates accordingly, often resulting in premiums that are 20–50% higher than those for safer drivers.

Consider the mechanics of aggressive driving: rapid acceleration and sudden braking put excessive strain on a vehicle’s systems, increasing wear and tear on brakes, tires, and engines. This not only elevates maintenance costs but also raises the risk of mechanical failure, which can lead to accidents. For instance, a driver who brakes suddenly at 60 mph experiences a force equivalent to crashing into a wall at 10 mph. Over time, such habits create a profile of high-risk behavior that insurers penalize with steeper premiums.

From a practical standpoint, drivers can mitigate these risks by adopting smoother driving techniques. Maintaining a consistent speed within the limit, anticipating traffic flow to avoid sudden stops, and accelerating gradually can reduce accident risk by up to 40%. Telematics programs, offered by many insurers, provide real-time feedback on driving habits and can lead to discounts of 10–30% for safe drivers. For example, a 35-year-old driver in California could save $300–$500 annually by improving their driving behavior based on telematics data.

The financial impact of aggressive driving extends beyond premiums. Accidents resulting from speeding or erratic maneuvers often lead to higher out-of-pocket costs due to deductibles, increased liability, and potential legal fees. A single at-fault accident caused by aggressive driving can raise premiums by $500–$1,000 per year for three to five years. For younger drivers (ages 16–25), who already face higher premiums, such incidents can double or triple their insurance costs.

In conclusion, aggressive driving is a costly habit that insurers penalize heavily. By understanding the direct link between speeding, sudden braking, and rapid acceleration and their impact on accident risk, drivers can take proactive steps to improve their behavior. Not only does this make roads safer, but it also leads to substantial savings on insurance premiums. Small changes in driving style can yield significant long-term benefits, both financially and in terms of personal safety.

Teen Driver Insurance: Is It Mandatory for Your 15-Year-Old?

You may want to see also

Explore related products

![]()

Mileage Impact: Higher annual mileage correlates with greater accident likelihood, leading to higher insurance costs

The more miles you drive annually, the higher your risk of being involved in an accident. This isn't just a hunch—it's a statistical reality backed by insurance companies and traffic safety studies. For every 1,000 miles driven, the average driver faces a 1% increase in accident probability. That might seem small, but consider a driver logging 20,000 miles a year compared to one driving 10,000. The higher-mileage driver statistically doubles their accident risk, a fact insurers factor into premiums.

This correlation isn’t arbitrary. Longer time on the road means more exposure to unpredictable variables: erratic drivers, adverse weather, and road hazards. Fatigue also plays a role, as extended driving sessions impair reaction times. A study by the National Highway Traffic Safety Administration found that drivers who travel over 15,000 miles annually are 25% more likely to report drowsy driving incidents. Insurers use this data to justify higher rates for high-mileage drivers, often charging up to 20% more for those exceeding 12,000 miles per year.

To mitigate these costs, consider practical adjustments. If possible, reduce non-essential trips or carpool to lower annual mileage. Telecommuting even one day a week can cut yearly mileage by 2,000 miles, potentially shaving hundreds off your premium. Some insurers offer pay-per-mile policies, ideal for drivers under 10,000 miles annually. Additionally, maintaining a clean driving record becomes even more critical for high-mileage drivers, as violations compound insurance costs exponentially.

Comparatively, low-mileage drivers often enjoy discounts, but this doesn’t mean they’re immune to accidents. The key difference lies in exposure. A driver with 5,000 annual miles might still crash due to distracted driving, but their overall risk remains lower than someone driving 25,000 miles. Insurers balance this by offering usage-based programs that monitor not just mileage but also driving habits, rewarding safe behavior regardless of distance traveled.

Ultimately, understanding the mileage-risk link empowers drivers to make informed choices. While you can’t control every variable on the road, you can control how much you drive. For high-mileage drivers, this might mean reevaluating commute options or negotiating policy terms. For everyone, it’s a reminder that every mile matters—not just for wear and tear on your vehicle, but for your wallet and safety too.

Does Insurance Cover CBT? Understanding Therapy Coverage and Costs

You may want to see also

Explore related products

![]()

Time of Day: Nighttime driving increases accident risk, often resulting in higher insurance rates for frequent night drivers

Nighttime driving presents a unique set of challenges that significantly elevate accident risks. Reduced visibility, fatigue, and a higher likelihood of encountering impaired drivers are key factors. Statistics show that while only a quarter of driving occurs at night, over half of traffic fatalities happen during these hours. This disparity underscores the heightened danger and explains why insurers often scrutinize driving habits during these times.

For insurers, nighttime driving frequency is a critical data point in assessing risk. Telematics and usage-based insurance programs track when and how often policyholders drive at night, adjusting premiums accordingly. For instance, a driver who logs 50% of their miles between 10 PM and 6 AM might see rates increase by 10-20%, depending on their overall driving record. This pricing reflects the actuarial reality: more nighttime driving equals greater exposure to risk.

To mitigate higher premiums, drivers can adopt specific strategies. Limiting nighttime trips, especially on weekends when impaired driving peaks, is one approach. Installing advanced safety features like adaptive headlights or lane-keeping assist can also offset risks, potentially earning discounts from insurers. Younger drivers, aged 16-25, should be particularly mindful, as their inexperience combined with nighttime driving can lead to even steeper rate increases.

Comparatively, daytime drivers benefit from lower accident rates and reduced insurance costs. However, for those whose schedules necessitate nighttime travel, understanding these dynamics is crucial. By balancing necessity with risk awareness—such as avoiding rural roads with poor lighting or planning routes with well-lit highways—drivers can minimize their exposure. Ultimately, while nighttime driving may be unavoidable for some, its impact on insurance rates is a tangible reminder of the risks involved.

Urine Tests: Why Life Insurance Requires Multiple Samples

You may want to see also

Explore related products

![]()

Distracted Driving: Phone use or multitasking while driving boosts accident chances, impacting insurance premiums negatively

Distracted driving, particularly phone use or multitasking behind the wheel, significantly increases the likelihood of accidents. Studies show that texting while driving makes a crash up to 23 times more likely, while even hands-free phone conversations can impair focus as much as having a blood alcohol level of 0.08%. These behaviors not only endanger lives but also trigger a chain reaction of consequences, with insurance premiums being a direct and costly result. Insurers rely on data-driven risk assessments, and distracted driving flags policyholders as high-risk, leading to rate hikes that can range from 20% to 40% or more, depending on the severity and frequency of violations.

Consider the mechanics of how insurers respond to distracted driving incidents. A single ticket for texting while driving can remain on your record for three to five years, during which time your premiums may stay elevated. Worse, if an accident occurs, the financial impact compounds. Claims related to distracted driving can lead to surcharges that persist for up to seven years, and in some cases, insurers may even drop coverage for repeat offenders. For young drivers aged 16–24, who are already in a high-risk category, distracted driving can make insurance nearly unaffordable, with premiums sometimes doubling after a single incident.

To mitigate these risks, practical steps can be taken. First, enable "Do Not Disturb" mode on your phone while driving, or use apps like Life360 or TrueMotion that reward safe driving habits. Second, pre-program navigation and music before starting your trip, and pull over if you need to respond to a message or call. Third, educate teen drivers about the long-term financial consequences of distracted driving, emphasizing that a single mistake can affect their insurance rates for years. Finally, consider telematics-based insurance programs, which monitor driving behavior and offer discounts for safe practices, effectively turning good habits into tangible savings.

Comparing distracted driving to other risky behaviors highlights its unique insurance implications. Speeding or running red lights typically result in fines and points on your license, but distracted driving, especially involving phones, is increasingly treated as a severe offense due to its proven link to fatal accidents. In states with strict hands-free laws, violations can lead to higher penalties and more significant insurance increases. For instance, in California, a first-time offense for using a handheld phone while driving results in a $20 base fine, but with added fees, the total cost exceeds $150—not including the insurance hike. This underscores the importance of treating phone use while driving as a non-negotiable safety issue.

Ultimately, the takeaway is clear: distracted driving is not just a momentary lapse in judgment but a decision with lasting financial repercussions. By understanding how insurers view and penalize this behavior, drivers can make informed choices to protect both their safety and their wallets. Small changes, like silencing notifications or designating a passenger to handle calls, can yield significant benefits, reducing accident risks and keeping insurance premiums in check. In the high-stakes game of auto insurance, avoiding distractions isn’t just smart—it’s essential.

Does T-Mobile Offer Insurance? Coverage, Costs, and Benefits Explained

You may want to see also

Explore related products

![]()

Claims History: Frequent claims due to poor driving behavior lead to higher premiums and policy restrictions

Insurance companies are keen observers of driving patterns, and one of the most critical factors they scrutinize is your claims history. A single claim might not raise alarms, but a pattern of frequent claims can significantly impact your insurance premiums and policy terms. This is because insurers view multiple claims as a red flag, indicating a higher risk of future incidents, especially if they stem from poor driving behavior. For instance, repeated claims for at-fault accidents, speeding-related damages, or reckless driving incidents suggest a driver who may not prioritize safety, leading insurers to adjust their risk assessment accordingly.

Consider this scenario: a driver files three claims within two years for collisions caused by distracted driving. The first claim might result in a modest premium increase, but by the third claim, the insurer is likely to classify the driver as high-risk. This classification often leads to substantial premium hikes, sometimes doubling or tripling the original cost. Additionally, insurers may impose policy restrictions, such as limiting coverage options or requiring the driver to purchase a high-risk insurance policy, which is typically more expensive and less flexible. These measures are designed to mitigate the financial risk the insurer assumes by covering a driver with a history of frequent claims.

From an analytical perspective, the relationship between claims history and insurance premiums is straightforward: higher claims frequency correlates with increased risk, which insurers offset through higher costs. However, this system also serves as a behavioral incentive. Drivers who understand the financial consequences of frequent claims are more likely to adopt safer driving habits. For example, a study by the Insurance Information Institute found that drivers who reduced their claims frequency by improving their driving behavior saw an average premium decrease of 15% within two years. This highlights the tangible benefits of responsible driving beyond just avoiding accidents.

To avoid falling into the high-risk category, drivers should focus on minimizing claims by addressing the root causes of poor driving behavior. Practical steps include enrolling in defensive driving courses, which can reduce premiums by up to 10% in some states, and using telematics programs that monitor driving habits and offer discounts for safe behavior. For younger drivers, who statistically file more claims, parents can encourage participation in graduated licensing programs that gradually increase driving privileges as skills improve. Additionally, maintaining a claim-free record for three to five years can lead to significant premium reductions, as insurers reward demonstrated responsibility.

In conclusion, frequent claims due to poor driving behavior are not just costly in the short term but can have long-lasting financial implications. By understanding how insurers interpret claims history, drivers can take proactive steps to improve their habits and maintain affordable coverage. The key takeaway is clear: safe driving isn’t just about avoiding accidents—it’s about protecting your financial health and ensuring access to favorable insurance terms.

Universal Life Insurance: Indexing for a Secure Future

You may want to see also

Frequently asked questions

Your driving behavior directly impacts your insurance rates through factors like speeding tickets, accidents, and claims history. Safe driving typically results in lower premiums, while risky behavior (e.g., frequent violations or at-fault accidents) can lead to higher costs.

Yes, many insurers offer usage-based insurance programs that monitor driving habits (e.g., speed, braking, and mileage). If you demonstrate safe driving behavior, you may qualify for discounts or lower rates.

Yes, a history of poor driving behavior (e.g., multiple DUIs, reckless driving, or frequent accidents) can make it harder to obtain coverage or result in being labeled a high-risk driver, which often comes with higher premiums or limited policy options.